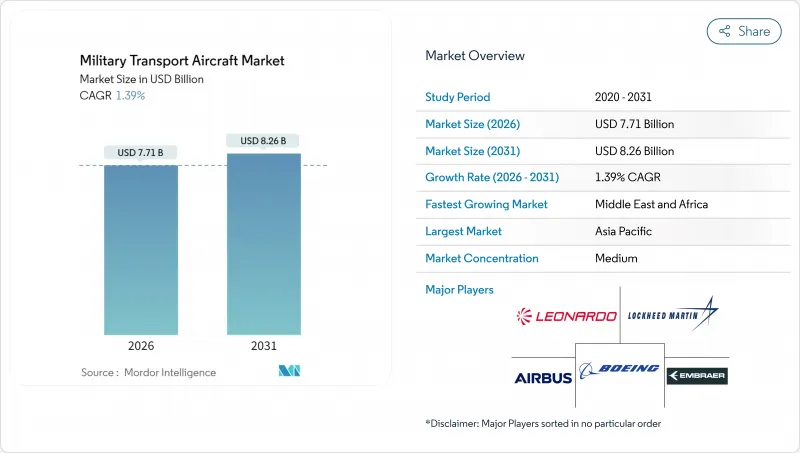

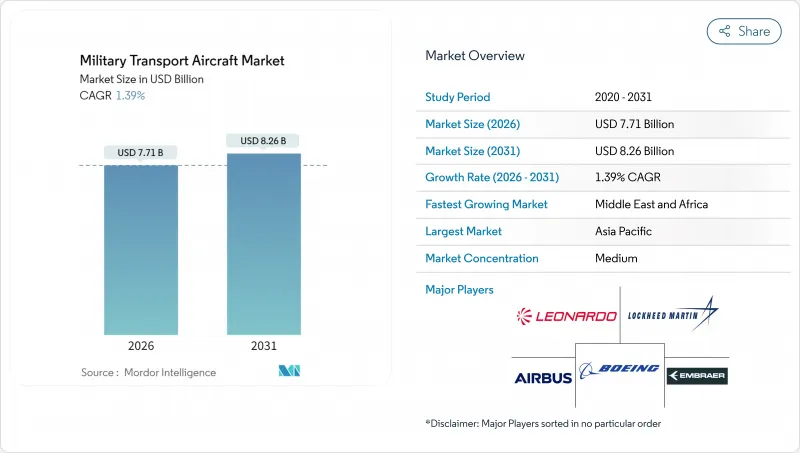

군용 수송기 시장은 2025년에 76억 달러로 평가되었으며, 2026년 77억 1,000만 달러, 2031년까지 82억 6,000만 달러에 이를 것으로 예측됩니다. 예측기간(2026-2031년)의 CAGR은 1.39%를 나타낼 전망입니다.

현재의 확대는 지정학적 긴장 증가, 긴급 인도적 지원 활동, 계획적인 기체 갱신 사이클에 기인하고 있습니다. 아시아태평양의 방위성은 대형 전략 플랫폼의 조달을 계속하는 한편, 소국에서는 인프라 투자가 적은 경·중형 수송기를 선호하고 있습니다. 현대화 계획은 오픈 아키텍처 항공 전자 장비, 디지털 스레드 정비 시스템 및 다목적 재구성을 점차 지정하고 운영자는 가동 중지 시간을 줄이고 임무 범위를 확장 할 수 있습니다. 조달 예산은 견고한 상태이지만, 복합 구조체와 항공 엔진 공급망의 병목 현상으로 인해 연간 납품 수가 줄어들고 제조업체는 긴 리드 타임 협상과 추가 Tier 2 공급업체의 활용을 강요하고 있습니다. 경쟁의 역학으로는 중국, 인도, 한국의 국내 제조업체가 에어버스, 보잉, 록히드 마틴 등 기존의 지배적 기업과 경쟁하고 있는 점이 특징이며, 이 움직임은 2030년까지의 수출 패턴을 재구축할 가능성이 높다고 생각됩니다.

