아프리카의 비료 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

Africa Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693544

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

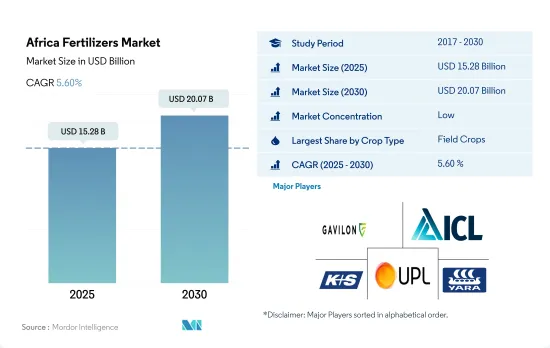

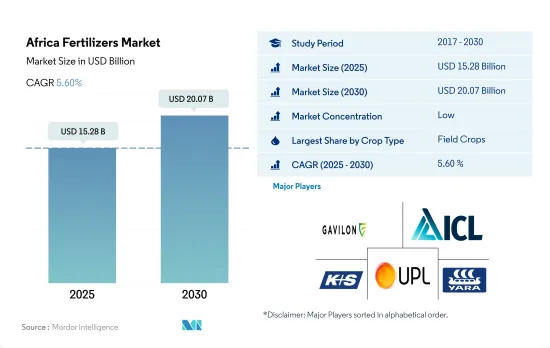

아프리카 비료 시장 규모는 2025년에 152억 8,000만 달러, 2030년에는 200억 7,000만 달러에 이르고, 예측 기간 중(2025-2030년) CAGR 5.60%로 성장할 것으로 예측됩니다.

각각의 작물 유형에 대한 비료의 용도는 증가하는 인구를 기르기 위한 식량 수요 증가에 의해 2023-2030년에 걸쳐 확대될 것으로 예측됩니다.

2022년 아프리카의 비료 소비량은 농작물이 압도적으로 많아 전체의 71.1%를 차지했습니다.

원예작물이 뒤를 이어 아프리카 비료소비량의 28.7%를 차지했고 2022년에는 47억 7,000만 달러가 됐습니다. 소비량은 9,000톤으로 적었지만 원예작물 재배면적은 2017년 3,650만 헥타르에서 2022년 3,770만 헥타르로 확대되었습니다. 이 성장의 원동력이 된 것은 숨겨진 기아나 영양 불량이 우려되는 가운데, 과일이나 야채라고 하는 고가치 작물에 수요가 높아진 것입니다.

주로 국제시장에 있어서의 아프리카의 화후 수요에 견인되는 잔디 및 관상용 작물은 2021년의 아프리카의 비료 소비량의 8.9%를 차지했습니다.

그러나 2022년에는 아프리카의 비료 소비량에 차지하는 잔디 및 관상용 작물의 비율은 불과 0.02%로 떨어졌습니다.

작물 유형을 불문하고 비료의 사용량은 증가할 것으로 예측됩니다.

남아프리카는 아프리카 대륙의 주요 농업 생산국 중 하나이며 수입에 의존합니다.

아프리카에는 질소, 인산, 칼리의 방대한 광물자원이 매장되어 있어 세계의 비료시장에서 주요 기업이 될 가능성을 지니고 있습니다.

2022년에는 나이지리아가 아프리카 비료 시장의 36.7%를 차지했으며, 아프리카 비료 시장을 독점했습니다.

주요 국가임에도 불구하고 나이지리아의 비료 사용량은 비교적 낮으며 헥타르 당 20 킬로그램 이하입니다. 이에 대해, 이집트나 남아프리카와 같은 나라들은 이미 나이지리아의 사용량을 크게 웃돌고 있어, 나이지리아가 따라잡기 위해서는 약 500%의 도약이 필요하다는 것을 시사하고 있습니다.

