ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

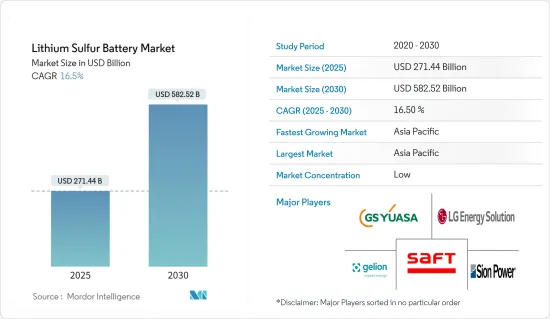

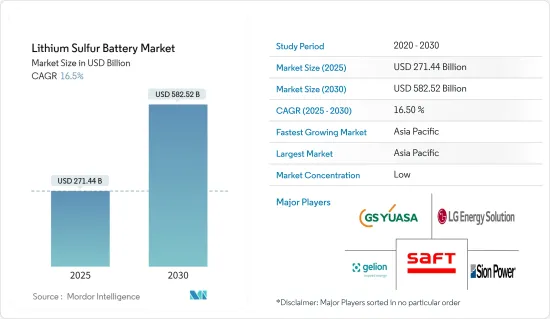

리튬황 배터리 시장 규모는 2025년에 2,714억 4,000만 달러로 추정되며, 예측 기간(2025-2030년) 동안 CAGR 16.5%로 성장하여 2030년에는 5,825억 2,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 배출량 감축을 위한 각국의 지원 시책이나 대처에 의한 전기자동차 수요 증가, 재생 가능 에너지 도입 증가에 수반하는 에너지 저장 장치 수요 증가 등의 요인이 예측 기간 중 시장 성장을 가속합니다.

한편, 리튬황 배터리의 높은 비용이 예측 기간 중 시장 성장을 억제할 가능성이 높습니다.

전지 기술의 진보에 의해 최종 사용자 산업 전체 수요는 극적으로 증가하고 있습니다. 또, 군사 및 항공 부문용의 고에너지밀도 전지를 개발하기 위한 정부 투자도 증가하고 있습니다.

예측 기간 중 아시아태평양이 최대 시장이며 가장 급성장하고 있는 시장이 될 것으로 예상되고 수요의 대부분은 중국, 일본 등의 나라들로부터 발생합니다.

리튬황 배터리 시장 동향

시장을 독점하는 항공우주 부문

항공우주 부문에서는 배터리가 중요한 부품이며, 인공위성, 고고도 항공기, 우주선, 무인 항공기 등 여러 용도로 사용되고 있습니다. 기기에 탑재되거나 주로 휴대용으로 사용되는 기기의 전원으로 사용되는 전지는 안전하며 에너지 밀도가 높고 경량이며 신뢰성이 높고 유지보수가 최소화되어 다양한 환경 조건에서 효율적으로 기능해야 합니다.

항공우주 부문에서는 보다 높은 에너지 밀도를 가지는 전지가 필요하기 때문에 리튬황 배터리의 사용이 증가하고 있습니다. 리튬황 배터리는 보다 긴 수명으로 강력한 에너지 저장을 가능하게 합니다.

미국의 전지 신흥 기업인 라이텐은 에너지 밀도가 높은 리튬황 배터리의 잠재 시장으로서 전기 항공기에 주목하고 있습니다. 라이텐의 리튬황 배터리 파일럿 라인은 방위, 물류, 자동차, 위성의 각 부문의 조기 채용 고객용으로, 2023년부터 상용 전지 셀의 납품을 개시하였습니다.

게다가 이러한 전지를 탑재할 수 있는 드론의 활용이 세계적으로 진행되고 있습니다.

2023년 7월, DroneShield는 한 미국 정부 기관으로부터 3,300만 달러의 계약을 획득했습니다. 이 계약은 복수 개 드론의 제어 및 항행 능력을 방해할 수 있는 DroneGun Mk4등의 기기 공급을 대상으로 하고 있습니다

항공 부문의 성장은 최근 항공 운임의 하락에 의한 세계의 항공 여객수 증가, 경제 상황의 진전, 가처분 소득 증가가 주요인이 되고 있습니다.

코로나바이러스의 대유행으로 국제항공운송협회(IATA)에 따르면 민간항공사는 2022년에 약 7,270억 달러의 수익을 올렸습니다.

위의 요인은 항공우주 부문의 성장을 가속하고 예측 기간 동안 리튬황 전지 수요를 밀어 올릴 가능성이 높습니다.

아시아태평양이 시장을 독점

아시아태평양이 세계의 리튬황 배터리 시장을 독점할 것으로 예측됩니다.

이 지역에서는 지역 전체적으로 깨끗한 전력을 공급하여 조명이나 휴대전화의 충전 요구에 필요한 등유나 디젤 등의 기존 연료에의 의존을 줄이려는 노력이 현저히 일어나고 있습니다.

