ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

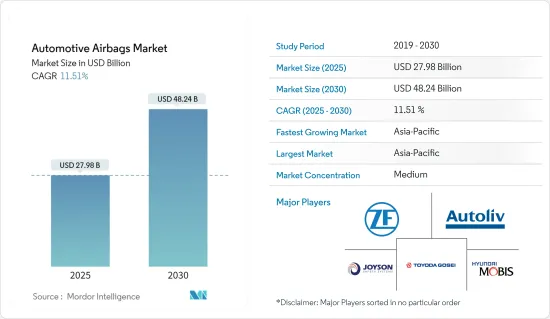

차량용 에어백 시장 규모는 2025년에 279억 8,000만 달러로 추정되고, 2030년에는 482억 4,000만 달러에 달할 것으로 예측되며, 예측기간(2025-2030년)의 CAGR은 11.51%를 나타낼 전망입니다.

장기적으로 차량 판매 및 생산량 증가와 차량 안전 시스템 강화를 위한 정부의 엄격한 규제는 글로벌 차량용 에어백 시장 성장의 주요 결정 요인으로 작용할 것으로 예상됩니다. 또한 소비자와 당국 사이에서 안전에 대한 인식이 높아지면서 도로에서의 안전이 개선되고 사고 사망자가 감소하는 등 상당한 발전이 이루어질 것으로 예상됩니다.

주요 하이라이트

국제자동차제조업협회(OICA)에 따르면 전 세계 경상용차 신차 판매량은 2021년 1,860만 대에 비해 2022년에는 1,980만 대를 기록하여 2021년과 2022년 사이에 전년 대비 7%의 큰 성장률을 기록할 것으로 예상됩니다.

마찬가지로 전 세계 버스 및 코치 차량 생산량은 2021년의 19만 8,500대에 대해, 2022년에는 25만 3,100대에 달하고, 2021년부터 2022년에 걸쳐 전년대비 28%의 성장을 기록했습니다.

또한 선진국에서 프리미엄 및 고급 자동차 제조업체들이 향상된 기능을 갖춘 신제품 생산에 집중하면서 전 세계적으로 차량용 에어백에 대한 수요가 더욱 증가하고 있습니다. 소비자들 사이에서 도로 안전에 대한 인식이 높아지고 정부 규제가 강화됨에 따라 주문자 상표 부착 생산(OEM) 업체들은 측면 창문을 덮는 커튼 에어백을 통합하는 새로운 모델 구조 설계에 주력하고 있습니다.

그러나 업계가 직면한 주요 과제 중 하나는 승용차 및 상용차에 장착된 에어백 결함으로 인한 차량 리콜이며, 이는 자동차 제조업체의 브랜드 가치에 부정적인 영향을 미쳐 비즈니스 성과에 영향을 미칩니다.

주요 하이라이트

기아차는 2023년 12월 미국에서 용접 오류로 인해 디퓨저 디스크가 파손되어 경고나 전개 명령 없이 커튼 에어백이 팽창하는 문제로 2023년형 셀토스를 리콜했습니다. 미국 도로교통안전국(NHTSA)의 보고서에 따르면 측면 커튼 에어백 모듈의 총 4개 부품 번호에 문제가 있었으며, 셀토스 크로스오버 1,367대에 영향을 미쳤습니다.

22023년 5월, 약 9만 대의 BMW 차량에서 타카타 운전석 에어백 인플레이터 시스템 결함으로 인해 “운전 금지” 경고가 보고되었습니다. 결함이 있는 사이드 에어백이 장착된 구형 BMW 모델의 경우, 에어백이 터질 경우 파편이 앞좌석 승객 방향으로 실내로 날아가 운전자와 다른 승객에게 심각한 위험을 초래할 수 있다는 것이 회사 측의 설명입니다.

아시이평양 지역이 시장 성장에 기여하는 주요 지역이 될 것으로 예상되며, 유럽과 북미가 그 뒤를 이을 것으로 전망됩니다. 일본과 한국은 안전 규범과 확고한 정부 규제로 인해 매출 성장에 크게 기여할 것으로 예상됩니다. 중국은 심각한 사고의 증가와 차량의 확대로 인해 에어백 수요에 크게 기여하는 주요 국가 중 하나로 부상할 것으로 예상됩니다. 또한 신에너지 차량에 대한 소비자의 선호로 인해 자동차 제조업체들이 차량의 전기화 전략을 점진적으로 전환하고 있으며, 이는 향후 차량용 에어백 시스템에 대한 수요에 긍정적인 영향을 미칠 것으로 예상됩니다.

