Global Steel Sections - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693695

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

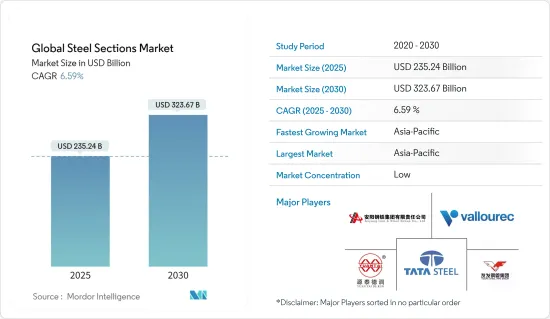

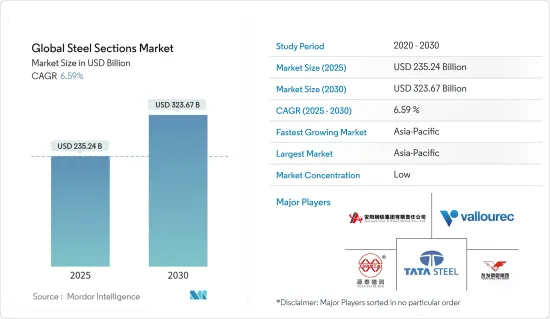

세계 철강 시장 규모는 2025년 2,352억 4,000만 달러, 2030년에는 3,236억 7,000만 달러에 이를 것으로 예측되고 있습니다. 예측 기간(2025-2030년)의 CAGR은 6.59%를 나타낼 전망입니다.

주요 하이라이트

모든 철강 생산국이 가입하는 세계철강협회(World Steel Association)에 따르면 세계의 철강 수요는 2024년에 1.9% 성장했습니다.

시장개척의 주요 요인으로는 건설 업계 수요 증가, 인프라 정비의 진전, 산업화의 진전 등을 들 수 있습니다.

세계 각국 정부는 도로, 교량, 철도 등의 인프라 개발 프로젝트에 상당액의 투자를 실시하고 있어 이것이 철강 수요를 끌어 올릴 가능성이 높습니다.

2023년 세계의 조강 생산량은 전년 대비 18억 8,820만 톤으로 2022년 18억 8,870만 톤을 웃돌았습니다. 그러나 2023년 12월 세계의 조강 생산량은 1억 3,570만 톤으로 전년 동기의 1억 4,330만 톤에서 5.3% 감소했습니다.

시장은 원료가격 변동, 무역보호주의, 환경규제 등의 과제에 직면하고 있습니다. 환경 규제는 철강 생산 비용을 증가시키고, 이는 강재 가격 상승을 통해 소비자에게 전가될 수 있습니다.

세계의 강재 시장 동향

지역별로는 아시아태평양이 더 많은 기회로 시장을 선도할 전망

아시아태평양은 여러 요인으로 인해 철강의 가장 큰 시장입니다. 이 지역은 세계적으로 가장 빠르게 경제 성장하는 지역 중 하나이며 건설, 인프라 및 제조 산업에서 철강 수요의 급증으로 이어지고 있습니다. 일부 출처에 따르면 이 지역 시장은 2024년에 3.5%에서 4.0%의 성장이 예측되고 있습니다.

중국은 세계 최고의 철강 제조 업체가되었습니다. 2021년 철강 생산량은 9억 4,300만 톤으로 세계 총 생산량 17억 5,000만 톤의 54%를 차지합니다.

중국의 철강 생산의 대부분(약 85%)은 BDF 공정에 의한 용광로에서 수행됩니다. 전기로(EAF)는 약 15%에 불과하며 고철을 사용하는 훨씬 "깨끗한" 프로세스입니다.

중국의 고철 공급과 국내 전력 가격은 향후 몇 년 동안 세계 EAF 생산의 중요한 촉매가 될 가능성이 높습니다. 중국 이외에서는 EAF 생산량이 전체 생산량에 차지하는 비율이 훨씬 크고 북미가 약 70%, 유럽이 40%를 차지하고 있습니다. 기후 변화 목표를 달성하기 위해 세계 EAF 증산과 보다 깨끗한 프로세스 개발이 추진되고 있습니다.

