인도네시아의 접착제 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Indonesia Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693383

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

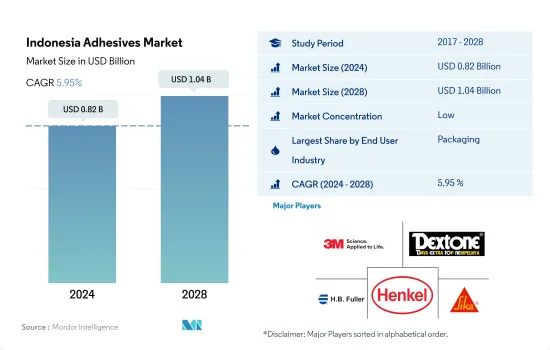

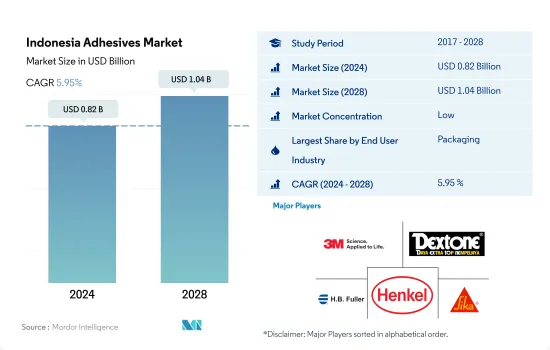

인도네시아의 접착제 시장 규모는 2024년에 8억 2,000만 달러로 추정되고, 2028년에는 10억 4,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2028년)의 CAGR은 5.95%를 나타낼 것으로 전망됩니다.

인도네시아에서 진행 중이거나 계획 중인 수많은 인프라 프로젝트가 접착제 수요 증가에 중요한 역할을 할 것

인도네시아의 접착제 소비량은 코로나19의 영향으로 2020년에 감소 추세를 보였습니다. 같은 해 소비량은 2019년에 비해 수량 기준으로 약 13% 감소했습니다. 인도네시아의 봉쇄 조치가 접착제 부족의 주요 원인으로 지목되고 있습니다. 또한 생산 시설의 가동 중단과 공급망 중단으로 인해 접착제 수요도 큰 영향을 받고 있습니다.

인도네시아 포장 산업은 모든 산업과 비즈니스에서 중요한 역할을 합니다. 따라서 포장 산업의 발전은 국가 산업의 발전과 분리될 수 없습니다. 실제로 포장은 국가 산업 제품의 경쟁력을 결정하는 요소 중 하나가 되었습니다. 최근 몇 년 동안 포장 부문은 전년 대비 6-7% 성장하여 2021년에는 104조 7,280억 IDR에 달할 전망입니다. 실제로 COVID-19 전염병이 확산되기 시작하면서 포장 사업은 큰 타격을 입지 않았습니다.

다른 한편으로, 업계에서는 인도네시아의 성장을 가속화하기 위해 대규모 인프라 프로젝트에 투자하고 있습니다. 예를 들어, 인도네시아는 자카르타의 지하철 네트워크를 확장하기 위해 400억 달러 이상을 투자할 계획이며, 이는 인도네시아의 건설 산업을 강화할 것으로 예상됩니다. 또한 인도네시아는 향후 25개의 공항과 신규 발전소 건설을 포함하여 4,000억 달러 이상의 야심찬 건설 프로젝트를 계획하고 있습니다. 이러한 모든 변수가 접착제 수요에 영향을 미칩니다.

인도네시아의 접착제 시장 동향

종이 및 판지 포장 활성화를 위한 정부 전략은 산업 규모를 확대

포장은 주로 보호, 밀봉, 정보, 사용의 유용성 및 홍보를 위해 사용됩니다. 따라서 포장은 대부분의 산업에서 필수적인 부분입니다. 성장하는 인도네시아 시장은 예측 기간 동안 포장재 사용량을 늘리고 4.33%의 연평균 성장률을 기록할 것으로 예상됩니다. 2017년 포장재 사용량은 종이와 판지, 플라스틱을 포함해 1억 4,346만 톤을 차지했습니다.

2021년 포장재 시장은 4.28%의 플러스 성장을 기록했으며, 다양한 용도로 1억 5,341만 톤의 포장재가 사용되었습니다.