2024년 중국의 방위 지출은 2,960억 달러로 평가되었고, 아랍 에미리트의 항공기 조달액은 18% 증가, 방위 지출은 급증했습니다. 이러한 예산 증가는 새로운 대형 수송기 프로그램, 수명 연장 패키지, 기술 이전 조항을 포함한 현지 산업 파트너십에 충당되고 있습니다. 또한 지속적인 지출은 수명주기 비용을 줄이고 임무 준비를 가속화하는 디지털 물류 제품군의 조사를 지원합니다. 걸프 협력 회의(GCC) 회원국은 모듈식 A400M 및 C-130J 변형을 향해 함대의 다양화를 계속하고 있으며, 연합 작전에서 연합 파트너와의 상호 운용성을 확보하고 있습니다.

구형 C-130A/B 및 An-26 기체의 60% 이상이 취항 40년을 넘고 있기 때문에 운용자는 신조의 C-390, C-295, KC-390 밀레니엄 모델을 우선하는 경쟁 입찰을 신속하게 진행하고 있습니다. 스웨덴이 2024년에 4대의 C-390을 주문한 것은 플라이 바이 와이어 제어와 저연비를 갖춘 높은 처리량 기체로의 전환을 보여줍니다. 동유럽 사용자들은 동시에 러시아 공급망에 대한 의존도를 줄이기 위해 소련 시대의 운송 시스템을 퇴역시키고 있으며, 2035년까지 꾸준한 대체 수요를 창출하고 있습니다.

플랫 앤 휘트니 사의 TP400 시리즈 및 도레이사의 탄소섬유 원료는 2024년에 18개월분의 수주 잔을 안고, A400M의 납품 지연을 초래함과 동시에, OEM 제조업체에 생산 스케줄의 재조정을 강요하게 했습니다. 이 공급 부족은 단가 상승을 초래하고, 각국 공군은 잠정적인 능력 부족을 용인하거나 추가 전세 항공편의 '긴급 증편' 비용을 지불해야 합니다.

2025년 군용 수송기 시장 규모에서 고정익 수송기는 61.12%를 차지했습니다. 이것은 C-130J 슈퍼 허큘리스와 A400M 아틀라스와 같은 신뢰성이 높은 기종이 견인하고 있습니다. 지속적인 블록 업그레이드는 상호 운용성 인증을 유지하면서 적재량과 항속 거리 생산성을 향상시킵니다. 한편, 회전익기는 제압환경하에서 포인트-투-포인트 수송으로의 교리전환의 혜택을 받아 군용 수송기 시장 전체를 상회하는 CAGR 4.20%로 성장을 지속하고, 있습니다. 복합재 블레이드의 보급과 개량된 전동 장치 설계에 의해 양력 중량비가 향상되어, 치누크나 CH-53K기군의 외부 매달림 능력이 확대되고 있습니다.

회전익기의 점유율 확대는 낮은 시그니처에 의한 침투작전에 대한 특수작전 수요도 반영하고 있으며, CV-22와 같은 틸트 로터기는 제트기 수준의 속도와 수직 이착륙(VTOL) 능력을 겸비하고 있습니다. 그러나 전역간 이동에 있어서는 고정익기는 여전히 대체 불가능합니다. C-390 밀레니엄 플라이 바이 와이어 제어 시스템은 민간 인증 카테고리 IIIb 자동 착륙을 실현하여 안개가 발생하기 쉬운 전선 기지로 진입할 수 있습니다. 2030년까지 고정익기의 납품수는 연간 약 95기로 안정될 것으로 예상되는 한편, 신형FLRAA(회전익군용수송기)의 진입이 성숙함에 따라 회전익기의 조달수는 140기로 피크에 달할 가능성이 있습니다.

2025년 군용수송기 시장 규모에서 병원 및 물자공수가 34억 1,000만 달러(총액의 44.85%)로 최대 점유율을 차지했고, 각국이 전략적 수송능력을 유지하는 가운데 시장 전체의 CAGR1.39%에 거의 연동하는 추이가 예상됩니다. 이 하위 부문은 C-130J나 A400M 등 고정익 주력기에 의한 혜택을 받았으며, 2024년에는 양 기종에서 병원 수송 출격의 60% 이상을 차지했습니다. 함대계획 담당자는 적재량과 항속거리의 향상, 신속한 임무 변경 구성을 우선하고 있으며, 성장이 두드러지더라도 부문의 규모를 유지하고 있습니다. 아시아태평양과 유럽의 조달 파이프라인은 안정적입니다. 한편, 북미의 운용기관은 아비오닉스의 갱신과 수명 연장에 주력하고 있으며, 이것이 군용 수송기 시장에서의 애프터마켓 지출의 기반이 되고 있습니다.