아프리카의 주요 농업국인 남아프리카는 비료의 수입에 크게 의존하고 있습니다.다른 일부 시장과 달리 남아프리카의 비료 부문은 수입 관세나 정부 계획이 없는 규제 완화된 환경에서 운영됩니다. 수입 관세나 정부의 제도는 존재하지 않습니다.

아프리카 비료 시장 동향

이 지역은 농업 생산을 두배로 할 수 있으며, 소비 수요가 증가함에 따라 농작물의 재배 면적이 확대될 것으로 예측됩니다.

아프리카의 농업 생태적 구역은 연간 2회의 강우량이 있는 밀생한 열대우림에서 강우량이 적은 건조한 사막까지 다양합니다. 옥수수, 수수, 밀, 쌀이 포함되어 있습니다.

2018-19년 시즌 남아프리카의 옥수수 농업 종사자는 공급 과잉으로 인한 가격 억제에 대응하기 위해 제작 면적을 10% 줄여 210만 헥타르로 했습니다. 양은 250만 톤에서 100만 톤으로 격감했습니다.

아프리카에서 가장 큰 수수 생산국은 나이지리아로 에티오피아가 그 뒤를 잇고 있습니다. 나이지리아의 곡물 생산량의 50%를 차지하고 곡물 재배지의 45%를 차지하는 수수는 가뭄에 강하고 다양한 토양 조건에 적응하는 작물입니다. 이러한 특성 때문에 수수는 특히 아프리카의 건조지대에서 선호되는 주식 작물이 되어 있어 식량과 소득의 안정을 확보하고 있습니다.

케냐, 소말리아, 에티오피아의 대부분은 심각한 음식 부족이라는 임박한 위협에 직면하고 있습니다. 지난 10년간 아프리카의 농업과 경작지가 지속적으로 확대되었음에도 불구하고 식량 수입에 대한 지출은 3배 가까이 증가하고 있습니다.

질소는 다양한 필드 작물에 필수적인 중요한 영양소로 눈에 띄고 있으며,이 지역에서는 유채가 주요 영양소 소비국입니다.

유채작물은 칼륨과 인의 시용률이 가장 높고, 2022년에는 각각 162.4kg/헥타르와 281.7kg/헥타르를 차지했습니다. 한편, 아프리카의 밭작물의 평균 질소 시용량은 2022년에는 364.9kg/헥타르입니다.

2022년에 아프리카의 농작물은 1차 양분 소비량 전체의 87.1%를 차지해 55만 6,100톤에 달했습니다. 이 우위는 농작물 전용의 광대한 토지 면적에 기인하고 있습니다. 구체적으로는 이들 작물에 있어서의 질소, 인, 칼륨의 평균 양분 시용량은 2022년에는 각각 223.2 kg/ha, 125.3 kg/ha, 155.3 kg/ha이었습니다.

나이지리아의 기니 사바나는 옥수수 생산에 적합한 환경 조건을 제공합니다. 사람은 낮은 수확량으로 고통받고 있습니다.그 주요 원인은 토지 이용의 격화에 의한 토양의 열화와 양분의 고갈(주로 질소)입니다. 충전, 단백질 합성 촉진 등 질소에는 여러 가지 장점이 있기 때문에 질소 적용이 우선합니다. 1차 영양소는 작물의 성장에 불가결하며, 토양의 고갈이나 질소의 용출이 우려되기 때문에 1차 영양소의 시용률은 향후 수년간 크게 성장할 것으로 예측됩니다.