인도네시아는 중국에 이어 두 번째로 많은 플라스틱 쓰레기를 해양에 배출하는 국가로, 인도네시아 정부는 플라스틱 사용에 대한 조치를 취하고 있습니다. 인도네시아 정부가 시행하는 생산자책임재활용제도(EPR) 규정에 따라 생산자와 소매업체는 재활용 가능한 재료의 비율을 높이도록 제품 포장을 재설계할 의무가 있습니다.

경쟁이 치열한 오늘날의 소비재 시장에서 기업이 경쟁사보다 돋보이고 시장에서 브랜드 가치를 유지하기 위해 매력적인 포장을 사용하는 것은 불가피한 일이 되었습니다.

자동차 부품 및 구성 요소의 수출 가치가 크게 증가함에 따라 산업 성장이 확산

인도네시아의 자동차 산업은 여전히 인도네시아의 경제 발전에 크게 기여하는 유망한 분야입니다. 인도네시아 산업부 장관 아구스 구미왕 카르타사스미타에 따르면, 인도네시아의 자동차 산업은 2021년에 17.82%의 두 자릿수 성장률을 기록하며 엄청난 성장세를 보였습니다. 2020년에는 69만 176대로 급감하여 코로나19 팬데믹으로 인해 약 46% 감소했습니다.

인도네시아의 자동차 부문 무역은 2019년부터 2021년까지 모든 해에 흑자를 기록했습니다. 2020년에는 전 세계적인 팬데믹으로 인해 경제 활동에 제한과 차질이 발생하여 글로벌 공급망에 지장을 초래하고 총 생산에 타격을 주면서 수출과 수입이 모두 감소했습니다. 그러나 2021년에는 견조한 생산량에 힘입어 수출과 수입 모두 크게 증가하여 무역수지는 19억 3,000만 달러의 흑자를 기록했습니다.

인도네시아의 접착제 산업 개요

인도네시아의 접착제 시장은 세분화되어 있으며 상위 5개 기업에서 15.91%를 차지하고 있습니다. 이 시장의 주요 업체는 3M, DEXTONE INDONESIA, H.B. Fuller Company, Henkel AG & Co. KGaA, Sika AG(알파벳 순으로 정렬)입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

신발 및 가죽

포장

목공 및 목공예

규제 프레임워크

인도네시아

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

신발 및 가죽

의료

포장

목공 및 목공예

기타

기술

핫멜트

반응성

용매

UV 경화형 접착제

수성

수지

아크릴계

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE 및 EVA

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

ALTECO co., ltd.

DEXTONE INDONESIA

HB Fuller Company

Henkel AG & Co. KGaA

Huntsman International LLC

MAPEI SpA

Pidilite Industries Ltd.

PT. Pamolite Adhesive Industry

Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The Indonesia Adhesives Market size is estimated at 0.82 billion USD in 2024, and is expected to reach 1.04 billion USD by 2028, growing at a CAGR of 5.95% during the forecast period (2024-2028).

The numerous ongoing and planned infrastructure projects in the country to have a key role in the growth of adhesive demand

The consumption of adhesives in Indonesia has shown a downward trend in 2020 due to the impact of COVID-19. The consumption was reduced by about 13% in terms of volume in the same year compared to 2019. The lockdown in the country has largely become the major reason for the shortage of adhesives in the country. Moreover, due to the shutdown of production facilities and supply chain disruption, the demand for these adhesives is largely being impacted.

The Indonesian packaging industry plays an important role in all industries and businesses. Therefore, the development of the packaging industry cannot be separated from the development of the national industry. In fact, packaging has become one of the determining factors for the competitiveness of national industrial products. In recent years, the packaging sector has grown by 6%-7% year-on-year, with a realized value of IDR 104,728 billion in 2021. In reality, as the COVID-19 epidemic began to spread, the packing business did not suffer considerably. The packaging industry is expected to increase at a 6%-8% annual rate, in conjunction with the growth of the major supporting sectors, such as food and beverage (Mamin), pharmaceutical, and retail.

On the other side, the industry is now investing in massive infrastructure projects to accelerate the country's growth. For example, Indonesia is planning to invest over USD 40 billion to expand Jakarta's metro network, which is expected to strengthen the country's construction industry. Indonesia is also planning ambitious construction projects worth more than USD 400 billion in the future years, including the construction of 25 airports and new power plants. All of these variables influence the demand for adhesives.

