ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

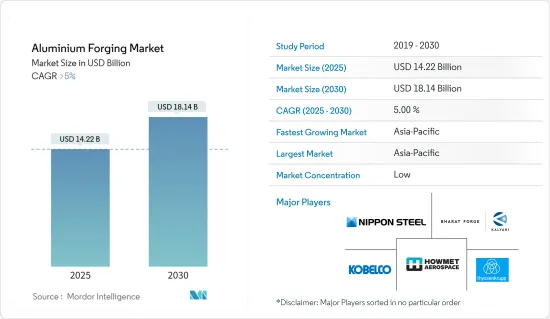

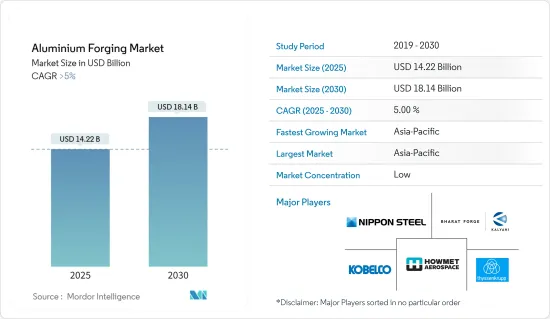

세계의 알루미늄 단조 시장 규모는 2025년 142억 2,000만 달러로 추정되며 예측 기간 중(2025-2030년) CAGR 5%를 넘을 것으로 예상되며 2030년에는 181억 4,000만 달러에 달할 것으로 예측되고 있습니다.

알루미늄 단조 시장은 COVID-19에 의한 후퇴에 직면했습니다. 세계의 록다운과 엄격한 정부 규제에 의해 생산 거점이 광범위하게 폐쇄되었습니다.

주요 하이라이트

단기적으로는 산업 부문에서의 경량 재료의 사용 확대와 자동차 및 운송 산업에서의 수요 증가가 조사 대상 시장 수요를 견인하는 주요인입니다.

그러나 알루미늄 가격의 변동과 엄격한 품질 기준이 시장 성장의 방해가 될 것으로 예측됩니다.

단조 기술이나 시뮬레이션 기술의 진보는 동 시장에 새로운 기회를 가져올 것으로 기대되고 있습니다.

아시아태평양은 중국과 인도 수요가 대부분을 차지하고 세계 시장을 독점할 것으로 예측됩니다.

알루미늄 단조 시장 동향

자동차 및 운송 부문이 시장을 독점

알루미늄은 자동차 부문에서 널리 사용되고 있습니다. 엔진 라디에이터, 휠, 범퍼, 서스펜션 요소, 엔진 실린더 블록, 기어 박스 바디, 도어, 프레임 등의 부품에 필수적입니다.

또한, 단조 알루미늄 부품은 자동차 부문에서 매우 중요합니다. 산업이 연비 효율, 경량화, CO2 배출량의 억제를 중시하는 가운데, 현대의 자동차에 있어서의 알루미늄의 중요성은 급상승하고 있습니다.

알루미늄의 충격 흡수 능력은 강철의 2배이기 때문에 선호되는 선택사항이 되고 있습니다.

2023년, 자동차 산업은 견조한 경기 확대와 소비자의 기호의 진화에 힘입어 큰 성장을 이루었습니다. 국제자동차제조기구(OICA)의 데이터에 따르면, 승용차와 상용차를 합친 세계의 자동차 생산 대수는 약 9,355만대였습니다.

2023년에는 아시아태평양의 상용차 신차 판매 대수는 2022년 대비 10.9% 증가하여 2022년 717만대에 대해 2023년에는 796만대가 등록되었습니다.

그러나 인도에서는 상용차(CV) 판매량은 2024년도에 2-5%의 소폭 성장을 보인 후 2024-25년도(25년도)는 떨어질 것으로 예측되고 있습니다. ICRA(Investment Information and Credit Rating Agency of India Limited)의 데이터에서는 25년도는 4-7%의 감소가 전망되고 있습니다.

