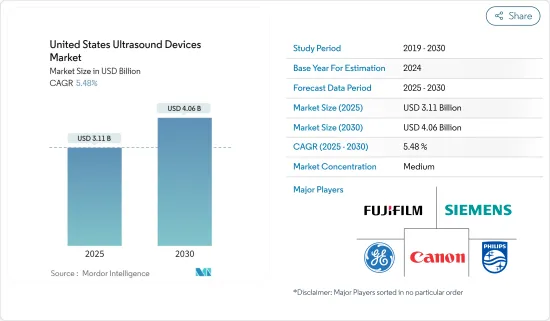

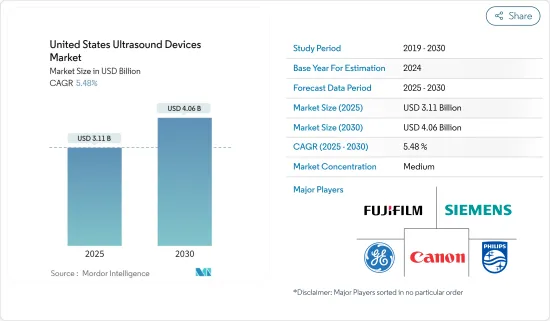

미국의 초음파 장치 시장 규모는 2025년 31억 1,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR 5.48%로 확대되어 2030년에는 40억 6,000만 달러에 달할 것으로 예측되고 있습니다.

COVID-19는 팬데믹에 의해 환자가 초음파 영상 진단과 같은 구명을 위한 영상 처치를 기다려야 하고, 환자의 의료시설에의 액세스에 영향을 주고 있습니다. 팬데믹은 환자가 영상 진단을 받기까지의 대기 시간을 증가시켰습니다. Radiology Society of North America가 2021년 4월 발표한 논문 「The Economic Impact of the COVID-19 Pandemic on Radiology Practices」에 의하면, 팬데믹은 미국의 방사선 진료소에 큰 영향을 미쳤습니다. 또한 2020년 5월에 Journal of the American College of Radiology에 게재된 Jason J. Naidich의 논문 「Impact of the COVID-19, Pandemic on Imaging Case Volumes에 따르면 2020년 상반기 총 촬영 건수는 2019년부터 12.29% 감소했습니다. 이것은 영상 기술이 시장 대수 감소를 가져왔다는 것을 보여줍니다. 기사에서는 또 모달리티 종류별로 영상 진단 건수의 감소가 다르며, 유방조영술이 가장 높은 감소율(94%)을 나타내며 핵의학(85%), MRI(74%), 초음파(64%), 인터벤셔널 라디올로지(56%), CT(46%), X선(22%)으로 이어졌습니다. COVID-19의 유행에 의한 영상 진단 사례 수에 대한 영향을 완화하고, 2021년에 회복 계획을 책정했습니다. 따라서, COVID-19는 미국에서 조사된 시장에 큰 영향을 준 것이 관찰됩니다.

시장 성장에 영향을 미치는 주요 요인은 만성 질환 증가, 기술의 진보, 초음파의 응용 분야의 확대입니다.

또한 이 분야의 새로운 연구개발과 혁신, 주요 시장 진출기업에 의한 신제품의 발매, 미국 식품의약품국으로부터의 새로운 승인과 함께, 초음파 시장은 본 조사의 예측 기간 중에 더욱 성장할 것으로 예측됩니다. 2021년 10월, Mindray North America는 포인트 오브 케어 시장에서 초음파 가능성을 최대화하는 신제품 TE7 Max 초음파 시스템을 출시했습니다. 이 신제품은 다른 추종을 불허하는 21.5인치의 수직 고화질 LED 디스플레이와 임상의가 볼 수있는 것을 진정으로 극대화하기위한 밀봉 된 터치 기반 인터페이스를 갖추고 있습니다.

따라서 위와 같은 요인들로 인해 이 시장은 예측기간 동안 건전한 성장을 이룰 것으로 기대됩니다.

마취학은 수술 전, 수술 중, 수술 후 환자의 종합적인 주술기 케어에 관련되는 의료 전문 분야라고 불립니다. 마취학에는 마취, 집중 치료 의학, 중증 구급 의학, 통증 의학이 포함됩니다.

이 분야의 성장을 가속하는 주요 요인은 혁신적인 제품 출시, 기술 발전, 초음파 장치의 채택 확대입니다.

예를 들어 General Electric는 2021년 3월에 새로운 무선 휴대형 초음파 진단 장치 Vscan Air를 발매했습니다.

또한, 2021년 1월, Konica Minolta Healthcare Americas, Inc.는 Medovate Ltd.와의 사이에서 Medovate사의 국소 마취 주사 솔루션 SAFIRA와 코니카 미놀타의 초음파 가이드 하수기용 솔루션 시리즈를 미국에서 공동 판매하는 계약을 체결했다고 발표했습니다. SONIMAGE HS2 등의 화상 진단 장치를 조합하는 것으로, 국소 마취의 한층 더 보급과 환자의 안전성 향상을 목표로 합니다.

