ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

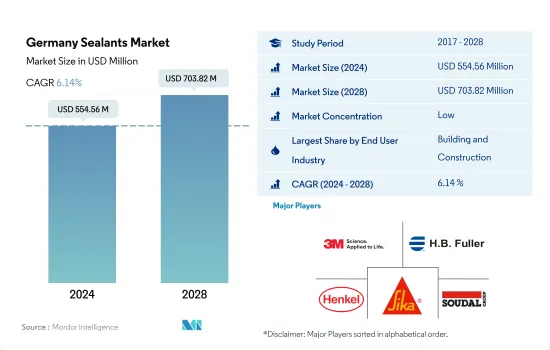

독일의 실란트 시장 규모는 2024년에 5억 5,456만 달러에 달했고, 2028년에는 7억 382만 달러에 이를 것으로 예측되며, 예측 기간 중(2024-2028년) CAGR은 6.14%를 나타낼 전망입니다.

독일의 EV 생산 확대로 실란트 사용 확대

독일의 실란트 시장은 방수, 내후성 실링, 균열 실링, 눈지름 실링 등 건축에 있어서의 실런트의 다양한 용도에 의해 건설 산업이 견인해, 다른 최종사용자 산업이 이어집니다. GDP의 5.9% 가까이를 차지하고 있어 향후 몇 년간의 실런트 수요를 끌어 올리는 요인이 되고 있습니다.

다양한 실란트가 전자기기나 전기기기의 제조에 있어서 포팅이나 재료 보호에 널리 사용되고 있습니다. 이것은 센서나 케이블 등의 씰에 사용됩니다. 세계 6위에서 수익 점유율은 2.6%(2021년)를 차지하고 있어 향후 수년간 성장할 가능성이 높습니다.

독일은 수십년동안 의료 산업과 자동차 산업에서 큰 발전을 이루었습니다. 2021년 프리미엄 자동차 생산 대수에서 독일은 시장 점유율의 약 23%를 차지하고 있습니다.

독일 실란트 시장 동향

디지털 파크나 병원 등의 인프라 정비를 위한 정부의 대처가 건설 산업을 뒷받침

건설업은 전체 공업 생산량의 11%를 차지합니다. 국가 지출 증가로부터 이익을 얻고 있습니다. 과거 5년간의 유럽 중앙은행의 초저 금리, 도시 인구 증가, 이민 증가가 건설업의 호황을 뒷받침해 왔습니다.

2021년 독일 건설시장은 전년대비 1.99%의 성장률을 기록했습니다. 건설 작업은 2021년 3분기에 시작되어 2028년 4분기에 완성될 예정입니다. 중앙 병원의 건설을 개시해, 2025년까지 완성될 예정입니다. 이 프로젝트는 정신 보건 센터와 주차장을 갖춘 의료 백화점의 건설을 목표로 하고 있습니다.

저금리, 실질가처분소득 증가, 유럽연합(EU)과 독일 정부에 의한 수많은 투자 등이 성장을 지지하는 것으로 예측됩니다.

자동차 제조업체에 대한 정부의 규제에도 불구하고 전기자동차 수요는 자동차 산업을 추진할 것으로 예측됩니다.

자동차 제조업은 독일에서 가장 중요한 산업이며, 국내 산업 수익의 24%는 이 산업에서 만들어지고 있습니다.

독일에서 생산되는 자동차 유닛의 75% 이상은 주로 미국, 중국 및 기타 EU 국가입니다. 2019년 미국과 중국 간의 무역 분쟁으로 인해 세계 수요가 위축되었습니다. 이는 자동차 제조사들이 새로 판매되는 차량의 평균 이산화탄소 배출량을 킬로미터당 95그램으로 달성하도록 의무화한 새로운 EU-28 이산화탄소 배출 기준과 맞물려, 해당 국가의 자동차 생산을 일시적으로 제한하는 결과를 초래했습니다.

2020년 COVID-19의 대유행은 이미 감소하고 있던 자동차 생산에 큰 타격을 주었습니다. 이 공급망 제약의 장기적인 영향으로 예측 기간 중 독일의 자동차 생산은 제한될 것으로 예측됩니다.

독일 실란트 산업 개요

독일 실란트 시장은 세분화되어 있으며 상위 5개 기업에서 37.69%를 차지하고 있습니다. 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Sika AG, Soudal Holding NV 등입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

규제 프레임워크

독일

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

의료

기타

수지

아크릴

에폭시

폴리우레탄

실리콘

기타

제6장 경쟁 구도

주요 전략적 움직임

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

Dow

EGO Dichtstoffwerke GmbH & Co. Betriebs KG

HB Fuller Company

Henkel AG & Co. KGaA

MAPEI SpA

Sika AG

Soudal Holding NV

Wacker Chemie AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

SHW

영문 목차

영문목차

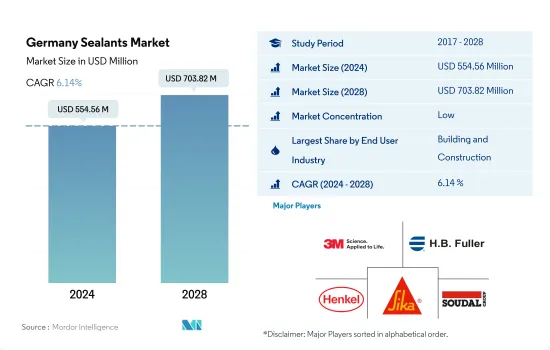

The Germany Sealants Market size is estimated at 554.56 million USD in 2024, and is expected to reach 703.82 million USD by 2028, growing at a CAGR of 6.14% during the forecast period (2024-2028).

