중국의 실란트 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

China Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693396

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

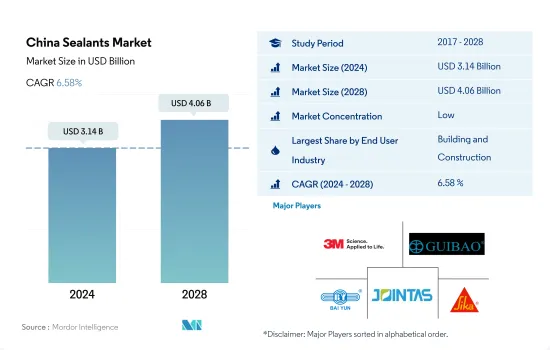

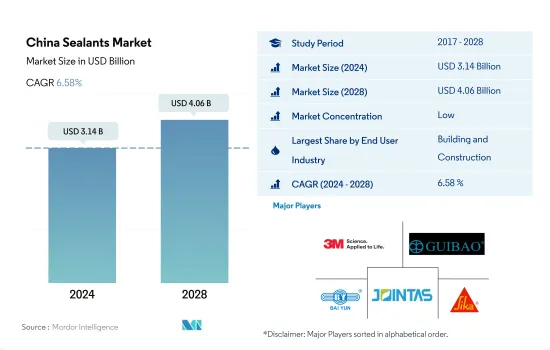

중국의 실란트 시장 규모는 2024년 31억 4,000만 달러, 2028년에는 40억 6,000만 달러에 이를 것으로 예측되며, 예측기간 중(2024-2028년) CAGR 6.58%로 성장할 전망입니다.

방수, 균열 씰, 조인트 씰의 용도로 건설용 실란트가 시장을 밀어 올립니다.

중국의 실란트 시장은 방수, 크랙 실링, 조인트 실링 등 건축 및 건설 활동에 있어서의 실란트의 다양한 용도에 의해 건설 업계가 주요한 견인역이 되고, 기타 최종 사용자 업계가 뒤를 이었습니다. 실란트는 수명이 길고 다양한 기재에 쉽게 도포할 수 있도록 설계되어 있습니다.

전기 장비 제조는 포팅 및 보호 용도에 다양한 실란트를 사용합니다. 이들은 센서 및 케이블과 같은 씰링에 사용됩니다. 기존의 향후 수년간 지속적인 성장이 예상됩니다.

실란트는 헬스케어와 자동차 산업에 있어서 다양한 용도가 있습니다. 주로 엔진이나 자동차의 개스킷에 사용되고 있습니다. 중국은 최근, 이러한 분야, 특히 자동차 산업에서 유망한 성장을 기록하고 있어 향후 수년간 계속될 것으로 보이며, 2028년까지 실란트 수요를 증대시킬 것으로 예상됩니다.

중국 실란트 시장 동향

중국 정부의 의료, 병원, 의료 시설 건설 계획이 중국 건설 견인

중국은 주택 및 상업 건설 부문의 풍부한 개발에 의해 크게 견인되고 있으며, 경제 성장에 지원되고 있습니다. 도시화의 결과, 도시에서 필요로 하는 거주 공간이 확대되어, 도시의 중산계급 주민이 생활 환경의 개선을 바라게 되는 것은 주택 시장에 큰 영향을 주어, 그것에 의해 국내의 주택 건설이 증가할 가능성이 있습니다.

비주거 인프라는 크게 확대될 가능성이 높습니다. 고령화가 진행 중인 중국에서는 의료 시설과 병원의 증설이 필요합니다. 중국 정부는 2019년에 약 1,420억 달러 규모의 26개 인프라 프로젝트를 승인했으며, 2023년에 완공될 예정입니다. 중국은 세계 최대 건설 시장으로 전 세계 건설 투자의 20%를 차지하고 있습니다.

중국에서는 홍콩 주택 당국이 저가 주택 건설을 추진하기 위해 몇 가지 시책을 시작했습니다. 움직임이 함께, 이 나라의 주택 건설 섹터 수요는 계속 확대될 것으로 예상됩니다.

정부 정책은 중국에서의 EV 수요를 높여 자동차 생산을 촉진할 가능성이 높습니다.

중국의 승용차 시장은 2021년에 2,141만대를 차지해, 일본, 미국, 독일 등 다른 주요 세계 기업과 비교해 세계 최대입니다.

COVID-19 팬데믹의 진원지인 중국에서는 전국적인 조업 정지, 공급 체인의 혼란, 인재 부족 등이 발생해, 2020년의 자동차 산업에서 막대한 손실이 발생했습니다.

중국 정부에 의한 전기자동차 소유자에 대한 기간 한정의 구입 보조금, 교통 규제의 면제, 충전 리베이트 등의 정책은 중국에 있어서의 전기자동차의 판매와 수요를 촉진했습니다. 중국의 EV 생산 대수는 2019년 100만대에서 2021년에는 350만대로 증가하고, 예측 기간 중(2022-2028년) CAGR은 15.07%를 나타낼 것으로 예상됩니다.

Shanghai Automotive Industry Corporation는 생산 대수로 중국 최대의 자동차 회사입니다.

중국의 실란트 산업 개요

중국의 실란트 시장은 세분화되어 있으며 주요 5개사에서 20.34%를 차지하고 있습니다. 이 시장 주요 기업은 3M, Chengdu Guibao Science and Technology Co., Ltd., Guangzhou Baiyun Chemical Industry Co.,ltd., Guangzhou Jointas Chemical Co.,Ltd., Sika AG(알파벳순)입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

규제 프레임워크

중국

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

헬스케어

기타 최종 사용자 산업

수지

아크릴

에폭시

폴리우레탄

실리콘

기타 수지

제6장 경쟁 구도

주요 전략적 움직임

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

Chengdu Guibao Science and Technology Co., Ltd.

