ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

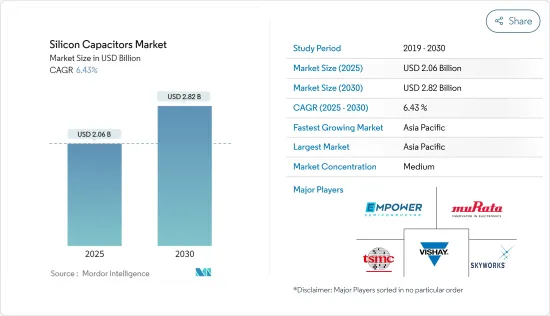

실리콘 커패시터 시장 규모는 2025년에 20억 6,000만 달러에 이르고 예측 기간(2025-2030년)의 CAGR은 6.43%를 나타내, 2030년에는 28억 2,000만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

실리콘 커패시터는 주로 싱글 또는 멀티 MIM 구조로 반도체 기술을 이용하여 제조됩니다.

반도체 제조 방법으로 만들어진 실리콘 커패시터는 뛰어난 정전 용량 밀도와 신뢰성을 높이기 위해 안정성을 높이는 실리콘 유전체층을 갖추고 있어, 고주파 용도가 뛰어납니다.

실리콘 커패시터는 그 고주파, 소형 설계 호환성을 위한 초소형·박형, 고성능 SoC 포장 모듈에의 응용에 의해 세계의 5G, 나아가서는 6G 통신의 성장에 수반해, 통신 기기나 소비자용 전자 기기 제품에서의 유용성이 높아지고 있습니다.

실리콘 커패시터는 안정성, 고주파 성능, 소형화 등 몇 가지 장점이 있지만, 단점도 있습니다.

인플레이션률 상승, 최종 사용자 수요 부진, COVID-19 위기시 개인 소비 감소 등 다양한 요인이 실리콘 커패시터 수요에 영향을 미쳤습니다. 긴장은 기술제한을 포함해 성장을 저해하는 자세입니다.

실리콘 커패시터 시장 동향

자동차 부문이 큰 성장을 이룰 전망

세계의 실리콘 커패시터 시장을 뒷받침하는 요인 중 하나는 자동차 부문에서 소형화가 받아들여지고 있다는 것입니다.

실리콘 커패시터는 등가 직렬 저항(ESR)이 낮기 때문에 에너지 효율이 매우 높은 것으로 알려져 있습니다. 실리콘 커패시터가 효과적으로 작동할 수 있는 넓은 온도 범위(-55°C - +150°C)는 혹독한 기후 조건에 노출되는 자동차 애플리케이션에 필수적입니다.

IEA에 따르면 신흥국의 전기차 판매량은 2배 이상으로 증가하고 있지만, 판매량은 여전히 늘어나야 합니다. 2022년 상반기에 판매량이 크게 증가했으며, EIA는 2023년 말까지 전 세계 전기차 판매 점유율이 18%를 넘었습니다. 따라서, 실리콘 커패시터는 산업이 보다 소형으로 효율적인 전원 시스템으로 이행함에 따라 수요가 높아지는 소형화 부품의 하나이며, 그 수요는 EV 제조의 대폭적인 증가와 밀접한 상관관계에 있습니다.

ADAS와 자율주행차에 있어서, 시그널 무결성과 고속 데이터 처리는 매우 중요합니다.

인텔에 따르면 자율주행차 등록 대수 점유율은 2030년까지 약 12%를 나타낼 것으로 예측되고 있습니다.

자동차 산업은 소형화를 추진하고 있으며, 실리콘 커패시터에 대한 요구가 높아지고 있습니다. 젠트 엔터테인먼트 시스템을 통합함으로써 자동차의 중요성이 높아지고 있습니다.

아시아태평양이 현저한 성장을 이룰 전망

이 지역, 특히 중국, 일본, 한국, 대만과 같은 국가들은 기술 혁신의 최전선에 있습니다.

Telenor IoT Megatrends Report에 따르면 아시아태평양의 IoT 도입은 전례없는 속도로 성장했으며, 2030년까지 389억대 이상의 IoT 장치가 존재할 것으로 예측됩니다.

2023년 2월, 인도 정부는 COVID-19 이후 전자 수요 증가를 받고, 전자 정보 기술부에 1,654억 9,000만 루피(20억 1,177만 달러)를 할당했습니다. 조업과 디스플레이 제조업을 뒷받침하기 위해 반도체 미션에 30억 루피(3,647만 달러)를 투자하는 것을 목표로 하고 있습니다.

수요 증가는 이 나라를 자동차 제조의 허브로 만들기 위한 정부의 지원적 규제와 함께 이 지역의 자동차 섹터의 성장을 더욱 촉진하고 있습니다.

자동차 산업에 있어서의 에너지 공급 수요의 고조는 이 부문(segment)의 성장의 큰 원동력이 되고 있습니다.

예를 들어, 2030년까지 전기를 달성하기 위해 하이브리드 자동차와 전기자동차 기술의 제조를 촉진하기 위해 정부는 "Faster Adoption and Manufacturing of Hybrid & Electric Vehicles in India Under the National Electric Mobility Mission Plan(NEMMP)"을 추진하고 있습니다.

