유럽의 건설용 접착제 및 실란트 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Europe Construction Adhesives & Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1692580

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

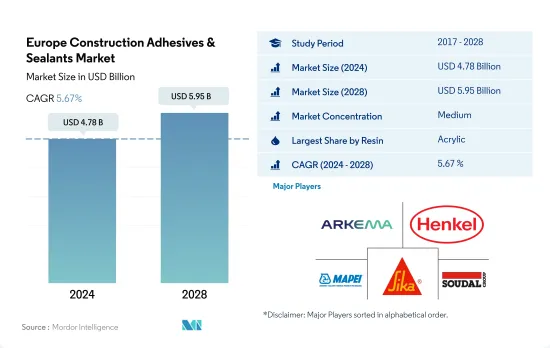

유럽의 건설용 접착제 및 실란트 시장 규모는 2024년 47억 8,000만 달러, 2028년에는 59억 5,000만 달러에 이르고, 예측 기간 중(2024-2028년) CAGR 5.67%로 성장할 것으로 예측됩니다.

유럽 건설용 접착제 및 실란트 성장을 지원하는 정부 정책 및 이니셔티브

건설 업계에서는 카펫 깔개, 바닥재, 목재, 조립식 패널 접합, 벽 코팅, 날씨 씰, 지붕 등의 목적으로 접착제 및 실란트가 필요합니다. EURO CONSTRUCT의 보고서에 따르면 건설 업계는 서유럽에서 2022-2024년 CAGR이 6.1%, 중동유럽에서 2022-2024년 CAGR이 6.4%를 나타낼 것으로 예상되고 있습니다.

유럽위원회는 에너지 효율 지령(Energy Efficiency Directive) 및 건설물의 에너지 성능(Energy Performance of Buildings) 등의 틀로 주택 인프라를 에너지 효율이 높은 디지털 자원 성능으로 이행시키는 정책을 책정하고 있습니다.

지붕재, 바닥재, 창 설치 등 다양한 용도의 건설산업에서 사용되는 패스너는 뛰어난 강도를 유지하는 건설용 접착제 및 실란트로 방지할 수 있는 고장이 발생하기 쉽습니다.

아크릴 수지는 기계적 접합이나 다른 기재와의 접착제로서, 또한 수축하기 쉬운 재료의 실란트로서 폭넓게 사용되고 있기 때문에 2021년 시점에서 유럽의 건설용 접착제 및 실란트 시장의 금액 점유율에서 최대의 점유율을 차지하고 있습니다.

아일랜드, 스페인, 슬로바키아의 건설 생산 증가로 건설용 접착제 및 실란트 수요 증가

2020년 건설생산고가 전체적으로 4.4% 감소한 이유는 COVID-19 팬데믹이 유럽 전역으로 퍼져 전국적인 단단히 묶여 공급망의 혼란, 사회적 거리의 강제규제 등으로 이어졌기 때문입니다. 20년의 건설에 필요한 접착제 및 실란트 수요는 감소했습니다.

건설용 접착제 및 실란트 수요는 2021년에 크게 증가하였으나 이는 차세대 EU와 같은 2020년 COVID-19에 의한 전반적인 경기 감속에 대한 EU 위원회 회복 계획 때문 건설용 접착제 및 실란트 수요에 있어서의 전체적인 성장은 덴마크 등의 북유럽 국가가 전년대비 17.8% 증가를 기록했기 때문에 기타 유럽 부문의 2021년이 가장 높았습니다.

유럽의 건설용 접착제 및 실란트 시장에서의 금액 점유율은 기타 유럽 부문이 가장 높고, 점유율의 절반 가까이를 차지하고 있습니다.

유럽의 건설용 접착제 및 실란트 시장 동향

리노베이션 요구가 증가함에 따라 신축 급증이 업계를 견인

2020년의 건설업 전체의 수익은 COVID-19에 의한 팬데믹 상황의 영향으로부터 급감을 나타내, 전체적인 회복의 둔화와 작업 현장에서의 사회적 거리 조치에 연결되었습니다.

유럽의 건설 부문 전체 매출은 엄청난 성장을 보였으며, 2021년 전년 대비 성장률은 2020년에 비해 가장 높았습니다. 차세대 EU 계획에서는 건설물의 그린화와 디지털화라는 유럽의 목표가 기존의 건설물과 구조물의 연간 개수율 증가로 이어졌기 때문에 건설 부문이 최대의 투자를 받았습니다.

EURO CONSTRUCT의 보고서에 따르면 EU의 정치적 지역을 기반으로 한 부문 중 중동 유럽의 CAGR은 6.4%, 그 다음 서유럽의 CAGR은 6.1%로 예상됩니다.

유럽연합(EU) 및 국가 수준의 정책 입안자는 ‘건설물의 에너지 성능에 관한 지령(Energy Performance of Buildings Directive)’을 비롯한 다양한 정책을 통해 신규 건설물의 건설과 기존 건설물의 에너지 효율화를 우선하고 있습니다.

유럽 건설용 접착제 및 실란트 산업 개요

유럽의 건설용 접착제 및 실란트 시장은 상위 5개사에서 51.69%를 차지하며 적당히 통합되어 있습니다. 시장의 주요 기업은 Arkema Group, Henkel AG & Co. KGaA, MAPEI SpA, Sika AG, Soudal Holding NV(알파벳순)이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

건설

규제 프레임워크

EU

러시아

밸류체인과 유통채널 분석

제5장 시장 세분화

수지

아크릴

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE 및 EVA

기타 수지

기술

핫멜트

반응성

실란트

용제형

수성

국가명

프랑스

독일

이탈리아

러시아

스페인

영국

기타 유럽

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

HB Fuller Company

Henkel AG & Co. KGaA

Illinois Tool Works Inc.

