베트남의 데이터센터 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Vietnam Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693788

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

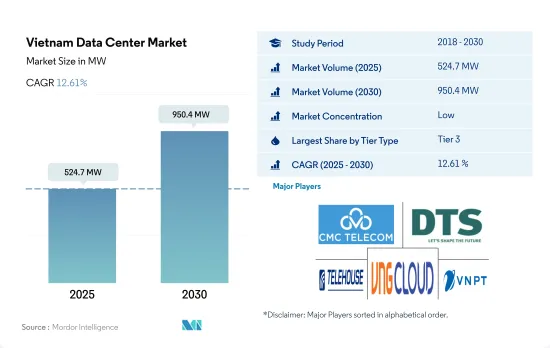

베트남의 데이터센터 시장 규모는 2025년 5억 2,470만 kW, 2030년 9억 5,040만 kW에 이를 것으로 추정되며 CAGR 12.61%를 나타낼 것으로 예측됩니다.

또한 2025년에는 5억 8,890만 달러의 코로케이션 수익이 예상되고, 2030년에는 14억 340만 달러에 이를 것으로 추정되며, 예측 기간(2025-2030년)의 CAGR은 18.97%를 나타낼 것으로 전망됩니다.

2023년 시장 점유율은 Tier 3 데이터센터가 대부분을 차지했지만 예측 기간 동안 Tier 4가 가장 성장

중단없는 비즈니스 서비스의 성장으로 Tier 1과 Tier 2의 시설은 수요를 잃고 있습니다.

베트남의 데이터센터 시장에서 Tier 3 섹터의 IT 부하 용량은 2022년에 119.56MW에 이르렀습니다.

동영상과 음악 스트리밍, 게임 등의 온라인 엔터테인먼트도 베트남 전역의 인터넷 사용자들 사이에서 기세를 늘리고 있는 활동입니다. 농촌 지역에서는 최근 몇 년 동안 비디오 및 영화 스트리밍이 일상적인 주요 온라인 활동 중 하나가되었습니다. YouTube는 가장 인기 있는 영화 스트리밍 플랫폼이었습니다. 이러한 서비스에는 다운타임이 적고 24시간 365일 지원을 받을 수 있는 데이터센터 시설이 필요하며, 3단계 시설이 이를 제공할 수 있습니다.

2021년에는 22%의 사람들이 공부, 엔터테인먼트, 쇼핑을 위해 하루 9시간 이상 인터넷을 이용했으며, 대부분 스마트폰을 이용했습니다. 2023년 1월 베트남 인터넷 이용자 수는 7,793만명이었습니다. 이용자 수는 2022-2023년 사이에 530만명 증가(7.3% 증가)했습니다.

베트남 시장에는 인프라의 비효율성과 장애가 많기 때문에 Tier 4 시설은 아직 개발 도상입니다. 따라서 분석에 따르면 최고 계층 기반 시설에 대해서는 시장 개척이 진행되지 않았습니다.

베트남의 데이터센터 시장 동향

5G 등 디지털 이니셔티브 우선, 개인 소비 확대가 시장 성장을 견인

이 나라의 스마트폰 유저수는 2023년에 7,790만명으로 예측기간 동안 CAGR 3.09%를 나타냈으며, 2029년에는 9,350만명에 달할 것으로 예상됩니다.

베트남에서는 디지털 기술의 이용이 급속히 확대되고 있습니다. 과거 더 많은 사람들이 스마트폰을 구입할 수 있게 되어 스마트폰 이용이 증가했습니다. 또한 베트남에서는 성인의 73% 이상이 스마트폰을 사용하고 있습니다.

향후 몇 년 동안 5G 기술이 도입되어 4G 네트워크가 전국에 퍼질 것으로 예측됩니다. 다른 도시 지역과 산업 지역으로 확장합니다. 원격지의 통신사업자간에 5G네트워크를 공유하고 비용 절감을 도모하는 것을 제안했습니다. 연결하는 시간이 가장 길기 때문에 중요성이 높습니다.

통신 사업자의 5G 네트워크 확대를 위한 투자 증가와 정부 지원을 통한 디지털 성장에 대한 지역 비전이 시장 성장을 뒷받침합니다.

2022년 5G 네트워크와 Viettel의 시작은 이 나라의 디지털 시장에 혁명을 일으켰습니다. Asia가 보도했듯이, 총무성은 디지털 경제 개발을 가속화하는 주요 책임을 맡고 있습니다. 또한, 이 나라의 GDP 증가에 의해 2023-2030년에 걸쳐, 베트남 전토에서 무선과 브로드밴드의 가입률이 계속 상승해, 그 결과, 통신 사업자의 수익이 증가할 것으로 예상되고 있습니다.