북미의 2023년 자동차 판매 대수는 1,919만대에 달했고, 2022년의 1,693만대에서 13.4% 증가했습니다. 그 내역은 승용차가 398만대, 상용차가 1,521만대, 나머지가 대형 트럭, 버스, 코치입니다.

또한 유럽 자동차 공업회의 데이터에 따르면 2023년 유럽 신차 등록 대수는 18.7% 급증합니다. 승용차 판매량은 1,500만대, 상용차는 290만대에 이르며, 각각 2022년 1,264만대, 244만대에서 증가했습니다.

2024년 1분기 영국 무역산업은 10만 4,000건의 상용차 등록을 기록해 전년 동기 대비 59% 증가하는 현저한 성장세를 보였습니다.

OICA의 데이터에 따르면 브라질의 2023년 소형 상용차 생산 대수는 42만 2,000대로 전년 대비 20% 증가했으며 시장 성장을 뒷받침하고 있습니다.

또한 사우디아라비아에서는 상용차 시장의 변화를 볼 수 있습니다. 경제의 다양화와 인프라의 근대화에 따라, 특히 NEOM이나 홍해 프로젝트와 같은 메가 프로젝트가 진행 중이며, 선진적인 상용차에 대한 수요가 높아지고 있습니다.

비전 2030의 목표를 향해 사우디아라비아의 상용차 섹터는 빠르게 발전하고 있습니다. 미국 사우디아라비아 비즈니스 평의회의 예측에 따르면 신속한 인프라 개척과 선진적 물류 솔루션에 대한 수요가 증가함에 따라 시장은 2025년까지 67억 달러에 달한다고 합니다.

이러한 역학을 고려하면 시장은 예측 기간 동안 크게 성장할 준비가 되어 있습니다.

아시아태평양이 시장을 독점

아시아태평양은 알루미늄 단조 시장을 선도하고 예측 기간 중에 가장 급성장하는 지역이 될 전망입니다.

알루미늄 단조 부품은 고강도, 경량, 내식성이 뛰어나 고층 빌딩이나 오피스 타워 등의 고층 건축물에는 빠뜨릴 수 없습니다.

2030년까지 도시화율 70%를 목표로 하는 중국의 도시화 추진은 주택 수요와 중간층의 생활 수준 향상에 대한 소망을 강조하고 있습니다.

2024년 인도에서는 저렴한 주택이 70% 증가할 것으로 예측됩니다. Invest India에 따르면 건설 부문은 2025년까지 1조 4,000억 달러의 평가액을 달성할 것으로 예측되고 있습니다. 적당한 가격의 주택이 급무가 되고 있습니다. 부동산법, GST(물품 서비스세), REIT(부동산 투자 신탁)등의 최근의 개혁은 인가를 신속화해, 건설 산업을 강화하는 것을 목적으로 하고, 시장의 성장을 가속하고 있습니다.

알루미늄 단조 부품은 항공우주 부문에서 중요한 역할을 하고 있으며, 기체, 날개, 제어면 등의 구조 부품에 사용되고 있습니다.

중국은 세계의 항공우주부문에서 두드러지고 있어 항공기 제조와 국내 항공 여행을 리드하고 있습니다.

국제무역국(ITA)의 데이터에 따르면, 중국은 세계 제2위의 민간 항공우주 시장입니다.

알루미늄 단조 부품은 자동차의 경량화에 극히 중요한 역할을 하고, 연비를 향상시키고, 배출가스를 억제합니다.

인도에서는 인도 자동차 공업회(SIAM)의 데이터에 따르면 2024년 1월부터 3월까지의 승용차, 상용차, 삼륜차, 사륜차의 생산 대수는 739만대에 달했습니다.

알루미늄 단조는 그 강도 대 중량비, 내식성, 내구성으로 진중되어 산업기계에 널리 응용되고 있습니다.

인도 상무부의 데이터에 따르면 2023 회계연도의 수출액에서는 전기기계기구가 최대였고 낙농, 식품가공, 섬유용 산업기계가 약간 차이가 있어 80억 달러를 넘어섰습니다.

단조 알루미늄 부품은 경량화와 에너지 소비의 삭감에 의해 전자·계장 부품의 성능을 향상시키고 있습니다.

