ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

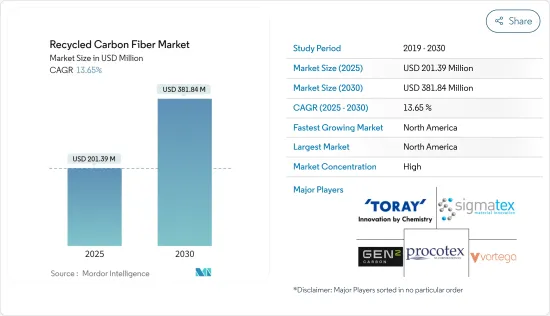

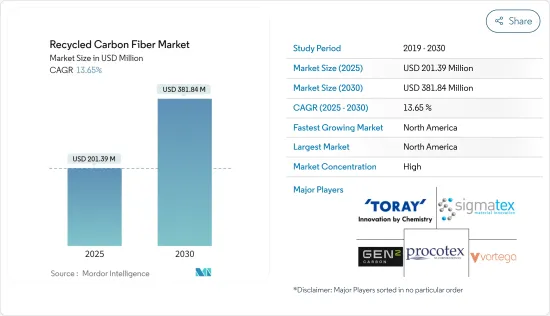

세계의 재활용 탄소섬유 시장 규모는 2025년 2억 139만 달러로 추정되며 예측기간 중(2025-2030년) CAGR 13.65%를 나타낼 전망이며, 2030년에는 3억 8,184만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

2020년, 시장은 공급 체인의 혼란에 의해 COVID-19의 악영향을 받았습니다.

단기적으로는 경량 자동차 수요 증가, 탄소섬유 스크랩의 리사이클 증가, 풍력에너지 분야에서의 재이용 증가, 리사이클 탄소섬유의 비용 대 효과 등이 시장 수요를 견인하는 요인의 하나입니다.

재활용 탄소섬유의 다양한 대안의 가용성과 공급망의 안전성은 시장 성장을 방해하는 요인입니다.

지속가능성 중시로의 전환, 리사이클 기술의 연구개발의 진전, 적층조형이나 3D 프린팅 분야로부터의 잠재적인 수요 증가는 향후 수년간 시장에 기회를 가져올 가능성이 높습니다.

북미가 시장을 독점하고 예측 기간 중에 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

재활용 탄소섬유 시장 동향

항공우주 및 방위 산업에서의 용도 증가

재활용 탄소섬유는 항공우주 및 방위산업에서 사용되는 복합재료의 제조에 사용되는 새로운 탄소섬유와 유사한 특성을 가지고 있습니다.

재활용 탄소섬유는 연비를 개선하기 위해 알루미늄을 대신하여 항공기에 사용되고 있습니다.

경량소재는 온실가스 배출량과 매립지로 보내지는 폐기물의 양을 줄이기 위해 사용되고 있습니다.

게다가 항공기의 폐기물이라는 중대한 문제를 관리하기 위해 항공우주산업에서는 재활용탄소섬유를 선호하는 경향도 강해지고 있습니다.

Airbus는 2020-2025년까지 탄소섬유 폐기물의 95%를 재활용하고, 5%를 항공우주 분야에 재이용한다는 목표를 내걸고 있습니다.

승객 수 증가와 항공기의 퇴역 증가에 따라 향후 20년간 4만 4,040대(6조 8,000억 달러 상당)의 새로운 제트기가 필요할 것으로 예상됩니다.

국제항공운송협회(IATA)에 따르면 민간항공사의 세계 매출은 2020년에는 3,730억 달러로 평가되었으며, 2021년에는 4,720억 달러로 추정되어 전년대비 26.7%의 성장률을 기록했습니다.

Boeing에 따르면 2040년까지 세계의 민간 항공기 보유 대수는 49,000대를 넘어 중국, 유럽, 북미, 아시아태평양 국가들이 각각 신형기 납품의 약 20%를 차지하고 나머지 20%는 그 밖의 신흥 시장으로 옮겨갑니다고 합니다.

이러한 요인으로부터, 재활용 탄소섬유 시장은 예측 기간 중에 세계적으로 성장할 것으로 보입니다.

북미가 시장을 독점

북미가 시장을 독점할 것으로 예상됩니다. 이 지역에서는 미국이 GDP에서 가장 큰 경제대국입니다.

급성장하는 자동차산업과 항공우주산업이 북미지역에서 연구되고 있는 시장의 성장을 견인하고 있습니다.

미국은 이 지역의 재활용 탄소섬유 소비의 리더이며, 대기업에 의해 사용되고 있습니다.

게다가 미국에서는 연방항공국(FAA)에 따르면 동국의 상업용 항공기 수는 2020년에 5,882기로 전년대비 22.9%의 감소율을 기록했습니다.

