일본의 접착제 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Japan Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1693372

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

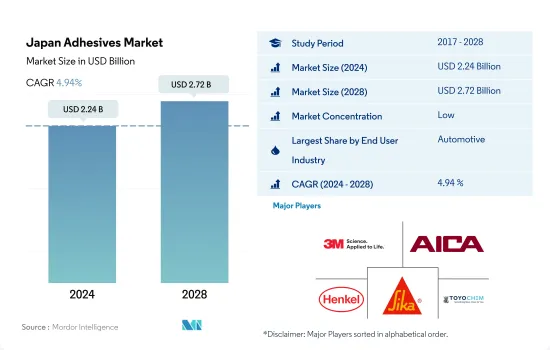

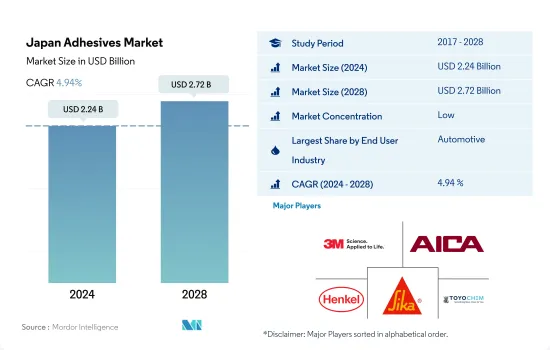

일본의 접착제 시장 규모는 2024년에 22억 4,000만 달러로 추정되고, 2028년에는 27억 2,000만 달러에 이를 것으로 예측되며, 예측 기간중(2024-2028년)에 CAGR 4.94%로 성장할 것으로 예측됩니다.

신흥 자동차 시장과 건축 및 건설 산업이 일본 내 접착제 소비를 촉진할 것으로 예측됩니다.

일본에서 접착제는 포장, 자동차, 건축 및 건설, 의료 산업 전반에 걸쳐 주로 사용됩니다. 2020년 일본의 접착제 소비는 코로나19 팬데믹의 영향으로 감소했습니다. 2019년 대비 2020년의 수요는 수량 기준으로 11% 감소했습니다.

일본의 자동차 산업은 22개 현에 78개 제조업체가 550만 명 이상을 고용하고 있는 세계 3위의 규모입니다. 일본 국내 및 전 세계 시장에서 전기 및 하이브리드 자동차의 생산이 증가하고 전 세계적으로 수요와 공급이 증가하는 등 고도로 혁신적이고 기술 지향적인 비즈니스입니다.

일본의 건설 산업에 대한 전망은 그 어느 때보다 좋습니다.

일본의 접착제 시장 동향

플라스틱 재활용성 향상과 식음료 산업의 수요 증가로 포장 산업을 주도하는 플라스틱 포장재

일본의 포장 산업은 제품의 안전성과 수명을 보호하고 향상시키려는 경향이 증가함에 따라 최근 상당한 성장을 기록했으며 일본 GDP에 1.13%를 기여했습니다. 식음료 부문은 복잡하고 진화하는 특성으로 인해 일본 포장 산업에서 큰 비중을 차지하고 있습니다. 일본 정부는 2025년까지 식품 자급률 45%를 달성한다는 목표를 세웠으며, 이는 향후 몇 년간 포장 산업에 기여할 것으로 보입니다. 또한 고령화로 인해 노인 소비자들이 쉽게 접근할 수 있는 포장 및 조리 식품을 선호함에 따라 포장 수요를 촉진할 것으로 예상됩니다.

COVID-19 팬데믹에 따른 전국적인 봉쇄와 제조 시설의 일시적인 폐쇄로 인해 공급망과 수출입에 차질이 생기는 등 여러 가지 문제가 발생했습니다. 그 결과 2020년 국내 포장재 생산량은 전년 대비 6% 감소하여 시장에 큰 영향을 미쳤습니다. 포장재 생산은 주로 플라스틱 포장재가 주도하고 있으며, 2021년에 생산된 포장재의 약 86%를 차지합니다. 다양한 용도의 연질 및 경질 포장에 대한 수요가 증가하고 플라스틱 재활용이 발전함에 따라 플라스틱 생산 부문은 예측 기간 동안 3.94 %의 연평균 성장률로 가장 빠른 성장을 기록 할 것으로 보입니다.

일본 포장 산업의 성장은 주로 1인당 소득 증가, 공급망 개선, 수년에 걸친 전자상거래 활동 증가에 기인합니다.

도요타, 혼다, 닛산 등 유명 자동차 제조업체의 본거지이자 전기차에 대한 수요 증가로 자동차 산업이 성장

일본에는 도요타, 혼다, 닛산 등 세계 최대의 자동차 회사가 있으며, 그 중 도요타는 시가총액 기준으로 세계 2위의 기업입니다. 도요타의 판매 수익은 2022년 3월에 마감된 회계연도에 전년 대비 15% 성장한 것으로 나타나 일본 자동차 시장의 성장 추세가 증가하고 있음을 알 수 있습니다.

COVID-19 팬데믹의 영향으로 전국적인 봉쇄 조치, 전반적인 경기 침체, 수출 감소, 공급망 중단 등으로 인해 자동차 판매가 급격히 감소했습니다. 이러한 요인으로 인해 승용차 판매 대수는 2019년의 399만 7,000대에서 2020년에는 384만 1,000대로 감소해, 2020년의 자동차 판매 대수는 감소했습니다.

일본은 환경 문제에 대한 인식이 높아지고 일본 도시에서 대중교통 이용이 증가하면서 2021년 자동차 시장 매출이 2020년에 비해 감소한 것으로 나타났습니다.

소비자들의 관심을 끌면서 전기자동차 판매량이 최고치를 기록했습니다. 자동차 산업의 전기자동차 부문은 2022-2027년 24.39%의 연평균 성장률을 기록할 것으로 예상됩니다.

일본의 접착제 산업 개요

일본의 접착제 시장은 세분화되어 있으며 상위 5개 기업이 25.89%를 점유하고 있습니다. 이 시장의 주요 업체는 3M, 아이카 코교 주식회사, 헨켈 AG & Co. KGaA, Sika AG 및 TOYOCHEM CO., LTD. (알파벳순으로 정렬).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

신발 및 가죽

포장

목공 및 목공예

규제 프레임워크

일본

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

신발 및 가죽

의료

포장

목공 및 목공예

기타

기술

핫멜트

반응성

용매

UV 경화형 접착제

수성

수지

아크릴계

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE 및 EVA

기타

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Aica Kogyo Co..Ltd.

Arkema Group

CEMEDINE Co.,Ltd.

HB Fuller Company

Henkel AG & Co. KGaA

Oshika

Sika AG

THE YOKOHAMA RUBBER CO., LTD.

TOYOCHEM CO., LTD.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

The Japan Adhesives Market size is estimated at 2.24 billion USD in 2024, and is expected to reach 2.72 billion USD by 2028, growing at a CAGR of 4.94% during the forecast period (2024-2028).

Emerging automotive market and building & construction industry expected to boost the consumption of adhesives in Japan

In Japan, adhesives are largely used across the packaging, automotive, building and construction, and healthcare industries. The consumption of adhesives in Japan declined in 2020 due to the impact of the COVID-19 pandemic. Demand fell by 11% in terms of volume in 2020 compared to 2019. The lockdown in the country for nearly six months, which resulted in the shutdown of production facilities and raw material shortage, is the major reason behind the decline in adhesives production and consumption in Japan.

The Japanese automobile industry is the third-largest globally, with 78 manufacturers in 22 prefectures employing over 5.5 million people. It is a vital pillar of the country's economy. Automotive manufacturing accounts for 89% of Japan's largest industrial sector (the transportation machinery industry), and car components suppliers have become a significant part of the Japanese economy, expanding into other industries such as chemicals and rubber. It is a highly innovative and technologically oriented business, with rising production of electric and hybrid vehicles in local and worldwide markets, as well as a growth in supply and demand on a global scale.

The prognosis for Japan's construction industries is better than it has been in years. The Japanese government has promised to boost the domestic economy with many public works projects. This commitment was prompted by its preparations for major events such as the 2020 Olympics and the 2025 World Expo in Osaka. The growing core industries across Japan are expected to increase the demand for adhesives over the forecast period.