아프리카 비료 산업 개요

아프리카의 비료 시장은 세분화되어 있으며 상위 5개 기업에서 7.43%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

주요 작물의 작부 면적

밭작물

원예작물

평균 양분 시용률

미량 영양소

밭작물

원예작물

1차 영양소

밭작물

원예작물

2차 다량 영양소

밭작물

원예작물

관개 농지

규제 프레임워크

밸류체인과 유통채널 분석

제5장 시장 세분화

유형

복합형

스트레이트

미량 영양소

붕소

구리

철

망간

몰리브덴

아연

기타

질소

질산암모늄

우레아

기타

인산

DAP

MAP

SSP

TSP

포타식

MoP

SoP

2차 영양소

칼슘

마그네슘

유황

형태

기존

특수

CRF

액체 비료

SRF

수용성

시비 모드

시비

잎면 살포

토양

작물 유형

밭작물

원예작물

잔디 및 관상용

생산국

나이지리아

남아프리카

기타 아프리카

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Foskor

Gavilon South Africa(MacroSource, LLC)

Haifa Group

ICL Group Ltd

KS Aktiengesellschaft

Kynoch Fertilizer

UPL Limited

Yara International ASA

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

SHW

영문 목차

영문목차

The Africa Fertilizers Market size is estimated at 15.28 billion USD in 2025, and is expected to reach 20.07 billion USD by 2030, growing at a CAGR of 5.60% during the forecast period (2025-2030).

The application of fertilizers in the respective crop types is anticipated to grow during 2023-2030, owing to the increasing need for food to feed the growing populations

In 2022, field crops dominated fertilizer consumption in Africa, representing 71.1% of the total. This translated to a volume consumption of 15.5 million metric tons, valued at USD 11.80 billion.

Horticultural crops followed, accounting for 28.7% of Africa's fertilizer consumption, valued at USD 4.77 billion in 2022. Despite a modest volume consumption of 9.0 thousand metric tons, the cultivation area for horticultural crops expanded from 36.5 million hectares in 2017 to 37.7 million hectares in 2022. This growth was driven by rising demand for high-value crops, such as fruits and vegetables, amidst concerns of hidden hunger and malnutrition. This surge in cultivation areas underscores the need for enhanced productivity, driving up fertilizer application in horticultural crops.

Turf & ornamental crops, primarily driven by the demand for African flowers in international markets, accounted for 8.9% of Africa's fertilizer consumption in 2021. This translated to a market value of USD 770.6 million and a volume consumption of 1.5 million metric tons.

However, in 2022, the share of turf and ornamental crops in Africa's fertilizer consumption dropped to a mere 0.02%. The market value for this segment was USD 3.5 million, with a volume consumption of 4.5 thousand metric tons. Conventional fertilizers dominated the market, capturing a 57.0% share, while specialty fertilizers accounted for the remaining 43.0%.

The application of fertilizers across crop types is expected to rise. This growth is driven by the need to meet the food demands of a burgeoning population, achieve higher yields, and enhance crop productivity.

South Africa is one of the major agriculture-producing countries in the continent and is import-dependent

Africa's vast mineral reserves of nitrogen, phosphate, and potash position it as a potential major player in the global fertilizer market. The region's rapid population growth, coupled with evolving food consumption patterns and rising incomes, is driving a need for increased agricultural production. This, in turn, is expected to lead to an increase in fertilizer demand.

In 2022, Nigeria dominated the African fertilizer market, accounting for 36.7% of the total. Nigeria boasts one of the world's highest rice consumption rates, with an annual production of 7 million metric tons. The country's economic growth, primarily propelled by the agricultural sector, is projected to sustain a CAGR of 5.5% in the coming years.

Despite being a major player, Nigeria's fertilizer usage remains relatively low, at under 20kg/hectare. This indicates a significant untapped potential for increased fertilizer application, potentially driving further market growth. In comparison, countries like Egypt and South Africa have already surpassed Nigeria's usage by a significant margin, suggesting a potential leap of around 500% for Nigeria to catch up.

South Africa, a key agricultural nation in Africa, heavily relies on fertilizer imports. While all potassic fertilizers are domestically consumed, a substantial 60%-70% of nitrogenous fertilizers are imported. Unlike some other markets, South Africa's fertilizer sector operates in a deregulated landscape, devoid of import tariffs or government schemes. With a surge in crop cultivation, the South African fertilizer market is projected to witness substantial growth, expanding from USD 1.77 billion in 2022 to USD 5.60 billion by 2030.

