ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

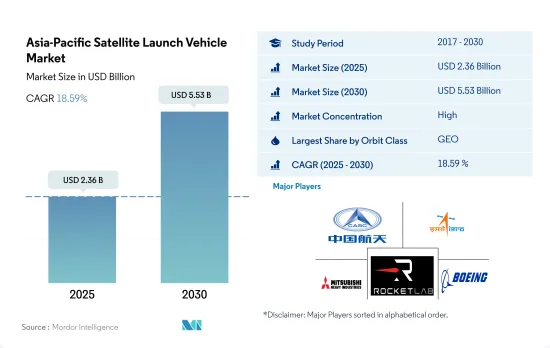

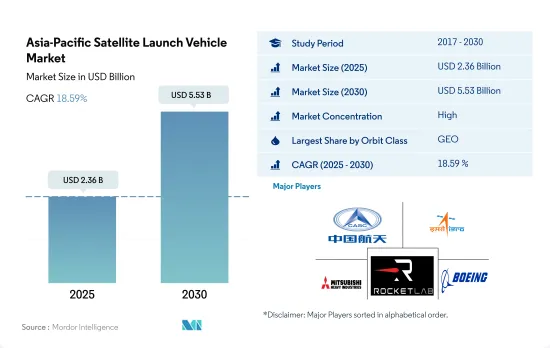

아시아태평양의 위성 발사체 시장 규모는 2025년에는 23억 6,000만 달러로 예측되고, 2030년에는 55억 3,000만 달러에 이를 전망이며 예측 기간(2025-2030년) 동안 CAGR 18.59%를 보일 것으로 예측됩니다.

아시아태평양의 궤도 발사 시스템 수요는 LEO 위성이 견인

아시아태평양에서는 LEO 기반의 궤도 발사 시스템 수요가 증가하고 있습니다. 중국의 장정 로켓 시리즈, 인도의 PSLV와 GSLV, 일본의 H-IIA 로켓과 H3 로켓, 한국의 한국 우주 로켓 II(KSLV-II)는 지구 관측, 원격 감지, 기상 모니터링, 통신 목적의 위성을 LEO에 발사하기 위해 사용되어 왔습니다.

MEO는 GNSS나 위성통신 등의 용도로 적합합니다. 이러한 위성은 중국이 개발한 북두항법위성시스템(BDS)과 같은 위성 기반의 네비게이션 시스템, 원격지 및 농촌 지역을 위한 통신서비스, 해양 및 항공산업, 재해 관리 등의 서비스를 제공하고 있습니다.

GEO에 있는 위성은 지구에 대해 정지하고 있는 것처럼 보이기 때문에 통신, 방송, 기상 관측 등의 용도로 이상적입니다. 중국의 장정 3B/G2, 인도의 GSLV Mk III, 일본의 H3, 한국의 KSLV-II는 통신, 방송, 기상 관측의 목적으로 GEO에 위성을 발사하기 위해서 이용되는 발사 시스템입니다.

중국 위성산업은 크게 성장할 전망

아시아태평양은 최근 위성의 주요 시장으로 대두해 왔습니다.

중국은 압도적인 우주대국이 되기 위해 노력을 기울이고 있습니다.

인도 우주연구기관(ISRO)은 소형 위성 발사체(SSLV)의 개발에 임하고 있습니다. SSLV는 LEO까지 500kg, 태양 동기 궤도까지 300kg의 발사가 가능합니다.

NewSpace India Limited는 인도 우주청이 새로 설립한 상업 부문으로 인도 산업이 인도의 우주 개발을 위한 하이테크 제조 및 생산 거점을 확대할 수 있도록 하는 것을 목표로 하고 있습니다.

한국의 우주개발은 타국이 핵심기술 이전에 소극적이기 때문에 진행이 늦어지고 있습니다.

아시아태평양 위성 발사체 시장 동향

아시아태평양 발사체 시장 수요 증가와 경쟁

아시아태평양은 최근 우주 산업의 동향에서 현저한 성장을 이루고 있으며, 많은 기업이 발사체의 개발 및 배치에 있어서 주요 기업으로서 대두해 왔습니다. 2017-2022년 동안 장정 로켓은 약 372기의 위성을 우주로 발사했습니다.

우주항공연구개발기구(JAXA)는 H-IIA 로켓과 H-IIB 로켓 등 수많은 발사체를 개발해 왔습니다. 2017-2022년에 걸쳐, JAXA의 H-IIA 로켓은 세계의 다양한 위성 사업자를 위해 약 25기의 위성을 우주로 발사했습니다. 인도의 ISRO는 이 나라의 발사체 개발에 중요한 역할을 합니다. ISRO는 PSLV와 GSLV를 포함한 다양한 발사체를 개발하여 다양한 위성 발사에 사용했습니다. 2017-2022년에 걸쳐, ISRO의 발사체는 세계의 다양한 위성 사업자를 위해 약 171기의 위성을 우주로 발사했습니다. 이러한 기존 기업 외에도 뉴질랜드에 본사를 둔 Electron 로켓을 개발한 Rocket Lab과 같은 신흥 기업도 많이 있습니다. 2017-2022년에 걸쳐, Electron 로켓은 세계의 다양한 위성통신 사업자를 위해 약 87개의 위성을 우주로 발사했습니다.

