India Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693398

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

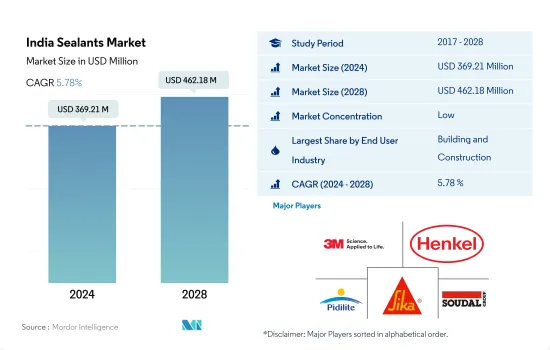

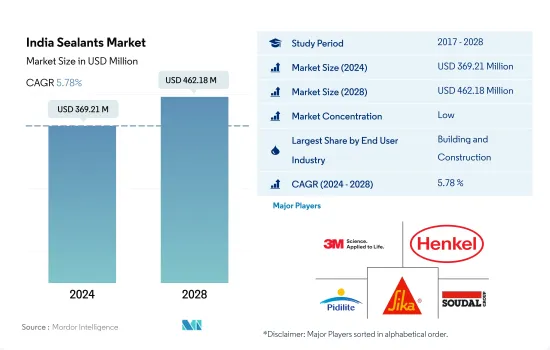

인도의 실란트 시장 규모는 2024년에 3억 6,921만 달러로 평가되었고, 2028년에는 4억 6,218만 달러에 이를 것으로 예측되며, 예측 기간(2024-2028년)동안 CAGR 5.78%로 성장할 것으로 예측됩니다.

자동차시장과 건설산업의 상승이 인도 실란트 소비를 끌어올릴 전망

건설 산업은 인도의 실란트 시장을 독점하고 있으며, 방수, 내후성 실링, 균열 실링, 눈지 실링 등, 건축 및 건설 활동에 있어서의 실란트의 다양한 용도에 의해 기타 최종사용자 산업이 그에 이어지고 있습니다. 인도의 건설 부문은 COVID-19 팬데믹의 악영향을 상쇄하여 2021년에는 국가의 GDP의 약 9%를 차지했습니다.

다양한 실란트는 전기기기 제조에 있어 포팅이나 보호용도로 사용되고 있으며, 이들은 센서나 케이블 등의 밀봉에 사용됩니다. 인도 전자제품 시장은 2021년 인도 GDP의 거의 2.5%를 차지했으며, 통신 및 가전제품 시장의 수요 증가로 인해 향후 몇 년간 유망한 성장을 기록할 가능성이 높습니다. 이것은 다른 최종 사용자 산업 부문에서의 실란트 수요를 촉진하는 것으로 예측됩니다.

실란트는 자동차 산업에서 다양한 용도가 있으며, 주로 엔진이나 자동차의 개스킷에 사용되어 다양한 기재에 광범위하게 접착합니다. 자동차 생산에서 상당한 성장을 이루고 있으며, 이 경향은 앞으로도 계속될 것으로 보입니다.

인도 실란트 시장 동향

Housing for All(모두를 위한 주택)이나 Pradhan Mantri Awas Yojana(PMAY) 등 주택 부문에 대한 정부 투자와 이니셔티브가 건설 산업을 견인

건설산업은 인도 2위 산업이며, GDP 공헌도는 약 9%로 2019년도 유망한 성장을 보였습니다. 건설 산업은 인도에서 두 번째로 큰 산업이며, GDP에의 공헌도는 약 9%입니다. 인도는 2025년까지 세계 제3위의 건설 시장이 될 것으로 예상되고 있습니다. 또한, 건설 산업은 예측 기간중(2022-2028년)에 약 3.79%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되고 있습니다.