일본전자정보기술산업협회의 데이터에 따르면 일본의 일렉트로닉스 산업은 2024년 1월부터 6월까지 5,452억 5,600만엔(약 33억 8,600만 달러) 상당의 제품을 생산해, 전년 동기 대비 104.7%라는 현저한 성장을 보였습니다.

이러한 동태를 생각하면, 아시아태평양은 예측 기간 중에 알루미늄 단조 수요가 급증하게 됩니다.

알루미늄 단조 산업 개요

알루미늄 단조 시장은 세분화되어 있습니다. 주요 기업(특별한 순서 없음)에는 Howmet Aerospace, Bharat Forge, Thyssenkrupp AG, Kobe Steel, Ltd., Nippon Steel Corporation 등이 포함됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

산업 부문에서 경량 재료의 사용 확대

자동차 및 운송 산업에서의 수요 증가

기타 촉진요인

성장 억제요인

알루미늄 가격 변동

엄격한 품질 기준

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

단조 유형

오픈 다이 단조

클로즈 다이 단조

링 롤 단조

최종 사용자 산업

항공우주 및 방위

자동차 및 운송

산업기계

건설

기타 최종 사용자 산업(전자 및 계측 기기, 에너지 파워, 농업 및 농촌)

지역

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

튀르키예

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

카타르

아랍에미리트(UAE)

나이지리아

이집트

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

Accurate Steel Forgings(INDIA) Limited

Al Forge Tech Co., Ltd.

All Metals & Forge Group

Aluminum Precision Products

Anchor Harvey

Anderson Shumaker Company

Bharat Forge

Ellwood Group Inc.

Howmet Aerospace

ILJIN Co., Ltd.

Kobe Steel, Ltd.

Nippon Steel Corporation

Norsk Hydro ASA

Ramkrishna Forgings Ltd

Scot Forge Company

Thyssenkrupp AG

Wheel India Limited

제7장 시장 기회와 앞으로의 동향

첨단 단조 기술과 시뮬레이션 기술

기타 기회

JHS

영문 목차

영문목차

The Aluminium Forging Market size is estimated at USD 14.22 billion in 2025, and is expected to reach USD 18.14 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The aluminum forging market faced setbacks due to COVID-19. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021 and is projected to see significant growth in the upcoming years.

Key Highlights

Over the short term, the growing use of lightweight materials in the industrial sector and increasing demand from the automotive and transportation industries are the major factors driving the demand for the market studied.

However, fluctuations in aluminum prices and stringent quality standards are expected to hinder the market's growth.

Nevertheless, advanced forging techniques and simulation technologies is expected to create new opportunities for the market studied.

Asia-Pacific region is expected to dominate the market across the world, with the majority of demand coming from China and India.

Aluminum Forging Market Trends

Automotive and Transportation Segment to Dominate the Market

Aluminum is extensively used in the automotive sector. It's integral to components like engine radiators, wheels, bumpers, suspension elements, engine cylinder blocks, gearbox bodies, and body parts, including hoods, doors, and frames. Valued for its lightweight nature, durability, and aesthetic appeal, aluminum is especially favored for exterior components.

Moreover, forged aluminum components are pivotal in the automotive realm. With the industry's emphasis on fuel efficiency, weight reduction, and curbing CO2 emissions, aluminum's significance in contemporary vehicles has surged. Every kilogram of aluminum reduces the vehicle's weight, prompting a growing reliance on aluminum for car parts and subsequently boosting market demand.

Aluminum's shock-absorbing capabilities, being twice as effective as steel, make it a preferred choice. This efficacy has led manufacturers to use aluminum in bumpers consistently. Additionally, aluminum bodies offer enhanced safety; when aluminum parts deform, the change is localized to the impact area, unlike steel, which maintains the overall shape, ensuring passenger safety.

In 2023, the automotive industry experienced significant growth, buoyed by robust economic expansion and evolving consumer preferences. Data from the Organisation Internationale des Constructeurs d'Automobiles (OICA) reveals a production of approximately 93.55 million units of vehicles worldwide, encompassing both passenger cars and commercial vehicles. This marked a notable uptick from the roughly 84.83 million units of vehicles produced in 2022, translating to a growth rate of about 10.26%.