중국, 인도, 일본, 한국의 지출 증가가 시장 성장을 견인

위성 발사체 수요는 최대 1만 3,000기의 위성으로 이루어진 국가 위성 인터넷 별자리의 구축 및 발사 등의 프로젝트가 견인하고 있습니다. SatNet은 Guowang Constellation Building의 청사진을 만들기 위해 민간 기업과 협력하고 있습니다. 인도 정부는 ISRO가 다양한 우주 관련 활동을 위해 20억 달러를 지원받을 것이라고 발표했습니다. 2021년 3월 일본은 우주 관련 활동에 41억 4,000만 달러를 지출했다고 발표했습니다. 2020년 1월, JAXA는 연비를 대폭 개선하여 환경 부하를 저감하는 코어 엔진 기술의 연구 개발, 정숙 초음속기나 제로 배출기(전기 추진 시스템)의 연구 개발에 36억엔을 할당했다고 발표했습니다.

2023년 3월 한국은 국내 우주산업 확대, 차세대 발사체 개발, 우주방위능력 강화를 위해 우주계획에 6억 7,400만 달러를 투입한다고 발표했습니다. 차세대 캐리어 로켓 KSLV-2의 개발에 약 1억 1,360 달러가 투입될 계획입니다.

아시아태평양 위성 발사체 산업 개요

아시아태평양의 위성 발사체 시장은 상당히 통합되어 있으며 상위 5개 기업이 100%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

위성의 소형화

발사체 소유자

우주 개발에의 지출

규제 프레임워크

호주

중국

인도

일본

뉴질랜드

싱가포르

한국

밸류체인과 유통채널 분석

제5장 시장 세분화

궤도 클래스

GEO

LEO

MEO

발사체 Mtow

대형

소형

중형

발사국

중국

인도

뉴질랜드

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Ariane Group

Blue Origin

China Aerospace Science and Technology Corporation(CASC)

Indian Space Research Organisation(ISRO)

Mitsubishi Heavy Industries

Rocket Lab USA, Inc.

Space Exploration Technologies Corp.

The Boeing Company

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

CSM

영문 목차

영문목차

The Asia-Pacific Satellite Launch Vehicle Market size is estimated at 2.36 billion USD in 2025, and is expected to reach 5.53 billion USD by 2030, growing at a CAGR of 18.59% during the forecast period (2025-2030).

The demand for orbital launch systems in Asia-Pacific is driven by LEO satellites

In Asia-Pacific, the demand for LEO-based orbital launch systems has been on the rise. Countries such as China, India, Japan, South Korea, Australia, and Taiwan have been actively developing and utilizing orbital launch systems to deploy satellites into LEO for various applications. For instance, China's Long March series of rockets, India's PSLV and GSLV, Japan's H-IIA and H3 rockets, and South Korea's Korea Space Launch Vehicle-II (KSLV-II) have been used to launch satellites for Earth observation, remote sensing, weather monitoring, and communication purposes in LEO.

MEO is well-suited for applications such as GNSS and satellite-based communications. In the region, China's Long March 3B and Long March 3B/G2 are some of the launch systems being developed or utilized by countries in the region to deploy satellites into MEO. These satellites provide services such as satellite-based navigation systems like the BeiDou Navigation Satellite System (BDS) developed by China, communication services for remote and rural areas, maritime and aviation industries, and disaster management.

GEO is ideal for applications such as telecommunications, broadcasting, and meteorological observations, as satellites in GEO appear to be stationary relative to Earth. China's Long March 3B/G2, India's GSLV Mk III, Japan's H3, and South Korea's KSLV-II are some launch systems utilized for launching satellites into GEO for telecommunications, broadcasting, and meteorological observation purposes. Overall, the market is expected to grow in the coming years by 219% in 2029 compared to 2023.

China's satellite industry is expected to witness significant growth

Asia-Pacific has emerged as a leading market for satellites in recent years. This market is projected to grow rapidly, driven by increasing demand for Earth observation, communication, and scientific research.

China is stepping up to become a dominant space power. Hence, in October 2020, the country unveiled its ambitious moon mission slated for 2024 and beyond. On this note, China planned to launch a mission to collect samples from the far side of the moon by the end of 2020.