주택 부문에서는 정부가 향후 몇 년 동안 거대한 프로젝트를 추진하고 있습니다. 이는 2023년까지 주거용 건설(시장에서 가장 큰 카테고리)에 상당한 도움이 될 것이며, 업계 전체 가치의 3분의 1 이상을 차지할 것입니다. 또, Pradhan Mantri Awas Yojana(PMAY)와 같은 이니셔티브는 2022년까지 많은 사람들에게 저렴한 주택을 제공하는 것을 목표로 했습니다. 또, 정부는 국민이 처음으로 집을 세우거나 구입하는 경우, 주택 대출 이자에 대한 일부 보조금을 제공하는 방안도 검토하고 있습니다.

인도는 또한 건설 부문에서 해외 투자자들의 큰 관심을 받고 있습니다. 2,000년 4월부터 2020년 3월까지 건설 개발 부문(타운십, 주택, 건설 인프라, 건설 개발 프로젝트)에 대한 외국인 직접 투자(FDI)는 256억 6,000만 달러에 달했습니다.

e-AMRIT와 자동차 대출 금리의 2-3% 저하 등 정부의 이니셔티브의 고조가 자동차 제조를 견인

인도의 자동차 산업은 2020년에는 아시아태평양에서 4위 규모가 됐습니다.

COVID-19의 유행에 의해 전국적인 봉쇄, 공급 체인의 혼란, 전체적인 경기 감속 때문에 승용차의 판매 대수는 2019년의 338만대에서 2021년에는 239만대로 떨어졌습니다. 제조부문을 지원하는 정부의 대처에 의해 2022년 3월에는 272만대까지 증가했습니다.승용차 부문에서는 멀티 스즈키가 최대로, 2021년 시장 점유율은 52%입니다.

상용차의 경우 타타 모터스가 대수 기준으로 최대이며, 2022년 3월 시장 점유율은 43% 가까이에 달하고 있습니다. 상업용 차량 판매량은 2020년 코로나19의 영향으로 손실이 컸던 경제가 회복됨에 따라 2021년 568,560대에서 2022년 3월에는 71만 6,570대로 증가했습니다.

e-AMRIT와 같은 이니셔티브를 가진 인도 정부에 의한 전기자동차 제조의 추진은 2028년까지 수년간 전기자동차 생산 증가로 이어집니다.

인도 실란트 산업 개요

인도의 실란트 시장은 세분화되어 있으며 상위 5개사에서 21.68%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

규제 프레임워크

인도

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

의료

기타

수지

아크릴

에폭시

폴리우레탄

실리콘

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

ASTRAL ADHESIVES

Dow

Henkel AG & Co. KGaA

Jubilant Industries Ltd.

Pidilite Industries Ltd.

Sika AG

Soudal Holding NV

Wacker Chemie AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

SHW

영문 목차

영문목차

The India Sealants Market size is estimated at 369.21 million USD in 2024, and is expected to reach 462.18 million USD by 2028, growing at a CAGR of 5.78% during the forecast period (2024-2028).

Emerging automotive market and construction industry are expected to boost the consumption of sealants in India

The construction industry dominates the Indian sealants market, followed by other end-user industries due to the diverse applications of sealants in building and construction activities, such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. Construction sealants are designed for longevity and ease of application on different substrates. The Indian construction sector accounted for about 9% of the nation's GDP in 2021 by offsetting the adverse impacts of the COVID-19 pandemic. The Indian government continuously promotes low-energy buildings and sustainable development, which is expected to increase the demand for sealants over the forecast period gradually.

Various sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables, etc. The Indian electronics market accounted for nearly 2.5% of the country's GDP in 2021 and is likely to record promising growth over the coming years due to the growing demand from the telecommunication and domestic appliances market. This, in turn, will foster the demand for sealants in the other end-user industry segment. India has showcased considerable growth in the locomotive, marine, and DIY industries, which is expected to boost the demand for the required sealants by 2028.

