India Aviation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693584

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

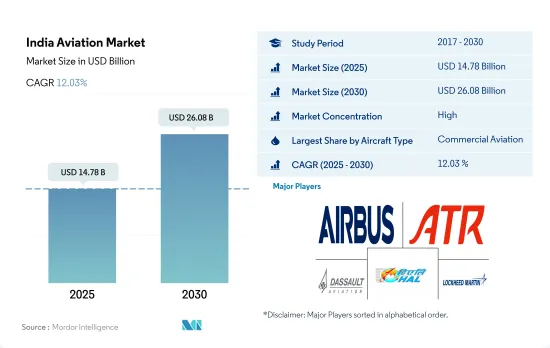

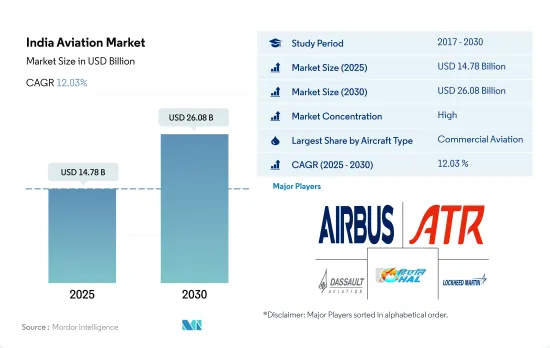

인도의 항공 시장 규모는 2025년 147억 8,000만 달러로 예측되며, 2030년에는 260억 8,000만 달러에 이를 것으로 예상되며, 예측 기간 중(2025-2030년) CAGR 12.03% 성장할 것으로 예측됩니다.

예측기간 중 민간항공이 인도시장을 독점할 전망

인도의 민간 항공 산업은 최근 몇 년간 동국에서 가장 급성장하고 있는 산업 중 하나로 부상했습니다.

항공 운송량은 세계 평균에 비해 급속히 증가하고 있습니다. 항공 항공편 수는 현재 600대에서 2024년까지 1,200대까지 증가할 수 있습니다. 인도의 일반항공산업은 비즈니스 및 프라이빗 니즈에 응하는 사치품이라고 생각되고 있어 나라의 경제 성장을 강력하게 뒷받침하고 있습니다.

이러한 원동력에도 불구하고, 비즈니스의 용이성, 세제의 복잡성, 불충분한 인프라, 운항 라이선스 취득의 복잡한 프로세스 등의 과제에 의해 인도의 비즈니스 항공 시장의 성장은 침체하고 있습니다.

HAL은 인도 최대의 항공기 및 헬리콥터 제조업체이며 BAE Hawk Trainers나 Tejas LCA를 생산하고 있습니다.

인도 항공 시장 동향

규제완화와 항공 여객수 증가로 시장 수요 견인

2022년에는 약 1억 2,320만 명의 여행객이 항공기를 이용했습니다.

2022년에 6,900만명의 여객을 운반한 IndiGo는 6,800만명의 여객을 운반한 2019년의 실적을 100만명 개선했습니다. 2022년 12월 국내 항공 여객수는 전년 동월비 15% 증가의 약 129,000명이었지만, 팬데믹 전(2019년 12월)의 수준을 1% 밑도는 채로 있었습니다.

2022년 1월부터 3월까지 인도의 국내 항공사가 운반한 여객수는 2021년 동기간 2,338만명에 비해 2,480만명이었습니다. 2022년 4월, 인도의 항공사 여객수는 185만명에 달했고, 2019년 4월에 기록한 183만명의 국제선 여객수를 약간 웃돌았습니다.

지정학적 위협이 국방비 증가의 원동력

인도는 세계 4위, 아시아태평양에서는 2위의 국방 지출국입니다. 인도의 국방예산 총액은 GDP의 2%로 견적되고 있습니다.

이 나라의 자본 지출은 군사 장비 업그레이드와 중국과의 계쟁 중인 국경을 따라 군사 인프라에 충당되는 것으로, 2022년 군사 지출 전체의 23%에 상당합니다.

최근, 특히 국산품의 구입에 할당이 행해졌습니다. Tejas 경전투기(LCA) Mk-1A, 경전투 헬리콥터(LCH), 기초 연습기 HTT-40, Arjun Mk-1A 전차, 미사일 수종, 기타 무기에 많은 돈이 투입될 수 있습니다. 국방 생산 증가는 수출에 길을 열고 비용을 상쇄하는 데 도움이 됩니다. 외국 장비 제조 업체는 합작 투자(JV)를 설립하고 하이테크 부문에 외국 직접 투자(FDI)를 유치 할 가능성이 높습니다. 이러한 합작투자의 일부는 방위 수출을 지원할 것으로 기대되고 있습니다.

인도의 항공 산업 개요

인도의 항공 시장은 상당히 통합되어 있으며 상위 5개 기업에서 92.04%를 차지합니다. 이 시장의 주요 기업은 Airbus SE, ATR, Dassault Aviation, Hindustan Aeronautics Limited, Lockheed Martin Corporation 등입니다(알파벳순).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

항공 여객 수송량

항공화물 수송량

국내총생산

수입 여객 킬로(rpk)

인플레이션율

액티브 플릿 데이터

국방 지출

개인 부유층(HNWI)

규제 프레임워크

밸류체인 분석

제5장 시장 세분화

항공기 유형

민간 항공기

서브 항공기 유형별

여객기

바디 유형별

협폭동체 항공기

와이드 바디 기계

일반 여객기

서브 항공기 유형별

비즈니스 제트기

바디 유형별

대형 제트기

소형 제트기

중형 제트기

피스톤 고정익기

기타

군용기

서브 항공기 유형별

고정익기

바디 유형별

다용도 항공기

훈련용 항공기

수송기

기타

회전익기

바디 유형별

멀티미션 헬리콥터

수송용 헬리콥터

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Airbus SE

ATR

Bombardier Inc.

