북미의 위성 발사체 시장(2025-2030년) : 시장 점유율 분석, 산업 동향, 성장 예측

North America Satellite Launch Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693952

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

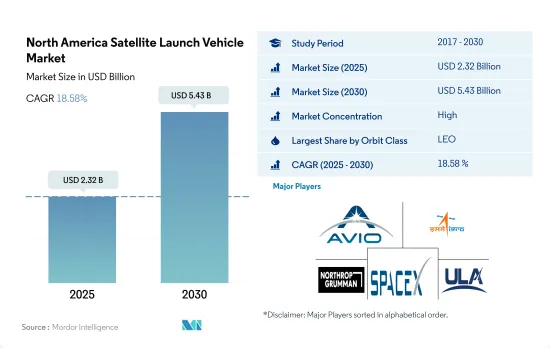

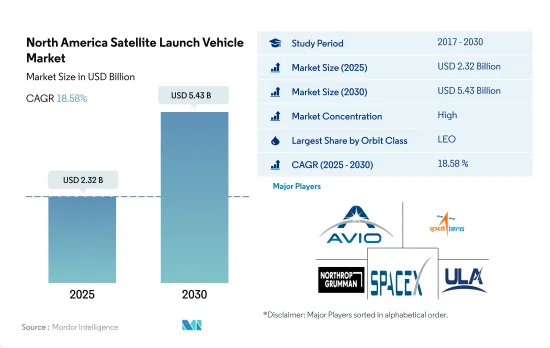

북미 위성 발사체 시장 규모는 2025년에 23억 2,000만 달러로 추정되고, 2030년에는 54억 3,000만 달러에 이를 전망이며 예측 기간(2025-2030년) 동안 CAGR 18.58%를 보일 것으로 예측됩니다.

북미의 위성 발사체 시스템 수요 증가가 성장을 뒷받침함

위성과 우주선은 발사 후 주로 지구를 도는 많은 특별한 궤도 중 하나에 배치됩니다. 각 궤도는 거리별로 고유의 이점과 과제가 있습니다.

조사 지역에서 제조 및 발사할 수 있는 위성은 각각 용도가 다릅니다. GEO 궤도의 위성 32기 중 대부분이 통신과 지구 관측의 목적으로 배치되었습니다.

전자 정보, 지구과학/기상학, 레이저 화상, 전자 정보, 광학 화상 등의 부문으로 위성의 이용이 확대되고 있기 때문에 북미의 위성 발사체 시장 수요는 확대하고 있으며 LEO 위성이 큰 점유율을 차지할 것으로 예상되고 있습니다.

저비용 발사 시스템에 대한 수요 증가가 시장을 견인

무거운 위성을 일년에 수회, 고고도 궤도에 보낼 수 있는 저비용 발사 시스템에 대한 수요가 북미 정부와 상업 조직 사이에서 높아지고 있습니다.

게다가 위성 제조 산업은 군사 모니터링, 통신, 네비게이션에서 지구 관측에 이르기까지 다양한 용도의 위성 수요에 의해 견인되고 있습니다. 과거 이 지역에서는 합계 4,351기의 위성이 발사되었습니다.

우주 기관과 비공개 회사는 최근 몇 년 동안 위성 발사 시스템의 비용을 절감하기 위해 노력해 왔습니다. SpaceX와 Blue Origin 등의 비공개회사가 우주기술에 투자하여 산업 이노베이션을 추진하고 있습니다.

북미 위성 발사체 시장 동향

북미 발사체 시장 수요 증가와 경쟁

북미의 발사체 수요는 주로 정부기관, 상업 위성 사업자, 다양한 미션을 실시하기 위해 우주에의 접근을 필요로 하는 과학 연구자의 요구에 의해 발생하고 있습니다. 또한, 우주 탐사의 비공개화가 진행되는 가운데, 재사용 가능한 로켓이나 3D 프린팅 등의 기술을 통해 기업이 우주에서 신기술을 개발 및 전개할 수 있는 비용 효율적이고 신뢰성 높은 발사 서비스에 대한 수요가 높아지고 있습니다.

