중동 및 아프리카의 일반 항공 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

Middle East and Africa General Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693652

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

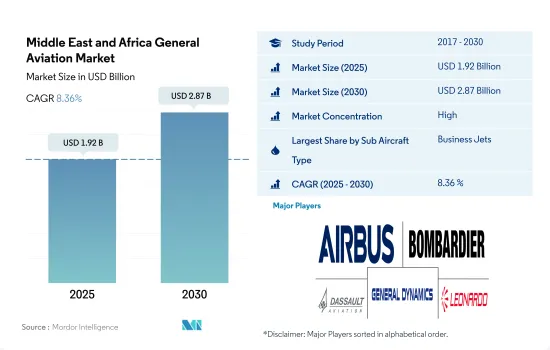

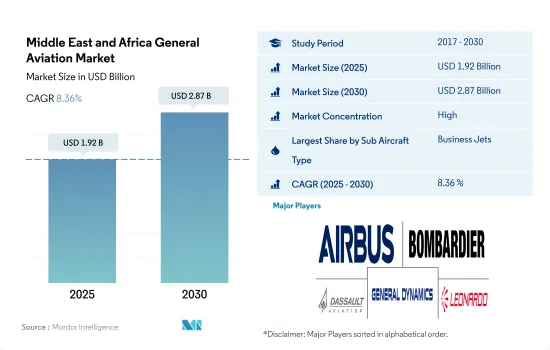

중동 및 아프리카의 일반 항공 시장 규모는 2025년 19억 2,000만 달러로 추정되며, 2030년에는 28억 7,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 8.36%로 성장할 전망입니다.

이 지역의 부유층 증가는 비즈니스 제트기와 피스톤 고정 날개 기계의 조달을 뒷받침하고 있습니다.

중동 및 아프리카는 2022년 세계 일반 항공 시장의 약 3.5%를 차지했습니다.

각 지역의 관광 섹터의 성장에 수반해, 많은 차터 오퍼레이터나 관광 회사는 새로운 피스톤 엔진기, 터보프롭기, 헬리콥터를 도입하는 것으로, 보유기의 확대를 계획하고 있습니다.

HNWI와 UHNWI는 개인 여행과 출장을 위해 개인 제트기와 헬리콥터를 선호합니다. UHNWI 인구는 아프리카에서는 2,146명에서 2022년에는 2,489명으로, 중동 국가에서는 2016년 4,452명에서 2022년에는 9,717명으로 증가했습니다.

항공기 납입수로는 Gulfstream이 약 29기로 OEM의 선두가 되고, 이어서 Embraer이 14기, Bombardier가 13기로, 2017-2022년에 중동에서 납입되었습니다.

석유가 풍부한 경제권에 있어서의 비즈니스 항공 서비스에 대한 수요의 높아지는 중동 및 아프리카의 일반 항공 섹터를 뒷받침할 것으로 예측됩니다.

HNWI가 이 지역 시장 성장을 견인

중동, 아프리카는 2022년 세계의 비즈니스 제트기 납입 대수의 약 3%를 차지하고 있습니다.

2022년에는 중동 및 아프리카 전역에서 비즈니스 항공의 신규 회원이 급증하고, 에어 차터 서비스 제공업체는 높은 수요를 목격했습니다.

팬데믹 후, 이 지역의 비즈니스 제트 수요는 2021년에 113% 급증했고, 특히 대형 비즈니스 제트 부문에서 급증했습니다. 2022년 7월 현재 중동의 비즈니스 제트기 전체의 약 50%, 아프리카에서는 36%를 대형 제트기가 차지하고 있습니다.

석유가 풍부한 경제권에 있어서의 비즈니스 항공 서비스 수요 증가는 중동 및 아프리카의 일반 항공 섹터 수요를 밀어 올릴 것으로 예측됩니다.

중동 및 아프리카의 일반 항공 시장 동향

석유 및 가스와 부동산이 중동의 HNWI 성장을 뒷받침하는 주요 산업이었습니다.

2017-2022년까지 동기간에 UHNWI의 수가 약 4.4%밖에 급증하지 않은 아프리카와 비교해 중동에서는 UHNWI의 인구가 약 118% 급증했습니다.

중동의 HNWI 친화적 인 조치로 많은 HNWI가이 나라로 이주했습니다. 많은 부유층은 인도, 러시아, 아프리카 및 기타 중동 국가에 속합니다.

중동에서는 하이테크 산업에 대한 관심이 높아짐에 따라 HNWI 인구의 성장은 주로 아랍에미리트(UAE)과 이스라엘이 견인했습니다. 금융 서비스, 기초 재료, 부동산, 운송, 물류는 이 지역에서 많은 HNWI를 차지하는 주요 산업이었습니다.

중동 및 아프리카 일반 항공 산업 개요

중동 및 아프리카의 일반 항공 시장은 상당히 통합되어 있으며 상위 5개 기업에서 87.80%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

부유층(HNWI)

규제 프레임워크

밸류체인 분석

제5장 시장 세분화

서브 항공기 유형

비즈니스 제트

대형 제트기

소형 제트기

중형 제트기

피스톤 고정익기

기타

국가명

알제리

이집트

카타르

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Airbus SE

Bombardier Inc.

