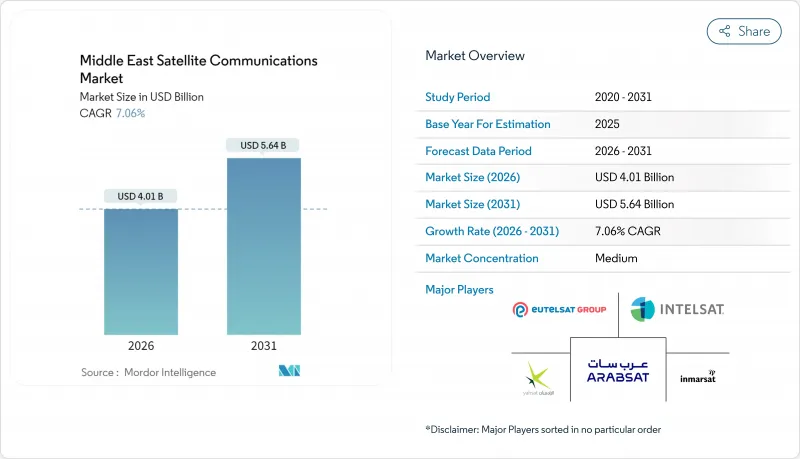

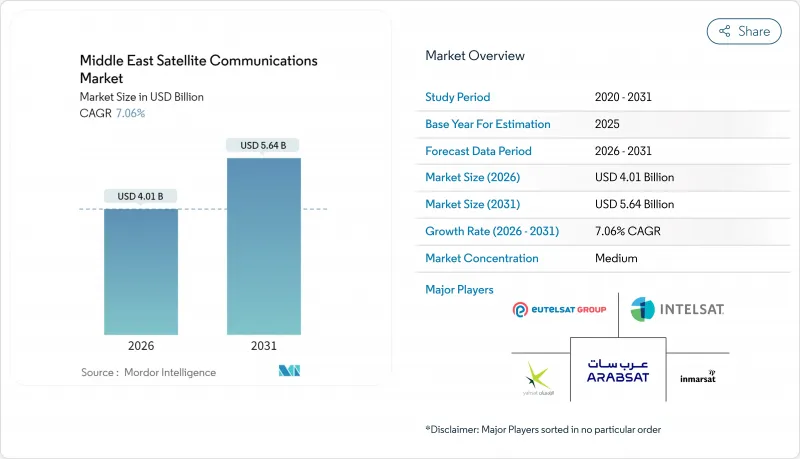

중동의 위성 통신 시장 규모는 2026년 40억 1,000만 달러로 추정되고 있으며, 2025년 37억 4,000만 달러에서 성장한 수치입니다. 2031년에 56억 4,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 7.06%로 확대될 전망입니다.

지정학적 복잡성, 정부 주도의 광대역 의무화, 유전, 항만, 항공기에서의 IoT 도입의 급증이 함께 수요를 확대하고 있습니다. 사업자는 대역폭을 대량으로 소비하는 기업 및 방위 분야의 요구에 대응하기 위해 고처리량 위성(HTS)에 대한 투자를 우선하고 있습니다. 한편, 주파수 조정의 과제에 의해 신규 발사 비용은 상승 경향에 있습니다. 경쟁 우위는 클라우드 게이트웨이, 관리형 연결 및 에지 분석 기능을 결합한 수직 통합 서비스 번들에 점점 의존하고 있습니다. 해상 및 항공기 연결, 5G 사설망 백홀, 장치 직접 연결(D2D) 이니셔티브는 고수익 틈새 시장으로 부상하고 있으며 중동 위성 통신 시장의 다음 성장파를 형성할 것입니다.

위성 접속 센서 수천대가 원격 유정의 압력, 유량, 배출량을 감시해, 예지 보전을 가능하게 하는 것과 동시에 예기치 않은 조업 정지를 저감하고 있습니다. 사우디 알람코의 실시간 유정 모니터링 네트워크는 광섬유가 불가능한 지역에서 에너지 대기업이 우주 통신을 활용하는 좋은 예입니다. Space42사의 AI를 활용한 분석 기술은 채굴 효율을 더욱 향상시키고 Globalstar사의 탱크 감시 툴은 걸프 지역의 터미널에서공급 중단을 삭감합니다. 이러한 도입은 운영 비용을 줄이고 중동 위성 통신 시장을 지속시키는 지속적인 대역폭 수요를 창출하고 있습니다.

두바이, 제다, 도하의 주요 항만에서는 선박교통관리 및 화물분석에 VSAT를 활용하여 해운회사에 의한 선대 전체 업그레이드를 추진하고 있습니다. 머링크사가 지역사업자와 체결한 계약은 HTS 용량이 영상 전달, IoT 텔레메트리, 승무원 복지 서비스를 제공하는 예를 보여줍니다. 자율항행 플랫폼과의 통합으로 무인수상정의 규제면에서의 진전에 따라 새로운 수익원이 개척되고 있습니다.

위성의 급속한 보급으로 간섭 위험이 악화되고 ITU의 조정 절차는 대응에 쫓기고 있습니다. 쿼드사트와 아랍사트의 주파수 모니터링 계약이 확대되고 있으며, 자동화 도구의 중요성이 업계에서 인식되고 있습니다. 그러나 미해결 C 밴드와 Ku 밴드의 중복은 발사 지연과 보험료 상승을 초래하여 중동 위성 통신 시장에 마찰을 일으키고 있습니다.

