ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

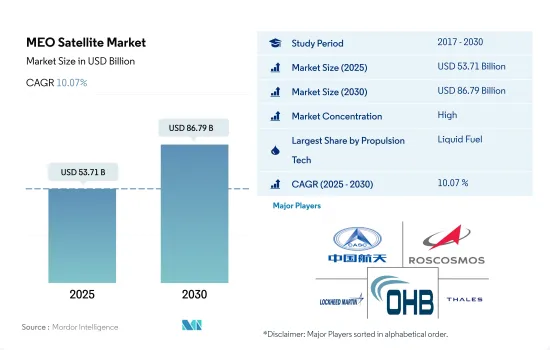

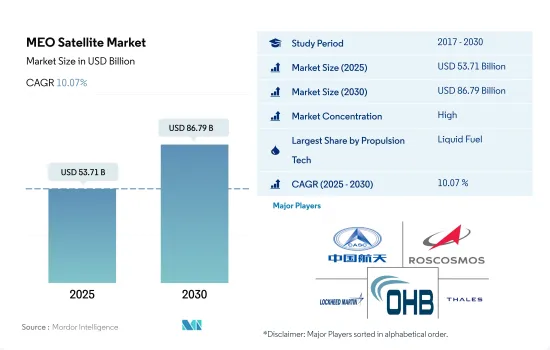

MEO 위성 시장 규모는 2025년에 537억 1,000만 달러로 예측되고, 2030년에는 867억 9,000만 달러에 이를 전망이며 예측 기간(2025-2030년) 동안 CAGR 10.07%로 성장할 것으로 예측됩니다.

액체 연료 추진 시스템 부문이 시장 성장을 견인

위성 추진 시스템은 우주선을 궤도로 추진하고 궤도에서 우주선의 위치를 조정하는 데 일반적으로 사용됩니다. 가스 추진제를 사용할 수 있으나 낮은 밀도와 기존 펌프 방식을 적용하기가 어려운 단점으로 널리 사용되지는 않습니다. 액체 연료 추진 시스템은 밀도와 비추력이 높기 때문에 3가지 추진 유형 중에서 가장 많이 채용되고 있습니다.

전기 추진은 2번째로 많이 채용되고 있는 추진 시스템으로, 상업 통신 위성의 스테이션 유지에 일반적으로 사용되고 있습니다. 전기 추진은 높은 비추력에 의해 일부의 우주 과학 미션에서 주추진력으로 사용되고 있습니다. Northrop Grumman Corporation, Moog Inc., Sierra Nevada Corporation, SpaceX, Blue Origin 등이 추진 시스템의 주요 제공 기업입니다.

이동을 가능하게 하는 가스 추진 시스템은 효율성과 신뢰성 면에서 입증 받았습니다. 그러므로 총 추력 용량이 미션 요구 사항을 충족하기에 충분한 경우에는 가스 시스템이 우주 추진 기술로 지속 선택되는 경우도 있습니다.

유럽에서는 상당한 신제품 개발로 새로운 비즈니스 기회가 확산될 것으로 기대되고 있습니다.

중궤도(MEO) 위성의 연구 개발비는 위성산업에 있어서의 기술 혁신과 기술 개발을 촉진하는 중요한 요인입니다.

러시아의 위성 산업은 세계에서 가장 활발하고 선진적인 산업 중 하나입니다. ISS Reshetnev는 러시아의 MEO 인공위성 시장을 독점하고 있습니다. GLONASS 시스템은 미국의 GPS 시스템에 대항하는 러시아 시스템으로 세계 사용자에게 범지구적 측위 서비스를 제공합니다.

중국은 이니셔티브의 일환으로 이미 많은 MEO 위성을 발사하고 있으며, 향후 수년간 더 많은 위성을 발사할 것으로 예상되고 있습니다. 정부 및 군사 목적으로 각각 800kg 중량의 네비게이션 위성 24기와 범지구적 측위 위성이 MEO에 배치되었습니다. 이 위성들은 BeiDou Navigation Satellite System(BDS)의 일부로 중국의 우주기술연구원(CASC의 일부)에 의해 발사되었습니다.

세계의 MEO 위성 시장 동향

연료 효율과 운영 효율 향상을 위한 위성 소형화가 시장에서 대두하고 있습니다.

MEO 위성은 LEO와 GEO의 중간에 위치하며, 통상 약 2,000-3만 6,000km(1,242-2만2,369마일)의 고도에 있습니다.

위성의 질량은 발사에 큰 영향을 미칩니다. 위성이 무거울수록 우주로 발사하는데 필요한 연료와 에너지가 늘어나기 때문입니다.