Vientel, Vinaphone, Mobifone 시장 점유율은 약 90%에서 90% 이상입니다. 동시에 Gmobile, Saigon Ho Chi Minh Telecommunications, Post Saigon Tel, SCTV 등 별로 유명하지 않은 참가 기업이 관여하는 합병도 향후 발표될 가능성이 있습니다. 국내총생산(GDP)에서 차지하는 점유율을 20%로 끌어올릴 계획을 가지고 있습니다.

베트남의 데이터센터 산업 개요

베트남의 데이터센터 시장은 세분화되어 있으며 상위 5개 기업에서 37.86%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 서론

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 시장 전망

IT 부하 용량

바닥 공간 증가

코로케이션 수익

설치된 랙

랙 공간 활용

해저 케이블

제5장 주요 산업 동향

스마트폰 사용자수

스마트폰 1대당 데이터 트래픽

모바일 데이터 속도

광대역 데이터 속도

광섬유 접속 네트워크

규제 프레임워크

베트남

밸류체인과 유통채널 분석

제6장 시장 세분화

핫스팟

하노이

호치민시

기타

기타 중동 및 아프리카

데이터센터의 규모

대규모

초대규모

중규모

메가규모

소규모

티어 유형

Tier 1 및 2

Tier 3

Tier 4

흡수량

미활용

활용

코로케이션 유형별

하이퍼스케일

소매

도매

최종 사용자별

BFSI

클라우드

전자상거래

정부

제조

미디어 및 엔터테인먼트

통신

기타 최종 사용자

기타

제7장 경쟁 구도

시장 점유율 분석

기업 상황

기업 프로파일

CMC Telecom

DTS Communication

FPT Telecom Joint Stock Company

GDS(JV of NTT and VNPT)

HTC-ITC(Hanoi Telecommunications Corporation)

QTSC Telecom Center

Telehouse(KDDI Corporation)

USDC Technology

Viettel-CHT Company Limited(Viettel IDC)

Viettel IDC

VNG Cloud

VNPT Online

VNTT

제8장 CEO에 대한 주요 전략적 질문

제9장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

세계 시장 규모와 DRO

정보원과 참고문헌

도표 목록

주요 인사이트

데이터 팩

용어집

KTH

영문 목차

영문목차

The Vietnam Data Center Market size is estimated at 524.7 MW in 2025, and is expected to reach 950.4 MW by 2030, growing at a CAGR of 12.61%. Further, the market is expected to generate colocation revenue of USD 588.9 Million in 2025 and is projected to reach USD 1,403.4 Million by 2030, growing at a CAGR of 18.97% during the forecast period (2025-2030).

Tier 3 data centers accounts for majority market share in 2023, Tier-4 is the fastest growing in forecasted period

The growth in uninterrupted business services is causing Tier 1 & 2 facilities to lose demand. A growing number of global companies are creating business continuity services and shifting priority to tier 3 data centers.

The tier 3 sector in the Vietnamese data center market reached an IT load capacity of 119.56 MW in 2022. It is expected to register a CAGR of 2.23% to reach 139.56 MW by 2029. There is an increased investment in data center infrastructure and technological advancements. It is expected to create lucrative opportunities for market growth in 2029.

Online entertainment, such as video and music streaming and games, was another activity gaining momentum among internet users across Vietnam. In rural areas, video and movie streaming has been one of the major daily online activities in recent years. YouTube was the most popular movie streaming platform. These services need data center facilities with minimum downtime and 24/7 support, which tier 3 facilities can offer.

In 2021, 22% of people were estimated to use the internet for more than 9 hours a day for studying, entertainment, and shopping, with the majority on their smartphones. Vietnam had 77.93 million internet users in January 2023. The number of users increased by 5.3 million (+7.3%) between 2022 and 2023.

The Vietnamese market is nascent for tier 4 facilities since it has many infrastructural inefficiencies and hiccups. Hence, as per analysis, the market has not witnessed any developments for the highest tier-based facilities.

Vietnam Data Center Market Trends

Prioritizing digital initiatives, such as 5G, growing consumer spending to drives the market growth

The total number of smartphone users in the country was 77.9 million in 2023, which is expected to register a CAGR of 3.09% during the forecast period to reach a value of 93.5 million by 2029.

