ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

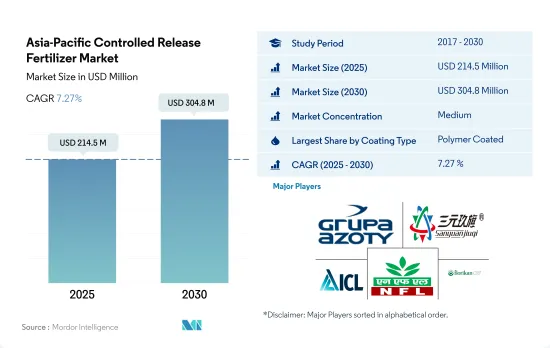

아시아태평양의 방출 조절 비료 시장 규모는 2025년 2억 1,450만 달러로 추정되며, 2030년에는 3억 480만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 7.27%로 성장할 전망입니다.

중국과 인도는 아시아태평양의 방출 조절 비료 시장을 독점

조사 기간 중 폴리머 피복 방출 조절 비료 시장은 현저한 성장을 이루었습니다.

옥수수, 콩, 유채 등의 곡물과 지방종자의 재배 확대가 폴리 유황 코팅 우레아 시장을 촉진하고 있습니다. 또한 폴리유황 코팅 CRF 시장은 고효율로 친환경 제품에 대한 수요 증가 등의 요인에 따라 성장하는 태세에 있습니다.

2022년에는 중국이 그 밖의 유형의 피복 방출 조절 비료 시장을 독점해 CRF 시장에서 42.3%의 금액 점유율을 차지했습니다.

화학 비료의 사용은 토양 pH의 변화, 미생물 성장의 저해, 과도한 질소 시용에 의한 온실 효과 가스의 방출 등, 유해한 영향을 미칩니다.

중국이 아시아태평양의 방출 조절 비료 시장을 독점

아시아태평양의 인구의 약 70.0%는 생활의 1차 기반을 농업에 직접 의존하고 있습니다.

중국은 아시아태평양의 방출 조절 비료 시장을 독점하고 있으며, 2022년 시장 가치 점유율의 43.8%를 차지했습니다. 폴리머 코팅 비료 부문은 2017년에 1,790만 달러로 평가되어 주로 CRF의 채용에 의한 비료 소비량의 삭감에 의해 NUE가 증가하기 때문에 2030년에는 5,800만 달러에 달할 것으로 예측되고 있습니다.

인도는 이 지역에서 방출 조절 비료의 2위 시장이며, 2022년에는 16.6%를 차지했습니다. 방출조절형 우레아는 인도에서 가장 일반적으로 사용되고 있는 CRF입니다. 이것은 휘발, 침출, 탈질에 의한 질소의 손실이 크기 때문입니다.

2017년 중국국제식물영양연구소는 후베이성에서 방출 제어형 요소 비료 시용 프로그램을 실시하였습니다.

아시아태평양의 방출 조절 비료 시장 동향

주요 성장 작물 재배의 대폭적인 확대가 시장 성장을 뒷받침할 것으로 예상됩니다.

농작물의 재배가 이 지역을 지배하고 있으며, 총재배면적의 95% 이상을 차지하고 있습니다.

중국, 인도, 파키스탄, 호주를 포함한 아시아태평양은 세계 최대의 밀 생산국 중 하나입니다. 중국과 인도는 세계 최대의 밀 생산국이며 소비국이기도 합니다.

쌀은 이 지역에서 가장 큰 농작물입니다. 2022년의 전체 농지 면적의 약 16.44%를 차지했습니다. 쌀은 아시아와 태평양 지역의 대부분의 지역에서 주식이 되고 있습니다. 중국은 2022년 1억 4,700만 톤의 쌀을 생산했고, 인도는 1억 2,400만 톤의 쌀을 수확했습니다.

농작물에 대한 국내외 수요의 급증은 농작물 전용 경작면적 확대를 촉진하고 있습니다.

세계 농지의 아산화질소 배출량의 약 28%는 중국 농지 때문입니다.

농작물에서 이 나라의 1차 양분(질소, 칼륨, 인)의 평균 시용량은 2022년에 129.1kg/ha였습니다. 대부분의 1차 양분은 토양 시용법으로 시용되고 있습니다.

아시아에서는 1차 영양소의 투입량이 많아 특히 질소비료와 칼리비료가 많습니다.

농작물에서는 밀의 평균 1차 양분 시용량은 214.9 kg/ha로, 2022년 농작물 중에서 가장 많아졌습니다.