위성의 질량은 발사에 큰 영향을 미칩니다. 실제로 위성이 무거울수록 우주에 발사하는 데 필요한 연료와 에너지가 많아집니다. 발사 속도를 달성하는 데 필요한 에너지량은 위성의 질량에 비례합니다. 소재 및 제조 기술의 발전으로 보다 경량이며 효율적인 위성 부품의 개발이 가능하게 되었습니다. 그 결과, 위성의 성능을 유지 혹은 향상시키면서 위성의 질량을 줄일 수 있게 되었습니다.

다양한 우주 기관에 의한 지출 증가는 MEO 위성 부문에 긍정적인 영향을 미칠 것으로 예측됩니다.

MEO 위성에 대한 연구 개발비의 세계 동향은 LEO 위성이나 GEO 위성의 동향만큼 명확하지는 않습니다. 유럽에서는 MEO 위성의 용도가 한정적입니다. 영국 우주청은 이 나라의 우주 산업을 뒷받침하는 18개의 프로젝트를 지원하기 위해 650만 유로의 자금을 제공한다고 발표했습니다. 지역 주도 계획과 우주 클러스터 개발 매니저를 지원함으로써 영국 우주 산업의 성장을 자극하는 것을 목표로 하고 있습니다. 데이터 활용 등 지역 문제에 대처하기 위한 다양한 혁신적 우주 기술을 개척할 예정입니다.

북미에서는 우주 계획을 위한 정부 지출이 2021년에 약 220억 달러로 역대 최고를 기록했습니다. 미국 정부는 우주 프로그램에 약 620억 달러를 지출하여 세계적으로 우주 개발에 대한 지출액이 가장 높은 국가가 되었습니다.

MEO 위성의 연구 개발비는 특정 용도와 이용 가능한 자금에 따라 다소 불규칙해질 수 있습니다.

MEO 위성 산업 개요

MEO 위성 시장은 상당히 통합되어 있으며 상위 5개 기업이 100%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

위성의 질량

우주 개발에의 지출

규제 프레임워크

세계

호주

브라질

캐나다

중국

프랑스

독일

인도

이란

일본

뉴질랜드

러시아

싱가포르

한국

아랍에미리트(UAE)

영국

미국

밸류체인과 유통채널 분석

제5장 시장 세분화

용도

통신

지구 관측

네비게이션

기타

위성 질량

100-500kg

500-1,000kg

1,000kg 이상

최종 사용자

상업

군사 및 정부

기타

추진 기술

전기

가스

액체 연료

지역

아시아태평양

유럽

북미

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

China Aerospace Science and Technology Corporation(CASC)

Information Satellite Systems Reshetnev

Lockheed Martin Corporation

OHB SE

Thales

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

CSM

영문 목차

영문목차

The MEO Satellite Market size is estimated at 53.71 billion USD in 2025, and is expected to reach 86.79 billion USD by 2030, growing at a CAGR of 10.07% during the forecast period (2025-2030).

The liquid fuel propulsion system segment leads the market's growth

A satellite's propulsion system is commonly used to propel a spacecraft into orbit and to coordinate the position of the spacecraft in orbit. Liquid propellants or liquid rockets use rocket engines that use liquid propellants. Gas propellants can also be used but are not common due to their low density and difficulty in applying conventional pumping methods. The liquid fuel propulsion system is the most adopted one of the three propulsion types because of its high density and specific impulse. It is expected to occupy a market share of 73.3% in 2023, which is anticipated to reach 69.5% in 2029.

Electric propulsion is the second most adopted type of propulsion system, and it is commonly used to hold stations for commercial communication satellites. It is the main propulsion of some space science missions due to its high specific impulses. Northrop Grumman Corporation, Moog Inc., Sierra Nevada Corporation, SpaceX, and Blue Origin are some of the major providers of propulsion systems. The new launch of satellites is expected to accelerate market growth over the forecast period.

Gas-based propulsion systems that enable movements have been proven efficient and reliable. These include hydrazine systems, other single or twin propulsion systems, hybrid systems, cold/hot air systems, and solid propellants. Typically, these systems are used when strong thrust or rapid maneuvering is required. Therefore, in some cases, gas-based systems continue to be the space propulsion technology of choice when their total impulse capacity is sufficient to meet the mission requirements. Cold gas thrusters are suitable for small satellites because of their low cost and complexity, but they are not ideal for large satellites.

Europe is expected to open new scope of opportunities with significant new product developments in the region

R&D expenditure on medium Earth orbit (MEO) satellites is an important factor in driving innovation and technology development in the satellite industry. MEO satellites are often used for specialized applications, such as providing global positioning system (GPS) services. As these applications become more critical to society, there may be more R&D investment to improve MEO satellite performance and capabilities.