Africa Fertilizers Market Trends

The region has the potential to double its agricultural production, and the area under field crops is expected to expand due to the rising consumption demand

The agroecological zones in Africa span from dense rainforests with bi-annual rainfall to arid deserts with minimal precipitation. Dominant field crops in the region include corn, sorghum, wheat, and rice. In 2022, the cultivation area for these crops reached 224.8 million hectares, accounting for over 95% of the total agricultural land.

In the 2018-19 season, South African corn farmers reduced their planted area by 10% to 2.1 million hectares, responding to an oversupply that suppressed prices. Consequently, corn production in the country dipped by 11%, from 13 million to 12 million tonnes, and exports plummeted from 2.5 million to 1 million tonnes. In light of this, producers were likely to pivot from corn to oilseed crops, with soybeans being a favored choice. This shift was anticipated to lead to an overall decline in corn cultivation across Africa from 2018 to 2019.

Nigeria takes the lead as the largest sorghum producer in Africa, closely followed by Ethiopia. Sorghum, accounting for 50% of Nigeria's cereal output and occupying 45% of its cereal cultivation land, is a drought-tolerant crop with adaptability to diverse soil conditions. These qualities make sorghum a preferred staple crop, particularly in Africa's drier regions, ensuring food and income security.

Kenya, Somalia, and significant parts of Ethiopia face an imminent threat of severe food shortages. Over the past decade, Africa's spending on food imports nearly tripled despite a consistent expansion in its agricultural industry and cultivated land.

Nitrogen stands out as a crucial nutrient essential for various field crops, with rapeseed being the primary nutrient consumer in this region

Rapeseed crops have the highest potassium and phosphorous application rates, accounting for 162.4 kg/hectare and 281.7 kg/hectare, respectively, in 2022. Meanwhile, the average nitrogen application rate for field crops in Africa stood at 364.9 kg/hectare in 2022.

In 2022, field crops in Africa accounted for 87.1% of the total primary nutrient consumption, which amounted to 556.1 thousand metric tons. This dominance can be attributed to the extensive land area dedicated to field crops. Specifically, the average nutrient application rates for nitrogen, phosphorous, and potassium in these crops were 223.2 kg/ha, 125.3 kg/ha, and 155.3 kg/ha, respectively, in 2022.

The Guinea savannas in Nigeria offer favorable environmental conditions for maize production. However, despite this potential, farmers in the region struggle with low yields. The primary culprits are soil degradation and nutrient depletion, primarily nitrogen, resulting from intensified land use. Field crops prioritize nitrogen application due to its multiple benefits, including promoting tillering, leaf area development, grain formation, filling, and protein synthesis. Nitrogen also plays a crucial role in enhancing both grain yield and quality. Given that primary nutrients are vital for crop growth and with concerns over soil depletion and nitrogen leaching, the application rates for primary nutrients are expected to witness significant growth in the coming years.

Africa Fertilizers Industry Overview

The Africa Fertilizers Market is fragmented, with the top five companies occupying 7.43%. The major players in this market are Gavilon South Africa (MacroSource, LLC), ICL Group Ltd, K+S Aktiengesellschaft, UPL Limited and Yara International ASA (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Acreage Of Major Crop Types

4.1.1 Field Crops

4.1.2 Horticultural Crops

4.2 Average Nutrient Application Rates

4.2.1 Micronutrients

4.2.1.1 Field Crops

4.2.1.2 Horticultural Crops

4.2.2 Primary Nutrients

4.2.2.1 Field Crops

4.2.2.2 Horticultural Crops

4.2.3 Secondary Macronutrients

4.2.3.1 Field Crops

4.2.3.2 Horticultural Crops

4.3 Agricultural Land Equipped For Irrigation

4.4 Regulatory Framework

4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)