차량용 에어백 시장 동향

예측 기간 동안 승용차 부문이 견인 역할

승용차 판매는 폭스바겐, 닛산, 제너럴 모터스, 포드 등 주요 자동차 브랜드를 중심으로 전 세계적으로 엄청난 성장세를 보이고 있습니다.

국제 자동차 제조업체 협회(OICA)에 따르면 전 세계 승용차 신차 판매량은 2021년 5,640만 대에서 2022년 5,740만 대를 기록해 2021년과 2022년 사이에 전년 대비 1.9%의 성장률을 기록할 것으로 예상됩니다.

도시화율이 높아지고 소비자의 1인당 가처분 소득이 증가함에 따라 통근용으로 개인 교통수단을 선호하는 소비자가 늘어나면서 승용차 수요가 증가하고 있습니다. 승객의 안전은 정부와 제조업체에게 가장 중요한 요소입니다. 소비자 안전과 보안에 대한 규제로 인해 제조업체는 자동차에 안전 장치를 설치하게 되었습니다. 많은 국가에서 안전벨트와 에어백 사용을 의무화하고 있습니다. 또한 제조업체는 브랜드 인지도를 높이기 위해 주요 자동차 제조업체와 파트너십을 맺는 데 적극적으로 주력하고 있습니다.

22023년 5월, 중국의 고성능 전기자동차 제조업체인 NIO는 차량용 에어백 및 안전벨트 제조업체인 오토리브와 전기차용 안전 제품 제조를 위한 협약을 체결했습니다.

세계적으로 자동차 생산 및 판매가 증가함에 따라 자동차 승객 안전 당국은 승객 부상을 줄이기 위해 다양한 안전 규정을 채택하고 있습니다.

예를 들어, 2023년 10월 인도 도로교통부와 고속도로부는 승용차에 6개의 에어백 장착을 의무화했습니다. 이 규정은 더 안전한 도로 여행을 위해 8인승 승용차에도 적용될 예정입니다. 글로벌 공급망의 어려움으로 인해 이 규정은 2023년 10월부터 시행될 예정입니다.

전기 승용차 판매가 증가하고 생산 시장이 확대됨에 따라 예측 기간 동안 승용차용 차량용 에어백 시스템에 대한 막대한 수요가 예상됩니다.

아시이평양 지역은 예측 기간 동안 가장 빠르게 성장하는 시장이 될 것으로 예상

아시이평양 지역은 시장에서 가장 빠르게 성장하는 지역이 될 것으로 예상되며 북미와 유럽이 그 뒤를 이을 것으로 예상됩니다.

전기자동차제조협회에 따르면 전기 사륜차 판매량은 2022년도의 1만 9,782대에 대해, 2023년도는 4만 8,105대에 이르고, 2022년도와 2023년도의 전년대비 성장률은 143.1%입니다.

일본 자동차 판매 협회 연합회에 따르면, 2023년 10월의 국내 신차 시장은 2022년 10월의 35만 9,159대에서 10.7% 증가한 39만 7,672대로 크게 회복했습니다.

안전 및 편의 기능에 대한 소비자 선호도 증가, 중형 차량의 사이드 및 커튼 에어백 보급률 증가, 차량 내 안전 기능에 대한 수요 증가가 아시이평양 지역의 승용차 및 상용차에서 첨단 안전 기능이 성장하는 주요 원인으로 꼽힙니다. 또한 승객 안전을 개선하려는 정부의 노력과 시스템 및 부품 비용 하락으로 인해 예측 기간 동안 에어백에 대한 수요가 증가할 것으로 예상됩니다.

게다가 이 지역의 각국 정부는 교통 사고와 사망자 수를 줄이는 데 주력하고 있어 차량용 에어백 시스템에 대한 수요를 촉진하고 있습니다.

인도 정부에 따르면 2022년 인도에서 461,312건의 교통사고가 발생하여 168,491명이 사망하고 443,366명이 부상을 입었으며, 이는 에어백에 대한 수요가 증가하고 있음을 시사합니다.

주요 자동차 제조업체들이 중국과 인도와 같은 국가에서 사업을 확장하고 새로운 차량 모델을 출시할 전략을 세우고 있기 때문에 예측 기간 동안 아시이평양 지역에서 차량용 에어백 시스템에 대한 엄청난 수요가 발생할 것으로 예상됩니다.