이 지역 내 이러한 전지 수요는 온그리드와 오프그리드 용도로의 에너지 저장 시스템이나 전기자동차의 채용에 의해 급속히 성장할 것으로 예측됩니다.

게다가 중국 정부는 전기자동차 판매를 촉진하기 위해 전국적인 충전소 건설에 투자하고 있습니다.

충전 인프라의 개발은 이 나라의 EV 보급을 뒷받침하고 있습니다.

일본은 "Well-to-Wheel Zero Emission'이라는 이름의 시책을 확립하는 것을 목표로 하고 있으며, 세계의 배출량 제로 대처와 보조를 맞춰 2050년까지 에너지 공급과 자동차 기술 혁신에 초점을 맞추어 모든 자동차를 EV로 전환하고 승용차 1 대당 약 90%의 배출량 절감을 포함해 승용차 1대 당 약 80%의 온실가스 배출량 감축을 목표로 하고 있습니다.

마찬가지로 한국 정부는 2023년 4월 주요 전지기업 3개사(LG Energy Solution, Samsung SDI, SK on)와 제휴해 고체 전지를 포함한 선진 전지 기술을 개발하기 위해 2030년까지 151억 달러를 공동 투자할 계획을 발표했습니다.

이 이니셔티브에 의해 한국은 세계의 경쟁사보다 앞서 고체 전지의 상업 생산을 개시할 수 있게 됩니다. 참가하는 전지 기업은 한국 내에 파일럿 생산 공장을 설립해, 제품 개발과 제조 기술 혁신의 거점을 구축할 계획입니다. LG Energy Solutions는 2027년까지 리튬황 배터리의 생산을 상업화하는 목표를 설정하였으며 우선은 우주 부문용으로 생산을 개시합니다.

따라서 위의 요인으로부터 예측 기간 동안 아시아태평양이 리튬 유황전지 시장을 독점할 것으로 예측됩니다.

리튬황 배터리 산업 개요

리튬황 배터리 시장은 세분화되어 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간 애널리스트 서포트

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

시장 규모와 수요 예측(-2028년, 단위 : 달러)

최근 동향과 개발

정부의 규제와 시책

시장 역학

성장 촉진요인

전기자동차의 보급 확대

에너지 저장 시스템(ESS) 수요 증가

억제요인

한정된 사이클 수명과 내구성

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

최종 사용자

항공우주

일렉트로닉스

자동차

전력 섹터

기타

지역

북미

미국

캐나다

기타 북미

유럽

독일

프랑스

영국

기타 유럽

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

합병, 인수, 합작사업, 제휴, 협정

주요 기업의 전략

기업 프로파일

GS Yuasa Corporation

Sion Power Corporation

LG Energy Solutions Ltd

Li-S Energy Limited

Polyplus Battery Co.

Saft Groupe SA

Gelion PLC

LYTEN Batteries Inc.

제7장 시장 기회와 미래 동향

전지 기술의 진보

CSM

영문 목차

영문목차

The Lithium Sulfur Battery Market size is estimated at USD 271.44 billion in 2025, and is expected to reach USD 582.52 billion by 2030, at a CAGR of 16.5% during the forecast period (2025-2030).

Key Highlights

Over the medium term, factors such as increasing demand for electric vehicles due to the various countries' supportive government policies and initiatives to reduce emissions and the increasing demand for energy storage devices amid increasing renewable energy installation drive growth in the market during the forecast period.

On the other hand, the high cost of lithium-sulfur batteries is likely to restrain the market growth during the forecast period.

Nevertheless, advancements in battery technology have dramatically increased the demand across end-user industries. Also, the government's investment is increasing to develop high-energy-density batteries for the military and aviation sectors. This will likely create immense opportunities for the market studied during the forecast period.

The Asia-Pacific is expected to be the largest and fastest-growing market during the forecast period, with most of the demand coming from countries like China, Japan, and other countries.

Lithium Sulfur Battery Market Trends

Aerospace Segment to Dominate the Market

In the aerospace sector, batteries are a vital component and have multiple applications in satellites, high-altitude aircraft, outer space vehicles, and unmanned aerial vehicles. Batteries in aerospace can be either primary (single-use) or secondary (rechargeable). Any battery designated for use as a power source in aircraft-installed or regularly carried equipment must be secure, have a high energy density, be lightweight, dependable, require minimal maintenance, and efficiently function in various environmental conditions.

The installation of lithium-sulfur batteries is increasing across the aerospace sector as this sector requires batteries with higher energy density. Therefore, it can provide longer-lasting and more powerful energy storage. The aerospace sector is also moving toward lower emission sources.

Lyten, a US-based battery startup company, is looking toward electric aircraft as a potential market for its energy-dense lithium-sulfur batteries. In June 2023, the company announced the commissioning of its lithium-sulfur battery pilot line in Silicon Valley. The lithium-sulfur pilot line is expected to start delivering commercial battery cells in 2023 to early adopting customers within the defense, logistics, automotive, and satellite sectors.