Japan Adhesives Market Trends

With the advancement in plastic recyclability and demand from food and beverage industry, plastic packaging to lead the packaging industry

The Japanese packaging industry registered significant growth in recent times and contributed 1.13% to the nation's GDP owing to the growing trend for protecting and enhancing products' safety and longevity. The food & beverages sector contributes a major share to the Japanese packaging industry due to its complex and evolving nature. The Japanese government has set a target of achieving 45% sufficiency of food products by 2025, likely contributing to the packaging industry over the coming years. Moreover, the aging population is expected to propel packaging demand as elderly consumers prefer packaged and prepared food for easy access.

In line with the COVID-19 pandemic, the country-wide lockdowns and temporary shutdown of manufacturing facilities caused several issues, including disruptions to the supply chain and imports & exports. As a result, the country's packaging production declined by 6% in 2020 compared to the previous year, significantly affecting the market. Packaging production is majorly driven by plastic packaging in the country, which accounts for around 86% of the packaging produced in 2021. With the growing demand for flexible and rigid packaging for various applications and plastic recycling advancements, the plastic production segment is likely to register the fastest growth, with a 3.94% CAGR during the forecast period.

The growth of the Japanese packaging industry is mainly attributed to the rising per capita income, improvement of the supply chain, and increasing e-commerce activities over the years. The growing attention to food safety and quality in post-pandemic times across the nation is likely to drive the food processing industry, which will further propel the packaging demand over the coming years.

In addition to being home to renowned automotive manufacturers including Toyota, Honda, and Nissan, the demand for EVs is rising the automotive industry

Japan is home to the world's largest automotive companies, such as Toyota, Honda, and Nissan, of which Toyota is the world's second-largest company in terms of market capitalization. Toyota's sales revenue showed a 15% Y-o-Y growth in the fiscal year ending March 2022, suggesting an increasing trend of automotive market growth in Japan. Passenger vehicle sales in Japan are expected to reach 3951.71 thousand units by 2027.

Due to the impact of the COVID-19 pandemic, the sales of automobiles reduced drastically because of nationwide lockdowns, overall economic slowdown, decreased exports, supply chain disruptions, etc. These factors led to a decrease in the sales volume of automobiles in 2020 as passenger car sales fell from 3997 thousand in 2019 to 3841 thousand in 2020.

Japan witnessed a decrease in automotive market revenue in 2021 compared to 2020 because of the increasing awareness of environmental concerns and increased use of public transport in the cities of Japan. The government is also supporting the cause by making public transport more efficient than before. The railways cover nearly 72% of the public transportation system in Japan.

Japan witnessed peak sales of electric vehicles in 2017 because of the launch of new plug-in hybrid vehicles, which appealed to consumers. The electric vehicles segment of the automotive industry is expected to record a CAGR of 24.39% in 2022-2027. The number of electric vehicles sold in Japan is expected to be 165.5 thousand by 2027. This will lead to an increase in the overall revenue of the automotive industry in Japan.

Japan Adhesives Industry Overview

The Japan Adhesives Market is fragmented, with the top five companies occupying 25.89%. The major players in this market are 3M, Aica Kogyo Co..Ltd., Henkel AG & Co. KGaA, Sika AG and TOYOCHEM CO., LTD. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.1.4 Footwear and Leather

4.1.5 Packaging

4.1.6 Woodworking and Joinery

4.2 Regulatory Framework

4.2.1 Japan

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Footwear and Leather

5.1.5 Healthcare

5.1.6 Packaging

5.1.7 Woodworking and Joinery

5.1.8 Other End-user Industries

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Solvent-borne

5.2.4 UV Cured Adhesives

5.2.5 Water-borne

5.3 Resin

5.3.1 Acrylic

5.3.2 Cyanoacrylate

5.3.3 Epoxy

5.3.4 Polyurethane

5.3.5 Silicone

5.3.6 VAE/EVA

5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Aica Kogyo Co..Ltd.

6.4.3 Arkema Group

6.4.4 CEMEDINE Co.,Ltd.

6.4.5 H.B. Fuller Company

6.4.6 Henkel AG & Co. KGaA

6.4.7 Oshika

6.4.8 Sika AG

6.4.9 THE YOKOHAMA RUBBER CO., LTD.

6.4.10 TOYOCHEM CO., LTD.

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)