차량용 에어백 산업 개요

차량용 에어백 시장은 고도로 통합되어 있고 경쟁이 치열합니다. 소수의 업체가 대부분의 시장 점유율을 차지하고 있습니다. 주요 업체로는 ZF Friedrichshafen AG, Autoliv Inc., Toyoda Gosei Co. Ltd, Joyson Safety Systems, Hyundai Mobis Co. Ltd, Continental AG, Sumitomo Corporation, Ashimori Industry Co. Ltd,등이 있습니다.

2023년 7월, ZF 그룹은 중국 중부 후베이성에 위치한 우한 경제개발구(WEDZ)와 자동차 에어백 생산 및 개발에 중점을 둔 신규 시설에 투자하기로 최종 합의했습니다. 이 시설은 ZF 우한 자동차 안전 시스템(우한) 유한공사로 명명될 예정입니다.

2023년 6월, 오토리브는 유체의 속도가 빨라질수록 정압이 감소하여 에어백의 팽창 과정에 주변 공기가 크게 유입된다는 베르누이 원리에 기반한 새로운 에어백 기술을 공개했습니다. 선구적인 '베르누이 에어백'은 미국 미시간주 오번힐스에서 열린 오토리브의 투자자의 날 행사에서 선보였습니다.

자동차 에어백 모듈 시장은 경쟁업체들이 경쟁 우위를 확보하기 위한 전략을 세우면서 빠르게 발전할 것으로 예상됩니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 성장 촉진요인

성장 촉진을위한 승용차 및 상용차 판매 증가

시장 성장 억제요인

에어백 오작동 및 리콜로 성장 저해

업계의 매력 - Porter's Five Forces 분석

신규 참가업체의 위협

구매자 및 소비자의 협상력

공급기업의 협상력

대체품의 위협

경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

자동차 부문별

승용차

상용차

부문별

전면 에어백

풍선 안전 벨트

커튼 에어백

사이드 에어백

무릎 에어백

판매 채널별

주문자 상표 부착 생산(OEM)

교환 및 애프터마켓

지역별

북미

미국

캐나다

기타 북미

유럽

독일

영국

프랑스

스페인

기타 유럽

아시이평양

중국

인도

일본

한국

기타 아시이평양

세계 기타 지역

남미

중동 및 아프리카

제6장 경쟁 구도

벤더의 시장 점유율

기업 프로파일

ZF Friedrichshafen AG

Autoliv Inc.

Yanfeng(Huayu Automotive Systems Co. Ltd)

Toyoda Gosei Co. Ltd

Continental AG

Joyson Safety Systems

현대모비스 주식회사 Ltd

Sumitomo Corporation

Jinzhou Jinheng Automotive Safety System Co. Ltd

Ashimori Industry Co. Ltd

제7장 시장 기회와 앞으로의 동향

자동차 안전 시스템 강화를 위한 정부의 적극적인 추진이 시장 수요를 촉진

제8장 공급자 정보

HBR

영문 목차

영문목차

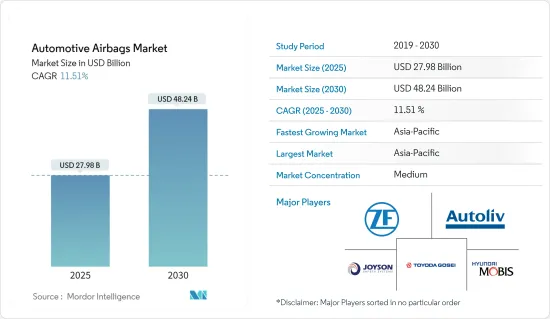

The Automotive Airbags Market size is estimated at USD 27.98 billion in 2025, and is expected to reach USD 48.24 billion by 2030, at a CAGR of 11.51% during the forecast period (2025-2030).

Over the long term, the increasing vehicle sales and production, coupled with the government's stringent regulations to enhance the safety system of vehicles, is expected to serve as the major determinant for the growth of the global automotive airbags market. The increasing awareness about safety among consumers and authorities is also anticipated to lead to significant developments, resulting in improved security and reduced accident fatalities on the road. With further technological advancements, the market is expecting even safer and more reliable airbag modules in cars and commercial vehicles.

Key Highlights

According to the International Organization of Motor Vehicle Manufacturers (OICA), new light commercial vehicle sales touched 19.8 million units in 2022 compared to 18.6 million units in 2021 worldwide, recording a substantial Y-o-Y growth of 7% between 2021 and 2022.

Similarly, bus and coach production worldwide reached 253.1 thousand units in 2022 compared to 198.5 thousand units in 2021, recording a Y-o-Y growth of 28% between 2021 and 2022.