Growing EV production in Germany to augment the use of sealants

The German sealants market is driven by the construction industry, followed by other end-user industries due to the diverse application of sealants in building construction, such as waterproofing, weather-sealing, cracks-sealing, and joint-sealing. The German construction industry obtained nearly 5.9% of the country's GDP, propelling the demand for sealants in the coming years. The increasing growth of residential construction projects due to the shortage in housing facilities and ongoing renovation works will augment the sealants demand in Germany during the forecast period.

A variety of sealants are widely used in electronics and electrical equipment manufacturing for potting and protecting materials. They are used for sealing sensors and cables, etc. The German electronics market is the sixth largest in the world, generating 2.6% (2021) of revenue share, which is likely to grow in the upcoming years. This, in terms, will foster the demand for sealants in the other end-user segment.

Germany has achieved significant development in the healthcare and automotive industries over the decades. Sealants are used in applications in healthcare, such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of sealants to various substrates, such as glass, metal, plastic, and painted surfaces. These are mostly used in engines and car gaskets. Germany has registered about 23% of the market share in terms of the production of premium cars in 2021. German automotive and OEMs focus on manufacturing electric vehicles to reduce carbon emissions and maintain vehicle weight to meet the industry standard. These factors will augment automotive and OEM production in the near future, which gradually influences demand.

Germany Sealants Market Trends

The government initiatives towards infrastructure including digital parks and hospitals to boost the construction industry

Construction accounts for 11% of total industrial production output. The construction industry in the country is growing at a slow pace, majorly driven by increasing new residential construction activities. German construction companies are benefiting from soaring demand for real estate, increased investments in buildings, and higher state spending on infrastructure. The upswing in construction has been encouraged by the European Central Bank's ultra-low interest rates, a growing urban population, and high immigration over the past five years. The sector is also helping to propel overall economic growth.

In 2021, the construction market in the country registered a 1.99% growth rate compared to the previous year. The German government has initiated the construction of the Digital Park Fechenheim on 10.7 hectares of area, with a gross floor area of 100,000 m2 in Frankfurt-Fechenheim, Hesse, Germany, with an investment of USD 1,179 million. The construction work started in Q3 2021 and is expected to be completed in Q4 2028. In the third quarter of 2021, the country started the construction of the Central Hospital in Lorrach, Baden-Wuerttemberg, with an investment of USD 418 million, and it is expected to be completed by 2025. The project aims to build a center for mental health and a medical department store with a parking garage.

The growth is likely to be supported by lower interest rates, increased real disposable incomes, and numerous investments by the European Union and the German government. Therefore, with the non-residential and commercial buildings in the country expected to witness significant growth prospects, the construction industry in the country is likely to increase during the forecast period.

Despite the government regulations on carmakers, electrical vehicles demand is likely to propel the automotive industry

The automotive manufacturing industry is the most important industry in Germany, and 24% of the domestic industry revenue is generated from this industry. Automotive production in Germany declined by 9.4% in the third quarter of 2018, as the country experienced an economic slowdown in the second half of 2018, coupled with the problems in the implementation of the new Worldwide Harmonized Light-Duty Vehicles Test Procedure (WLTP).

Over 75% of the automotive units manufactured in Germany are destined for international markets, which are mainly the United States, China, and other EU countries. The trade conflicts between the United States and China sapped away the global demand in 2019. This, coupled with the new EU-28 standard of CO2 emissions, which mandates carmakers to achieve average CO2 emissions of 95 grams per kilometer across newly-sold vehicles, has briefly restricted automotive production in the country.

In 2020, the COVID-19 pandemic hit hard on the already declining automotive production. In 2020, automotive production fell by 24.5% Y-o-Y, and the supply chain constraints that quickly followed, coupled with the semiconductor chip shortage in 2021, have further declined automotive production by 10.8% compared to 2020 levels. The long-lasting effects of chip shortages and supply chain restrictions are expected to restrict automotive production in Germany in the forecast period. The German government's e-mobility plan aims to achieve 15 million EVs on the road by 2030. This is expected to drive up automotive production in the country. Due to all these factors, Germany's automotive production is expected to increase during the forecast period.

Germany Sealants Industry Overview

The Germany Sealants Market is fragmented, with the top five companies occupying 37.69%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.2 Regulatory Framework

4.2.1 Germany

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Healthcare

5.1.5 Other End-user Industries

5.2 Resin

5.2.1 Acrylic

5.2.2 Epoxy

5.2.3 Polyurethane

5.2.4 Silicone

5.2.5 Other Resins

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 Dow

6.4.4 EGO Dichtstoffwerke GmbH & Co. Betriebs KG

6.4.5 H.B. Fuller Company

6.4.6 Henkel AG & Co. KGaA

6.4.7 MAPEI S.p.A.

6.4.8 Sika AG

6.4.9 Soudal Holding N.V.

6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)