Philippines Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1692498

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

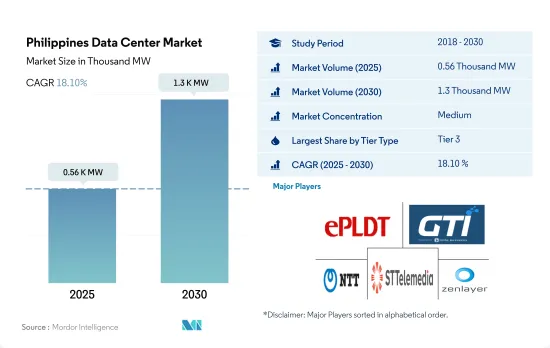

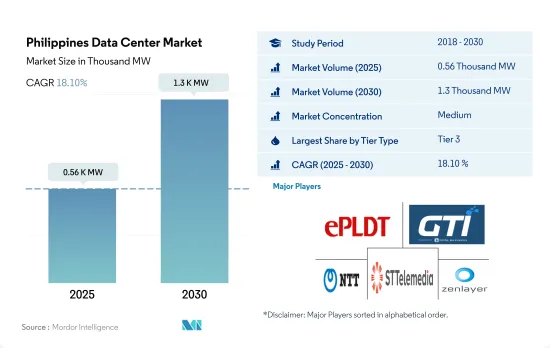

필리핀의 데이터센터 시장 규모는 2025년 560kW로 추정되며, 2030년에는 1,300kW에 이를 것으로 예상되며 CAGR은 18.10%로 성장할 것으로 예상됩니다.

또한 2025년에는 3억 9,200만 달러의 코로케이션 수익이 예상되며, 2030년에는 11억 6,200만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 24.27%로 확대될 것으로 예상됩니다.

2023년에는 Tier 3 데이터센터가 수량 기준으로 대부분의 점유율을 차지하지만, 예측 기간 동안 Tier 4가 가장 빠르게 성장하고 있습니다.

Tier 1 부문의 성장은 시설의 신뢰성이 낮고 가동 중지 시간이 길어지기 때문에 정체가 예상됩니다. Tier 2 부문의 IT 부하 용량은 CAGR 4.33%로 2021년 125.6MW에서 2029년에는 172.6MW로 증가할 것으로 예측됩니다.

필리핀 데이터센터 시장에서 Tier 3 부문의 IT 부하 용량은 CAGR 25.75%로 2021년 78.3MW에서 2029년에는 489.3MW로 증가할 것으로 예측됩니다. 이 데이터센터는 N+1중복화에 의해 99.98%의 업타임을 제공해, 1년간의 다운타임은 불과 1.6시간 정도입니다.

현재 이 지역에서는 Tier 3 데이터센터가 매우 보급되어 있어 일부 시설에서는 구조와 서비스를 필요한 수준까지 업그레이드하고 있습니다.

2029년까지 필리핀의 데이터센터 시장에서 Tier 4 부문의 IT부하 용량은 70MW에 달할 것으로 예상되고 있습니다. 현재 필리핀에는 Tier 4 인증을 받은 코로케이션 시설은 없습니다. 그러나, ePLDT는 산타로사에 있는 11번째의 데이터센터를 Tier 4로 2023년까지 가동시킨다고 발표했습니다.

새로운 데이터센터 운영자는 높은 신뢰성을 제공하기 위해 인프라 시설에 Tier 4 등급 인증을 선호합니다.

필리핀 데이터센터 시장 동향

필리핀 소비자는 하루 10시간을 스마트폰으로 보내 매일 대량의 데이터 전송을 합니다.

2022년 필리핀의 스마트폰 사용자 수는 약 1억 100만명으로, 2029년에는 CAGR 8.79%로 1억 8,100만명에 이를 것으로 예상되고 있습니다.

