ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

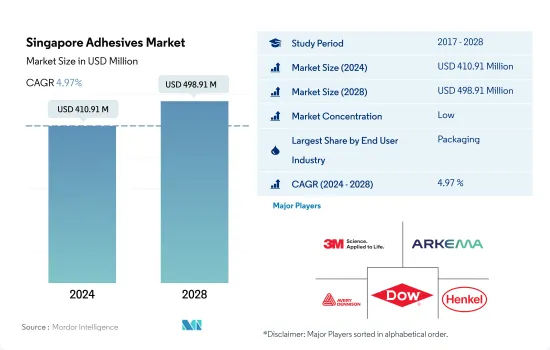

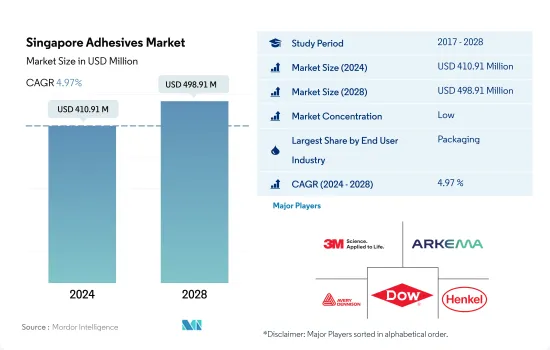

싱가포르의 접착제 시장 규모는 2024년 4억 1,091만 달러, 2028년에는 4억 9,891만 달러에 이르고, 예측 기간 중(2024-2028년) CAGR 4.97%로 성장할 것으로 예측됩니다.

접착제 시장 전체의 성장에 큰 영향을 미치는 싱가포르의 건강 관리 산업의 주요 성장률

싱가포르의 건강 관리, 패키징 및 전자 산업에 걸친 강력한 제조 능력과 접착제는 접착 및 조립 응용 분야에서 성장 기회를 찾습니다. 2020년 접착제 수요는 COVID-19 팬데믹에 의한 무역과 공급망의 한계에 따라 감소하여 2019년에 비해 7.5% 이상 감소했습니다.

접착제는 플라스틱, 금속, 종이 및 골판지 포장 용도의 접착에 대한 중요성으로 인해 국내 포장 산업에서 주로 소비되고 있습니다. 수성 접착제는 이러한 용도에 필요한 저렴한 비용과 높은 접착 강도로 인해 업계에서 매우 소비되고 있습니다. 2021년에는 국내 포장업계에서 약 3만 2,000톤의 수성 접착제가 소비된 것으로 보입니다. 핫멜트 접착제는 포장 산업에서 가장 급성장하고 있는 기술이며, 2022-2028년의 CAGR은 5.58%입니다. 지속가능한 식품 포장은 소비되는 식품의 안전성을 보장하는 동시에 식품 폐기물을 줄이고, 따라서 접착제 수요가 업계에서 증가하는 것을 도울 수 있습니다. 이러한 요인은 식품 분야의 포장 수요를 매우 동기 부여합니다.

싱가포르의 접착제는 주로 건강 관리 산업 전반에 걸쳐 소비됩니다. 싱가포르의 건강 관리 시스템은 최첨단 치료를 제공하고 세계에서 가장 위대한 것 중 하나로 간주됩니다. 이는 단단한 규제 감독, 상업 부문 및 공공 부문 모두를 포함한 비용 부담 구조, 의료 저축 계좌로부터의 지불로 인한 것입니다.

싱가포르 접착제 시장 동향

포장용 플라스틱에 재활용 가능한 플라스틱을 사용하여 산업 성장에 새로운 기회를 제공

포장은 주로 보호, 봉쇄, 정보 제공, 실용성, 판촉에 사용됩니다. 성장하는 싱가포르 포장 시장 부문은 예측 기간 동안 CAGR 3.77%를 나타낼 것으로 예상됩니다. 2017년 종이, 판지 및 플라스틱 포장을 포함한 포장 사용량은 3,340만 톤을 차지했습니다. 2020년에는 COVID-19의 발생으로 공급망의 혼란, 포장재의 부족, 상품의 수출입 제한, 공장의 저능력 조업으로 시장은 -5.54%의 마이너스 성장을 기록했습니다.