In 2023, the Asia Pacific region witnessed 10.9% increase in new commercial vehicle sales compared to 2022, with 7.96 million units registered in 2023, compared to 7.17million units in 2022.

However, in India, commercial vehicle (CV) sales are projected to dip in the financial year 2024-25 (FY 25) after a modest 2-5% growth in FY24. As per the data from ICRA (Investment Information and Credit Rating Agency of India Limited) forecasts a 4-7% decline in FY25.

North America saw motor vehicle sales reach 19.19 million units in 2023, a 13.4% rise from 2022's 16.93 million units, as reported by OICA. Of the total, passenger cars comprised 3.98 million units, commercial vehicles accounted for 15.21 million units, with the remainder being heavy trucks, buses, and coaches.

Furthermore, as per the data from the European Automobile Manufacturers Association highlights an 18.7% surge in new motor vehicle registrations in Europe for 2023. Passenger car sales hit 15 million units, while commercial vehicles reached 2.90 million units, both up from 2022's 12.64 million and 2.44 million units, respectively.

In the first quarter of 2024, the United Kingdom's trade industry recorded 104,000 commercial registrations, a notable 59% increase year-on-year, bolstered by the Ministry of Commerce's issuance of 65,363 permits in the same quarter of 2023.

OICA data highlights Brazil's light commercial vehicle production at 422 thousand units in 2023, a 20% increase from the previous year, underscoring the market's growth.

Moreover, Saudi Arabia is witnessing a transformation in its commercial vehicle market. As the nation diversifies its economy and modernizes its infrastructure, there's a growing demand for advanced commercial vehicles, especially with mega projects like NEOM and the Red Sea Project underway.

Racing towards its Vision 2030 goals, Saudi Arabia's commercial vehicle sector is rapidly evolving. Projections suggest the market will reach USD 6.7 billion by 2025, driven by swift infrastructure developments and a rising demand for advanced logistics solutions, as per the U.S.-Saudi Arabian Business Council.

Given these dynamics, the market is poised for significant growth during the forecast period.

Asia-Pacific Region to Dominate the Market

Asia-Pacific is poised to lead the aluminum forging market, emerging as the region with the fastest growth during the forecast period. This surge is primarily fueled by rising demands in sectors like aerospace and defense, automotive and transportation, industrial machinery, and construction, particularly in nations such as China, India, South Korea, Japan, and various Southeast Asian countries.

Owing to their high strength, lightweight nature, and corrosion resistance, forged aluminum parts are integral to high-rise buildings, including skyscrapers and office towers. These parts can endure harsh environmental conditions, minimizing maintenance and repair needs. With the region's construction sector expanding, the demand for aluminum forging is set to increase in the coming years.

China's urbanization drive, targeting a 70% urban rate by 2030, underscores the demand for housing and the middle class's aspirations for improved living standards. These trends are poised to invigorate the housing market and residential construction, benefiting the aluminum forging market.

In 2024, India is set to witness a 70% surge in the availability of affordable housing. According to Invest India, the construction sector is projected to attain a valuation of USD 1.4 trillion by 2025. With forecasts suggesting that over 30% of the population will be urban dwellers by 2030, there's a pressing need for 25 million more mid-end and affordable housing units. Recent reforms, such as the Real Estate Act, GST (Goods and Services Tax) and REITs (Real Estate Investment Trusts), aim to expedite approvals and strengthen the construction industry, driving market growth.

Forged aluminum parts play a crucial role in aerospace, being used in structural components like fuselages, wings, and control surfaces. These parts enhance aircraft and spacecraft performance by lightening engine and structural components. As the aerospace sector expands in the region, the demand for aluminum forging is projected to grow.

China stands out in the global aerospace arena, leading in aircraft manufacturing and domestic air travel. The nation's aircraft parts and assembly sector is rapidly expanding, boasting over 200 small parts manufacturers.