유행 이후 스마트폰은 브라우징, 금융 거래, 온라인 쇼핑 등에 편리한 것으로 밝혀졌기 때문에 수요가 크게 증가했습니다. 게임, 스트리밍 컨텐츠, 뉴스 열람, 온라인 쇼핑 등에 이러한 가제트를 사용하고 있습니다.

필리핀은 세계에서 유일하게 사용자가 하루 평균 10시간 동안 전화를 사용하는 국가입니다. 하자 온라인게임이 주최하는 이벤트는 스마트폰 수요를 더욱 높였습니다.

DITO, Globe, Smart 등 모바일 사업자에 의한 5G 네트워크의 확대가 데이터센터 시장을 뒷받침

필리핀의 소비자는 현재 4G와 3G 서비스를 큰 비율로 이용하고 있습니다.

필리핀에서 5G 서비스를 제공하는 시설은 DITO, Globe, Smart입니다. 이들 기업은 네트워크 연결을 강화하기 위해 거점을 확대하고 있습니다

예를 들어, Smart는 5G 네트워크를 강화하기 위해 2022년에 5G 변전소의 수를 7300으로 늘렸습니다.

필리핀 데이터센터 산업 개요

필리핀의 데이터센터 시장은 적당히 통합되어 있으며 상위 5개 기업에서 54.17%를 차지하고 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 시장 전망

내하중

바닥면적

코로케이션 수입

설치 랙 수

랙 공간 이용률

해저 케이블

제5장 주요 업계 동향

스마트폰 사용자수

스마트폰 1대당 데이터 트래픽

모바일 데이터 속도

광대역 데이터 속도

광섬유 접속 네트워크

규제 프레임워크

필리핀

밸류체인과 유통채널 분석

제6장 시장 세분화

핫스팟

NCR(메트로 마닐라)

기타 지역

데이터센터의 규모

라지

매시브

미디움

메가

스몰

티어 유형

Tier 1 및 2

Tier 3

Tier 4

흡수량

비이용

이용

코로케이션 유형별

하이퍼스케일

소매

도매

최종 사용자별

BFSI

클라우드

전자상거래

정부기관

제조업

미디어 및 엔터테인먼트

텔레콤

기타 최종 사용자

제7장 경쟁 구도

시장 점유율 분석

기업 상황

기업 프로파일

Bitstop

Dataone

ePLDT Inc.

GTI Corporation

NTT Ltd

Space DC Pte Ltd

STT GDC Pte Ltd

VSTECS Phils Inc.

Zenlayer Inc.

조사한 기업 목록

제8장 CEO에 대한 주요 전략적 질문

제9장 부록

세계의 개요

개요

Porter's Five Forces 분석 프레임워크

세계의 밸류체인 분석

세계 시장 규모와 DRO

정보원과 참고문헌

도표 목록

주요 인사이트

데이터 팩

용어집

JHS

영문 목차

영문목차

The Philippines Data Center Market size is estimated at 0.56 thousand MW in 2025, and is expected to reach 1.3 thousand MW by 2030, growing at a CAGR of 18.10%. Further, the market is expected to generate colocation revenue of USD 392 Million in 2025 and is projected to reach USD 1,162 Million by 2030, growing at a CAGR of 24.27% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, Tier 4 is fastest growing through out the forecasted period

Growth in the tier 1 segment is expected to be stagnant due to the unreliability and longer downtimes of facilities. The IT load capacity of the tier 2 segment is expected to increase from 125.6 MW in 2021 to 172.6 MW by 2029 at a CAGR of 4.33%. These data centers are preferred mainly by small businesses due to the performance they offer at an affordable cost. However, a downtime of 22 hours annually, at times, makes companies reluctant and hesitant to opt for them.

The IT load capacity of the tier 3 segment of the data center market in the Philippines is anticipated to increase from 78.3 MW in 2021 to 489.3 MW by 2029 at a CAGR of 25.75%. These data centers offer an uptime of 99.98% with N+1 redundancies, and they only have around 1.6 hours of downtime in a year. These advantages have made them highly preferable by large businesses.