캐나다에서는 퀘벡주 복합재료개발센터(Centre developpement des composites du Quebec)(CDCQ)가 탄소섬유를 포함한 다양한 복합재료의 가치사슬에 관한 다양한 활동을 실시했습니다.

세계적으로 볼 때, 캐나다는 민간 비행 시뮬레이션으로 1위, 민간 엔진 생산으로 3위, 민간 항공기 생산으로 4위에 위치해 있습니다.

캐나다의 풍력에너지는 발전량의 3.5%를 차지하고, 이 지역에서 두 번째로 중요한 재활용 가능 에너지발전원이 되고 있습니다. 캐나다는 수력, 바이오매스, 풍력, 태양광 등 다양한 에너지원을 가지는 지역이기 때문에 재활용 가능 에너지의 생산과 이용에 있어서 세계를 리드하는 나라의 하나입니다.

이러한 요인으로부터, 이 지역의 재활용 탄소섬유 시장은 예측 기간 중에 안정된 성장이 예상됩니다.

재활용 탄소섬유 산업 개요

재활용 탄소섬유 시장은 부분적으로 통합되어 있습니다.

기타 혜택:

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트·지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

경량 자동차에 대한 수요 증가

탄소섬유 스크랩의 재활용과 풍력에너지 분야에서의 재이용의 확대

재활용 탄소섬유의 비용 효과

억제요인

다양한 대체품의 이용가능성

재활용 탄소섬유공급 체인의 안전성

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

유형

찹드 재활용 탄소섬유

분쇄 재활용 탄소섬유

소스

자동차용 스크랩

항공우주 스크랩

기타

최종 사용자 산업

자동차

항공우주 및 방위

풍력에너지

스포츠 용품

기타 최종 사용자 산업

지역

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

세계 기타 지역

남미

중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

Alpha Recyclage Composites

Carbon Conversions

Carbon Fiber Recycling

Carbon Fiber Remanufacturing

Gen 2 Carbon Limited

Karborek RCF

Mitsubishi Chemical Holdings Corporation.

Procotex

Shocker Composites LLC

Sigmatex

Toray Industries Inc.

Vartega Inc.

제7장 시장 기회와 앞으로의 동향

지속가능성으로의 이동

리사이클 기술의 연구 개발의 진전

적층 조형과 3D 프린팅 분야로부터의 잠재 수요 증가

JHS

영문 목차

영문목차

The Recycled Carbon Fiber Market size is estimated at USD 201.39 million in 2025, and is expected to reach USD 381.84 million by 2030, at a CAGR of 13.65% during the forecast period (2025-2030).

Key Highlights

The market was negatively impacted by COVID-19 in 2020 due to disruption in the supply chain. As the pandemic spread, many manufacturing plants involved in the recycling of carbon fiber globally were shut down due to the strict lockdowns. However, the sector has been recovering since restrictions were lifted owing to increased demand from various end-user industries, such as wind energy.

Over the short term, the rising demand for lightweight vehicles, growing carbon fiber scrap recycling, its increasing reuse in the wind energy sector, and the cost-effectiveness of recycled carbon fiber are some of the factors driving the market demand.

The availability of various substitutes and supply chain security for recycled carbon fiber are the factors hindering the market's growth.

Shifting focus toward sustainability, advancement in research and development for recycling techniques, and increasing potential demand from additive manufacturing and 3D printing sectors are likely to create opportunities for the market in the coming years.

The North American region is expected to dominate the market and is likely to witness the highest CAGR during the forecast period.

Recycled Carbon Fiber Market Trends

Increasing Usage in the Aerospace and Defense Industry

Recycled carbon fiber possesses similar properties to new carbon fiber used for manufacturing composites that are used in the aerospace and defense industry. These carbon fibers offer specific advantages to components used for the aerospace and defense industry, such as durability in harsh conditions and at high temperatures, abrasion resistance, and corrosion resistance.

Recycled carbon fiber has replaced aluminum in aircraft to improve fuel economy. Lightweight materials and structures allow military aircraft to carry more fuel and payload while in commercial aircraft.

Lightweight materials are used to reduce greenhouse gas emissions and the amount of waste sent to landfills. For instance, the Boeing 787 was made 20% lighter, which helped in increasing the fuel economy by nearly 10% to 12%.

Moreover, the preference for recycled carbon fiber is also increasing in the aerospace industry to manage the significant problem of aircraft waste. It is estimated that, in the global aerospace industry, about 6000-8000 aircraft will reach the end of their service life by 2030, which may create a potential source for carbon recycling in the industry.

Airbus has set a target of recycling 95% of its carbon fiber waste by 2020-2025, with 5% recycled back into the aerospace sector. The gross orders of aircraft for airbus were 771 units in 2021, as compared to 383 units in 2020.