Dow

Guangzhou Baiyun Chemical Industry Co.,ltd.

Guangzhou Jointas Chemical Co.,Ltd.

HB Fuller Company

Hangzhou Zhijiang Advanced Material Co., ltd.

Henkel AG & Co. KGaA

Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업의 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 저해요인, 기회

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The China Sealants Market size is estimated at 3.14 billion USD in 2024, and is expected to reach 4.06 billion USD by 2028, growing at a CAGR of 6.58% during the forecast period (2024-2028).

Construction sealants to boost the sealants, owing to waterproofing, cracks-sealing, and joint-sealing applications

The China sealants market is majorly driven by the construction industry, followed by other end-user industries due to diverse applications of sealants in building and construction activities, such as waterproofing, cracks-sealing, and joint-sealing. Moreover, construction sealants are designed for longevity and ease of application on different substrates. The construction sector achieved a GDP of 6.9% in 2020 despite supply chain disruption and production suspension due to COVID-19 impacts.

A variety of sealants are used in electrical equipment manufacturing for potting and protecting applications. They are used for sealing sensors and cables, etc. The Chinese electronics market registered a market share of 41% globally in 2020 and is likely to have sustainable growth in the upcoming years due to the extensive presence of the manufacturing ecosystem with a huge labor force. This, in terms, will foster the demand for sealants in the other end-user segment. Moreover, China has a massive production capacity for locomotive and marine industries in the world, boosting the demand for required sealants.

Sealants have diverse applications in the healthcare and automotive industries. Sealants are used in healthcare applications such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of sealants to various substrates, mostly used for engines and car gaskets. China registered promising growth in these sectors, specifically in automotive, in recent times and is likely to continue in the upcoming years, which will augment the demand for sealants by 2028.

China Sealants Market Trends

Housing, hospitals, and healthcare facilities schemes by the Chinese government to lead the construction in the country

China has been majorly driven by the ample developments in the residential and commercial construction sectors and supported by the growing economy. China is promoting and undergoing a process of continuous urbanization, with a target rate of 70% for 2030. The increased living spaces required in the urban areas resulting from urbanization and the desire of middle-class urban residents to improve their living conditions may have a profound effect on the housing market and thereby increase the residential construction in the country.

Non-residential infrastructure is likely to expand significantly. The country's aging population necessitates the construction of additional healthcare facilities and hospitals. The Chinese government approved 26 infrastructure projects worth approximately USD 142 billion in 2019, with completion due in 2023. The country boasts the world's largest construction market, accounting for 20% of all worldwide construction investments.

In China, the housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units by 2030. The rising household income levels, combined with the population migrating from rural to urban areas, are expected to continue to drive the demand for the residential construction sector in the country. By 2030, the country is estimated to spend over USD 13 trillion on construction. Thus, the construction market is expected to register a 4.48% CAGR during the forecast period (2022-2028).

Owing to government policies, EVs demand in China is rising and is likely to propel the automotive production

China's automotive market for passenger vehicles is the largest in the world, as it accounted for 21.41 million units in 2021 compared to other major global players such as Japan, the United States, and Germany. This number is expected to grow at the same pace because of the increasing production capacity of automotive companies post-pandemic in China, as BYD, which is a local electric vehicle manufacturer in China, holds 8.84% of total electric vehicle production in the world.

China, being the epicenter of the COVID-19 pandemic, witnessed huge losses in the automotive industry in 2020 as it led to nationwide lockdowns, supply chain disruptions, lack of human resources availability, etc. This was the reason for the negative Y-o-Y growth rate in China in 2020.

The Chinese government's policies for electric vehicle owners, such as time-limited purchase subsidies, traffic regulations waivers, and charging rebates for EV owners, have encouraged the sale and demand for EVs in China. The sales of electric vehicles are expected to reach 7,526 thousand in 2027. EV production in China increased from 1 million units in 2019 to 3.5 million units in 2021, and it is expected to record a 15.07% CAGR in the forecast period (2022-2028).

Shanghai Automotive Industry Corporation is China's largest automotive company in terms of production. The growth in the number of both passenger and commercial vehicles manufactured by SAIC is significant, as it increased from nearly 2 million units in 2019 to 7 million units in 2021. This growth trend shows that the Chinese automotive market is expected to grow steadily during the forecast period.

China Sealants Industry Overview

The China Sealants Market is fragmented, with the top five companies occupying 20.34%. The major players in this market are 3M, Chengdu Guibao Science and Technology Co., Ltd., Guangzhou Baiyun Chemical Industry Co.,ltd., Guangzhou Jointas Chemical Co.,Ltd. and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.2 Regulatory Framework

4.2.1 China

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Healthcare

5.1.5 Other End-user Industries

5.2 Resin

5.2.1 Acrylic

5.2.2 Epoxy

5.2.3 Polyurethane

5.2.4 Silicone

5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 Chengdu Guibao Science and Technology Co., Ltd.

6.4.4 Dow

6.4.5 Guangzhou Baiyun Chemical Industry Co.,ltd.

6.4.6 Guangzhou Jointas Chemical Co.,Ltd.

6.4.7 H.B. Fuller Company

6.4.8 Hangzhou Zhijiang Advanced Material Co., ltd.

6.4.9 Henkel AG & Co. KGaA

6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)