유럽의 시아노아크릴레이트계 접착제 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Cyanoacrylate Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693420

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

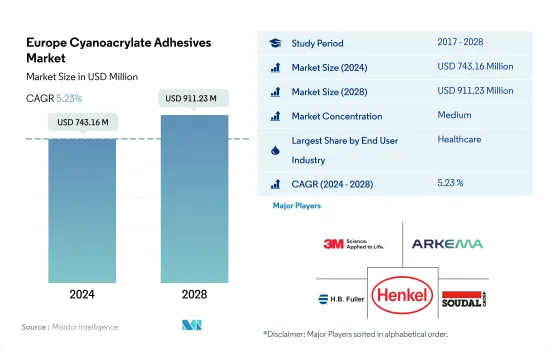

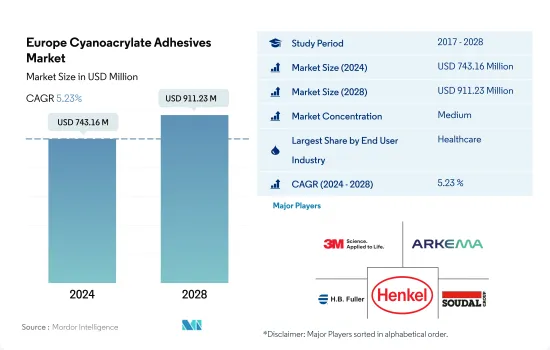

유럽의 시아노아크릴레이트계 접착제 시장 규모는 2024년에 7억 4,316만 달러로 평가되었고, 2028년에는 9억 1,123만 달러에 이를 것으로 예측되며, 예측 기간인 2024-2028년 CAGR 5.23%로 성장할 것으로 예측됩니다.

항공우주 분야의 반응 기술을 기반으로 시아노아크릴레이트계 접착제 수요가 유럽의 성장률 견인

유럽에는 대규모 제조 기지가 있으며 수출 네트워크도 확립되었습니다. 헬스케어, 항공우주, 자동차, 건축 및 건설, 해양은 2017-2019년 시아노아크릴레이트계 접착제에 안정적인 수요를 창출한 이 지역의 수많은 확립된 산업의 하나입니다. 독일, 프랑스, 영국과 같은 국가들은 유럽에서 시아노아크릴레이트계 접착제로 생성된 수요의 더 큰 점유율을 차지합니다.

2020년 시아노아크릴레이트계 접착제에 대한 수요는 COVID-19 팬데믹 때문에 2019년 수준에 비해 11.24% 감소했습니다. 조업, 무역, 공급망의 한계로 인해 자동차, 항공우주 등의 산업은 감산을 피할 수 없었습니다. 이것은 이 기간 동안 이 지역의 시아노아크릴레이트계 접착제 수요에 부정적인 영향을 미쳤습니다.

전 지역 중에서도 유럽의 자동차, 항공우주, 목공 및 건구, 기타 산업은 연구개발 활동에 힘을 쏟고 있습니다. 이 지역의 모든 산업은, 2050년까지 넷 제로 에미션을 달성하기 위해, 카본 풋 프린트의 삭감에 주력하고 있습니다. 자동차 및 항공우주 산업 등 연비 효율과 경량화가 중요한 역할을 하는 산업에서는 예측 기간 동안 시아노아크릴레이트계 접착제 수요가 급증할 수 있습니다. 유럽의 모든 국가 중 프랑스는 예측 기간(2022-2028) 중 6.27%의 CAGR로 시아노아크릴레이트 접착제 수요가 가장 높은 성장세를 보일 것으로 기대됩니다.

시아노아크릴레이트계 접착제 수요는 용도가 많으며, 헬스케어가 가장 큰 점유율을 차지하고 있습니다. 그러나, 항공 우주의 최종 사용자 산업으로부터의 반응성 기술에 의한 시아노아크릴레이트계 접착제 수요의 성장은, 2022-2028년 6.95%의 가장 높은 CAGR로 기대되고 있습니다.

유럽 각국의 항공우주 산업 개발이 시장 성장을 가장 밀어올립니다.

시아노아크릴레이트계 접착제는 조립 시간을 단축하는 데 도움이 되며 주로 헬스케어 산업에서 소비됩니다. 헬스케어 산업은 유럽에서 접착제의 약 3만 7,362톤을 소비해 2021년 유럽 시아노아크릴레이트계 접착제 시장의 36.21%를 차지했습니다. 이러한 접착제는 일회용 의료기기의 제조 및 기타 헬스케어 용도로 사용되고 있습니다.