MAPEI SpA

RPM International Inc.

Sika AG

Soudal Holding NV

Wacker Chemie AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업의 개요

개요

Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 억제요인, 기회

정보원과 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Europe Construction Adhesives & Sealants Market size is estimated at 4.78 billion USD in 2024, and is expected to reach 5.95 billion USD by 2028, growing at a CAGR of 5.67% during the forecast period (2024-2028).

Government policies and initiatives to support the growth of construction adhesives and sealants in Europe

The construction industry requires adhesives and sealants for purposes such as carpet layering, flooring, timber, prefabricated panels joining, wall covering, weather-sealing, and roofing. The construction industry is expected to record a 6.1% CAGR in 2022-2024 in Western Europe and a 6.4% CAGR in 2022-2024 in Central and Eastern Europe, per the EURO CONSTRUCT report. This is expected to increase demand for construction adhesives and sealants in the forecast period.

The European Commission has framed policies to transit the residential infrastructure to energy-efficient and digital resource performance with frameworks such as the Energy Efficiency Directive and Energy Performance of Buildings. These initiatives will require the renovation of existing buildings, leading to an increase in demand for adhesives and sealants required for construction in the forecast period 2022-2028.

The fasteners used in the construction industry for different applications, such as roofing, flooring, and window fitting, are prone to failures that can be prevented with good strength holding construction adhesives and sealants. With the development of efficient resource planning in construction, the demand for construction adhesives and sealants is expected to increase in the period 2022-2028.

Acrylic resin accounted for the maximum share of the European construction adhesives and sealants market value share as of 2021 because of its wide usage as an adhesive for mechanical joining and with different substrates and as a sealant for materials prone to shrinkage. These applications make them widely used in the construction industry, and their demand is expected to grow over the forecast period.

Rising construction output from Ireland, Spain, and Slovakia to raise the demand for construction adhesives and sealants

In 2020, the overall decline in construction output by 4.4% was due to the COVID-19 pandemic spreading across Europe, which led to nationwide lockdowns, supply chain disruptions, mandatory social distancing regulations, etc. These factors led to declining demand for adhesives and sealants required for construction in 2020. The decline was maximum for the Rest of Europe regional segment because of the huge recessions in countries such as Slovakia, which recorded a 16.8% Y-o-Y decline in its construction output.

The demand for construction adhesives and sealants increased tremendously in 2021 because of the EU Commission's recovery plan for an overall economic slowdown due to COVID-19 in 2020 such as Next Generation EU, in which the maximum fund allocation was done for the construction sector to make European buildings environmentally benign with decreased wastage of resources. The overall growth in demand for construction adhesives and sealants was highest in 2021 for the Rest of Europe segment because of Nordic countries, such as Denmark, which registered a growth of 17.8% Y-o-Y in construction output.

The value share in the European construction adhesives and sealants market is highest for the Rest of Europe segment, which accounts for nearly half of the share because the overall construction output from countries such as Ireland is expected to grow by 15.1%, followed by Spain with 14.3%, and Slovakia with 13.5%, as published in a report by EURO CONSTRUCT in 2021.

Europe Construction Adhesives & Sealants Market Trends

Rapid growth of new construction along with rising need for renovation activities will drive the industry

The overall revenue of construction showed a steep decrement in 2020 because of the impact of the pandemic situation due to COVID-19, which led to an overall recovery slowdown and social distancing measures on work sites.

The overall revenue of the construction sector in Europe grew tremendously, with the highest year-on-year growth in 2021 compared to that of 2020 because of the initiatives and measures taken by the EU Commission, such as the infusion of EUR 750 billion for all sectors under the COVID recovery plan named Next Generation EU. Under the Next Generation EU plan, the construction sector received the maximum investment because of the European objective of green and digital transition in buildings which led to growth in the annual renovation rate of existing buildings and structures.

As per the EUROCONSTRUCT report, among the segments of the European Union based on political geography, Central and Eastern Europe are expected to register a CAGR of 6.4%, followed by Western Europe at a CAGR of 6.1% in 2022-2024.

The policymakers at European Union and national level are prioritizing the construction of new buildings and conversion of existing buildings to be energy efficient through various policies including Energy Performance of Buildings Directive and others. These policies will lead to an increase in overall revenue for construction in the forecast period.

Europe Construction Adhesives & Sealants Industry Overview

The Europe Construction Adhesives & Sealants Market is moderately consolidated, with the top five companies occupying 51.69%. The major players in this market are Arkema Group, Henkel AG & Co. KGaA, MAPEI S.p.A., Sika AG and Soudal Holding N.V. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Building and Construction

4.2 Regulatory Framework

4.2.1 EU

4.2.2 Russia

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 Resin

5.1.1 Acrylic

5.1.2 Cyanoacrylate

5.1.3 Epoxy

5.1.4 Polyurethane

5.1.5 Silicone

5.1.6 VAE/EVA

5.1.7 Other Resins

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Sealants

5.2.4 Solvent-borne

5.2.5 Water-borne

5.3 Country

5.3.1 France

5.3.2 Germany

5.3.3 Italy

5.3.4 Russia

5.3.5 Spain

5.3.6 United Kingdom

5.3.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 H.B. Fuller Company

6.4.4 Henkel AG & Co. KGaA

6.4.5 Illinois Tool Works Inc.

6.4.6 MAPEI S.p.A.

6.4.7 RPM International Inc.

6.4.8 Sika AG

6.4.9 Soudal Holding N.V.

6.4.10 Wacker Chemie AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)