In addition, the growing focus by premium and luxury car manufacturers on manufacturing new products with enhanced features in developed countries is further fostering the demand for automotive airbags worldwide. With growing awareness of road safety among consumers and a push from government regulations, original equipment manufacturers (OEM) are focusing on designing their new model structures to incorporate curtain airbags covering the side windows.

However, one of the major challenges faced by the industry is vehicle recalls due to faulty airbags being incorporated in cars and commercial vehicles, which negatively impacts the brand value of automakers, affecting their business performance.

Key Highlights

In December 2023, Kia recalled the 2023 Seltos in the United States due to a welding error, causing the diffuser disk to break, resulting in the curtain airbags inflating without warning or deployment command. As per the National Highway Traffic Safety Administration (NHTSA) report, a total of 4-part numbers for the side curtain airbag modules had the issue, affecting 1,367 units of the Seltos crossover.

In May 2023, a major "do not drive" warning was reported for nearly 90,000 BMW vehicles due to a faulty Takata driver-side airbag inflator system. The company stated that the older models of BMW fitted with faulty side airbags could send shrapnel flying into the cabin, in the direction of the front passengers, if nudged, which can pose a serious risk to drivers and other passengers.

Asia-Pacific is anticipated to be a major region contributing to the market's growth, followed by Europe and North America. Japan and South Korea are expected to contribute significantly to the growth in terms of revenue due to safety norms and firm government regulations. Due to an increase in the number of serious accidents and an expanded fleet, China is expected to emerge as one of the major countries that contribute significantly to the demand for airbags. Moreover, the preference of consumers toward new-energy vehicles is witnessing a gradual shift in automakers strategizing to electrify their vehicle fleets, which is expected to positively influence the demand for automotive airbag systems in the coming years.

Automotive Airbags Market Trends

Passengers Cars Segment to Gain Traction during the Forecast Period

Passenger car sales are witnessing tremendous growth globally, with leading car brands including Volkswagen, Nissan, General Motors, and Ford. With the expanding passenger car market, there exist rising safety concerns among automakers to ensure that their vehicle models can provide all necessary safety solutions that can mitigate road fatalities, which is positively impacting the surging demand for automotive airbag systems.

According to the International Organization of Motor Vehicle Manufacturers (OICA), new passenger car sales worldwide touched 57.4 million units in 2022 compared to 56.4 million units in 2021, representing a year-on-year growth of 1.9% between 2021 and 2022.

The rising urbanization rate and increasing per capita disposable income of consumers are aiding the demand for passenger cars as these consumers prefer private transportation mediums for their commuting purposes. Passenger safety is of utmost importance to governments and manufacturers. Regulations toward consumer safety and security have made manufacturers install safety devices in cars. Many countries have made using seat belts and airbags mandatory. Moreover, manufacturers are actively focusing on forming partnerships with major automakers to enhance their brand presence. They are introducing new products that can suit the requirements of new-age passenger cars.

In May 2023, NIO, a Chinese-based high-performance electric vehicle manufacturer, reached an agreement with Autoliv Inc., the leading manufacturer of automotive airbags and seat belts, to manufacture safety products for electric vehicles. This development of safety technologies will increase the demand for inflatable seat belts, as airbag deployment works only when the seat belts are intact.

With the rising automobile vehicle production and sales worldwide, the automotive passenger safety authorities are adopting various safety regulations to reduce passenger injuries.

For instance, in October 2023, the Ministry of Road Transport and Highways India made six airbags mandatory for automotive passenger vehicles. This rule will apply to eight-seater passenger cars to make road travel safer. Due to the challenges faced in the global supply chain, this rule has been in effect since October 2023. Initially, the Indian government officials wanted to roll it out in October 2022.

With the growth in electric passenger car sales and the expanding production market, a massive demand for automotive airbag systems for passenger cars is projected during the forecast period.

Asia-Pacific Region is Expected to be Fastest-Growing Market During Forecast Period

Asia-Pacific is expected to be the fastest-growing region in the market, followed by North America and Europe. Asia-Pacific is a huge market for passenger vehicles, with India and China being some of the world's largest markets for passenger vehicles, contributing to almost 30% of worldwide passenger vehicle sales.

According to the Society of Manufacturers of Electric Vehicles, electric four-wheeler sales touched 48,105 units in FY 2023 compared to 19,782 units in FY 2022, representing a Y-o-Y growth of 143.1% between FY 2022 and FY 2023.

According to the Japan Automobile Dealers Association, in October 2023, the new vehicle market in Japan made a strong recovery, with sales rising by 10.7% to 397,672 units from 359,159 units in October 2022. In January 2024, mini vehicle sales in Japan touched 334 thousand units.