실리콘 커패시터 산업 개요

실리콘 커패시터 시장은 반고정적입니다. 시장에 대한 침투도와 새로운 기술에 대한 투자 능력을 고려하면 경쟁 기업간 경쟁 관계가 향후 확대될 것으로 예측됩니다. Inc., Empower Semiconductor, TSMC 등이 있습니다.

2024년 5월 - 엠파워 세미컨덕터는 고주파 디커플링용 ECAP 제품군 중에서 가장 큰 실리콘 커패시터를 발표했습니다. 이 제품은 고성능 시스템 온칩(SoC)에서 일반적으로 볼 수 있는 가장 까다로운 전력 무결성 목표에 적합합니다. GHz까지의 초저 임피던스를 제공해, 고성능 컴퓨팅(HPC)이나 인공지능(AI) 용도에 적합합니다.

2023년 10월 - 넥스페리아는 첨단 전자 부품의 세계적인 제조업체인 교세라 AVX 구성 요소(잘츠부르크)사와의 전략적 제휴를 발표했습니다. 양사는 공동으로 새로운 650V, 20A의 탄화규소(SiC) 정류기 모듈을 개발합니다 는 3kW에서 11kW의 전력 스택 범위 내 고주파 전력용으로 설계되어 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

기술 동향

산업의 매력 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

산업 밸류체인 분석

기술 스냅샷

COVID-19의 영향과 거시경제 요인이 시장에 미치는 영향의 평가

제5장 시장 역학

시장 성장 촉진요인

자동차 산업에서의 소형화의 인기가 높아짐

높아지는 기술 진보

시장의 과제

실리콘 커패시터의 고전하 누설과 저용량 범위

제6장 시장 세분화

기술별

MOS 커패시터

MIS 커패시터

딥 트렌치 실리콘 커패시터

최종 사용자 용도별

자동차

소비자용 전자 기기

IT 및 통신

항공우주 및 방위

의료

기타 최종 사용자 용도

지역별

북미

유럽

아시아

호주 및 뉴질랜드

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

Murata Manufacturing Co. Ltd

Vishay Intertechnology Inc.

Skyworks Solutions Inc.

Empower Semiconductor

TSMC

KYOCERA AVX Components Corporation

Microchip Technology Inc.

ELOHIM Inc.

Massachusetts Bay Technologies

MACOM Technology Solutions Holdings Inc.

제8장 시장의 미래

KTH

영문 목차

영문목차

The Silicon Capacitors Market size is estimated at USD 2.06 billion in 2025, and is expected to reach USD 2.82 billion by 2030, at a CAGR of 6.43% during the forecast period (2025-2030).

Key Highlights

Silicon capacitors, predominantly single or multiple MIM structures, are crafted using semiconductor technologies. Their dielectrics, composed of silicon dioxide or silicon nitride, are favored for high-density applications, offering stability, reliability, and temperature resilience. These capacitors, with their robust performance, find utility in demanding environments. High-density variants employ 3D nano-shaped electrodes to enhance surface area.

Silicon capacitors, crafted through semiconductor manufacturing methods, feature silicon dielectric layers for enhanced stability to enhance superior capacitance density and reliability and excel in high-frequency applications. These capacitors exhibit a significant aging time of up to a decade. They can operate at high temperatures and in harsh environmental conditions, driving the future market adoption of silicon capacitors.

Due to their high frequency, ultra-small and thin for miniaturized design compatibility, and application in high-performance SoC package modules, silicon capacitors are finding increased utility in communication devices and consumer electronics, in line with the growth of 5G and even 6G communications worldwide.

Although silicon capacitors have several benefits, including stability, high-frequency performance, and miniaturization, they also have some drawbacks. There are several drawbacks, including smaller capacitance ranges and higher charge leakages compared to more conventional capacitors like ceramic or tantalum. These limitations impede the expansion of the global silicon capacitor market.

Various factors, including rising inflation, weak end-user demand, and reduced consumer spending during the COVID-19 crisis, impacted the demand for silicon capacitors. The Russo-Ukraine conflict and US-China tensions, including technology restrictions, are poised to hinder growth. However, the increasing demand for consumer electronic products, the emergence usage of electric vehicles, and the manufacturing expansion of semiconductor industries worldwide in the post-pandemic period would support the market's growth.

Silicon Capacitors Market Trends

Automotive Sector to Witness Major Growth

One factor propelling the global silicon capacitor market is the growing acceptance of miniaturization in the automotive sector. Modern automotive technologies, such as autonomous driving systems, enhanced driver assistance systems, and electric cars (EVs), depend on the trend toward smaller, more economical, and higher-performing electronic components required in ADAS.

Due to the low equivalent series resistance (ESR) of silicon capacitors, they are well known for being extremely energy efficient. This is crucial for EVs and HEVs, which depend on effective power management to increase battery life and driving range. The broad temperature range (-55 °C to +150 °C) over which silicon capacitors may function effectively makes them essential for automotive applications subjected to harsh climatic conditions. Silicon capacitor's small dimensions enable more adaptable and space-efficient designs to fit into the constrained interior of contemporary EV automotives.