The Indian Space Research Organisation (ISRO) is working on its Small Satellite Launch Vehicle (SSLV). The SSLV is a three-stage launch platform powered entirely by solid fuel, with a lift-off mass of 120 metric tons and capable of lifting 500 kg to LEO and 300 kg to the sun-synchronous orbit. The first static fire test of SS1 conducted in March 2021 was unsuccessful. The first demonstration flight was expected to take place in October 2021.

NewSpace India Limited, a newly formed commercial arm of the Indian space agency, is tasked with enabling the Indian industry to scale up high-technology manufacturing and production base for Indian space efforts. It will be involved in the manufacture of SSLV in collaboration with the private sector.

South Korea's space program has seen slow progress as other countries are reluctant to transfer core technologies. In February 2021, the Ministry of Science and ICT announced a space budget of USD 553.1 million for manufacturing satellites, rockets, and other key space equipment. Such initiatives will drive the demand for launch vehicles in Asia-Pacific during the forecast period.

Growing demand and competition in the Asia-Pacific launch vehicle market

Asia-Pacific has witnessed significant growth in the space industry in recent years, with a number of companies emerging as major players in the development and deployment of launch vehicles. CASC developed a range of launch vehicles, including the Long March series, which has become one of the most reliable launch vehicles in the world. During 2017-2022, CASC's Long March rocket launched approximately 372 satellites into space for various satellite operators across the world. Russia's Roscosmos State Corporation is responsible for the development of the Soyuz and Proton rockets, which have been used to launch a range of satellites and crewed missions to space. During 2017-2022, the Soyuz rocket launched approximately 611 satellites into space for various satellite operators across the world.

The Japan Aerospace Exploration Agency (JAXA) has developed a number of launch vehicles, including the H-IIA and H-IIB rockets. During 2017-2022, JAXA's H-IIA rockets launched approximately 25 satellites into space for various satellite operators across the world. India's ISRO is playing a key role in the development of the country's launch vehicles. ISRO has developed a range of launch vehicles, including the PSLV and the GSLV, which have been used to launch a range of satellites. During 2017-2022, ISRO's rockets launched approximately 171 satellites into space for various satellite operators across the world. In addition to these established players, there are also a number of emerging companies, such as Rocket Lab, which is based in New Zealand and has developed the Electron rocket. During 2017-2022, the Electron rocket launched approximately 87 satellites into space for various satellite operators globally.

Increased spending by China, India, Japan, and South Korea is driving the market's growth

The demand for satellite launch vehicles is driven by projects such as manufacturing and launching a national satellite internet constellation of up to 13,000 satellites. China SatNet has been engaging with commercial companies as it develops a blueprint for constructing the Guowang constellation. Hence, several space agencies in the region are developing space launch vehicle technologies. In February 2023, the Indian government announced that ISRO is expected to receive USD 2 billion for various space-related activities. Under the outlay on major schemes, a partial split up of the budget of INR 9441 crore has been allocated for space technology (including launch activity, R&D on rockets, engines, satellites, etc.). In March 2021, Japan announced that it expended USD 4.14 billion for space-related activities. The country mentioned that it had allocated JPY 18.9 billion for the H3 rocket development. In January 2020, JAXA mentioned that JPY 3.6 billion was allocated to fund the research and development of core engine technologies that significantly improve fuel consumption and reduce environmental burden, as well as the research and development of the silent supersonic airplane and emission-free aircraft (electric-powered propulsion systems).

In March 2023, South Korea announced that it would spend USD 674 million on space programs to expand its domestic space industry, develop a next-generation launch vehicle, and bolster space defense capabilities. Approximately USD 113.6 million will be expended on developing a next-generation carrier rocket, the KSLV-2. The new rocket KSLV-3, expected to debut in 2030, is designed to be a kerosene and liquid oxygen-fueled two-stage vehicle.

Asia-Pacific Satellite Launch Vehicle Industry Overview

The Asia-Pacific Satellite Launch Vehicle Market is fairly consolidated, with the top five companies occupying 100%. The major players in this market are China Aerospace Science and Technology Corporation (CASC), Indian Space Research Organisation (ISRO), Mitsubishi Heavy Industries, Rocket Lab USA, Inc. and The Boeing Company (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Satellite Miniaturization

4.2 Owner Of Launch Vehicle

4.3 Spending On Space Programs

4.4 Regulatory Framework

4.4.1 Australia

4.4.2 China

4.4.3 India

4.4.4 Japan

4.4.5 New Zealand

4.4.6 Singapore

4.4.7 South Korea

4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

5.1 Orbit Class

5.1.1 GEO

5.1.2 LEO

5.1.3 MEO

5.2 Launch Vehicle Mtow

5.2.1 Heavy

5.2.2 Light

5.2.3 Medium

5.3 Country

5.3.1 China

5.3.2 India

5.3.3 New Zealand

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 Ariane Group

6.4.2 Blue Origin

6.4.3 China Aerospace Science and Technology Corporation (CASC)