인도의 콘크리트 혼화제 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

India Concrete Admixtures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693691

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

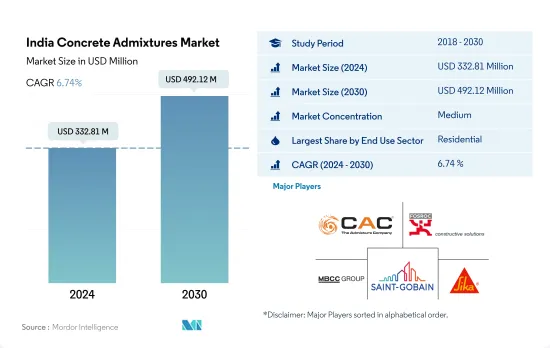

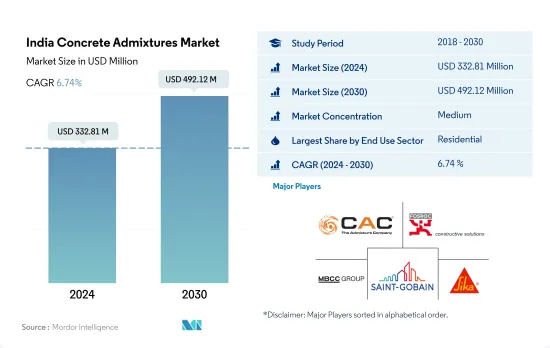

인도의 콘크리트 혼화제 시장 규모는 2024년 3억 3,281만 달러로 추정되고, 2030년에는 4억 9,212만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2030년) CAGR 6.74%로 성장할 것으로 예측됩니다.

외국투자 유치와 경제 성장 추진에 주력하는 인도가 시장 성장에 영향을 미칠 것

콘크리트 혼화제 시장은 2022년에 크게 급증했으며, 2021년의 값을 8.15% 웃돌았습니다.

콘크리트가 인도의 대부분의 주택 건축물의 기초 재료라는 것을 고려하면, 2022년에 콘크리트 혼화제 수요와 금액이 주택 부문을 지배한 것은 놀라운 일이 아닙니다. 이 수요에 한층 더 박차를 가하고 있는 것이, 인도의 도시 인구의 일관한 증가입니다.

2022년에는 인프라 부문이 콘크리트 혼화제 시장의 제2위 공헌자로 부상했지만, 이것은 인도가 인프라 개척에 힘을 쏟고 있다는 증거입니다. 예를 들어, 2022년의 인프라 지출은 전년 대비 3.09% 증가하여 2019-2023년까지 약 1조 4,000억 달러를 인프라 프로젝트에 투자한다는 국가의 계획과 일치하고 있습니다.

새로운 상업 빌딩의 건설은 2023-2030년의 예측 기간 동안 CAGR 5.26%를 기록할 전망입니다.

인도의 콘크리트 혼화제 시장 동향

인도의 A등급 오피스 시장은 2030년까지 12억 평방 피트에 이를 것으로 예상되며 상업 건축 부문 수요를 견인할 가능성이 높습니다.

2022년, 인도의 신규 상업층 면적은 2021년 대비 6.2%의 수량 증가가 되었습니다. 쇼핑몰 스페이스는 260만 평방 피트를 넘어 2021년부터 27% 증가 2023년을 전망하면 외국직접투자(FDI)의 급증이 새로운 오피스, 소매점, 기타 시설의 필요성을 부추겼으며, 이 섹터의 신규 바닥면적은 3,800만 평방피트 급증할 것으로 예측됩니다.

2020년 인도 상업시설의 신설 바닥 면적은 2019년 대비 68.3% 감소했습니다. 그러면 신규 바닥 면적이 약 5억 2,600만 평방 피트 급증하고, 대폭적인 회복이 보였습니다.

2030년을 전망하면 인도 상업시설의 신설 바닥 면적은 3억 5,800만 평방 피트에 달할 것으로 예측되며, 2023년부터 크게 급증합니다. 예를 들어, 상위 7개 도시의 인도 A등급 오피스 시장은 2026년까지 10억 평방 피트로 확대되어, 2030년까지 12억 평방 피트로 확대될 예정입니다. 5.26%라는 견조한 성장을 기록하는 전망입니다.