그 중에서도 발사체를 보유하는 주요 기업 SpaceX는 선진적인 로켓과 우주선을 설계, 제조, 발사하는 비공개 항공우주 회사입니다. 이 회사의 발사체에는 Falcon-9, Falcon Heavy, Starship 등이 있습니다. United Launch Alliance는 아틀라스 V와 델타 IV 로켓을 운용하고 있습니다. Northrop Grumman은 국제 우주 정거장에서 보급 미션에 사용되는 Antares 로켓을 운용하고 있습니다.

북미 위성 발사체 시장의 투자 기회

연구와 투자 환경의 조성은 북미의 위성 발사체 시장의 혁신과 성장의 주요 추진력이 되고 있습니다. 북미에서는 우주 계획에 대한 정부 지출이 2022년에 약 248억 달러로 역대 최고치를 기록했습니다. NASA는 연구조성금으로 3억 3,300만 달러를 분배했습니다.

캐나다 우주국(CSA)의 예산은 적정 수준이며 2022-2023년의 예산 지출 전망액은 3억 2,900만 달러였습니다. 캐나다 정부는 AstroSat 데이터 프로젝트를 지원하기 위해 캐나다 대학에 총 1억 3,283만 달러의 3종류의 보조금을 지급하였습니다. NASA는 2022-2027 회계연도 동안 발사체 개발을 위해 138억 달러를 지원받을 전망입니다. 해당 투자는 승무원과 대량의 화물을 수송하기 위한 대형 발사체의 개발을 지속하기 위해서 행해지고 있습니다.

북미 위성 발사체 산업 개요

북미 위성 발사체 시장은 상당히 통합되어 있으며 상위 5개 기업에서 97.58%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

위성의 소형화

발사체 소유자

우주 개발에의 지출

규제 프레임워크

캐나다

미국

밸류체인과 유통채널 분석

제5장 시장 세분화

궤도 클래스

GEO

LEO

MEO

로켓

대형

소형

중형

발사국

미국

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Ariane Group

Avio

Indian Space Research Organisation(ISRO)

Mitsubishi Heavy Industries

Northrop Grumman Corporation

Rocket Lab USA, Inc.

Space Exploration Technologies Corp.

The Boeing Company

United Launch Alliance, LLC.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

CSM

영문 목차

영문목차

The North America Satellite Launch Vehicle Market size is estimated at 2.32 billion USD in 2025, and is expected to reach 5.43 billion USD by 2030, growing at a CAGR of 18.58% during the forecast period (2025-2030).

Rising demand for orbital launch systems in the North American region has supplemented the growth

At launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. Satellites orbit the Earth at varying distances depending on their design and primary purpose. Each distance has its own benefits and challenges, including increased coverage and decreased energy efficiency. Satellites in the Medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most scientific satellites, including NASA's Earth Observation System team, are in the low Earth orbit.

Different satellites manufactured and launched from this region have different applications. For instance, during 2017-2022, out of the seven satellites launched in the MEO orbit, most were built for navigation/global positioning purposes. Similarly, out of the 32 satellites in the GEO orbit, most were deployed for communication and earth observation purposes. Around 3,000 LEO satellites launched were owned by North American organizations.

The growing use of satellites in areas such as electronic intelligence, Earth science/meteorology, laser imaging, electronic intelligence, optical imaging, and meteorology is expected to drive demand for the North American satellite launch vehicle market, with LEO satellites expected to account for a major share. Between 2023 and 2029, the market is expected to surge by 213%.

Rising demand for low-cost launch systems driving the market

The demand for low-cost launch systems capable of sending heavy satellites into high-altitude orbits several times a year is growing among governments and commercial organizations in North America. Due to the growing number of small satellite launches, including ride-hailing services on medium and heavy-duty launchers, as well as the growth of small launch capacities, launch prices have decreased Y-o-Y.

In addition, the satellite manufacturing industry is driven by the demand for satellites for applications ranging from military surveillance, communications, and navigation to earth observation. As a result, the demand for satellites from the civilian/government, commercial, and military industries is increasing. During the historical period, a total of 4,351 satellites were launched in the region. The growth in the number of satellites launched from 2021 to 2022 was 61%, while the growth from 2021 to 2020 was 40%.