질소와 인에 의한 지표수와 지하수의 오염은 비료의 시용률이나 작물의 대규모화에 관한 농가에 대한 어드바이스가 불충분했던 결과라고 생각되어 왔습니다.

아시아태평양의 방출 조절 비료 산업 개요

아시아태평양의 방출 조절 비료 시장은 적당히 통합되어 있으며 상위 5개 기업에서 61.40%를 차지하고 있습니다. 이 시장 주요 기업은 Grupa Azoty S.A.(Compo Expert), Hebei Sanyuanjiuqi Fertilizer, ICL Group Ltd, National Fertilizers Ltd, New Mountain Capital(Florikan)(알파벳순)입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

주요 작물의 작부 면적

밭 작물

원예 작물

평균 양분 시용률

주요 양분

밭 작물

원예 작물

규제 프레임워크

밸류체인과 유통채널 분석

제5장 시장 세분화

코팅 유형

폴리머 코팅

폴리머 유황 코팅

기타

작물 유형

밭 작물

원예 작물

잔디 및 관상용

생산국

호주

방글라데시

중국

인도

인도네시아

일본

파키스탄

필리핀

태국

베트남

기타 아시아태평양

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

Grupa Azoty SA(Compo Expert)

Haifa Group

Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

Hebei Woze Wufeng Biological Technology Co., Ltd

ICL Group Ltd

National Fertilizers Ltd

New Mountain Capital(Florikan)

Zhongchuang xingyuan chemical technology co.ltd

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

시장 역학(DROs)

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

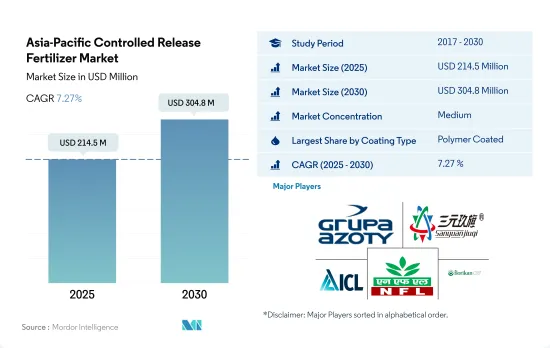

The Asia-Pacific Controlled Release Fertilizer Market size is estimated at 214.5 million USD in 2025, and is expected to reach 304.8 million USD by 2030, growing at a CAGR of 7.27% during the forecast period (2025-2030).

China and India dominate the Asia-Pacific controlled-release fertilizers market

During the study period, the market for polymer-coated controlled-release fertilizers experienced notable growth. By 2022, these fertilizers held a significant share of 76.0% in the overall controlled-release fertilizer (CRF) market in Asia-Pacific. The region's increasing emphasis on ecologically safe fertilizers is a key driver behind the surge in demand for new controlled-release options.

The cultivation expansion of cereal and oilseeds, including corn, soybeans, and rapeseed, is propelling the market for poly-sulfur-coated urea. Moreover, excessive urea accumulation in soils has led to depletion, fueling the demand for poly-sulfur-coated controlled-release fertilizers. In addition, the market for poly-sulfur-coated CRFs is poised for growth, driven by factors like the rising demand for highly efficient and eco-friendly products. It is projected to achieve a value CAGR of 6.8% in the region between 2023-2030.

In 2022, China dominated the market for other types of coated controlled-release fertilizers, commanding a 42.3% value share in the CRF market. Of these fertilizers, approximately 69.6% were utilized in field crops, with horticultural crops following suit.

The use of chemical fertilizers has detrimental effects, including soil pH alteration, inhibition of microbial growth, and the release of greenhouse gases from excessive nitrogen application. These environmental concerns, coupled with escalating nutrient losses, are fueling the demand for alternative fertilizers. As a result, the market is projected to witness a CAGR of 6.2% in value during the period spanning from 2023 to 2030.

China dominates the APAC controlled-release fertilizer market

Approximately 70.0% of the population in the Asia-Pacific region depends directly on agriculture as the primary source of their livelihood. However, the region's agriculture sector is facing many issues in terms of low productivity.

China dominates the APAC controlled-release fertilizer market, accounting for 43.8% of the market value share in 2022. Polymer-coated fertilizers accounted for the largest share of the controlled-release fertilizer market, followed by polymer sulfur-coated fertilizers. The polymer-coated fertilizer segment was valued at USD 17.9 million in 2017, and it is anticipated to reach USD 58.0 million by 2030, mainly due to increasing NUE by reducing fertilizer consumption by adopting CRFs.