주택 수요 증가와 부동산 섹터 확대로 주택 섹터 수요 증가

2022년, 인도의 주택 바닥 면적은 전년을 웃도는 9.4%의 성장을 나타냈습니다. 2023년 1분기에는 이들 도시의 주택 판매 호수는 11.4만호에 달했고, 전년보다 9.95만호 이상 급증했습니다.

2020년 인도의 주택 섹터는 후퇴에 직면해 신설 바닥 면적은 전년 대비 6.25% 감소했습니다. 이 감소는 전국적인 봉쇄, 공급망 혼란, 노동력 부족, 건설 생산성 저하, 외국 투자 침체로 인한 것입니다. 그러나 2021년에는 인도의 주택 부동산 시장이 회복되어 상위 7개 도시에서 약 16만 3,000호의 신축 주택이 증가했습니다. 이러한 급증으로 2021년 주택 섹터의 신설 바닥 면적은 2020년 대비 약 6억 4,900만 평방 피트로 크게 증가했습니다.

향후 인도의 주택 섹터는 2023-2030년까지 수량 기준으로 2.95%의 연평균 복합 성장률(CAGR)을 보여주는 전망입니다. 이 성장은 지속적인 주택 수요, 투자 증가, 유리한 정부 시책 때문입니다. 특히 2030년까지 인도 인구의 40% 이상이 도시에 거주하게 되어, 저렴한 주택이 약 2,500만호 추가되는 수요가 높아질 것으로 예측되고 있습니다. 게다가 2030년까지 주택 부동산 시장은 주요 도시에서 150만 호에 달할 것으로 예상되고 있으며, 이 부문 수요를 더욱 촉진하고 있습니다.

인도 콘크리트 혼화제 산업 개요

인도의 콘크리트 혼화제 시장은 적당히 통합되어 상위 5개사에서 52.50%를 차지하고 있습니다. 이 시장의 주요 기업은 CAC Admixtures, Fosroc, Inc., MBCC Group, Saint-Gobain, Sika AG 등입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 용도 부문의 동향

상업

산업 및 시설

인프라

주택용

주요 인프라 프로젝트(현재로 발표됨)

규제 프레임워크

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 용도 부문

상업

산업 및 시설

인프라

주택용

서브 제품

촉진제

공기 혼입 혼화제

고범위 감수제(초가소제)

리타더

수축 저감 혼화제

점도 조정제

감수제(가소제)

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

CAC Admixtures

Chembond Chemicals Limited

Don Construction Products Ltd.

ECMAS Group

Fosroc, Inc.

MAPEI SpA

MBCC Group

MC-Bauchemie

Saint-Gobain

Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The India Concrete Admixtures Market size is estimated at 332.81 million USD in 2024, and is expected to reach 492.12 million USD by 2030, growing at a CAGR of 6.74% during the forecast period (2024-2030).

India's focus on attracting foreign investment and propelling economic growth to influence the market's growth

The market for concrete admixtures witnessed a significant surge in 2022, surpassing its 2021 value by 8.15%. This growth was primarily propelled by a nationwide uptick in construction activities. A 5% increase in the demand for concrete admixtures was projected for 2023, with the infrastructure and commercial sectors spearheading this surge.

Given that concrete is a cornerstone material in the majority of residential buildings in India, it comes as no surprise that the residential segment dominated the demand and value for concrete admixtures in 2022. This demand is further fueled by India's consistently rising urban population. Notably, the urban population in 2022 and 2021 saw a 2.1% and 2.2% increase, respectively, compared to the preceding years.

In 2022, the infrastructure sector emerged as the second-largest contributor to the concrete admixtures market, a testament to India's heightened focus on infrastructure development. This emphasis has translated into a notable surge in the demand for concrete admixtures. For instance, in 2022, infrastructure spending saw a 3.09% increase from the previous year, aligning with the nation's plan to invest approximately USD 1.4 trillion in infrastructure projects spanning 2019-2023.

The construction of new commercial buildings is poised to witness a CAGR of 5.26% during the forecast period of 2023-2030. This momentum can be attributed to India's burgeoning economy and the anticipated influx of investments from foreign companies. Within the commercial segment, the growth is expected to be even more pronounced, with a projected CAGR of 8.04% during the forecast period.