지상 설비는 2025년 중동 위성 통신 시장에서 58.05%의 점유율을 유지했습니다. 사우디아라비아와 UAE에서의 텔레포트, 게이트웨이, VSAT의 전개가 기반이 되고 있습니다. 그러나 서비스 수익은 하드웨어를 뛰어넘는 7.85%의 연평균 복합 성장률(CAGR)로 성장이 예상되고, 관리형 대역폭 패키지, 클라우드 게이트웨이, 위성 대응 IoT 플랫폼이 견인 역할을 하고 있습니다.

서비스 분야의 성장은 네트워크 관리 부담을 줄이는 종량 과금 모델에 대한 기업 수요를 반영합니다. 에스헤일새트와 넥사트사의 OSS/BSS 제휴는 자동화가 운영 비용 절감과 도입 촉진에 기여하는 좋은 예입니다. HTS 페이로드가 보급됨에 따라 운영자는 사이버 보안, 에지 분석 및 SLA 기반 가동 시간 보증을 패키징하고 중동 위성 통신 시장에서 고객의 지출 점유율을 확대하고 있습니다.

2025년 중동 위성 통신 시장 점유율에서 해상 용도는 40.30%를 차지했습니다. 이것은 수에즈 운하와 홀름스 해협을 통과하는 조밀한 항로가 요인입니다. 한편 항공기 연결은 8.22%라는 가장 빠른 CAGR을 나타낼 것으로 예측됩니다. 항공사가 승객의 스트리밍 수요를 충족하는 경쟁을 격화시켜 방위용 UAV(무인 항공기) 함대가 확대되고 있기 때문입니다.

지역 항공사는 고객 경험의 차별화를 도모하기 위해 Ka 밴드 기내 Wi-Fi를 도입하고 UAE의 도시형 항공 모빌리티 실증 사업에서는 지휘 통제에 저지연 위성 링크를 활용하고 있습니다. 육상 플랫폼은 유전 SCADA 백업 및 재해 복구 네트워크에서 여전히 중요하며 중동 위성 통신 시장을 지원하는 다양한 수요 기반을 강화하고 있습니다.

Middle East satellite communications market size in 2026 is estimated at USD 4.01 billion, growing from 2025 value of USD 3.74 billion with 2031 projections showing USD 5.64 billion, growing at 7.06% CAGR over 2026-2031.

Geopolitical complexities, government-backed broadband mandates, and a surge of IoT deployments across oilfields, ports, and aircraft are collectively amplifying demand. Operators are prioritizing high-throughput satellite (HTS) investments to meet bandwidth-intensive enterprise and defense needs, even as spectrum coordination challenges raise the cost of new launches. Competitive positioning increasingly hinges on vertically integrated service bundles that blend cloud gateways, managed connectivity, and edge analytics capabilities. Maritime and airborne connectivity, 5G private-network backhaul, and direct-to-device (D2D) initiatives are emerging as high-margin niches that will shape the next growth wave of the Middle East satellite communications market.

Thousands of satellite-connected sensors now track pressure, flow, and emissions in remote wells, enabling predictive maintenance and lowering unplanned downtime. Saudi Aramco's real-time well-monitoring network exemplifies how energy majors leverage space-borne links where fiber is impractical. Space42's AI-powered analytics further enhance extraction efficiency, while Globalstar's tank-monitoring tools reduce supply interruptions across Gulf terminals. These deployments cut operating expenses and create recurring bandwidth demand that sustains the Middle East satellite communications market.

Major ports in Dubai, Jeddah, and Doha rely on VSAT for vessel traffic management and cargo analytics, driving fleet-wide upgrades by shipping lines. Marlink's agreements with regional operators showcase how HTS capacity delivers video, IoT telemetry, and crew welfare services. Integration with autonomous navigation platforms opens fresh revenue streams as unmanned surface vessels gain regulatory traction.

Rapid satellite proliferation has exacerbated interference risks, and ITU coordination procedures struggle to keep pace. Quadsat's spectrum-monitoring deal with Arabsat signals is growing, and industry recognition that automated tools are vital. Still, unresolved C- and Ku-band overlaps can delay launches and elevate insurance premiums, adding friction to the Middle East satellite communications market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Ground equipment retained a 58.05% share of the Middle East satellite communications market in 2025, anchored by teleport, gateway, and VSAT deployments across Saudi Arabia and the UAE. Yet services revenue is projected to outpace hardware at an 7.85% CAGR, buoyed by managed bandwidth packages, cloud gateways, and satellite-enabled IoT platforms.

Services momentum reflects enterprise appetite for pay-as-you-go models that offload network management overhead. Es'hailSat's OSS/BSS partnership with neXat exemplifies how automation trims operating costs and accelerates onboarding. As HTS payloads proliferate, operators bundle cybersecurity, edge analytics, and SLA-backed uptime guarantees, expanding wallet share within the Middle East satellite communications market.

Maritime applications accounted for 40.30% of the Middle East satellite communications market share in 2025, due to dense shipping lanes through the Suez Canal and Strait of Hormuz. Airborne connectivity, however, is forecast to post the quickest 8.22% CAGR as airlines race to satisfy passenger streaming expectations and defense UAV fleets scale up.

Regional carriers adopt Ka-Band inflight Wi-Fi to differentiate customer experience, while the UAE's urban-air-mobility pilots lean on low-latency satellite links for command and control. Land platforms remain critical for oilfield SCADA backups and disaster-recovery networks, reinforcing diverse demand pillars that underpin the Middle East satellite communications market.

The Middle East Satellite Communications Market Report is Segmented by Type (Ground Equipment and Services), Platform (Portable, Land, Maritime, and Airborne), Frequency Band (L-Band, C-Band, Ku-Band, and Ka-Band), End-User Vertical (Maritime, Defense and Government, Enterprises, and More), Application (Voice Communications, Data Communications, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).