The usage of digital technology is rapidly expanding in Vietnam. The quick adoption of Internet and smartphone technology in various businesses has significantly impacted consumer behaviour. In 2022, consumer spending in Vietnam increased to USD 214.68 Billion from USD 193.08 Billion in 2021. As a result, more people can now purchase smartphones, leading to an increase in smartphone usage. Additionally, Vietnam has more than 73% of adults using smartphones. The government aims to increase this proportion to more than 80% by 2025 through the National Digital Infrastructure Strategy by 2025.

Over the next several years, it is anticipated that 5G technology will be deployed, and the 4G network will extend across the country. The government has four operators: MobiFone, Vietnamobile, Viettal Mobile, and Vinaphone, with 4G customers. In 2022, Vietnam will issue licenses for 5G services, starting to expand 5G from Ho Chi Minh City and Hanoi and extending to other urban and industrial zones. Vietnam's three mobile operators, MobiFone, Viettel Mobile, and Vinaphone, have piloted 5G in 16 cities and provinces. MobiFone proposed sharing a 5G network among carriers in remote areas with low demand to uptake cost-saving. The operators are looking to commercialize 5G over the coming years, while 4G and 3G are highly significant because consumers spend most time connected to these mature technologies. The increased network connectivity of 3G and 4G networks and the deployment of 5G in smartphones will cater to an increase in smartphone users in the country.

The increasing investments for the expansion of 5G network by Operators and region vision to grow digital with the government support drives the growth of the market

In 2022, the launch of the 5G network and Viettel revolutionized the digital market of the country. MIC has been assigned primary responsibility for accelerating the development of the digital economy, as reported by OpenGov Asia. The Ministry is tasked with directing and assisting other ministries, agencies, and local governments in implementing the strategy. In addition, it provides the Prime Minister with reports on its achievements. Further, owing to an increase in the country's GDP, it is expected that from 2023 to 2030, wireless and broadband subscription rates will continue to rise across Vietnam, resulting in increased revenues for operators.

The market share of Vientel, Vinaphone, and Mobifone ranges from about 90% to more than 90%. At the same time, mergers involving less prominent players such as Gmobile, Saigon Ho Chi Minh Telecommunications, Post Saigon Tel, or SCTV could be announced in the future. Also, to attract private investment and improve market transparency, the government could sell down its stakes in VNPT and Mobifone by up to 50%. Moreover, according to a resolution passed by the Politburo on Guidelines for Participation in the Fourth Industrial Revolution, Vietnam has plans to increase its share of the digital economy's gross domestic product (GDP) to 20% by 2025. Vietnam enjoys 99.8% 4G coverage nationwide, with three major carriers, Viettel, VNPT, and MobiFone, successfully piloting 5G technology in 16 cities and provinces. Due to the increasing launch of 4G and 5G, the country is expected to shut down its 2G and 3G services.

Vietnam Data Center Industry Overview

The Vietnam Data Center Market is fragmented, with the top five companies occupying 37.86%. The major players in this market are CMC Telecom, DTS Communication, Telehouse (KDDI Corporation), VNG Cloud and VNPT Online (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 MARKET OUTLOOK

4.1 It Load Capacity

4.2 Raised Floor Space

4.3 Colocation Revenue

4.4 Installed Racks

4.5 Rack Space Utilization

4.6 Submarine Cable

5 Key Industry Trends

5.1 Smartphone Users

5.2 Data Traffic Per Smartphone

5.3 Mobile Data Speed

5.4 Broadband Data Speed

5.5 Fiber Connectivity Network

5.6 Regulatory Framework

5.6.1 Vietnam

5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

6.1 Hotspot

6.1.1 Hanoi

6.1.2 Ho Chi Minh City

6.1.3 Others

6.1.4 Rest of Vietnam

6.2 Data Center Size

6.2.1 Large

6.2.2 Massive

6.2.3 Medium

6.2.4 Mega

6.2.5 Small

6.3 Tier Type

6.3.1 Tier 1 and 2

6.3.2 Tier 3

6.3.3 Tier 4

6.4 Absorption

6.4.1 Non-Utilized

6.4.2 Utilized

6.4.2.1 By Colocation Type

6.4.2.1.1 Hyperscale

6.4.2.1.2 Retail

6.4.2.1.3 Wholesale

6.4.2.2 By End User

6.4.2.2.1 BFSI

6.4.2.2.2 Cloud

6.4.2.2.3 E-Commerce

6.4.2.2.4 Government

6.4.2.2.5 Manufacturing

6.4.2.2.6 Media & Entertainment

6.4.2.2.7 Telecom

6.4.2.2.8 Other End User

6.4.2.2.9 Others

7 COMPETITIVE LANDSCAPE

7.1 Market Share Analysis

7.2 Company Landscape

7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).