아시아태평양은 2025년 수익의 39.05%를 차지했으며, 군용 수송기 시장에서 지역적인 주도적 지위를 확고히 하고 있습니다. 생산량은 Y-20의 지속적인 생산, 인도의 국산 C-295 라인 및 일본의 C-2 생산률 확대로 인한 것입니다. 주요 경제권에서 연평균 8.5%의 방위 예산 성장에 견인되었으며, 이 지역의 CAGR은 1.75%로 예측되고 있습니다. 쿼드가 추진하는 상호 운용성 요구 사항과 같은 능력 협력은 공동 승무원 훈련 계약을 더욱 촉진합니다.

북미는 28.50%의 점유율을 차지하며 주로 미국 공군 프로그램이 견인하고 있습니다. 2024년에는 C-130J의 비행 시간이 12% 증가했습니다. 캐나다의 CC-330 허스키 급유 운송획과 멕시코의 CN-235 확충은 대륙 전체 수요 증가를 뒷받침하고 있습니다. 대서양을 분리한 유럽은 22.05%를 차지했지만, 공급망의 혼란에 의해 A400M의 생산은 8기에 머물렀습니다. NATO 전략공수능력(SAC)은 아빠 공군기지에서 C-17을 로테이션 운용하고 있으며, 동맹이 공유자산에 의존하고 있음을 나타냅니다.

중동 및 아프리카은 3.60%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 시장으로 떠오르고 있습니다. 나이지리아의 C-295 4기 주문과 남아프리카의 C-130BZ 현대화 계획은 평화 유지 활동과 인도주의 임무가 엄격한 예산 제약을 초과한다는 것을 보여줍니다. 걸프 국가들은 중동 및 아프리카 통계를 통합하고 UAE의 신형 C-130J-30 도입과 카타르의 A400M 구매 계획이 지역 전체의 CAGR2.32%를 지원하고 있습니다. 아프리카 연합의 공유 인프라는 국경을 넘은 공수 작전을 가능하게 하고, 규제상의 장벽을 완화함과 동시에 공동 정비 기지의 설치를 촉진하고 있습니다.

The military transport aircraft market was valued at USD 7.60 billion in 2025 and estimated to grow from USD 7.71 billion in 2026 to reach USD 8.26 billion by 2031, at a CAGR of 1.39% during the forecast period (2026-2031).

Current expansion stems from heightened geopolitical tensions, urgent humanitarian operations, and programmed fleet renewal cycles. Asia-Pacific defense ministries continue to order heavy strategic platforms while smaller nations favor light and medium airlifters that require lower infrastructure investment. Modernization programs increasingly specify open-architecture avionics, digital-thread maintenance suites, and multi-role reconfigurability, enabling operators to reduce downtime and expand mission sets. Although procurement budgets remain sound, supply-chain bottlenecks for composite structures and aero-engines restrain annual deliveries, causing manufacturers to negotiate longer lead times and activate additional Tier-2 suppliers. Competitive dynamics now feature indigenous entrants from China, India, and South Korea contesting the traditional dominance of Airbus, Boeing, and Lockheed Martin, an evolution likely to reshape export patterns through 2030.

Defense outlays rose sharply in 2024, with China allocating USD 296 billion and the United Arab Emirates lifting aviation procurement by 18%. These higher budgets are funneled into new heavy airlift programs, life-extension packages, and local industrial partnerships that include technology transfer clauses. Sustained spending also underpins research into digital logistics suites that cut lifecycle costs and speed mission readiness. Countries in the Gulf Cooperation Council continue to diversify their fleets toward modular A400M and C-130J variants, ensuring interoperability with coalition partners for coalition operations.