As per the data from the International Trade Administration (ITA), China is the second-largest civil aerospace market globally. As of January 2024, the National Bureau of Statistics of China and the Civil Aviation Administration of China reported 7,351 civil aircraft, an increase of over 550 airplanes from 2022.

Forged aluminum parts play a pivotal role in reducing vehicle weight, which in turn boosts fuel efficiency and curtails emissions. Beyond weight reduction, these components enhance vehicle safety by lightening the body and reinforcing the chassis. Given the uptick in vehicle production in the region, the demand for aluminum forging is set to rise.

In India, data from the Society of Indian Automobile Manufacturers (SIAM) indicates that from January to March 2024, the production of passenger vehicles, commercial vehicles, three wheelers, two wheelers and quadricycle reached 7.39 million units. Specifically, sales for passenger and commercial vehicles were 1.14 million and 268 thousand units, respectively.

Aluminum forging finds extensive application in industrial machinery, prized for its strength-to-weight ratio, corrosion resistance, and durability. Common applications include gears, gearboxes, pumps, valves, bearings, and bushings. As demand for industrial machinery rises, so too will the market's demand for aluminum forging.

Data from India's Department of Commerce highlights that in the 2023 fiscal year, electric machinery and equipment topped the export value charts, followed closely by industrial machinery for dairy, food processing, and textiles, exceeding USD 8 billion. Looking ahead, exports of electrical machinery and equipment are expected to reach nearly USD 12.4 billion in the 2024 fiscal year.

Forged aluminum parts enhance the performance of electronic and instrumentation components by reducing weight and energy consumption. With the electronics sector booming in Asia-Pacific, the demand for aluminum forging in this domain is set to escalate.

Data from the Japan Electronics and Information Technology Industries Association reveals that Japan's electronics industry produced goods worth JPY 5,452,56 million (~USD 3,386 million) from January to June 2024, marking a remarkable 104.7% growth compared to the same period the previous year.

Given these dynamics, the Asia-Pacific region is poised for a surge in aluminum forging demand during the forecast period.

Aluminum Forging Industry Overview

The aluminum forging market is fragmented in nature. The major players (not in any particular order) include Howmet Aerospace, Bharat Forge, Thyssenkrupp AG, Kobe Steel, Ltd., and Nippon Steel Corporation, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Use of Lightweight Material in Industrial Sector

4.1.2 Increasing Demand from the Automotive and Transportation Industry

4.1.3 Other Drivers

4.2 Restraints

4.2.1 Fluctuations in Aluminum Prices

4.2.2 Stringent Quality Standards

4.2.3 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Forging Type

5.1.1 Open Die Forging

5.1.2 Close Die Forging

5.1.3 Ring Rolled Forging

5.2 End-User Industry

5.2.1 Aerospace and Defense

5.2.2 Automotive and Transportation

5.2.3 Industrial Machinery

5.2.4 Construction

5.2.5 Other End-user Industries (Electronics and Instrumentation, Energy Power, Agriculture and Farming)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 Nordic Countries

5.3.3.7 Turkey

5.3.3.8 Russia

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 Qatar

5.3.5.3 United Arab Emirates

5.3.5.4 Nigeria

5.3.5.5 Egypt

5.3.5.6 South Africa

5.3.5.7 Rest of Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%) **/ Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Accurate Steel Forgings (INDIA) Limited

6.4.2 Al Forge Tech Co., Ltd.

6.4.3 All Metals & Forge Group

6.4.4 Aluminum Precision Products

6.4.5 Anchor Harvey

6.4.6 Anderson Shumaker Company

6.4.7 Bharat Forge

6.4.8 Ellwood Group Inc.

6.4.9 Howmet Aerospace

6.4.10 ILJIN Co., Ltd.

6.4.11 Kobe Steel, Ltd.

6.4.12 Nippon Steel Corporation

6.4.13 Norsk Hydro ASA

6.4.14 Ramkrishna Forgings Ltd

6.4.15 Scot Forge Company

6.4.16 Thyssenkrupp AG

6.4.17 Wheel India Limited

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Advanced Forging Techniques and Simulation Technologies