Space agencies and private companies have been trying to reduce the costs of satellite launching systems over the past few years. Many market players have invested in the development of reusable launch systems to recover some or all the component stages. The market is dominated by only a few players due to their huge product offerings. Private companies such as SpaceX and Blue Origin are investing in space technology and driving innovation in the industry. Space organizations such as NASA have partnered with private players like SpaceX for the production and launch of satellites in this region. The market is expected to surge by 219% in the forecast period, and the United States is expected to be the largest country-wise market.

North America Satellite Launch Vehicle Market Trends

Growing demand and competition in the North American launch vehicle market

The demand for launch vehicles in North America is primarily driven by the requirements of government agencies, commercial satellite operators, and scientific researchers who require access to space to conduct a variety of missions. There is growing interest in commercial space exploration and tourism, which has created a new market for launch providers. Additionally, with the increasing privatization of space exploration, there is a growing demand for cost-effective and reliable launch services that enable companies to develop and deploy new technologies in space, such as reusable rockets and 3D printing. There are several companies that own and operate launch vehicles in North America.

Among them, a major owner of launch vehicles, SpaceX, is a private aerospace company that designs, manufactures, and launches advanced rockets and spacecraft. It is currently the leading provider of launch services in North America and has conducted numerous successful missions for both commercial and government customers. The company's launch vehicles include Falcon-9, Falcon Heavy, and Starship. It is followed by United Launch Alliance, which develops reliable, cost-effective access to space for government and commercial customers. It operates the Atlas V and Delta IV rockets. Blue Origin is also developing a variety of launch vehicles, including the New Shepard suborbital vehicle and the New Glenn orbital rocket. Northrop Grumman is a global aerospace and defense technology company that operates the Antares rocket, which is used for resupply missions to the International Space Station. Rocket Lab specializes in small satellite launches. It operates the Electron rocket, which is designed to provide frequent and affordable access to space for small payloads.

Investment opportunities in the North American satellite launch vehicle market

The grant of research and investments has been a major driver of innovations and growth in the satellite launch vehicle market in North America. It has helped fund the development of new technologies, such as reusable launch vehicles, which have the potential to significantly reduce the cost of satellite launches. In terms of research and investment grants, the region's governments and the private sector have dedicated funds for research and innovation in the space industry. In North America, government expenditure for space programs hit a record of approximately USD 24.8 billion in 2022. For instance, till February 2023, NASA distributed USD 333 million as research grants. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender in the space industry in the world.

The Canadian Space Agency's (CSA) budget was modest, and its estimated budgetary spending for 2022-23 was USD 329 million. In April 2022, three grants totaling USD1 32,831 were awarded to Canadian universities to support projects that use data collected by AstroSat to understand how stars are formed. In terms of funds allocated for launch vehicle development, under the FY 2023 President'S Budget Request Summary from FY 2022-FY 2027, NASA was expected to receive USD 13.8 billion. NASA was also expected to receive USD 500 million for the SLS Program Integration and Support during the same period. These investments are being made as NASA continues the development of a heavy-lift launch vehicle to deliver crew and large volumes of cargo to deep space. The Space Launch System (SLS) program is preparing to carry humans farther into deep space than ever before.

North America Satellite Launch Vehicle Industry Overview

The North America Satellite Launch Vehicle Market is fairly consolidated, with the top five companies occupying 97.58%. The major players in this market are Avio, Indian Space Research Organisation (ISRO), Northrop Grumman Corporation, Space Exploration Technologies Corp. and United Launch Alliance, LLC. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Satellite Miniaturization

4.2 Owner Of Launch Vehicle

4.3 Spending On Space Programs

4.4 Regulatory Framework

4.4.1 Canada

4.4.2 United States

4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Orbit Class

5.1.1 GEO

5.1.2 LEO

5.1.3 MEO

5.2 Launch Vehicle Mtow

5.2.1 Heavy

5.2.2 Light

5.2.3 Medium

5.3 Country

5.3.1 United States

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).