Furthermore, the utilization of drones for various purposes is increasing worldwide, which can be equipped with such batteries. The investment in manufacturing drones is growing significantly.

In July 2023, DroneShield was awarded a USD 33 million contract with an unnamed U.S. government agency. The contract covers the supply of equipment such as DroneGun Mk4, which can be used to disrupt the control and navigation capabilities of multiple drones.

The growth in the aviation sector is mainly driven by the increasing number of air passengers globally because of the cheaper airfare in recent times, developing economic conditions, and rising disposable income.

Due to the coronavirus pandemic, According to the International Air Transport Association (IATA), commercial airlines generated about USD 727 billion in revenue in 2022. However, the market's revenue was estimated to reach USD 779 billion by the end of 2023.

The abovementioned factors will likely drive growth in the aerospace sector, boosting the demand for lithium-sulfur batteries during the forecast period.

Asia-Pacific to Dominate the Market

Asia-Pacific is expected to dominate the global lithium-sulfur battery market. Countries in the region, such as China, Japan, and South Korea, are the leading supporters and are contributing to the growth of the market studied. Countries like Australia, India, and Vietnam are also following plans to set up lithium-based battery manufacturing facilities in their countries during the forecast period.

The region is significantly making efforts to supply clean electricity to every corner and reduce dependency on conventional fuels, such as kerosene and diesel, for their lighting and mobile phone charging needs. Lithium-sulfur battery integrated energy storage solutions will likely witness an increasing adoption rate due to their technical benefits, such as high energy density and storage capacity.

The demand for these batteries in the region is expected to grow rapidly, owing to the adoption of energy storage systems and electric vehicles for on-grid and off-grid applications. Further, the increasing installation of renewable energy generation facilities also boosts the demand for such batteries.

Furthermore, the Chinese government is investing in building charging stations nationwide to promote electric vehicle sales. For instance, in January 2022, the Chinese government announced plans to build enough charging stations for 20 million electric vehicles by 2025.

The development of charging infrastructure is propelling EV adoption in the country. As of May 2022, China Electric Vehicle Charging Infrastructure Promotion Alliance (EVCIPA) confirmed that there were nearly 1.42 million charging stations across the country, including 806 AC charging stations, 613 thousand DC charging stations, and 485 DC-AC combined charging stations.

Japan aims to establish a policy named 'Well-to-Wheel Zero Emission,' in line with the global efforts to eliminate emissions, focusing on energy supply and vehicle innovation by 2050 and replacing all vehicles with EVs to reduce greenhouse gas emissions by around 80% per vehicle, including an approximate 90% reduction per passenger vehicle. Such government initiatives are likely to increase the demand for electronic vehicles, which, in turn, is expected to increase the demand for lithium-sulfur batteries.

Similarly, in April 2023, the South Korean government, in partnership with the three leading battery companies (LG Energy Solution Ltd, Samsung SDI Co., Ltd and SK on Co., Ltd.), announced plans to jointly invest USD 15.1 billion by 2030 to develop advanced battery technologies, including solid-state batteries.

The initiative will enable South Korea to begin commercial production of solid-state batteries ahead of global competitors. The participating battery firms will establish pilot production plants in South Korea, serving as centers for product development and manufacturing innovation. These facilities will be used to test and manufacture advanced products, including solid-state batteries, before initiating mass production at overseas production sites. As a part of this effort, LG Energy Solutions set out a target for commercializing the production of lithium-sulfur batteries by 2027, primarily for the aerospace sector to start with.

Therefore, based on the above factors, the Asia-Pacific is expected to dominate the lithium-sulfur battery market during the forecast period.

Lithium Sulfur Battery Industry Overview

The lithium-sulfur battery market is fragmented. Some of the major players in the market include (in no particular order) GS Yuasa Corporation, LG Energy Solutions Ltd, Saft Groupe SA, Gelion PLC, and Sion Power Corporation, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2028

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Growing Adoption of Electric Vehicles

4.5.1.2 Increasing Demand for Energy Storage Systems (ESS)

4.5.2 Restraints

4.5.2.1 Limited Cycle Life and Durability

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 End User

5.1.1 Aerospace

5.1.2 Electronics

5.1.3 Automotive

5.1.4 Power Sector

5.1.5 Other End Users

5.2 Geography

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Rest of North America

5.2.2 Europe

5.2.2.1 Germany

5.2.2.2 France

5.2.2.3 United Kingdom

5.2.2.4 Rest of Europe

5.2.3 Asia-Pacific

5.2.3.1 China

5.2.3.2 India

5.2.3.3 Japan

5.2.3.4 South Korea

5.2.3.5 Rest of Asia-Pacific

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Rest of South America

5.2.5 Middle East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 United Arab Emirates

5.2.5.3 South Africa

5.2.5.4 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements