북미의 배터리 관리 시스템 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

North America Battery Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693670

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

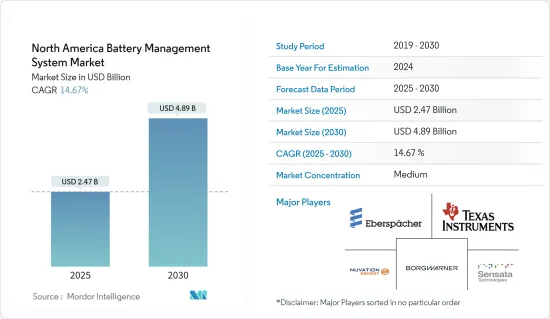

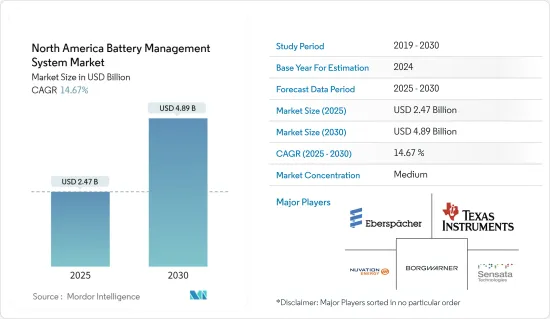

북미의 배터리 관리 시스템 시장 규모는 2025년에 24억 7,000만 달러, 예측 기간(2025-2030년)의 CAGR은 14.67%, 2030년에는 48억 9,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

중기적으로는 ESS에서의 리튬이온 전지의 사용에 관한 안전성에 대한 우려의 고조와 전기자동차의 보급이, 예측 기간중의 혁신적이고 효율적인 전지 관리 시스템(BMS) 수요를 촉진할 것으로 예측됩니다.

한편, 기성품의 배터리 관리 시스템에는 한계가 있기 때문에 현재의 설계는 시대 지연이 되어, 예측 기간중 시장 조사에 영향을 미칠 것으로 예측됩니다.

하지만 인공지능을 통합한 배터리 관리 시스템의 기술적 진보는 복잡성 완화, 효율 향상, 신뢰성 개선 등의 장점을 제공하여 미래의 성장 기회를 가져올 것으로 예측됩니다.

미국은 에너지저장시스템과 전기자동차의 2개의 산업으로부터의 높은 수요에 의해 예측기간 중에 시장을 독점할 것으로 예측됩니다.

북미 배터리 관리 시스템 시장 동향

시장을 독점할 것으로 예상되는 운송 부문

이전에는 내연 기관차(ICE)만이 사용되고 있었습니다.그러나, 환경 문제에 대한 관심이 높아짐에 따라, 기술은 전기자동차(EV)로 전환되고 있습니다.

리튬 이온 배터리는 높은 에너지 밀도, 낮은 자기 방전, 경량, 낮은 유지 보수를 실현하기 위해 주로 전기자동차에 사용되고 있습니다. 내연 기관 자동차에서는 납 기반 배터리가 널리 사용되고 있습니다. 당분간 유일한 대중시장 배터리 시스템으로 계속될 것으로 예측됩니다.

리튬 이온 배터리 시스템은 플러그인 하이브리드 자동차 및 전기자동차를 추진합니다. 제품 제조업체의 요구 사항을 충족할 수 있는 유일한 사용 가능한 기술입니다.

멕시코에서는 전기자동차 제조시장이 급성장하고 있습니다. 특히, 테슬라가 멕시코에 50억 달러 규모의 기가팩토리를 건설할 계획이어서, 멕시코는 전기차 생산의 중심지가 될 것으로 예상됩니다.

또한 2024년 2월에는 중국의 유명한 전기자동차(EV) 제조업체인 BYD가 멕시코에 새로운 제조공장을 설립 중임을 발표했습니다.

미국과 마찬가지로 캐나다의 자동차 산업도 전환기를 맞이하고 있으며, 대부분의 자동차 제조업체가 신공장의 설립이나 구공장의 EV생산에의 재이용에 의해 전기차를 생산하는 방식으로 전환하고 있습니다.

예를 들어, Honda Motor는 2024년 4월, 온타리오주의 전기자동차 및 배터리 생산 공장에 110억 달러를 투입해, 현재의 생산 체제를 증강한다고 발표했습니다. 캐나다에 있어서 가장 대규모 투자가 될 것입니다. 이 구상은 2028년까지 운영을 개시하는 것을 목표로 하고 있어, 최대 24만대의 전기자동차 연간 생산 능력을 전망하고 있습니다.

에너지 정보기관(EIA)에 따르면 2023년 현재 캐나다의 전기자동차 재고는 약 3만 8,000대로 2022년에 기록된 재고 대수에서 35.71% 가까이 증가하고 있습니다.

이와 같이, 상기 요인으로부터, 예측 기간중 수송 분야가 북미의 배터리 관리 시스템 시장을 독점할 가능성이 높습니다.

미국이 시장을 독점할 전망

미국은 2023년에는 에너지 저장 시스템과 전기자동차의 세계 최대 시장 중 하나가 될 것으로 예측되었습니다.

미국은 세계에서 가장 발달한 자동차 산업 중 하나입니다. 기후와 환경에 대한 우려가 높아지는 가운데, 미국 대부분의 자동차 제조업체는 전기자동차의 생산을 우선하고 있습니다. 또한 미국 정부는 화석 연료에의 의존도와 배출량을 줄이기 위해, 전기자동차의 보유 대수를 늘리는 것에 주력하고 있습니다.

에너지 정보기관(EIA)에 따르면, 2023년 시점의 미국의 EV 재고 대수는 약 350만대로, 2022년의 재고 대수로부터 66.67% 가까이 증가해, 중국에 이어 세계 제2위의 EV 시장이 되고 있습니다.

2023년 시점의 재생 가능 에너지 용량은 약 387.54GW로, 전년 대비 약 8.7% 증가했습니다. 2030년까지 청정 에너지의 80% 신규 발전 용량을 포함한 목표를 통해 증가할 가능성이 높습니다.

이러한 재생 가능 에너지 발전의 급속한 증가로 송전망에 재생 가능 에너지가 고도로 통합되어 있는 국가에서는 송전망의 안정성이 큰 문제가 되고 있습니다. 이들은 본질적으로 변동하는 에너지원입니다. 에너지 저장 시스템은 재생 가능 에너지 발전을 발전량이 많은 시간대에 저장해, 피크 수요시에 방출하기 위해서 필요해, 배터리 관리 시스템은 이러한 시스템의 효율과 운용을 결정합니다.

미국에서는 대규모 배터리 농장이 개발되어 유틸리티 스케일의 에너지 저장이 기대되고 있습니다.

2024년 4월, 자연에너지의 고부가가치 성장에 전념하고 에너지 전환을 리드하기를 열망하는 에퀴놀은 미국 최초의 배터리 스토리지 벤처에 그린 라이트를 맞췄습니다. 110MW의 용량을 자랑하며 텍사스 주 송전망의 에너지 안보를 강화하는 태세를 갖추고 있습니다. 이 프로젝트는 준비가 진행 중입니다. 선셋 리지의 10MW/20MWh 배터리는 특히 피크 수요시 신뢰성을 강화하고 Equinol 고객에게 더 나은 서비스를 제공하는 것을 목표로합니다. 2024년 후반에 상업운전을 개시할 예정입니다. 한편, 보다 대규모 100MW/200MWh 프로젝트인 시트러스 플랫은 아메리칸 일렉트릭 파워의 송전망과 링크하여 2026년 초에 상업운전을 개시할 예정입니다.

이상과 같은 요인이 미국의 배터리 관리 시스템 시장을 견인하고 있어 예측 기간 중에 더욱 성장할 것으로 예측됩니다.

북미 배터리 관리 시스템 산업 개요

북미의 배터리 관리 시스템 시장은 반쯤 분열 상태입니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 주요 요약

제3장 조사 방법

제4장 시장 개요

소개

2029년까지 시장 규모 및 수요 예측(단위 : 달러)

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

전기자동차의 보급

리튬 이온 전지 시스템에 관한 안전성에 대한 우려

억제요인

기성품 배터리 관리 시스템의 기술적 한계

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

투자분석

제5장 시장 세분화

용도

거치형

휴대용

수송

지역별 시장 분석

미국

캐나다

기타 북미

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

Strategies Adopted & SWOT Analyses for Leading Players

기업 프로파일

Eberspaecher Vecture Inc.

BorgWarner Inc.

Texas Instruments Incorporated

Nuvation Energy

Sensata Technologies Inc.

BorgWarner Inc.

Romeo Power Inc.

ION Energy

Ewert Energy Systems Inc.

Schneider Electric SE

List of Other Prominent Companies(Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

Market Ranking/Share(%) Analysis

제7장 시장 기회와 앞으로의 동향

기술 진보 : 배터리 관리 시스템과 인공지능· 머신러닝의 통합

SHW

영문 목차

영문목차

The North America Battery Management System Market size is estimated at USD 2.47 billion in 2025, and is expected to reach USD 4.89 billion by 2030, at a CAGR of 14.67% during the forecast period (2025-2030).

Key Highlights

Over the medium term, the increasing safety concerns regarding the use of lithium-ion batteries in ESS and the widespread adoption of electric vehicles are expected to drive the demand for an innovative and efficient battery management system (BMS) during the forecast period.

On the other hand, limitations in off-the-shelf battery management systems are expected to make the current design outdated and impact the market studied during the forecast period.

Nevertheless, technological advancements in battery management systems with the integration of artificial intelligence, which offer advantages such as reduced complexity, better efficiency, and improved reliability, are expected to provide growth opportunities in the future.

The United States is expected to dominate the market during the forecast period due to high demand from two industries: energy storage systems and electric vehicles.

North America Battery Management System Market Trends

Transportation Segment Expected to Dominate the Market

Vehicles with internal combustion engines (ICE) were the only types used earlier. However, technology has been shifting toward electric vehicles (EVs) in line with growing environmental concerns. Therefore, due to these reasons, battery management systems do not hold any share in the internal combustion engine market.

Lithium-ion batteries are primarily used in electric vehicles as they provide high energy density, low self-discharge, less weight, and low maintenance. For internal combustion engine vehicles, the lead-based battery is being widely used and is expected to continue to be the only viable mass-market battery system for the foreseeable future. For use in SLI applications, lithium-ion batteries still require higher cost reductions to be considered a viable mass-market alternative to lead-based batteries.

Lithium-ion battery systems propel plug-in hybrid and electric vehicles. Owing to their high energy density, fast recharge capability, and high discharge power, lithium-ion batteries are the only available technology capable of meeting the requirements of original equipment manufacturers for the vehicle's driving range and charging time. Lead-based traction batteries are not competitive for use in full hybrid electric vehicles or electric vehicles because of their lower specific energy and higher weight.

Mexico is witnessing rapid growth in its electric vehicle manufacturing market. In March 2023, the Mexican government announced its intention for EVs to account for half of all cars sold domestically by 2030. Particularly, with Tesla Inc.'s plan to open a USD 5 billion Gigafactory in Mexico, the country is expected to become a production hub of electric vehicles. Such initiatives are likely to raise the sales of electric vehicles across the country and boost the demand for lithium-ion batteries for electric vehicles during the forecast period.

In addition, in February 2024, BYD Co. Ltd, a prominent Chinese electric vehicle (EV) manufacturer, announced that it was in the process of establishing a new manufacturing plant in Mexico. The company has initiated a feasibility study for this venture and is actively engaged in discussions with Mexican officials, particularly focusing on finalizing the factory's precise location.

Similar to the United States, the Canadian automobile industry is also undergoing a transition, with most auto producers pivoting toward electrification by setting up new plants or repurposing older plants to produce EVs.

For instance, in April 2024, Honda Motor announced that it was set to inject a substantial USD 11 billion into new electric vehicle and battery production plants in Ontario, augmenting its current setup. This would mark the company's most significant investment in Canada to date. The initiative aims to kick off operations by 2028, boasting an anticipated annual production capacity of up to 240,000 electric vehicles.

According to the Energy Information Agency (EIA), as of 2023, Canada's electric vehicle stock was recorded at approximately 38 thousand units, up by nearly 35.71% from stock volumes recorded in 2022.

Thus, based on the abovementioned factors, the transportation segment is likely to dominate the North American battery management systems market during the forecast period.