The growing passenger volumes and increasing retirements of aircraft are expected to drive the need for 44,040 new jets (valued at USD 6.8 trillion) over the next two decades. The global commercial fleet is expected to reach 50,660 aircraft by 2038, considering all the new aircraft and jets that may remain in service.

According to the International Air Transport Association (IATA), the global revenue for commercial airlines was valued at USD 373 billion in 2020 and was estimated at USD 472 billion in 2021, registering a growth rate of 26.7% Y-o-Y. Furthermore, the revenue was expected to reach USD 658 billion by the end of 2022.

According to Boeing, by 2040, the worldwide commercial fleet will exceed 49,000 planes, with China, Europe, North America, and the Asia-Pacific countries each accounting for around 20% of new plane deliveries and the remaining 20% going to other rising markets.

Owing to all these factors, the market for recycled carbon fiber is likely to grow globally during the forecast period.

The North American Region to Dominate the Market

The North American region is expected to dominate the market. In the region, the United States is the largest economy in terms of GDP. The United States and Canada are among the fastest emerging economies in the world.

The fast-growing automotive and aerospace industries are driving the growth of the market studied in the North American region. Strategic developments, the presence of established car manufacturers, leading recycled carbon fiber manufacturers, and technological advancements related to recycled carbon fiber products all contribute to the market's growth in this region.

The United States is the region's leader in the consumption of recycled carbon fiber, which is used by major corporations. Due to the growing demand for lightweight materials to reduce vehicle weight, the use of recycled carbon fiber in the automotive and aerospace end-use industries has increased in the region.

Moreover, in the United States, according to the Federal Aviation Administration (FAA), the number of aircraft in the country's commercial fleet accounted for 5,882 in 2020, witnessing a decline rate of 22.9% compared to the previous year. However, the commercial fleet is projected to increase to 8,756 in 2041, with an average annual growth rate of 2% per year. This is expected to increase the demand for carbon fiber from multiple applications in the aerospace industry.

In Canada, the country has a Centre de developpement des composites du Quebec (Composite Development Centre of Quebec) (CDCQ) engaged in various activities related to the value chain of various composite materials, including carbon fibers. The center is also actively involved in the recycling of carbon fiber as one of its major activities.

Globally, Canada ranks first in civil flight simulation, third in civil engine production, and fourth in civil aircraft production. It is the only nationally ranked in the top five of all the key categories. The Canadian aerospace industry exports over 70% of its products to over 190 countries across six continents.

Wind energy in Canada accounts for 3.5% of electricity generation, being the region's second most important renewable energy source. Wind energy plays a crucial role in reaching global net-zero carbon emissions. Canada is one of the world leaders in producing and using renewable power due to its diversified geography with hydro, biomass, wind, and solar energy sources.

Due to all such factors, the market for recycled carbon fiber in the region is expected to have steady growth during the forecast period.

Recycled Carbon Fiber Industry Overview

The recycled carbon fiber market is partially consolidated in nature. Some of the major players in the market include Toray Industries Inc., Procotex, Vartega Inc., Gen 2 Carbon Limited, and Sigmatex, among others (not in any particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Rising Demand For Lightweight Vehicles

4.1.2 Growing Carbon Fiber Scrap Recycling and its Reuse in the Wind Energy Sector

4.1.3 Cost Effectiveness of Recycled Carbon Fiber

4.2 Restraints

4.2.1 Availability of Various Substitutes

4.2.2 Supply Chain Security for Recycled Carbon Fiber

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

5.1 Type

5.1.1 Chopped Recycled Carbon Fiber

5.1.2 Milled Recycled Carbon Fiber

5.2 Source

5.2.1 Automotive Scrap

5.2.2 Aerospace Scrap

5.2.3 Other Sources

5.3 End-user Industry

5.3.1 Automotive

5.3.2 Aerospace and Defense

5.3.3 Wind Energy

5.3.4 Sporting Goods

5.3.5 Other End-user Industries

5.4 Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 Italy

5.4.3.4 France

5.4.3.5 Rest of Europe

5.4.4 Rest of the World

5.4.4.1 South America

5.4.4.2 Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Alpha Recyclage Composites

6.4.2 Carbon Conversions

6.4.3 Carbon Fiber Recycling

6.4.4 Carbon Fiber Remanufacturing

6.4.5 Gen 2 Carbon Limited

6.4.6 Karborek RCF

6.4.7 Mitsubishi Chemical Holdings Corporation.

6.4.8 Procotex

6.4.9 Shocker Composites LLC

6.4.10 Sigmatex

6.4.11 Toray Industries Inc.

6.4.12 Vartega Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Shifting Focus Toward Sustainability

7.2 Advancement in Research and Development for Recycling Techniques

7.3 Increasing Potential Demand from Additive Manufacturing and 3D Printing Sectors