The Russian satellite industry is one of the most active and advanced in the world. ISS Reshetnev dominates the MEO satellite market in Russia. ISS Reshetnev is a leading Russian satellite manufacturer responsible for developing and producing most of the country's MEO satellites. ISS Reshetnev's most notable contribution to the MEO satellite market in Russia is its GLONASS series. The GLONASS system is a Russian counterpart to the American GPS system and provides global positioning services to users worldwide. All of these satellites are of the GLONASS series and were manufactured and launched by ISS Reshetnev.

China has already launched a number of MEO satellites as part of this initiative and is expected to launch many more in the coming years. For instance, during 2017-2022*, 24 navigation and global positioning satellites weighing 800 kg each were placed in MEO for government and military purposes. These satellites were launched by China's Space Technology Research Institute (part of CASC) as part of China's BeiDou Navigation Satellite System (BDS), China's global navigation system. The Asia-Pacific region is expected to dominate during the forecast period.

Global MEO Satellite Market Trends

Satellite miniaturization for better fuel and operational efficiency witnessed in the market

MEO satellites are located between LEO and GEO, typically at an altitude of about 2,000 to 36,000 kilometers (1,242 to 22,369 miles). MEO is commonly used for satellite navigation systems such as the Global Positioning System (GPS). The mass of MEO satellites can also vary depending on their specific applications, but they are generally lighter than GEO satellites due to their lower altitude.

The mass of a satellite has a significant impact on its launch. This is because the heavier the satellite, the more fuel and energy will be required to launch it into space. The launch of a satellite involves accelerating it to a very high speed, typically around 28,000 kilometers per hour, in order to place it in orbit around the Earth. The amount of energy required to achieve this speed is proportional to the mass of the satellite.

The mass of a satellite has a significant impact on its launch. Indeed, the heavier the satellite, the more fuel and energy it will need to be launched into space. The amount of energy required to achieve this speed is proportional to the mass of the satellite. Advancements in materials, manufacturing techniques, and technology have enabled the development of lighter and more efficient satellite components. This has resulted in a reduction in satellite mass while maintaining or even improving performance. During 2017-2022, around 55 satellites were launched into MEO globally.

Increasing expenditure by different space agencies is expected to positively impact the MEO satellites segment

The global trend in R&D expenditure on MEO satellites is not as well-defined as that for LEO or GEO satellites. This is because MEO satellites are not as widely used as LEO or GEO satellites, and their applications are somewhat limited in Europe. The UK Space Agency announced that it would be funding EUR 6.5 million to support 18 projects to boost its space industry. The funding aims to stimulate growth in the UK space industry by supporting high-impact, locally-led schemes and space cluster development managers. The 18 projects will pioneer various innovative space technologies to combat local issues, such as utilizing Earth observation (EO) data to enhance public services. In November 2022, the Government of Spain announced that it would allocate EUR 1.5 billion to the ESA over the next five years, which will reinforce Spain's leadership in space.

In North America, government expenditure for space programs hit a record of approximately USD 22 billion in 2021. The region is the epicenter of space innovation and research, with the presence of the world's biggest space agency, NASA. In 2022, the US government spent nearly USD 62 billion on its space programs, making it the highest spender on space globally. In the United States, federal agencies receive funds worth USD 32.33 billion from the government every year.

R&D spending on MEO satellites can be somewhat irregular depending on specific applications and available funding. However, as with other satellite technologies, continued investment in R&D will likely lead to the development of new and improved MEO satellite technologies that can support different applications and promote industry growth over the forecast period.

MEO Satellite Industry Overview

The MEO Satellite Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are China Aerospace Science and Technology Corporation (CASC), Information Satellite Systems Reshetnev, Lockheed Martin Corporation, OHB SE and Thales (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Satellite Mass

4.2 Spending On Space Programs

4.3 Regulatory Framework

4.3.1 Global

4.3.2 Australia

4.3.3 Brazil

4.3.4 Canada

4.3.5 China

4.3.6 France

4.3.7 Germany

4.3.8 India

4.3.9 Iran

4.3.10 Japan

4.3.11 New Zealand

4.3.12 Russia

4.3.13 Singapore

4.3.14 South Korea

4.3.15 United Arab Emirates

4.3.16 United Kingdom

4.3.17 United States

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Application

5.1.1 Communication

5.1.2 Earth Observation

5.1.3 Navigation

5.1.4 Others

5.2 Satellite Mass

5.2.1 100-500kg

5.2.2 500-1000kg

5.2.3 above 1000kg

5.3 End User

5.3.1 Commercial

5.3.2 Military & Government

5.3.3 Other

5.4 Propulsion Tech

5.4.1 Electric

5.4.2 Gas based

5.4.3 Liquid Fuel

5.5 Region

5.5.1 Asia-Pacific

5.5.2 Europe

5.5.3 North America

5.5.4 Rest of World

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 China Aerospace Science and Technology Corporation (CASC)