Dassault Aviation

General Dynamics Corporation

Leonardo SpA

Lockheed Martin Corporation

Pilatus Aircraft Ltd

Robinson Helicopter Company Inc.

Textron Inc.

The Boeing Company

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Middle East and Africa General Aviation Market size is estimated at 1.92 billion USD in 2025, and is expected to reach 2.87 billion USD by 2030, growing at a CAGR of 8.36% during the forecast period (2025-2030).

The rising number of HNWIs in the region is boosting the procurement of business jets and piston fixed-wing aircraft

Middle East & Africa accounted for around 3.5% of the global general aviation market in 2022. Out of the overall Middle East & Africa market, around 52% accounted for others, 34% accounted for the piston-fixed wing, and 14% accounted for business jets.

With the growth in the tourism sector in various regions, many charter operators and tourism companies plan to expand their fleets by introducing new piston-engine aircraft, turboprop aircraft, and helicopters. This trend is helping them further expand their presence globally.

The HNWIs and UHNWIs prefer private jets and helicopters for personal or business travel. The rising number of HNWIs in the region is boosting the procurement of aircraft in the general aviation sector. The UHNWI population increased from 2,146 in 2016 to 2,489 in 2022 in Africa and from 4,452 in 2016 to 9,717 in 2022 in Middle Eastern countries.

Gulfstream was the leading OEM in terms of aircraft deliveries, with around 29 aircraft, followed by Embraer and Bombardier, with 14 and 13 deliveries in the Middle East during 2017-2022. Similarly, in Africa, Bombardier was the prominent player with nine deliveries, followed by Dassault, Gulfstream, and Cessna, with around seven, five, and five deliveries.

The growing demand for business aviation services in oil-rich economies is expected to boost the general aviation sector in the Middle East & Africa. More than 1200 aircraft comprising business jets, helicopters, turboprops, and piston aircraft are expected to be delivered in the region during the forecast period.

HNWIs emphasize growth of the market in the region

The Middle East & Africa accounted for around 3% of global business jet deliveries in 2022. Similarly, turboprop and piston aircraft accounted for 6.3% and 2.3% of the global deliveries in their category.

In 2022, air charter service providers witnessed high demand in the whole Middle East & Africa with the surge in new memberships for business aviation. The HNWIs and UHNWIs prefer private jets and helicopters for personal or business travel. The rise in the number of HNWI individuals in the Middle East & African region has aided in procuring aircraft in the general aviation sector. From 2017 to 2022, the HNWI population in the Middle East increased from 176,000 in 2017 to 754,000 in 2022, and in Africa, it increased from 45,000 in 2017 to 128,000 in 2022.

After the pandemic, business jet demand in this region surged 113% in 2021, specifically in the large business jet segment. In terms of the current operational fleet, large jets accounted for around 50% of the overall Middle East business jet fleet and 36% in Africa as of July 2022, as large jets are more prevalent in the Middle East & Africa. Air charter service providers witnessed high demand in the Middle East & Africa during the pandemic.

The growth in demand for business aviation services in oil-rich economies is expected to boost the demand for the general aviation sector in the Middle East & Africa. Around 1,160 aircraft comprising business jets, helicopters, turboprops, and piston aircraft are expected to be delivered in the Middle East & Africa during the forecast period.

Middle East and Africa General Aviation Market Trends

Oil and gas and real estate were the major industries that boosted the growth of HNWIs in the Middle East

From 2017 to 2022, there was a surge of around 118% in the UHNWI population in the Middle East compared to Africa, where the number of UHNWIs surged only by around 4.4% in the same period. In 2022, the number of UHNWIs in the Middle East increased by 8%, while Africa experienced a 0.8% decrease compared to 2021.

The HNWI-friendly policies of the Middle East led to the migration of a large number of HNWIs into these countries. For instance, in 2022, the United Arab Emirates was expected to attract the largest number of high-net-worth individuals. An inflow of around 4,000 millionaires is expected in the country. Most of the HNWIs belong to India, Russia, Africa, and other Middle Eastern countries. Saudi Arabia, the United Arab Emirates, and Turkey were the major countries in terms of the UHNWI population, witnessing growth rates of 98%, 57%, and 59%, respectively, during 2017-2022.

In the Middle East, the growth in the HNWI population was majorly led by the United Arab Emirates and Israel due to an increase in tech industrial focus. The recovery in oil prices also helped the GDP growth of the Middle East and North Africa, reaching 4.3% in 2022 compared to a contraction of 3.9% in 2021. Financial services, basic materials, real estate, transportation, and logistics were the major industries that accounted for a large number of HNWIs in the region. In Africa, South Africa, Egypt, Kenya, Nigeria, and Morocco account for over 55% of the overall region's high-net-worth individuals (HNWIs).

Middle East and Africa General Aviation Industry Overview

The Middle East and Africa General Aviation Market is fairly consolidated, with the top five companies occupying 87.80%. The major players in this market are Airbus SE, Bombardier Inc., Dassault Aviation, General Dynamics Corporation and Leonardo S.p.A (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 High-net-worth Individual (hnwi)

4.2 Regulatory Framework

4.3 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)