2022년 9월 중국 정부는 현지 제조업의 디지털화와 반합법화를 가속화하는 최신 개발 계획을 발표했습니다.

2026년 이후 중국에 있는 BMW의 자동차 공장은 HBIS 그린 스틸의 사용을 시작할 예정입니다. HBIS는 2050년까지 탄소 중립을 달성하겠다는 목표를 발표한 다음 해인 2022년 3월에 "저탄소 개발 기술 로드맵"을 발표했습니다. 탄소배출량을 줄이기 위해 2025년에는 정점 대비 10%, 2030년에는 30% 삭감하고, 2050년에 탄소 중립을 달성하기 위해, '6개의 기술 경로를 탐색하고 2개의 관리 플랫폼을 구축한다' 라고 하고 있습니다.

주택 부문은 앞으로 수년 만에 기세를 늘릴 것으로 예상

가처분 소득 증가와 건축 및 건설 프로젝트의 기술 진보에 의해 철강 시장은 향후 수년간 안정된 성장이 전망됩니다.

철강은 장거리를 넘는 우아하고 비용 효율적인 방법을 제공합니다.

스틸은 색상, 텍스처, 형상면에서 건축가에 의해 자유로운 디자인을 제공합니다. 그 강도, 내구성, 아름다움, 정밀도, 가단성에 의해 건축가는 아이디어를 탐구하고 혁신적인 솔루션을 개발하기 위한 폭넓은 파라미터를 얻을 수 있습니다.

세계의 철강 산업 개요

철강 시장은 분열화되어 있어 세계의 기업뿐만 아니라, 현지 및 지역의 기업도 복수 존재하고 있습니다. 시장은 공급망의 제약과 소비자 수요 변화에 따라 많은 변화를 경험하고 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

분석 방법

조사 단계

제3장 주요 요약

제4장 시장 역학

현재의 시장 시나리오

시장 개요

시장 역학

성장 촉진요인

억제요인

기회

밸류체인, 공급망 분석

Porter's Five Forces 분석

신규 참가업체의 위협

구매자·소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계

철강의 기술적 진보

각 강재의 생산과 수요에 관한 통찰

철강 시장의 가격 분석

시장에 대한 COVID-19의 영향

제5장 시장 세분화

제품 유형별

중량 구조용 강철

경량 구조용 강철

철근

최종 사용자 산업별

주택

제조업

항공우주 및 자동차

전력 및 유틸리티

건설

석유 및 가스

기타 최종 사용자 산업

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

라틴아메리카

브라질

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

기업 프로파일

Tata Steel

Vallourec

Yuantai Derun Group

Anyang Steel Group

Youfa Steel Pipe Group

ArcelorMittal SA

POSCO Holdings Inc.

Baoshan Iron & Steel Co. Ltd

Nippon Steel Corp.

Nucor Corp.

Ansteel Group

Hyundai Steel*

제7장 시장의 미래

제8장 부록

SHW

영문 목차

영문목차

The Global Steel Sections Market size is estimated at USD 235.24 billion in 2025, and is expected to reach USD 323.67 billion by 2030, at a CAGR of 6.59% during the forecast period (2025-2030).

Key Highlights

According to the World Steel Association, a body with membership in every steel-producing country, the demand for steel worldwide is expected to grow by 1.9% in 2024. Based on its short-range forecast, the World Steel Association reported that demand will rise to 1,849.1 mt by 2024. It had projected that the demand for crude steel would reach 1,831.5 mt in 2022, down by 4.3% compared to 2021.

Some of the key factors driving the market's growth include increasing demand from the construction industry, rising infrastructure development, and growing industrialization. Steel sections are an essential component of construction projects, and the growth of the construction industry is expected to drive the demand for steel sections.

Governments worldwide are investing heavily in infrastructure development projects, such as roads, bridges, and railways, which will likely boost the demand for steel sections. As of June 2023, Asia-Pacific accounted for more than USD 2.3 trillion of investments in road construction projects. In such projects, Europe ranked second, with investments amounting to around USD 700 million.