독일은 유럽에서 시아노아크릴레이트계 접착제의 최대 소비국입니다. 2021년에는 이러한 접착제의 약 40%가 독일 헬스케어 산업에서 사용되었으며, 이는 세계 3위의 헬스케어 산업입니다. 2021년, 이 나라의 의료 지출은 약 7,920억 달러였으며, 이 나라 GDP의 거의 12%에 기여했습니다. 같은 해, 이 나라에 의한 의료기기 수출은 11.85% 증가했습니다. 이 나라의 헬스케어 산업으로부터 이러한 수요의 고조는, 향후 수년간 시아노아크릴레이트계 접착제의 수요를 촉진할 것으로 예상됩니다.

항공우주 산업은 유럽에서 시아노아크릴레이트계 접착제 소비에서 가장 급성장하는 최종 사용자 산업이며, 예측 기간 2022-2028년 CAGR 7.24%를 나타낼 것으로 예상되고 있습니다. 독일의 항공우주 산업은 기술 혁신에 의해 견인되고 있으며, 2021년에는 약 25억 유로가 연구 개발에 사용되었습니다. 프랑스에서는 에어버스가 생산 속도와 생산 능력을 2021년 월산 40대에서 2023년 월산 64대, 2024년 초에는 월산 70대까지 끌어올리겠다는 계획을 발표했습니다. 이러한 요인들로 인해 유럽의 시아노아크릴레이트계 접착제 수요는 향후 수년간 증가할 것으로 예상됩니다.

반응성 시아노아크릴레이트계 접착제는 주로 유럽에서 소비되어 2021년에는 시아노아크릴레이트 총 수요의 75%를 차지했습니다. 그 수요는 예측 기간 중에 한층 더 성장할 것으로 예상됩니다.

유럽의 시아노아크릴레이트계 접착제 시장 동향

전기차를 추진하는 정부의 적극적인 대처가 업계 규모를 밀어 올립니다.

유럽의 1인당 GDP는 3만 4,230달러로, 2022년의 성장률은 전년대비 1.6%였습니다. 자동차 산업 부문이 GDP 전체에서 차지하는 비율은 약 2%였습니다. 2021년 유럽의 자동차 생산량은 승용차 81%, 상용차 17%, 기타 2%였습니다.

2020년에는 독일, 이탈리아, 스페인, 러시아 등 많은 유럽 국가들이 COVID-19 팬데믹의 영향을 받았습니다. 팬데믹은 공급망의 혼란, 각국에서의 조업 중단, 칩 부족을 초래하여 유럽의 자동차 생산에 영향을 주었습니다. 자동차 생산량은 2019년 대비 22%나 급감했습니다.

미국은 유럽에서 25.3% 상당의 자동차를 수입하고 있으며, 2021년에는 독일이 10.3%, 영국이 4.7%를 차지하는 주요 수입국 중 하나가 되었습니다. 2022년 초 러시아의 우크라이나 침공으로 신차 판매가 20.5% 감소하였고 자동차 생산에도 반영되었습니다. 2022년 1분기 유럽 자동차 시장은 전년 동기 대비 10.6% 감소했습니다.

자동차 생산 대수는 많은 유럽 국가들이 전기자동차에 새로운 투자를 하고 있기 때문에 예측 기간(2022-2027년) 중 CAGR 2.25%로 성장할 가능성이 높습니다. 예를 들어, 스페인은 전기차 생산에 51억 달러를 투자할 예정입니다.

심미적이고 스마트한 가구에 대한 수요 증가가 업계 성장을 뒷받침합니다.

유럽은 세계 최고의 가구 생산국입니다. 이 지역은 아시아태평양에 이어 세계 가구 생산의 거의 30%를 차지합니다. 독일, 이탈리아, 러시아, 스페인이 가구와 그 제품의 최고 생산국입니다. 그러나 이 지역은 2020년에 발생한 코로나19의 영향으로 여러 나라에서 생산 시설의 조업을 중단해야 했습니다. 이 때문에 가구 생산량은 전년 대비 7.14% 감소했습니다.

독일은 유럽 최대의 가구 생산국입니다. 2021년에는 3억 2,360만개 가까이를 생산해, 이것은 유럽의 가구 생산량의 23%에 해당했습니다. 독일 소매업체들은 3D 제품 비주얼라이제이션과 증강현실 앱을 제공하기 시작했고, 이것이 이 나라 전자상거래 포털을 통해 가구 제품의 수요를 끌어올리고 있습니다.

이탈리아 역시 유럽의 가구와 그 제품의 주요 생산국이며 이탈리아 가구가 인기의 나라입니다. 이 나라는 유럽 가구 생산의 15%를 차지하고 있습니다. 이 나라의 가구 수출은 일정한 성장률을 기록하고 있으며, 2018년은 약 2.7%, 2019년은 약 3%였습니다. 이탈리아의 목공 및 창호 산업에 있어서의 기술 진보는 세계적으로 채용되고 있습니다.