Indonesia Adhesives Market Trends

The government initiatives to promote paper and paperboard packaging will escalate the industry size

The packaging is mainly used for protection, containment, information, utility of use, and promotion. This makes packaging an integral part of most industries. The growing Indonesian market is expected to boost packaging usage and register a CAGR of 4.33% during the forecast period. In 2017, packaging usage accounted for 143.46 million tons of packaging, including paper and paperboard and plastic. Due to COVID-19, in 2020, the market registered a negative growth of -5.77%, and this was due to disruption in the supply chain, shortage of packaging material, restrictions on the import and export of goods, and factories operating at low capacity.

In 2021, the market registered a positive growth of 4.28%, with 153.41 million tons of packaging material used for various purposes. It is expected that the packaging industry will keep growing as there has been a rise in the e-commerce sector which has given a significant boost to the packaging industry in the past few years as special packaging is required for shipping goods.

The government of Indonesia has taken steps toward the use of plastic, as Indonesia is the second-largest contributor of plastic waste in the ocean after China. The extended producer responsibility (EPR) regulation imposed by the Indonesian government will oblige producers and retailers to redesign their product packaging to have a higher proportion of recyclable material. This will encourage manufacturers to use paper and paperboard as the base material for the packaging, which will increase the volume of adhesives used in the packaging process.

In today's competitive market of consumer products, it has become inevitable for companies to use attractive packaging to stand out from their competitors and maintain their brand value in the market.

Considerable growth of export values for automotive parts & components will proliferate the industry growth

The automotive industry in Indonesia remains a promising sector that contributes significantly to the country's economic progress. According to Agus Gumiwang Kartasasmita, Minister of Sector Republic of Indonesia, the automobile industry in Indonesia witnessed tremendous growth in 2021, with a double-digit growth rate of 17.82%. In 2019, the country produced about 12,86,848 units of vehicles which drastically reduced to 6,90,176 units in 2020, accounting for a decline of about 46% owing to the COVID-19 pandemic. Due to this reason, the variation in automotive production between 2019 and 2021 resulted in about -13%, whereas between 2020 and 2021, the variation was about 63%.

The trade in the automotive sector in Indonesia showed a surplus in all years from 2019 to 2021. Both exports and imports fell in 2020 as a result of the global pandemic, which generated limitations and disruptions in economic activities, so impeding the global supply chain and hurting total production. However, in line with the robust output in 2021, both export and import values increased significantly, with a trade balance of USD 1.93 billion. Although 2021 had the highest level of commercial activity in the prior ten years, the trade balance surplus was the lowest in comparison to 2019 and 2020, which had balance values of USD 2 billion and USD 1.95 billion, respectively.

Globally, the development of EVs signaled a fundamental shift in the Indonesian transportation sector's policies. Given the country's nickel reserves, Indonesia is well-placed to become a major player in the global EV supply chain. To be a part of the region's EV future, Indonesia needs to invest in technology, talent resources, renewable energy, and infrastructure.

Indonesia Adhesives Industry Overview

The Indonesia Adhesives Market is fragmented, with the top five companies occupying 15.91%. The major players in this market are 3M, DEXTONE INDONESIA, H.B. Fuller Company, Henkel AG & Co. KGaA and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.1.4 Footwear and Leather

4.1.5 Packaging

4.1.6 Woodworking and Joinery

4.2 Regulatory Framework

4.2.1 Indonesia

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Footwear and Leather

5.1.5 Healthcare

5.1.6 Packaging

5.1.7 Woodworking and Joinery

5.1.8 Other End-user Industries

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Solvent-borne

5.2.4 UV Cured Adhesives

5.2.5 Water-borne

5.3 Resin

5.3.1 Acrylic

5.3.2 Cyanoacrylate

5.3.3 Epoxy

5.3.4 Polyurethane

5.3.5 Silicone

5.3.6 VAE/EVA

5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 ALTECO co., ltd.

6.4.3 DEXTONE INDONESIA

6.4.4 H.B. Fuller Company

6.4.5 Henkel AG & Co. KGaA

6.4.6 Huntsman International LLC

6.4.7 MAPEI S.p.A.

6.4.8 Pidilite Industries Ltd.

6.4.9 PT. Pamolite Adhesive Industry

6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)