2021년 시장은 4.40%의 성장을 기록했으며 3,560만 톤의 포장재료가 다양한 목적으로 사용됩니다. 전자상거래 부문이 증가하고 제품 출하에 특수 포장이 필요하기 때문에 포장 업계를 크게 뒷받침하고 있기 때문에 포장 업계는 앞으로도 계속 성장할 것으로 예상됩니다. 2021년 싱가포르 전자상거래 시장은 59억 달러로 평가되었으며 2026년에는 100억 달러로 상승할 것으로 예상됩니다. 경쟁이 치열한 오늘날의 FMCG 시장에서 기업이 경쟁사를 차지하고 시장에서 브랜드를 유지하기 위해서는 매력적인 포장을 사용하고 포장에 혁신을 가져오는 것이 불가피해지고 있습니다.

싱가포르 정부는 제품에 재활용 가능한 플라스틱을 포함하는 규제를 실시했습니다.

공공 건축물 건설에 대한 지속적이고 미래의 투자는 최종 사용자 산업을 지원합니다.

싱가포르의 건설 업계는 2022-2028년 예측기간 중 약 2.6%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 건설 수요는 2019년, 5년만에 최고 수준에 달해 추정 334억 SGD 상당의 프로젝트가 수주되어 상기 예측의 320억 SGD를 상회했습니다. 2020년에는 COVID-19 팬데믹의 영향으로 프로젝트 실시 스케줄이 혼란해 건설 수요의 속보치는 36.5% 감소한 213억 SGD가 되었습니다. 싱가포르의 건설용 접착제 및 실란트 시장은 2022-2028년의 예측기간 중에 수량으로 약 2.86%, 금액으로 약 5.31%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 예측되고 있습니다.

공공 부문 건설은 2019년 190억 SGD에서 2020년 132억 SGD로 감소했지만, 이는 유통관리가 자원 관리 및 프로젝트 스케줄링에 미치는 영향을 검토하는 데 시간이 필요했기 때문에 특정 대형 인프라 프로제 또한 싱가포르의 건설 수요는 2022년에는 270억-320억 달러에 달할 것으로 추정되며, 공공 부문이 수요 전체의 약 60%를 차지할 것으로 보입니다.

한편, 싱가포르의 주택건설은 남아있는 건물의 재고가 증가함에 따라 여전히 저조하고, COVID-19의 유행에 의한 경기후퇴에 의해 더욱 악화되고 있습니다. 정부는 2020년 말까지 약 6만명의 이주 노동자용으로 주택을 추가 건설할 계획을 세우고 있었습니다.

싱가포르 접착제 산업 개요

싱가포르의 접착제 시장은 세분화되어 있으며 주요 5개사에서 19.36%를 차지하고 있습니다. 시장 주요 기업에는 3M, Arkema Group, AVERY DENNISON CORPORATION, Dow, Henkel AG & Co. KGaA(알파벳순)가 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

신발 및 가죽

포장

목공 및 건구

규제 프레임워크

싱가포르

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

신발 및 가죽

헬스케어

포장

목공 및 건구

기타 최종 사용자 산업

기술

핫멜트

반응성

용제계

UV 경화형 접착제

수계

수지

아크릴계

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE 및 EVA

기타 수지

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

ALTECO co., ltd.

Arkema Group

AVERY DENNISON CORPORATION

Dow

Dymax

HB Fuller Company

Henkel AG & Co. KGaA

Huntsman International LLC

Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업의 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Singapore Adhesives Market size is estimated at 410.91 million USD in 2024, and is expected to reach 498.91 million USD by 2028, growing at a CAGR of 4.97% during the forecast period (2024-2028).

The major growth rates poised for the Healthcare industry of Singapore to have a considerable influence on the overall growth of adhesives market

Singapore's strong manufacturing capacities across healthcare, packaging, and electronic industries and adhesives have found a growth opportunity in terms of bonding and assembling applications. The demand for adhesives declined in 2020 due to trade and supply chain restrictions because of the COVID-19 pandemic, which resulted in a decline of above 7.5% in comparison to that of 2019.

Adhesives are majorly consumed in the packaging industry in the country owing to their importance in bonding plastics, metals, and paper and cardboard packaging applications. Waterborne adhesives are highly consumed in the industry because of their cheaper cost and high bonding strength, which is required in these applications. It is seen that nearly 32 thousand tons of water-borne adhesives were consumed in the packaging industry of the country in 2021. Hot-melt adhesives are the fastest-growing technology in the packaging industry, with a CAGR of 5.58% during the period 2022-2028. Sustainable food packaging may assist ensure the safety of the food consumed while also reducing food waste and thus helping the adhesives demand to increase in the industry. These factors have highly motivated the demand for packaging in the food sector.