According to IEA, Electric car sales in emerging nations have more than doubled, but sales volumes still need to grow. In the first quarter of 2023, sales increased by 25% compared to the same period in 2022. Sales climbed significantly in the first half of 2022, and EIA implies that the global EV sales share was over 18% by the end of 2023. Therefore, silicon capacitors are among the miniaturized components in high demand as the industry moves toward smaller and more efficient power systems, and their demand is closely correlated with the significant increase in EV manufacturing.

Signal integrity and high-speed data processing are critical to ADAS and autonomous cars. Silicon capacitors are strong candidates for high-frequency applications since they offer the reliable performance needed for sophisticated radar, LIDAR, and camera systems. Silicon capacitors' exceptional endurance and dependability guarantee steady performance throughout the car's life cycle, which is essential for safety-related applications in autonomous driving.

According to Intel, the share of registered autonomous vehicles is expected to reach about 12% by 2030. The increasing prevalence of autonomous driving systems will drive demand for dependable high-frequency components such as silicon capacitors.

The automotive industry's push for miniaturization drives the need for silicon capacitors. Reliability, performance, and compactness are critical for electrical components such as silicon capacitors, which are becoming more important in cars by integrating electric drivetrains, autonomous driving technologies, and intelligent entertainment systems. In addition to increasing the capabilities of modern cars, this factor is driving significant growth in the global silicon capacitor industry.

Asia-Pacific to Witness Significant Growth

The region, particularly countries like China, Japan, South Korea, and Taiwan, is at the forefront of technological innovation. These countries are significant semiconductor manufacturing and electronics players, providing a solid foundation for adopting and developing silicon capacitors.

According to the Telenor IoT Megatrends Report, the adoption of IoT in Asia-Pacific is expected to grow at an unprecedented rate, and more than 38.9 billion IoT devices will be there by 2030. The report stated that the revenue from cellular IoT connections would grow continuously.

In February 2023, the Government of India allocated INR 16,549 crore (USD 2011.77 million) to the Ministry of Electronics and Information Technology, owing to the growing demand for electronics post-COVID-19. The government aims to invest INR 300 crore (USD 36.47 million) in the semiconductor mission to boost the semiconductor manufacturing and display manufacturing industry. This is expected to fuel the production of consumer electronics.

Increasing demand, along with supportive government regulations to make the country an automotive manufacturing hub, is further driving the growth of the automotive sector in the region. For instance, India's Automotive Mission Plan 2026 is a mutual initiative by the Government of India and the Indian automotive industry to lay down the roadmap for the industry's evolution.

The rise in demand for energy supply in the automobile industry has been a significant driver for growth in this sector. Exhaust emission control norms have become even more stringent in the country.

For instance, to promote the manufacturing of hybrid and electric vehicle technologies to achieve electrification by 2030 ultimately, the government has even launched the Faster Adoption and Manufacturing of Hybrid & Electric Vehicles in India Under the National Electric Mobility Mission Plan (NEMMP) as silicon capacitors are increasingly used in the electronics and subsystems of electric vehicles. Such trends are expected to support the growth of the market studied.

Silicon Capacitors Industry Overview

The silicon capacitor market is semi-consolidated. Considering the market penetration and ability to invest in new technologies, the competitive rivalry is expected to grow in the future. This may be termed beneficial for the buyers, as product differentiation would be a determinate factor during the forecast period. Some of the key players include Murata Manufacturing Co. Ltd, Vishay Intertechnology Inc., Skyworks Solutions Inc., Empower Semiconductor, and TSMC.

May 2024 - Empower Semiconductor revealed the largest silicon capacitor in its ECAP product range for high-frequency decoupling. The new EC1005P is a single 16.6-microfarad (μF) capacitance device suitable for the most demanding power integrity goals typically found in high-performance systems-on-chip (SoCs). It offers ultra-low impedance up to 1 GHz in a compact form that may be inserted into the substrate or interposer of any SoC, making it well-suited for high-performance computing (HPC) and artificial intelligence (AI) applications.

October 2023 - Nexperia announced a strategic partnership with KYOCERA AVX Components (Salzburg) GmbH, a global manufacturer of advanced electronic components. Together, they will develop a new 650 V, 20 A silicon carbide (SiC) rectifier module. This module is designed for high-frequency power applications within the 3 kW to 11 kW power stack range. Target applications include industrial power supplies, EV charging stations, and on-board chargers. This collaboration signifies a significant advancement in the longstanding partnership between the two companies.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Technology Trends

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Threat of Substitutes

4.3.5 Intensity of Competitive Rivalry

4.4 Industry Value Chain Analysis

4.5 Technology Snapshot

4.6 Assessment of the Impact of COVID-19 and the Impact of Macroeconomic Factors on the Market

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Increasing Popularity of Miniaturization in the Automotive Industries

5.1.2 Growing Technological Advancements

5.2 Market Challenges

5.2.1 High Charge Leakages and Lower Capacitance Range of Silicone Capacitors