ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

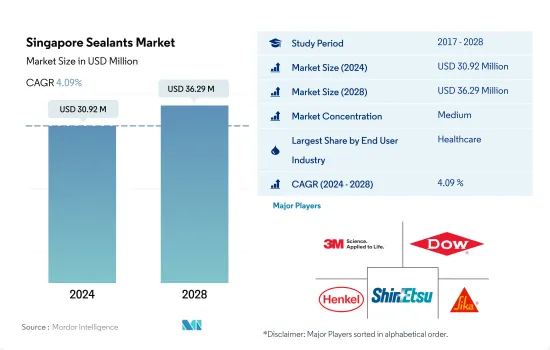

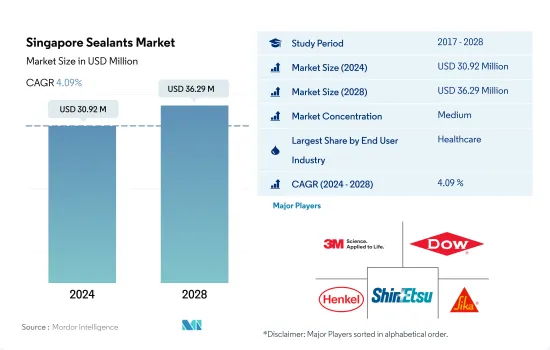

싱가포르의 실란트 시장 규모는 2024년 3,092만 달러, 2028년에는 3,629만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR 4.09%로 성장할 전망입니다.

싱가포르의 의료기기 제조업 성장이 이 나라의 실란트 수요에 큰 영향을 줄 것으로 예측됩니다.

싱가포르의 실란트 시장은 주로 기타 최종 사용자 산업 부문이 지배적이며, 헬스케어 산업이 이에 이어집니다. 커머스 활동의 급성장과 가전 부문의 강력한 시장 포지셔닝이 싱가포르의 실란트 시장 규모를 밀어 올릴 가능성이 높습니다.

방수, 내후성 실링, 균열 실링, 조인트 실링 등 DIY 용도도 최근 인기를 얻고 있습니다.

헬스케어 산업에서는 주로 의료기기 부품의 조립이나 씰에 실란트가 사용되고 있습니다.

싱가포르 실란트 시장 동향

공공 건축물 건설에 대한 지속적이고 미래의 투자는 최종 사용자 산업을 지원합니다.

싱가포르의 건설 업계는 2022년부터 2028년의 예측기간 중 약 2.6%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측되고 있습니다. 건설 수요는 2019년에 5년만의 고수준에 도달해 추정 334억 SGD 상당의 프로젝트가 수주되어 상기 예측의 320억 SGD를 상회했습니다. 이는 2018년에 비해 건설 수요가 9.5% 증가한 것을 나타냅니다. 그러나 2020년에는 COVID-19 팬데믹의 영향으로 프로젝트 실시 스케줄이 혼란해 건설 수요의 속보치는 36.5% 감소한 213억 SGD가 되었습니다. 싱가포르의 건설용 접착제 및 실란트 시장은 2022-2028년의 예측 기간 중에 수량으로 약 2.86%, 금액으로 약 5.31%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측되고 있습니다.

공공 부문 건설은 2019년 190억 SGD에서 2020년 132억 SGD로 감소했지만, 이는 유통관리가 자원 관리 및 프로젝트 스케줄링에 미치는 영향을 검토하는 데 시간이 필요했기 때문에 특정 대형 인프라 프로제 또한 싱가포르의 건설 수요는 2022년에는 270억-320억 달러에 달할 것으로 추정되며, 공공 부문이 수요 전체의 약 60%를 차지할 것으로 보입니다.

한편, 싱가포르의 주택건설은 남아있는 건물의 재고 증가로 여전히 저조하고, COVID-19의 유행에 의한 경기후퇴에 의해 더욱 악화되고 있습니다. 밀도를 낮추기 위해, 정부는 2020년 말까지 약 6만명의 이주 노동자용으로 주택을 추가 건설할 계획을 세우고 있었습니다. 이러한 요인은 예측 기간중, 접착제 및 실란트 수요를 억제할 것으로 예상됩니다.

민간항공 수요 증가가 이 나라의 항공우주산업을 촉진

싱가포르의 항공우주 섹터는 아시아태평양 시장을 독점하고 있습니다.

싱가포르는 예상되는 개발 패턴을 활용하기 위해 아시아태평양의 주요 항공 허브로서 인프라를 개선하기 위해 노력하고 있습니다. Changi Terminal 5(T5)는 세계 최대급 공항터미널이 될 전망입니다.

Changi Terminal 5의 건설을 서두르면서 싱가포르 항공 업계는 팬데믹에 의해 3만 5,000명의 직원의 3분의 1을 잃은 후, 2022년 말까지 팬데믹 전 노동력의 85%에서 90%를 회복시키고 싶습니다.

민간항공은 싱가포르의 항공우주산업에서 가장 큰 점유율을 차지하고 있습니다. 기관 간 진행중인 협력 관계는 싱가포르의 소형 위성의 능력을 확대하고 혁신적인 우주 서비스와 애플리케이션을 창출하는 것을 목표로하고 있습니다.

싱가포르 실란트 산업 개요

싱가포르의 실란트 시장은 적당히 통합되어 있으며 상위 5개사에서 52.63%를 차지하고 있습니다. 시장의 주요 기업에는 3M, Dow, Henkel AG & Co. KGaA, Shin-Etsu Chemical and Sika AG(알파벳순)가 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

규제 프레임워크

싱가포르

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

헬스케어

기타 최종 사용자 산업

수지

아크릴

에폭시

폴리우레탄

실리콘

기타 수지

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

ALTECO co., ltd.