Dassault Aviation

General Dynamics Corporation

Hindustan Aeronautics Limited

Leonardo SpA

Lockheed Martin Corporation

Textron Inc.

The Boeing Company

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The India Aviation Market size is estimated at 14.78 billion USD in 2025, and is expected to reach 26.08 billion USD by 2030, growing at a CAGR of 12.03% during the forecast period (2025-2030).

Commercial aviation is expected to dominate the market in India during the forecast period

The civil and military aviation industry in India emerged as one of the fastest-growing industries in the country in the past few years. According to the Indian government, the commercial aviation sector contributed USD 30 billion to India's GDP in 2021. With this growth, the domestic aviation market is projected to rank third globally by 2024.

Air traffic has been growing rapidly in the country as compared to the global average. The air fleet number may rise from the present 600 to 1,200 during 2024. The general aviation industry in India is considered a luxury for both business and private needs and strongly drives the country's economic growth. The surge of tourist traffic into India and the rising HNWIs have driven the growth of the general aviation sector in the country.

Despite these driving factors, challenges in ease of doing business, complications with the tax structures, inadequate infrastructure, and complicated processes to obtain operating licenses have resulted in subdued growth of the business aviation market in India. India is a critical military aircraft market, as the country has been modernizing its aerial capabilities by procuring new aircraft and indigenously developing military aircraft to defend its borders from Pakistan and China.

HAL is the largest manufacturer of aircraft and helicopters in India and has been producing BAE Hawk Trainers and Tejas LCA. It is also developing fifth-generation Advanced Medium Combat Aircraft under the Make in India initiative, with deliveries expected to start during the forecast period.

India Aviation Market Trends

Ease of restrictions and rising air passenger travel are driving the market demand

In 2022, nearly 123.2 million passengers traveled by air. This was 47% more than the passenger numbers in 2021. The year closed with IndiGo retaining the market share crown at almost 55%, with others trailing far behind. Vistara and Air India were both a distant second in December with a market share of 9.2% each, followed by SpiceJet and AIX Connect (AirAsia India) with 7.6% each. Go First recorded a share of 7.5%, while Akasa Air ended the year with 2.3%.

By carrying 69 million passengers in 2022, IndiGo improved its 2019 performance by a million when it carried almost 68 million passengers. This is after the company suffered from reduced capacity following the grounding of several of its planes. Domestic air passenger traffic grew 15 percent year-on-year to around 129 lakhs in December 2022 but remained 1 percent lower than the pre-pandemic level (December 2019). According to ICRA, the domestic aviation industry operated at an estimated passenger load factor of around 91% in December 2022 against approximately 80% in December 2021 and about 88% in December 2019.

A total of 24.8 million passengers were carried by domestic airlines in India between January and March 2022, compared to 23.38 million during the same period in 2021. In March 2022, India resumed its scheduled international flights, leading to a surge in international passenger traffic. As a result, in April 2022, Indian carriers reached 1.85 million passengers, slightly surpassing the traffic recorded in April 2019, which was 1.83 million international passengers. As of January 2022, the country had air bubble arrangements with 35 countries aimed at restarting international travel. These air bubble arrangements will provide direct/indirect connectivity to more than 100 countries.

Geopolitical threats are the driving factor for rising defense expenditure

India is the fourth-largest defense spender in the world and the second largest in the Asia-Pacific region. In 2022, the country's defense spending was USD 81.4 billion, a growth of 6% compared to 2021. India proposed USD 72.6 billion in defense spending for the 2023-24 financial year, 13% up from the previous period's initial estimates, aiming to add more fighter jets and roads along its tense border with China. The total Indian defense budget is estimated at 2% of GDP. India plans to spend nearly INR 242 billion (USD 3 billion) for naval fleet construction and INR 571.4 billion (USD 7 billion) for air force procurements, including more aircraft.

The country's expenditure on capital outlays, which funds equipment upgrades for the armed forces and the military infrastructure along its disputed border with China, amounted to 23% of total military spending in 2022. Personnel expenses (e.g., salaries and pensions) remained the largest expenditure category in the Indian military budget, accounting for around half of all military spending.

Recently, allocations for specifically indigenous purchases were made. The Tejas Light Combat Aircraft (LCA) Mk-1A, Light Combat Helicopters (LCH), basic trainer HTT-40 aircraft, Arjun Mk-1A tanks, several missiles, and other weapons may receive significant funding. Increased defense production will pave the way for exports and help offset expenses. Foreign equipment manufacturers are more likely to establish joint ventures (JVs) and attract foreign direct investment in high technology fields (FDI). Some of these joint ventures are also expected to aid in defense exports.

India Aviation Industry Overview

The India Aviation Market is fairly consolidated, with the top five companies occupying 92.04%. The major players in this market are Airbus SE, ATR, Dassault Aviation, Hindustan Aeronautics Limited and Lockheed Martin Corporation (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Air Passenger Traffic

4.2 Air Transport Freight

4.3 Gross Domestic Product

4.4 Revenue Passenger Kilometers (rpk)

4.5 Inflation Rate

4.6 Active Fleet Data

4.7 Defense Spending

4.8 High-net-worth Individual (hnwi)

4.9 Regulatory Framework

4.10 Value Chain Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)