Singapore's adhesives are also largely being consumed across the healthcare industry. Singapore's healthcare system is regarded as one of the greatest in the world, offering some of the most cutting-edge medical treatments. This is due to robust regulatory oversight, a cost-sharing structure that includes both the commercial and public sectors and payments from medical savings accounts.

Singapore Adhesives Market Trends

Usage of recyclable plastics for packaging production will open new opportunities to the industry growth

Packaging is mainly used for protection, containment, information, utility, and promotion. The growing Singaporean packaging market segment is expected to register a CAGR of 3.77% during the forecast period. In 2017, packaging usage accounted for 33.4 million ton of packaging, including paper, paperboard, and plastic packaging. Due to the COVID-19 outbreak in 2020, the market registered a negative growth of -5.54% due to disruptions in the supply chain, shortage of packaging material, restrictions on the import and export of goods, and factories operating at low capacity.

In 2021, the market registered a positive growth of 4.40%, with 35.6 million ton of packaging material used for various purposes. The packaging industry is expected to keep growing as there has been a rise in the e-commerce sector, which has significantly boosted the packaging industry as special packaging is required for shipping goods. In 2021, the Singaporean e-commerce market was valued at USD 5.9 billion, and it is expected to rise to USD 10 billion by 2026. In today's competitive FMCG market, it has become inevitable for companies to use attractive packaging and bring innovation to their packaging to stand out from their competitors and maintain their brand in the market.

The Singaporean government has implemented regulations to include recyclable plastics in products. Packaging production is majorly driven by plastic in the country, which nearly accounts for around 64% of the packaging produced in 2021. With the advancement of plastic recyclability, the plastic segment is likely to maintain its growth and record a CAGR of around 4.75% during the forecast period.

Ongoing and upcoming investments in the construction of public buildings will support the end-user industry

The Singaporean construction industry is projected to record a CAGR of about 2.6% during the forecast period from 2022 to 2028. The construction demand hit a five-year high in 2019, with an estimated SGD 33.4 billion worth of projects awarded, higher than its top-end projection of SGD 32 billion. This represented a 9.5% increase in construction demand compared to 2018. However, in 2020, due to the impact of the COVID-19 pandemic, which disrupted project implementation schedules, the preliminary figure for construction demand witnessed a decline of 36.5% to SGD 21.3 billion. The Singaporean construction adhesives and sealants market is projected to record a CAGR of about 2.86% in volume and 5.31% in value during the forecast period 2022-2028.

Public sector construction declined from SGD 19 billion in 2019 to SGD 13.2 billion in 2020, as certain large infrastructure projects were postponed due to the need for more time to examine the pandemic's impact on resource management and project scheduling. Moreover, construction demand in Singapore is estimated to be between USD 27 billion and USD 32 billion in 2022, and the public sector is likely to provide roughly 60% of the overall demand. The public sector's construction demand is expected to range between USD 16 billion and USD 19 billion.

On the other hand, residential construction in Singapore remains weak due to the growing stock of unsold buildings, further aggravated by the economic downturn due to the COVID-19 pandemic. However, to reduce the population density in dormitories amid the pandemic, the government had planned to construct additional housing for around 60,000 migrant workers by the end of 2020. These factors are expected to restrain the demand for adhesives and sealants over the forecast period.

Singapore Adhesives Industry Overview

The Singapore Adhesives Market is fragmented, with the top five companies occupying 19.36%. The major players in this market are 3M, Arkema Group, AVERY DENNISON CORPORATION, Dow and Henkel AG & Co. KGaA (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.1.4 Footwear and Leather

4.1.5 Packaging

4.1.6 Woodworking and Joinery

4.2 Regulatory Framework

4.2.1 Singapore

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Footwear and Leather

5.1.5 Healthcare

5.1.6 Packaging

5.1.7 Woodworking and Joinery

5.1.8 Other End-user Industries

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Solvent-borne

5.2.4 UV Cured Adhesives

5.2.5 Water-borne

5.3 Resin

5.3.1 Acrylic

5.3.2 Cyanoacrylate

5.3.3 Epoxy

5.3.4 Polyurethane

5.3.5 Silicone

5.3.6 VAE/EVA

5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 ALTECO co., ltd.

6.4.3 Arkema Group

6.4.4 AVERY DENNISON CORPORATION

6.4.5 Dow

6.4.6 Dymax

6.4.7 H.B. Fuller Company

6.4.8 Henkel AG & Co. KGaA

6.4.9 Huntsman International LLC

6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)