India is the region's second-largest market for controlled-release fertilizers, accounting for 16.6% in 2022. Controlled-release urea is the most commonly used form of CRF in India. Nitrogen loss is one of the main problems faced by rice farmers, and the efficiency of nitrogen utilization in rice is often inadequate. This is due to the large loss of nitrogen due to volatilization, leaching, and denitrification. One way to improve nitrogen efficiency is to use controlled-release urea. Controlled-release urea generally outperforms granular urea fertilizers in reducing nitrogen loss, stimulating plant growth, and increasing nitrogen concentration.

In 2017, the International Plant Nutrition Institute of China conducted a controlled-release urea fertilizer Application Program in Hubei province. It was proven that the consistent use of CRU fertilizer helps improve the yield and profitability of major crops, such as rice and eggplant. Hence, the market is expected to grow in the future.

The significant expansion of cultivation of major growing crops is anticipated to boost the growth of the market

Field crop cultivation dominates the region, accounting for more than 95% of the total crop area. Rice, wheat, and corn are the major field crops produced in the region, together accounting for about 38% of the total crop area in 2022. The rising area under cultivation is expected to increase the demand for fertilizer usage in the country.

The Asia-Pacific region, which includes China, India, Pakistan, and Australia, is among the world's largest wheat producers. China and India are also the world's largest wheat producers and consumers. The increase in demand and consumption of wheat is due to wheat being one of the major staple foods of this region, and the area increased by a percentage point during the study period. In 2022, China accounted for the production of 138 million metric tons of wheat, making it the largest wheat producer in the world, and India had a wheat production of 103 million metric tons.

Rice is the largest cultivated field crop in the region. Its cultivation alone accounted for about 16.44% of the total agricultural land in 2022. Rice is the staple food of Asia and most parts of the Pacific region. China was projected to produce 147 million tons of rice, and India was expected to harvest 124 million tons of rice in 2022. India was expected to consume 109 million tons while exporting a world-leading 19.5 million tons.

The surge in both domestic and international demand for field crops has prompted an expansion in the cultivation area dedicated to these crops. This significant increase in cultivated land is expected to have a direct and positive impact on the Asia-Pacific CRF market from 2023 to 2030.

About 28% of nitrous oxide emissions from croplands in the world are from China's agricultural lands

In field crops, the average primary nutrient (nitrogen, potassium, and phosphorus) application rate in the country was 129.1 kg/ha in 2022. Nitrogen accounted for 58.5%, potassium for 25.3%, and phosphorus for 16.1% of the average primary nutrient application for field crops. Most primary nutrients were applied through the soil application method. Conventional soil-based primary macronutrient fertilizers accounted for 69.2% of the total primary macronutrient fertilizer market in 2022.

In Asia, the primary nutrient input is high, particularly for nitrogenous and potassic fertilizers, because most soils in the region are deficient in nitrogen and potassic nutrients. However, Asia-Pacific, which is the largest region in the world in terms of land area and population, is also the largest producer and consumer of agrochemicals among all the regions worldwide. About 28% of nitrous oxide emissions from croplands worldwide are from China's agricultural lands.

In field crops, wheat had an average primary nutrient application rate of 214.9 kg/ha, the highest among field crops in 2022. In primary nutrients, nitrogen occupies the first place with an average application rate of 448.5 kg/ha, as nitrogen is required in large amounts for plant metabolism. It is also a major component of chlorophyll and amino acids.

The contamination of surface and groundwater with nitrogen and phosphorus has been considered a result of inadequate advice given to farmers regarding fertilizer application rates and a possible larger crop. However, the trend is shifting toward highly efficient fertilizers.

Asia-Pacific Controlled Release Fertilizer Industry Overview

The Asia-Pacific Controlled Release Fertilizer Market is moderately consolidated, with the top five companies occupying 61.40%. The major players in this market are Grupa Azoty S.A. (Compo Expert), Hebei Sanyuanjiuqi Fertilizer Co., Ltd., ICL Group Ltd, National Fertilizers Ltd and New Mountain Capital (Florikan) (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 Acreage Of Major Crop Types

4.1.1 Field Crops

4.1.2 Horticultural Crops

4.2 Average Nutrient Application Rates

4.2.1 Primary Nutrients

4.2.1.1 Field Crops

4.2.1.2 Horticultural Crops

4.3 Regulatory Framework

4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2030 and analysis of growth prospects)