유럽은 가구 시장의 하이엔드 부문을 선도하고 있습니다. 세계에서 판매되는 고급 가구 제품 3개 중 2개 가까이가 EU에서 생산되고 있다고 합니다. 유럽의 가구 제조업체는, 파인재, 오크재, 너도밤나무재 등, 환경 친화적인 소재를 생산에 사용하고 있어, 이 지역에서의 수요가 높아지고 있습니다. 이러한 요인에 의해 향후 수년간 유럽에서의 가구 생산은 증가할 것으로 생각됩니다.

유럽의 시아노 아크릴레이트 접착제 산업 개요

유럽의 시아노아크릴레이트계 접착제 시장은 상위 5개사에서 63.01%를 차지하며 완만하게 통합되어 있습니다. 이 시장의 주요 기업은 다음과 같습니다. 3M, Arkema Group, H.B. Fuller Company, Henkel AG & Co. KGaA and Soudal Holding N.V.(알파벳순 정렬)

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

조사의 전제조건 및 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

신발 및 가죽

목공 및 건구

규제 프레임워크

EU

러시아

밸류체인 및 유통 채널 분석

제5장 시장 세분화

최종 사용자 산업별

항공우주

자동차

건축 및 건설

신발 및 가죽

헬스케어

목공 및 건구

기타 최종 사용자 산업

기술별

반응성

UV 경화형 접착제

국가별

프랑스

독일

이탈리아

러시아

스페인

영국

기타 유럽

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

DELO Industrie Klebstoffe GmbH & Co. KGaA

HB Fuller Company

Henkel AG & Co. KGaA

Illinois Tool Works Inc.

Jowat SE

Permabond LLC.

Soudal Holding NV

ThreeBond Holdings Co., Ltd.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업의 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인 및 기회

정보원 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

AJY

영문 목차

영문목차

The Europe Cyanoacrylate Adhesives Market size is estimated at 743.16 million USD in 2024, and is expected to reach 911.23 million USD by 2028, growing at a CAGR of 5.23% during the forecast period (2024-2028).

Demand for cyanoacrylate adhesives based on reactive technology in aerospace to lead in growth rate in Europe

Europe has a large manufacturing base and well-established export networks. Healthcare, aerospace, automotive, building and construction, and marine are among the few well-established industries in the region which have collectively generated steady demand for cyanoacrylate adhesives from 2017 to 2019. Countries like Germany, France, and The United Kingdom have occupied a larger share of the demand generated for cyanoacrylate adhesives from the Europe region.

In 2020, the demand for cyanoacrylate adhesives declined by 11.24% compared to the 2019 levels because of the covid-19 pandemic. Operational, trade and supply chain restrictions have forced industries like automotive, aerospace, and others to have production cuts. This has negatively affected the demand for cyanoacrylate adhesives from the region during this period.

Among all regions, European automotive, aerospace and woodworking and joinery, and other industries are heavily engaged in R&D activities. All Industries in the region are focusing on reducing their carbon footprint to achieve a net zero emissions goal by 2050. Industries like automotive and aerospace, where fuel efficiency and weight reduction play an important role, might witness a surge in demand for cyanoacrylate adhesives during the forecast period. Among all countries in Europe, France is expected to witness the highest growth in the demand for cyanoacrylate adhesives, with a CAGR of 6.27% during the forecast period (2022-2028).

Healthcare occupies the largest share of the demand for cyanoacrylate adhesives because of the large number of applications. However, the growth in demand for cyanoacrylate adhesives with reactive technology from the aerospace end-user industry is expected to be with the highest CAGR of 6.95% in 2022-2028.

Developments in the aerospace industry across the European countries to have boost the market's growth the most

Cyanoacrylate adhesives help in the reduction of assembly times and are consumed mainly in the healthcare industry. The healthcare industry consumes around 37,362 tons of adhesives in Europe, which accounted for 36.21% of the European cyanoacrylate adhesives market in 2021. These adhesives are used to manufacture disposable medical devices and other healthcare applications.

Germany is the largest consumer of cyanoacrylate adhesives in Europe. In 2021, around 40% of these adhesives were used in the healthcare industry of Germany, which is the third largest healthcare industry globally. In 2021, the healthcare expenditure in the country was around USD 792 billion and contributed nearly 12% of the country's GDP. In the same year, the exports of medical devices by the country increased by 11.85%. Such rising demand from the healthcare industry in the country is expected to drive the demand for cyanoacrylate adhesives over the coming years.