The increased consumer preference for safety and comfort features, the increased penetration of side and curtain airbags in mid-level cars, and the rising demand for safety features in vehicles are primarily responsible for the growth of advanced safety in passenger cars and commercial vehicles in Asia-Pacific. The demand for airbags is also anticipated to increase over the forecast period due to government initiatives to improve passenger safety and falling system and component costs.

Furthermore, governments in the region are increasing their focus on reducing road accidents and fatalities, fueling the demand for automotive airbag systems. Airbags are crucial in any vehicle to mitigate the impact of an accident, and therefore, integrating advanced airbag modules is a necessity that can enhance road safety in the region.

According to the Indian government, 461,312 road accidents were reported in the country in 2022, resulting in 168,491 fatalities and injuries to 443,366 individuals, suggesting a growing need for airbags.

With major automakers strategizing to expand their operations and launch new vehicle models in countries such as China and India, a massive demand for automotive airbag systems across Asia-Pacific is expected during the forecast period.

Automotive Airbags Industry Overview

The automotive airbags market is highly consolidated and competitive. A few players capture most of the market share. Some of the major players include ZF Friedrichshafen AG, Autoliv Inc., Toyoda Gosei Co. Ltd, Joyson Safety Systems, Hyundai Mobis Co. Ltd, Continental AG, Sumitomo Corporation, and Ashimori Industry Co. Ltd, among others. These players are investing hefty sums in research and development to constantly manufacture innovative airbag solutions that can enhance the safety of drivers. For instance,

In July 2023, ZF Group finalized a deal with the Wuhan Economic Development Zone (WEDZ) located in Hubei province, central China, to invest in a new facility focused on producing and developing automotive airbags. The establishment will be known as ZF Wuhan Automotive Safety Systems (Wuhan) Co. Ltd. Once operational, this center is projected to achieve a maximum yearly production value of approximately CNY 3 billion (USD 4,200 million)

In June 2023, Autoliv unveiled its new airbag technology based on the Bernoulli Principle, which states that, as the speed of a fluid increases, the static pressure decreases, which assists in significantly incorporating surrounding air into the airbag's inflation process. The pioneering 'Bernoulli airbag' was showcased at Autoliv's Investor Day in Auburn Hills, Michigan, United States.

The market is anticipated to witness rapid enhancement in automotive airbag modules as competitors strategize to gain a competitive edge. Major players seek to form long-term partnerships with automakers to boost their profitability prospects.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Drivers

4.1.1 Increasing Passenger and Commercial Vehicle Sales to Foster Growth

4.2 Market Restraints

4.2.1 Airbag Malfunction and Recall Deters Growth

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Threat of New Entrants

4.3.2 Bargaining Power of Buyers/Consumers

4.3.3 Bargaining Power of Suppliers

4.3.4 Threat of Substitute Products

4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value - USD)

5.1 By Vehicle Type

5.1.1 Passenger Cars

5.1.2 Commercial Vehicles

5.2 By Type

5.2.1 Front Airbags

5.2.2 Inflatable Seat Belts

5.2.3 Curtain Airbags

5.2.4 Side Airbags

5.2.5 Knee Airbags

5.3 By Sales Channel

5.3.1 Original Equipment Manufacturer (OEM)

5.3.2 Replacement/Aftermarket

5.4 By Geography

5.4.1 North America

5.4.1.1 United States

5.4.1.2 Canada

5.4.1.3 Rest of North America

5.4.2 Europe

5.4.2.1 Germany

5.4.2.2 United Kingdom

5.4.2.3 France

5.4.2.4 Spain

5.4.2.5 Rest of Europe

5.4.3 Asia-Pacific

5.4.3.1 China

5.4.3.2 India

5.4.3.3 Japan

5.4.3.4 South Korea

5.4.3.5 Rest of Asia-Pacific

5.4.4 Rest of the World

5.4.4.1 South America

5.4.4.2 Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Vendor Market Share

6.2 Company Profiles

6.2.1 ZF Friedrichshafen AG

6.2.2 Autoliv Inc.

6.2.3 Yanfeng (Huayu Automotive Systems Co. Ltd)

6.2.4 Toyoda Gosei Co. Ltd

6.2.5 Continental AG

6.2.6 Joyson Safety Systems

6.2.7 Hyundai Mobis Co. Ltd

6.2.8 Sumitomo Corporation

6.2.9 Jinzhou Jinheng Automotive Safety System Co. Ltd

6.2.10 Ashimori Industry Co. Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Government's Aggressive Push to Enhance Vehicle Safety Systems to Propel the Market Demand