India Concrete Admixtures Market Trends

India's Grade A office market is expected to reach 1.2 billion sq. ft by 2030 and is likely to drive the demand for the commercial construction sector

In 2022, India's new commercial floor area saw a 6.2% volume growth compared to 2021. The retail sector, particularly in the top seven cities (Delhi NCR, Bangalore, Hyderabad, Mumbai, Pune, Chennai, and Kolkata), witnessed robust demand, adding over 2.6 million sq. ft of mall space, a 27% increase from 2021. Looking ahead to 2023, the sector's new floor area is expected to surge by 38 million sq. ft, driven by a surge in foreign direct investment (FDI) fueling the need for new offices, retail outlets, and other facilities. Notably, the FDI equity inflow for construction development in 2023 was projected to hit USD 96 million.

In 2020, India's commercial new floor area plummeted by 68.3% in volume compared to 2019. This decline was primarily due to a nationwide lockdown imposed by the government, which disrupted ongoing projects, strained supply chains, and impacted labor availability. However, as restrictions eased in 2021, the country witnessed a significant rebound, with the new floor area surging by approximately 526 million sq. ft. Additionally, 2021 saw a notable uptick in green building initiatives, with around 55% of commercial projects embracing sustainability, further bolstering the demand for the sector.

Looking ahead to 2030, India's commercial new floor area is projected to hit 358 million sq. ft, a significant jump from 2023. This surge drives a growing appetite for shopping malls, office spaces, and other commercial facilities. For instance, India's Grade A office market in the top seven cities is set to expand to 1 billion sq. ft by 2026 and further to 1.2 billion sq. ft by 2030. Consequently, the country's commercial new floor area is poised to witness a robust CAGR of 5.26% during the forecast period.

Rise in demand for housing units and increasing real estate sector to boost residential sector demand

In 2022, India witnessed a 9.4% growth in residential floor area, outpacing the previous year. The demand for housing in the country surged, with the top seven cities (Delhi NCR, Bangalore, Hyderabad, Mumbai, Pune, Chennai, and Kolkata) collectively adding approximately 402,000 new units, marking a 44% increase from 2021. In Q1 2023, housing sales in these cities reached 1.14 lakh units, a staggering jump of over 99,500 units from the previous year. Consequently, it was projected that the residential new floor area in India would expand by approximately 71 million sq. ft in 2023 compared to 2022.

In 2020, the residential sector in India faced a setback, witnessing a 6.25% decline in new floor area compared to the previous year. This decline was attributed to the nationwide lockdown, disruptions in the supply chain, labor shortages, reduced construction productivity, and a dip in foreign investments. However, in 2021, the Indian residential real estate market rebounded, adding around 163,000 new residential units across the top seven cities. This surge translated into a significant increase of about 649 million sq. ft in the residential sector's new floor area in 2021 compared to 2020.

Looking ahead, the residential sector in India is poised to exhibit a CAGR of 2.95% in terms of volume from 2023 to 2030. This growth can be attributed to sustained housing demand, increased investments, and favorable government policies. Notably, by 2030, it is projected that over 40% of India's population will reside in urban areas, driving a demand for approximately 25 million additional affordable housing units. Furthermore, by 2030, the residential real estate market is expected to hit 1.5 million units in key cities, further fueling the demand in the sector.

India Concrete Admixtures Industry Overview

The India Concrete Admixtures Market is moderately consolidated, with the top five companies occupying 52.50%. The major players in this market are CAC Admixtures, Fosroc, Inc., MBCC Group, Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End Use Sector Trends

4.1.1 Commercial

4.1.2 Industrial and Institutional

4.1.3 Infrastructure

4.1.4 Residential

4.2 Major Infrastructure Projects (current And Announced)

4.3 Regulatory Framework

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

5.1 End Use Sector

5.1.1 Commercial

5.1.2 Industrial and Institutional

5.1.3 Infrastructure

5.1.4 Residential

5.2 Sub Product

5.2.1 Accelerator

5.2.2 Air Entraining Admixture

5.2.3 High Range Water Reducer (Super Plasticizer)

5.2.4 Retarder

5.2.5 Shrinkage Reducing Admixture

5.2.6 Viscosity Modifier

5.2.7 Water Reducer (Plasticizer)

5.2.8 Other Types

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles

6.4.1 CAC Admixtures

6.4.2 Chembond Chemicals Limited

6.4.3 Don Construction Products Ltd.

6.4.4 ECMAS Group

6.4.5 Fosroc, Inc.

6.4.6 MAPEI S.p.A.

6.4.7 MBCC Group

6.4.8 MC-Bauchemie

6.4.9 Saint-Gobain

6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

8.1 Global Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)