Arkema Group

Dow

HB Fuller Company

Henkel AG & Co. KGaA

PFE Technologies Pte Ltd

Shin-Etsu Chemical Co., Ltd.

Sika AG

Soudal Holding NV

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업의 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 저해요인, 기회

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Singapore Sealants Market size is estimated at 30.92 million USD in 2024, and is expected to reach 36.29 million USD by 2028, growing at a CAGR of 4.09% during the forecast period (2024-2028).

The forecasted growth in the medical device manufacturing of Singapore to significantly influence the sealants demand in the country

The Singaporean sealants market is dominated mainly by the other end-user industries segment, followed by the healthcare industry. The other end-user industries segment comprises electronics and electrical components, locomotive, marine, DIY, etc., of which the electronics industry holds the major share due to the diverse applications. They are used for sealing sensors and cables, etc. Moreover, the rapid growth of e-commerce activities and the strong market positioning of the consumer electronics segment are likely to propel the size of the Singaporean sealants market. However, the electronics industry's growth declined in 2020 due to the COVID-19 pandemic and resultant restrictions, which caused a scarcity of raw materials. However, the raw materials supply chain was restored in 2021, which led to a hike in demand for sealants across the country.

DIY applications, such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing, have also recently gained popularity. Sealants are designed to provide longevity and ease of application on different substrates. The DIY industry in Singapore is expected to grow at a rate of 14.31%, which will create scope for the sealants market over the coming years.

The healthcare industry primarily uses sealants for assembling and sealing medical device parts. Medical-grade sealants have unique applicability to various substrates such as glass, metal, plastic, painted surfaces, etc., and their features, such as weather-proofing, heat resistance, and anti-aging, are likely to boost the sealants' demand. Singapore is expected to register significant growth in medical device manufacturing due to unprecedented demand from the domestic sector. Such developments are expected to boost sealant demand over the forecast period.

Singapore Sealants Market Trends

Ongoing and upcoming investments in the construction of public buildings will support the end-user industry

The Singaporean construction industry is projected to record a CAGR of about 2.6% during the forecast period from 2022 to 2028. The construction demand hit a five-year high in 2019, with an estimated SGD 33.4 billion worth of projects awarded, higher than its top-end projection of SGD 32 billion. This represented a 9.5% increase in construction demand compared to 2018. However, in 2020, due to the impact of the COVID-19 pandemic, which disrupted project implementation schedules, the preliminary figure for construction demand witnessed a decline of 36.5% to SGD 21.3 billion. The Singaporean construction adhesives and sealants market is projected to record a CAGR of about 2.86% in volume and 5.31% in value during the forecast period 2022-2028.

Public sector construction declined from SGD 19 billion in 2019 to SGD 13.2 billion in 2020, as certain large infrastructure projects were postponed due to the need for more time to examine the pandemic's impact on resource management and project scheduling. Moreover, construction demand in Singapore is estimated to be between USD 27 billion and USD 32 billion in 2022, and the public sector is likely to provide roughly 60% of the overall demand. The public sector's construction demand is expected to range between USD 16 billion and USD 19 billion.

On the other hand, residential construction in Singapore remains weak due to the growing stock of unsold buildings, further aggravated by the economic downturn due to the COVID-19 pandemic. However, to reduce the population density in dormitories amid the pandemic, the government had planned to construct additional housing for around 60,000 migrant workers by the end of 2020. These factors are expected to restrain the demand for adhesives and sealants over the forecast period.

Increasing demand from civil aviation will propel the aerospace industry in the country

The aerospace sector in Singapore dominates the Asia-Pacific market. The Singaporean aerospace sector registered a CAGR of 8.6% during the last two decades, with a total yearly output of more than USD 8 billion in 2020. It is a significant economic driver for Singapore.

Singapore strives to improve its infrastructure as the principal aviation hub in Asia-Pacific to capitalize on anticipated development patterns. The Changi Airport is witnessing the construction of the massive Terminal 5. When it is finished in the 2030s, Changi Terminal 5 (T5) is expected to be one of the largest airport terminals in the world. In its initial operation phase, T5 will have the capacity to handle up to 50 million passengers annually, bringing the airport's total annual passenger handling capacity to 135 million.

Along with pressing forward with the construction of Changi Terminal 5, Singapore's aviation industry hopes to have restored 85% to 90% of its pre-COVID-19 pandemic workforce by the end of 2022 after losing a third of its 35,000 staff to the pandemic.

Civil aviation holds the largest share of Singapore's aerospace industry. Around 16 civil aircraft were delivered to the country in 2021, compared to 9 units in 2020, and it is forecasted that around 32 civil aircraft will be needed in 2028. In addition, ongoing collaborations between businesses and research institutions aim to expand Singapore's small satellite capacity and produce innovative space services and applications. Therefore, all the abovementioned factors are likely to impact the market studied.

Singapore Sealants Industry Overview

The Singapore Sealants Market is moderately consolidated, with the top five companies occupying 52.63%. The major players in this market are 3M, Dow, Henkel AG & Co. KGaA, Shin-Etsu Chemical Co., Ltd. and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.2 Regulatory Framework

4.2.1 Singapore

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Healthcare

5.1.5 Other End-user Industries

5.2 Resin

5.2.1 Acrylic

5.2.2 Epoxy

5.2.3 Polyurethane

5.2.4 Silicone

5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 ALTECO co., ltd.

6.4.3 Arkema Group

6.4.4 Dow

6.4.5 H.B. Fuller Company

6.4.6 Henkel AG & Co. KGaA

6.4.7 PFE Technologies Pte Ltd

6.4.8 Shin-Etsu Chemical Co., Ltd.

6.4.9 Sika AG

6.4.10 Soudal Holding N.V.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)