Compared to the previous year, crude steel production worldwide remained unchanged in 2023, with an output of 1,888.2 million ton over 1,888.7 million ton in 2022. However, in December 2023, crude steel production worldwide decreased by 5.3% to 135.7 million ton compared to 143.3 million ton in the same period of the previous year.

The market is facing some challenges, such as volatility in raw material prices, trade protectionism, and environmental regulations. Environmental regulations are increasing the cost of steel production, which can be passed on to consumers through higher prices for steel sections.

Global Steel Sections Market Trends

By Region, Asia-Pacific is Expected to Lead the Market with More Opportunities

Asia-Pacific is the largest market for steel sections due to several factors. The region has some of the fastest-growing economies globally, leading to a surge in demand for steel in the construction, infrastructure, and manufacturing industries. According to some sources, the regional market is projected to grow between 3.5% and 4.0% in 2024.

China has become the world's dominant steel manufacturer. The country produced 943 million metric ton of steel in 2021, 54% of the global total of 1.75 billion metric ton.

Most (about 85%) of China's steel production is done in blast furnaces using the BOF process. Only about 15% is electric-arc furnace (EAF), the far "cleaner" process that uses scrap steel.

The country's scrap steel supply and domestic power pricing will likely become key catalysts of EAF production worldwide in the coming years. Outside of China, EAF production accounts for a far greater proportion of the overall output, with North America at about 70% and Europe at 40%. There is a push to build more EAF and develop even cleaner processes to meet climate goals across the world.

In September 2022, the Chinese government announced its latest development plan to accelerate the digitalization and antilegalization of the local manufacturing industry. This move benefits the smart manufacturing industry, especially key industries like automobiles, petrochemicals, home appliances, and medical devices. The scale of the intelligent manufacturing equipment industry has reached almost CNY 3 trillion, satisfying more than 50% of market demand.

From 2026, BMW's car plants in China will begin to use HBIS green steel, which is produced via EAF with renewable-source electricity, with CO2 emissions cut by about 95%. This method will allow BMW to remove about 230,000 ton of CO2 emissions per year from the supply chain side. HBIS launched its Low Carbon Development Technology Roadmap in March 2022, a year after it announced the goal of achieving carbon neutrality by 2050. It said it would "explore six technology paths and build two management platforms" to cut carbon emissions by 10% from the peak in 2025 and by 30% in 2030 and achieve carbon neutrality in 2050.

The Residential Segment is Expected to Gain Momentum in the Coming Years

The steel sections market is expected to grow steadily in the coming years due to rising disposable incomes and technological advancements in building and construction projects. One of the major factors driving the market is the development of a construction index that aims to encourage the adoption of advanced construction methods using prefabricated components.

Steel sections provide an elegant, cost-effective method of spanning long distances. Extended steel spans can create large, open-plan, column-free internal spaces, with many clients now demanding column grid spacing over 15 meters. In single-story buildings, rolled beams provide clear spans of over 50 meters.

Steel offers architects more design freedom in terms of color, texture, and shape. Its strength, durability, beauty, precision, and malleability give architects broader parameters to explore ideas and develop innovative solutions. Steel's long-spanning ability gives rise to large open spaces free of intermediate columns or load-bearing walls.

Global Steel Sections Industry Overview

The steel sections market is fragmented, with the presence of several local and regional players, as well as global players. Some of the major players include Tata Steel, Vallourec, Yuantai Derun Group, Anyang Steel Group, and Youfa Steel Pipe Group. The market is going through many changes due to supply chain constraints and a shift in demand among consumers. Companies are working on increasing their production capacities and improving the quality of products through technological advancements.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

2.1 Analysis Methodology

2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS DYNAMICS

4.1 Current Market Scenario

4.2 Market Overview

4.3 Market Dynamics

4.3.1 Drivers

4.3.2 Restraints

4.3.3 Opportunities

4.4 Value Chain/Supply Chain Analysis

4.5 Porter's Five Forces Analysis

4.5.1 Threat of New Entrants

4.5.2 Bargaining Power of Buyers/Consumers

4.5.3 Bargaining Power of Suppliers

4.5.4 Threat of Substitute Products

4.5.5 Intensity of Competitive Rivalry

4.6 Technological Advancements in Steel Sections

4.7 Insights on Production and Demand for Different Steel Sections