따라서 초음파에 대한 위의 개발은 앞으로 수년간 시장 성장을 가속할 것으로 예측됩니다.

시장은 소수의 대기업에 집중하고 있습니다. 기업은 세계적으로 높은 평가를 받고 있으며 각 회사는 선진국 시장과 신흥국 시장에 폭넓게 진출하고 있습니다.

The United States Ultrasound Devices Market size is estimated at USD 3.11 billion in 2025, and is expected to reach USD 4.06 billion by 2030, at a CAGR of 5.48% during the forecast period (2025-2030).

COVID-19 has impacted the patient's access to healthcare facilities as the pandemic has forced the patients to wait for life-saving imaging procedures such as ultrasound imaging. The pandemic has increased the waiting time for patients to have their imaging done. According to an article published by the Radiology Society of North America in April 2021, titled,' The Economic Impact of the COVID-19 Pandemic on Radiology Practices', The pandemic had a profound impact on radiology practices across the country. Policy measures adopted to slow the transmission of disease are decreasing the demand for imaging independent of COVID-19. Hospital preparations to expand crisis capacity are further diminishing the amount of appropriate medical imaging that can be safely performed. Furthermore, according to Jason J. Naidich's article titled 'Impact of the COVID-19,) Pandemic on Imaging Case Volumes,' published in the Journal of the American College of Radiology in May 2020, the total imaging volume in the first half of 2020 was down 12.29% from 2019. Imaging volumes decreased by 28.10% across all patient care sites and modality types after COVID-19. This indicates that imaging techniques resulted in a decline in market volumes. The article also noted that the imaging volume decline differed by modality type, with mammography showing the highest reduction (94%) by week 16, followed by nuclear medicine (85%), MRI (74%), ultrasound (64%), interventional radiology (56%), CT (46%), and x-ray (22%). However, the radiology clinics mitigated the impact of the COVID-19 epidemic on imaging case volumes and established recovery plans in 2021. Therefore, it is observed that COVID-19 significantly impacted the market studied in the United States.

The major factors affecting the growth of the market are the increasing incidences of chronic diseases, increasing technological advancements, and the growing applications of ultrasound.

Furthermore, with the new research and developments and innovations in the area, coupled with the launch of new products by the key market players and new approvals from the United States Food and Drug Administration, the ultrasound market is further expected to grow over the forecast period of the study. For instance, in October 2021, Mindray North America launched a new product that is maximizing the potential of ultrasound in the Point of Care (POC) market: the TE7 Max Ultrasound System. This new product has an unrivaled 21.5-inch vertically oriented high-definition LED display and a sealed touch-based interface to truly maximize what clinicians can see.

Therefore, owing to the above-mentioned factors, it is expected that the market studied will witness healthy growth over the forecast period.

Anesthesiology is referred to as a medical specialty concerned with the total perioperative care of the patients before, during, and after surgery. It includes anesthesia, intensive care medicine, critical emergency medicine, and pain medicine. Anesthesiology includes the study and use of anesthesia to safely support a patient's vital functions through the perioperative period.

The major factors fueling the growth of the segment are innovative product launches, technological advancements, and the growing adoption of ultrasound devices.

For instance, in March 2021 General Electric launched its new wireless, hand-held ultrasound device, Vscan Air, as the company seeks to capture a leading position in the growing market in the United States and some other countries. The device provides the procedure guidance needed to deliver regional anesthesia and guidance for other procedures. Such developments are expected to boost the adoption of ultrasound devices for anesthesiology applications in the United States, thereby supporting the market growth.

Moreover, in January 2021, Konica Minolta Healthcare Americas, Inc. announced an agreement with Medovate Ltd. to jointly promote Medovate's SAFIRA regional anesthesia injection solution with Konica Minolta's range of solutions for ultrasound-guided procedures in the United States. This initiative is the latest addition to Konica Minolta's UGPro Solution, which brings together education, procedures, and imaging equipment, such as the SONIMAGE HS2 Compact Ultrasound System, to further expand the use of regional anesthesia and enhance patient safety. Such developments are further expected to expand the usage of ultrasound devices for anesthesiology applications in the country.

Hence, the above developments about ultrasound is expected to drive the market growth in the coming years.

The market is concentrated with a few large players. Public and private companies are found investing in R&D to advance their technologies in the field of ultrasound imaging, as it is becoming one of the fundamental aspects of healthcare. The updated technological portable devices are praised globally, and the companies have a wide presence across the developed and emerging markets. Some of the major companies investing in ultrasound devices are Philips, Siemens, Canon, and Fujifilm.