Sealants have diverse applications in the automotive industry and exhibit extensive bonding to various substrates, mainly used for engines and car gaskets. India has achieved decent growth in automotive production due to the shifting consumer trend toward personal mobility, which is likely to continue over the coming years. Thus, such a trend is expected to augment the demand for sealants over the forecast period 2022-2028.

India Sealants Market Trends

Government investments and initiatives such as Housing for All and Pradhan Mantri Awas Yojana (PMAY) for the housing sector to lead the construction industry

The construction industry is the second-largest industry in India, with a GDP contribution of about 9%, and it showed promising growth in 2019. However, due to the outbreak of COVID-19, the construction sector witnessed a significant decline, owing to the lockdown by the government for a brief period. The construction industry is the second-largest industry in India, with a GDP contribution of about 9%. India is expected to become the third-largest construction market in the world by 2025. Moreover, the construction industry is expected to register a CAGR of about 3.79% during the forecast period (2022 - 2028).

In the residential segment, the government is pushing huge projects in the next few years. The government's 'Housing for All initiative aims to build more than 20 million affordable homes for the urban poor by 2022. This will provide a significant boost to residential construction (the market's largest category) and accounts for more than a third of the industry's total value by 2023. Furthermore, initiatives such as Pradhan Mantri Awas Yojana (PMAY) are intended to provide affordable homes to many people by 2022. The government is also into providing some subsidiary on interest on housing loans if a citizen builds/buys their first house.

India is also witnessing significant interest from international investors in the construction space. Foreign Direct Investment (FDI) in the construction development sector (townships, housing, built-up infrastructure, and construction development projects) stood at USD 25.66 billion from April 2000 to March 2020. The increasing infrastructure and construction development across the nation leads to an increase in the demand for adhesives and sealants.

Rising government initiatives such as e-AMRIT and auto loan interest rates decrease by 2-3% to lead the automotive manufacturing

The Indian automotive industry was the fourth largest in the Asia-Pacific by volume in 2020. With the government initiatives such as the expansion of roads in 2021 by allocation of funds of INR 4.32 trillion, the number of vehicles has also increased on roads. This trend of growth is expected to sustain in the coming years up to 2028.

Due to the COVID-19 pandemic, there was a dip in sales of passenger vehicles from 3.38 million in 2019 to 2.39 million in 2021 because of nationwide lockdown, supply chain disruptions, and overall economic slowdown. But, with the government initiatives to support the automobile manufacturing sector, such as decreasing interest rates for auto loans by 2-3%, it moved up to 2.72 million vehicles by March 2022. Maruti Suzuki is the largest in the passenger vehicles segment, with a market share of 52% in 2021. This growth trend is expected to sustain in the forecast period, which is 2022-2028.

In the case of commercial vehicles, Tata Motors is the largest vehicle producer by number, with a market share of nearly 43% in March 2022. The commercial vehicle sales increased from 568,560 in 2021 to 716570 by March 2022 because of recovering loss-ridden economy due to the impact of COVID-19 in 2020. With this growing post-pandemic economy, it is expected to increase in the mentioned period.

The electric vehicle manufacturing push by the Indian government with initiatives such as e-AMRIT will lead increase in the production of electric vehicles in years up to 2028. The increase in the number of electric vehicles being sold in India increased by 108% in 2021 compared to 2020.

India Sealants Industry Overview

The India Sealants Market is fragmented, with the top five companies occupying 21.68%. The major players in this market are 3M, Henkel AG & Co. KGaA, Pidilite Industries Ltd., Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.2 Regulatory Framework

4.2.1 India

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Healthcare

5.1.5 Other End-user Industries

5.2 Resin

5.2.1 Acrylic

5.2.2 Epoxy

5.2.3 Polyurethane

5.2.4 Silicone

5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 ASTRAL ADHESIVES

6.4.4 Dow

6.4.5 Henkel AG & Co. KGaA

6.4.6 Jubilant Industries Ltd.

6.4.7 Pidilite Industries Ltd.

6.4.8 Sika AG

6.4.9 Soudal Holding N.V.

6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)