ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

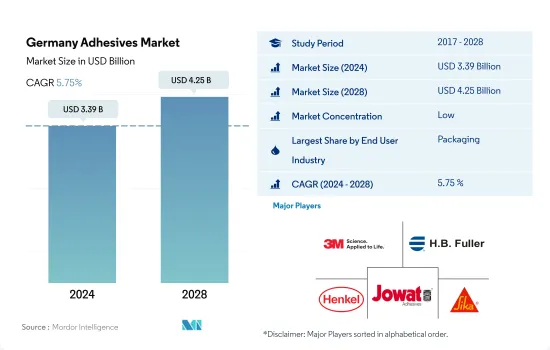

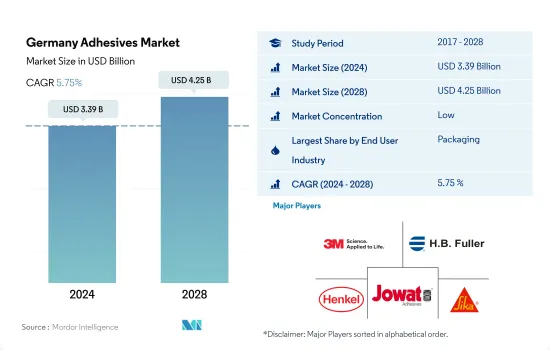

독일의 접착제 시장 규모는 2024년에 33억 9,000만 달러로 추정되고, 2028년에는 42억 5,000만 달러에 이를 것으로 예측되며, 예측 기간중(2024-2028년)에 CAGR 5.75%로 성장할 것으로 예측됩니다.

건설 및 리노베이션 활동 증가로 접착제 수요 증가

접착제는 플라스틱, 금속, 종이 및 판지 포장재를 접착하는 데 중요하기 때문에 국내 포장 산업에서 주로 소비됩니다.

독일의 접착제 시장은 지붕, 배관, 바닥재 등 다양한 용도로 인해 주로 건설 산업이 주도하고 있습니다. 독일의 건설 산업은 국내총생산(GDP)의 5.9%를 차지하며 향후 몇 년간 접착제 수요를 견인할 것입니다.

독일은 수십 년 동안 의료 및 자동차 산업에서 상당한 발전을 이루었습니다. 접착제는 의료 기기 부품 조립 및 밀봉과 같은 의료 분야의 응용 분야에 사용됩니다. 자동차 산업은 유리, 금속, 플라스틱 및 도장 표면과 같은 다양한 기질에 접착제를 적용하는 데 상당한 가능성을 보여줍니다. 독일은 2021년 프리미엄 자동차 생산량 기준으로 약 23%의 시장 점유율을 기록했습니다.

독일의 접착제 시장 동향

플라스틱 재활용성 향상과 식음료 산업의 수요 증가로 포장 산업을 주도하는 플라스틱 포장재

COVID-19 팬데믹으로 인해 전국적인 봉쇄와 제조 시설의 일시적인 폐쇄로 인해 공급망 차질과 수출입 무역 등 여러 가지 문제가 발생했습니다.

독일은 유럽에서 가장 큰 전자상거래 시장 중 하나이며 유럽에서 두 번째로 많은 인구를 보유하고 있어 포장재 생산 시장을 견인할 것입니다. 독일은 유럽 평균에 비해 온라인 쇼핑객 수, 인터넷 사용 인구 비율, 연평균 지출액이 높습니다.

포장재 생산은 주로 플라스틱이 주도하고 있으며, 2021년에 생산된 포장재의 약 79%를 플라스틱이 차지했습니다. 플라스틱 포장 산업은 주로 식음료 산업의 급속한 성장에 의해 주도되고 있습니다. 또한 플라스틱 재활용성이 발전함에 따라 플라스틱 생산 부문은 예상 기간 동안 약 3.32%의 가장 빠른 성장률을 기록 할 것으로 예상됩니다.

자동차 제조업체에 대한 정부 규제에도 불구하고 전기자동차 수요는 자동차 산업을 견인할 것

자동차 제조 산업은 독일에서 가장 중요한 산업으로, 국내 산업 수익의 24%가 이 산업에서 창출됩니다.

독일에서 생산되는 자동차의 75% 이상이 주로 미국, 중국, 기타 EU 국가 등 해외 시장으로 향하고 있습니다. 2019년에는 미국과 중국 간의 무역 갈등으로 인해 글로벌 수요가 감소했습니다. 이는 자동차 제조업체가 새로 판매되는 차량의 평균 CO2 배출량을 1km당 95g으로 제한하는 새로운 EU-28 CO2 배출량 기준과 맞물려 독일 내 자동차 생산에 잠시 제동이 걸렸습니다.

2020년 COVID-19 팬데믹이 이미 감소세를 보이던 자동차 생산에 큰 타격을 주었습니다. 2020년 자동차 생산량은 전년 대비 24.5% 감소했으며, 곧바로 이어진 공급망 제약과 2021년 반도체 칩 부족으로 인해 자동차 생산량은 2020년 수준 대비 10.8% 더 감소했습니다. 칩 부족과 공급망 제한의 장기적인 영향으로 인해 예측 기간 동안 독일의 자동차 생산이 제한될 것으로 예상됩니다.

독일의 접착제 산업 개요

독일의 접착제 시장은 세분화되어 있으며 상위 5개 기업이 37.88%를 점유하고 있습니다. 이 시장의 주요 업체는 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Jowat SE, Sika AG(알파벳 순으로 정렬)입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

신발 및 가죽

포장

목공 및 목공예

규제 프레임워크

독일

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

신발 및 가죽

의료

포장

목공 및 목공예

기타

기술

핫멜트

반응성

용매

UV 경화형 접착제

수성

수지

아크릴계

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE 및 EVA

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

AVERY DENNISON CORPORATION

DELO Industrie Klebstoffe GmbH & Co. KGaA

Dow

HB Fuller Company

Henkel AG & Co. KGaA

Jowat SE

KLEBCHEMIE MG Becker GmbH & Co. KG

Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The Germany Adhesives Market size is estimated at 3.39 billion USD in 2024, and is expected to reach 4.25 billion USD by 2028, growing at a CAGR of 5.75% during the forecast period (2024-2028).

Growing construction and renovation activities to boost the demand for adhesives

Adhesives are majorly consumed in the packaging industry in the country owing to their importance in bonding plastics, metals, and paper & cardboard packaging applications. Waterborne adhesives are highly consumed in the industry because of their cheaper cost and high bonding strength which is required in these applications. It is seen that nearly 161 thousand tons of water-borne adhesives are consumed in the packaging industry of the country during 2021.

The German adhesives market is majorly driven by the construction industry due to diverse applications, such as roofing, plumbing, and flooring. The construction industry of Germany obtained nearly 5.9% of the country's GDP, which will propel the adhesives demand in the coming years. The increasing growth of residential construction projects due to the shortage in housing facilities and ongoing renovating works will augment the adhesives demand in Germany during the forecast period.

Germany has achieved significant development in the healthcare and automotive industries over the decades. Adhesives are used in applications in healthcare, such as assembling and sealing medical device parts. The automotive industry exhibits significant applicability of adhesives to various substrates, such as glass, metal, plastic, and painted surfaces. Germany has registered about 23% of the market share in terms of the production of premium cars in 2021. German automotive and OEMs focus on manufacturing electric vehicles to reduce carbon emissions and maintain vehicle weight to meet the industry standard. These factors will augment automotive and OEM production in the near future, which gradually influences the demand for automotive adhesives.

Germany Adhesives Market Trends

With the advancement in plastic recyclability and demand for food and beverage industry, plastic packaging to lead the packaging industry

With the rise in busier lifestyles, greater spending power, and related factors in the country, the demand for quick and on-the-go packaged products is increasing.Due to the COVID-19 pandemic, the country-wide lockdowns and temporary shutdown of manufacturing facilities caused several issues, including supply chain disruptions and imports and exports trade. As a result, the country's packaging production declined by 5% in 2020 compared to the previous year, significantly affecting the market.

Germany is one of the biggest e-commerce markets in Europe and has the second largest population in Europe, which will drive the packaging production market. Compared to Europe's average, Germany has a high number of online shoppers, the percentage of people using the internet, and the average annual spending. Total sales of goods sold online reached around EUR 99.1 billion in 2021, an increase compared to EUR 83.3 billion in 2020.

Packaging production is majorly driven by plastics in the country, which nearly accounts for around 79% of the packaging produced in 2021. The plastic packaging industry is majorly driven by the rapid growth of the food and beverages industry in the country. In addition, with the advancement of plastic recyclability, the plastic production segment is likely to register the fastest growth rate of around 3.32% CAGR during the projected period. Therefore, all the above-mentioned factors will further thrive the packaging demand in the coming years in the country.

Despite the government regulations on carmakers, electrical vehicles demand is likely to propel the automotive industry

The automotive manufacturing industry is the most important industry in Germany, and 24% of the domestic industry revenue is generated from this industry. Automotive production in Germany declined by 9.4% in the third quarter of 2018, as the country experienced an economic slowdown in the second half of 2018, coupled with the problems in the implementation of the new Worldwide Harmonized Light-Duty Vehicles Test Procedure (WLTP).

Over 75% of the automotive units manufactured in Germany are destined for international markets, which are mainly the United States, China, and other EU countries. The trade conflicts between the United States and China sapped away the global demand in 2019. This, coupled with the new EU-28 standard of CO2 emissions, which mandates carmakers to achieve average CO2 emissions of 95 grams per kilometer across newly-sold vehicles, has briefly restricted automotive production in the country.

In 2020, the COVID-19 pandemic hit hard on the already declining automotive production. In 2020, automotive production fell by 24.5% Y-o-Y, and the supply chain constraints that quickly followed, coupled with the semiconductor chip shortage in 2021, have further declined automotive production by 10.8% compared to 2020 levels. The long-lasting effects of chip shortages and supply chain restrictions are expected to restrict automotive production in Germany in the forecast period. The German government's e-mobility plan aims to achieve 15 million EVs on the road by 2030. This is expected to drive up automotive production in the country. Due to all these factors, Germany's automotive production is expected to increase during the forecast period.

Germany Adhesives Industry Overview

The Germany Adhesives Market is fragmented, with the top five companies occupying 37.88%. The major players in this market are 3M, H.B. Fuller Company, Henkel AG & Co. KGaA, Jowat SE and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.1.4 Footwear and Leather

4.1.5 Packaging

4.1.6 Woodworking and Joinery

4.2 Regulatory Framework

4.2.1 Germany

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Footwear and Leather

5.1.5 Healthcare

5.1.6 Packaging

5.1.7 Woodworking and Joinery

5.1.8 Other End-user Industries

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Solvent-borne

5.2.4 UV Cured Adhesives

5.2.5 Water-borne

5.3 Resin

5.3.1 Acrylic

5.3.2 Cyanoacrylate

5.3.3 Epoxy

5.3.4 Polyurethane

5.3.5 Silicone

5.3.6 VAE/EVA

5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 AVERY DENNISON CORPORATION

6.4.4 DELO Industrie Klebstoffe GmbH & Co. KGaA

6.4.5 Dow

6.4.6 H.B. Fuller Company

6.4.7 Henkel AG & Co. KGaA

6.4.8 Jowat SE

6.4.9 KLEBCHEMIE M. G. Becker GmbH & Co. KG

6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)