Aerospace is the fastest-growing end-user industry in the consumption of cyanoacrylate adhesives in Europe and is expected to record a CAGR of 7.24% during the forecast period 2022-2028. Germany's aerospace industry is driven by technological innovation, and around EUR 2.5 billion was spent on research and development in 2021. In France, Airbus announced plans to increase production speeds and capacity from 40 aircraft per month in 2021 to 64 per month in 2023 and as many as 70 per month by early 2024. These abovementioned factors are expected to boost the demand for cyanoacrylate adhesives over the coming years in Europe.

Reactive cyanoacrylate adhesives are primarily consumed in Europe and accounted for 75% of the total cyanoacrylate demand in 2021. Their demand is expected to grow further over the forecast period.

Europe Cyanoacrylate Adhesives Market Trends

Supportive government initiatives to promote electric vehicles will raise the industry size

Europe has a GDP of 34,230 USD per capita with a growth rate of 1.6% y-o-y in 2022. The automotive industry sector contributes a percentage of around 2% of the total GDP. The European vehicle production comprises 81% passenger vehicles, 17% commercial vehicles, and 2% other vehicles in 2021.

In 2020, many European countries were affected by the COVID-19 pandemic, including Germany, Italy, Spain, Russia, and the United Kingdom. The pandemic resulted in supply chain disruptions, lockdowns in the countries, and chip shortages which affected automotive production in Europe. The production of vehicles sharply declined by 22% compared to 2019.

The United States imports 25.3% worth of cars from Europe and became one of the leading importers of the United States, where Germany accounted for 10.3% and the United Kingdom for 4.7% of total imports of vehicles in the country in 2021. At the beginning of 2022, the sale of the new vehicle dropped by 20.5% due to the invasion of Ukraine by Russia, which reflected in vehicle production as well. In the first quarter of 2022, the European automotive market was down by 10.6% compared to the same period last year.

Vehicle production is likely to grow with a CAGR of 2.25% during the period (2022 to 2027) due to the new investments being made in electric vehicles by many European countries. For instance, Spain is going to invest USD 5.1 billion in electric vehicle production.

Rising demand for aesthetic and smart furniture to aid the industry growth

Europe is one of the largest producers of furniture in the world. The region contributes nearly 30% of global furniture production after the Asia-Pacific region. Germany, Italy, Russia, and Spain are the top producers of furniture and its products. However, the region was impacted by the COVID-19 outbreak in 2020, which resulted in the shutdown of production facilities in several countries. This has reduced their furniture production by 7.14% compared to the previous year.

Germany is the largest producer of Furniture units in Europe. The country produced nearly 323.6 million units in 2021, which is 23% of Europe's furniture production. German retailers have started offering 3D product visualizations or augmented reality apps which are boosting the demand for furniture products through e-commerce portals in the country.

Italy is another major producer of furniture and its products in Europe, and the country is popular for Italian Furniture. The country holds 15% of Europe's furniture production. The country's furniture exports recorded a constant growth rate, which was about 2.7% in 2018 and 3% in 2019. The technological advancement in the woodworking and joinery industry of Italy is adopted worldwide.

Europe is a leader in the high-end segment of the furniture market. It is said that nearly two out of every three high-end furniture products sold in the world are produced in the European Union. The furniture manufacturers in Europe are using eco-friendly materials such as pine wood, oak wood, beech wood, and a few others for production, which is gaining demand in the region. These factors will raise furniture production in the coming years in Europe.

Europe Cyanoacrylate Adhesives Industry Overview

The Europe Cyanoacrylate Adhesives Market is moderately consolidated, with the top five companies occupying 63.01%. The major players in this market are 3M, Arkema Group, H.B. Fuller Company, Henkel AG & Co. KGaA and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.1.4 Footwear and Leather

4.1.5 Woodworking and Joinery

4.2 Regulatory Framework

4.2.1 EU

4.2.2 Russia

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Footwear and Leather

5.1.5 Healthcare

5.1.6 Woodworking and Joinery

5.1.7 Other End-user Industries

5.2 Technology

5.2.1 Reactive

5.2.2 UV Cured Adhesives

5.3 Country

5.3.1 France

5.3.2 Germany

5.3.3 Italy

5.3.4 Russia

5.3.5 Spain

5.3.6 United Kingdom

5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 DELO Industrie Klebstoffe GmbH & Co. KGaA

6.4.4 H.B. Fuller Company

6.4.5 Henkel AG & Co. KGaA

6.4.6 Illinois Tool Works Inc.

6.4.7 Jowat SE

6.4.8 Permabond LLC.

6.4.9 Soudal Holding N.V.

6.4.10 ThreeBond Holdings Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)