The United States Expected to Dominate the Market

The United States was projected to be one of the largest global markets for energy storage systems and electric vehicles in 2023. Both the end-user segments utilize battery management systems (BMS) to ensure the battery system's adequate performance. Due to the high demand from these two massive end-user industries, the country is expected to be one of the most prominent and fastest-growing regional markets for battery management systems during the forecast period.

The United States has one of the world's most well-developed automotive industries. As climate and environmental concerns are rising, most automakers in the country have prioritized the production of electric vehicles. Additionally, the US government has focused on increasing its electric vehicle fleet to reduce fossil fuel dependence and emissions.

According to the Energy Information Agency (EIA), as of 2023, EV stock in the United States was approximately 3.5 million, up by nearly 66.67% from 2022 stock volumes, making it the second largest global EV market after China.

As of 2023, the country had a renewable energy capacity of around 387.54 GW, an increase of around 8.7% compared to the previous year. In the upcoming years, renewable capacity in the country is likely to increase through targets that include having 80% new power generation capacity of clean energy by 2030. Further, the country aims to have 30 GW of offshore wind by 2030 and 110 GW by 2050.

Due to this rapid rise in renewable generation, grid stability has become a major issue in countries with a high level of renewable integration in their grids. Nearly 66% of the installed renewable energy capacity in the United States is from wind and solar, which are inherently variable energy sources. Energy storage systems are needed to store renewable energy generation during high generation periods and release it during peak demand, while battery management systems dictate the efficiency and operation of these systems.

The United States is expected to witness the development of massive battery farms, which are expected to provide utility-scale energy storage. These utility-scale systems are to be monitored and operated via a sophisticated battery management system, which is expected to allow bi-directional energy flow and battery optimization to improve battery life while maximizing efficiency and minimizing accidents.

In April 2024, Equinor, a company dedicated to high-value growth in renewables and aspiring to lead the energy transition, greenlit its inaugural US battery storage ventures. These two projects, collectively boasting a 110 MW capacity, are poised to enhance energy security for the Texas grid. The Sunset Ridge Energy Center, located in Frio County, Texas, is already under construction, while preparations are underway for the Citrus Flatts project in Cameron County, Texas. The 10 MW/20 MWh battery storage at Sunset Ridge aims to bolster reliability, especially during peak demand, ensuring better service for Equinor's customers. Sunset Ridge is slated for commercial operation in the latter half of 2024. On the other hand, Citrus Flatts, a more substantial 100 MW/200 MWh project, will link up with American Electric Power's transmission network and is anticipated to commence commercial operations in early 2026.

The abovementioned factors are driving the US battery management systems market, which is expected to grow further during the forecast period.

North America Battery Management System Industry Overview

The North American battery management systems market is semi-fragmented. Some of the major players in the market (in no particular order) include Eberspaecher Vecture Inc., BorgWarner Inc., Texas Instruments Incorporated, Nuvation Energy, and Sensata Technologies Inc.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Widespread Adoption of Electric Vehicles

4.5.1.2 Safety Concerns Regarding Lithium-ion Battery Systems

4.5.2 Restraints

4.5.2.1 Technical Limitations in Off-the-Shelf Battery Management Systems

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitute Products and Services

4.7.5 Intensity of Competitive Rivalry

4.8 Investment Analysis

5 MARKET SEGMENTATION

5.1 Application

5.1.1 Stationary

5.1.2 Portable

5.1.3 Transportation

5.2 Geography Regional Market Analysis {Market Size and Demand Forecast till 2028 (For Regions Only)}

5.2.1 United States

5.2.2 Canada

5.2.3 Rest of North America

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted & SWOT Analyses for Leading Players

6.3 Company Profiles

6.3.1 Eberspaecher Vecture Inc.

6.3.2 BorgWarner Inc.

6.3.3 Texas Instruments Incorporated

6.3.4 Nuvation Energy

6.3.5 Sensata Technologies Inc.

6.3.6 BorgWarner Inc.

6.3.7 Romeo Power Inc.

6.3.8 ION Energy

6.3.9 Ewert Energy Systems Inc.

6.3.10 Schneider Electric SE

6.4 List of Other Prominent Companies (Company Name, Headquarter, Relevant Products & Services, Contact Details, etc.)

6.5 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Technological Advancements: Integration of Battery Management Systems With Artificial Intelligence and Machine Learning