Currently, tier 3 data centers are highly prevalent in the region, as some facilities have upgraded their structures and services to the required standards. Operators prefer newly constructed facilities to be tier 3 and tier 4 ready.

The IT load capacity of the tier 4 segment of the data center market in the Philippines is expected to reach 70 MW by 2029. These data centers are expected to be operational in 2023 and are preferred due to their high reliability and lower downtime of around 26.3 minutes. Currently, the Philippines has no colocation facility with Tier 4 certification. However, ePLDT announced that its 11th data center in Santa Rosa would be tier 4 and would be launched by 2023.

Operators of new data centers prefer Tier 4 grade certifications for their infrastructure facilities due to the high reliability offered.

Philippines Data Center Market Trends

Philippines consumers spends 10hr/day on smartphone, generating huge amount of data transfer daily, this would drive data center market

The Philippines had around 101 million smartphone users in 2022, which is expected to reach 181 million by 2029 at a CAGR of 8.79%.

Post-pandemic, the demand for smartphones has significantly increased as they turned out to be useful for browsing, financial transactions, online shopping, and others. People are adopting urban lifestyles and use these gadgets for automation functions in their homes, online gaming, streaming content, browsing news, and online shopping. The convenience of doing almost everything instantly has increased the number of users and is expected to increase with the increasing population.

The Philippines is the only country in the world where users, on average, spend an average of 10 hours a day on the phone. As the telecom network developed and improved its facilities, users could attain good mobile data speeds on their smartphones which increased their functionality and experience. Online games on mobile have improved their quality, and the events organized by them have furthermore increased the demand for smartphones. As phones with higher processors, better displays, and batteries are available at a budget price. 74% of the users prefer mobile gaming over PC and console gaming.

Expansion of 5G network by mobile operators such as DITO, Globe, and Smart boost the data center market

Consumers in the Philippines currently use 4G and 3G services in greater proportion. 5G network services were launched at the end of 2021 and were increasingly adopted by customers in the first quarter of 2022.

Facilities offering 5G services in the Philippines are DITO, Globe, and Smart. These companies are expanding their bases to strengthen their network connectivity.

For instance, Smart increased the count of its 5G substations to 7300 in 2022 to strengthen its 5G networks.

Philippines Data Center Industry Overview

The Philippines Data Center Market is moderately consolidated, with the top five companies occupying 54.17%. The major players in this market are ePLDT Inc., GTI Corporation, NTT Ltd, STT GDC Pte Ltd and Zenlayer Inc. (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 MARKET OUTLOOK

4.1 It Load Capacity

4.2 Raised Floor Space

4.3 Colocation Revenue

4.4 Installed Racks

4.5 Rack Space Utilization

4.6 Submarine Cable

5 Key Industry Trends

5.1 Smartphone Users

5.2 Data Traffic Per Smartphone

5.3 Mobile Data Speed

5.4 Broadband Data Speed

5.5 Fiber Connectivity Network

5.6 Regulatory Framework

5.6.1 Philippines

5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

6.1 Hotspot

6.1.1 NCR (Metro Manila)

6.1.2 Rest of Philippines

6.2 Data Center Size

6.2.1 Large

6.2.2 Massive

6.2.3 Medium

6.2.4 Mega

6.2.5 Small

6.3 Tier Type

6.3.1 Tier 1 and 2

6.3.2 Tier 3

6.3.3 Tier 4

6.4 Absorption

6.4.1 Non-Utilized

6.4.2 Utilized

6.4.2.1 By Colocation Type

6.4.2.1.1 Hyperscale

6.4.2.1.2 Retail

6.4.2.1.3 Wholesale

6.4.2.2 By End User

6.4.2.2.1 BFSI

6.4.2.2.2 Cloud

6.4.2.2.3 E-Commerce

6.4.2.2.4 Government

6.4.2.2.5 Manufacturing

6.4.2.2.6 Media & Entertainment

6.4.2.2.7 Telecom

6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

7.1 Market Share Analysis

7.2 Company Landscape

7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).