Over 60% of legacy C-130A/B and An-26 airframes have exceeded 40 years in service, prompting operators to fast-track competitive tenders that favor new-build C-390, C-295, and KC-390 Millennium models. Sweden's 2024 order for four C-390 aircraft marks a shift toward higher-throughput airframes with fly-by-wire controls and lower fuel consumption. Eastern European users are simultaneously retiring Soviet-era transport systems to reduce their dependence on Russian supply chains, creating a steady replacement funnel through 2035.

Pratt & Whitney's TP400 line and Toray's carbon-fiber feedstocks reached 18-month backlogs in 2024, delaying A400M handovers and forcing original equipment manufacturers to resequence production slots. The scarcity raises unit pricing and compels air forces to accept interim capability gaps or pay premium "surge" fees for supplemental charter lift.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Fixed-wing transports captured 61.12% of the 2025 military transport aircraft market size, anchored by dependable performers such as the C-130J Super Hercules and A400M Atlas. Continuous block upgrades raise payload-range productivity while preserving interoperability certifications. At the same time, rotorcraft benefit from doctrinal shifts toward point-to-point lift in denied environments, driving a 4.20% CAGR that outpaces the broader military transport aircraft market. The widespread use of composite blades and improved transmission designs raises lift-to-weight ratios, expanding external-sling capacities for the Chinook and CH-53K fleets.

Rotorcraft share gains also reflect special-operations demand for low-signature infiltration, where tilt-rotor platforms like the CV-22 offer jet-class speed combined with vertical takeoff and landing (VTOL) capabilities. However, fixed-wing aircraft remain irreplaceable for inter-theater moves; the C-390 Millennium's fly-by-wire controls provide civil-certified Category IIIb autoland, allowing entry to fog-prone forward locations. Through 2030, fixed-wing deliveries are expected to stabilize at around 95 aircraft annually, whereas rotary procurement could peak at 140 units as new FLRAA entrants mature.

Troop and cargo airlifting generated the largest slice of the 2025 military transport aircraft market size, at USD 3.41 billion, equivalent to 44.85% of the total value, and is forecasted to track closely to the overall 1.39% CAGR as nations sustain their strategic lift requirements. The sub-segment benefits from fixed-wing workhorses such as the C-130J and A400M, which together accounted for more than 60% of troop-movement sorties in 2024. Fleet planners prioritize payload-range improvements and rapid re-role configurations, ensuring the segment defends its scale even as growth plateaus. Procurement pipelines in the Asia-Pacific and Europe remain steady. At the same time, North American operators focus on avionics refreshes and service-life extensions, which anchor aftermarket spending within the military transport aircraft market.

The Global Military Transport Aircraft Market Report is Segmented by Aircraft Type (Fixed-Wing Transport Aircraft, Rotary-Wing Transport Aircraft), Application (Troop and Cargo Airlifting, and More), End-User Service (Air Force, Army Aviation, and More), Propulsion Type (Turboprop, Turboshaft, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

The Asia-Pacific region accounted for 39.05% of 2025 revenue, solidifying its regional leadership in the military transport aircraft market. Volume comes from continuous Y-20 production, India's indigenous C-295 line, and Japan's expanded C-2 build rate. The regional CAGR is forecasted at 1.75%, driven by annual defense budget growth averaging 8.5% across major economies. Capability cooperatives, such as the Quad-spur interoperability requirements, further stimulate joint crew-training contracts.

North America held a 28.50% share, primarily through US Air Force programs, which saw a 12% increase in C-130J flight hours in 2024. Canada's CC-330 Husky tanker-transport initiative and Mexico's CN-235 expansion underscore the growing continental demand. Across the Atlantic, Europe accounted for 22.05%, though supply-chain snarls limited A400M outputs to eight units. NATO's Strategic Airlift Capability rotates C-17s from Papa Air Base, underscoring the alliance's reliance on pooled assets.

The Middle East and Africa emerge as the fastest-growing slice with a 3.60% CAGR. Nigeria's four-unit C-295 order and South Africa's C-130BZ modernization illustrate how peacekeeping and humanitarian mandates override tight budgets. Gulf states blend Middle East and Africa statistics; the UAE's fresh C-130J-30s and Qatar's pending A400M purchase underpin a 2.32% regional CAGR. Shared infrastructure under the African Union mobilizes cross-border airlift operations, easing regulatory hurdles and encouraging cooperative maintenance depots.