중동 및 아프리카의 연포장 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)

Middle East And Africa Flexible Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1692157

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

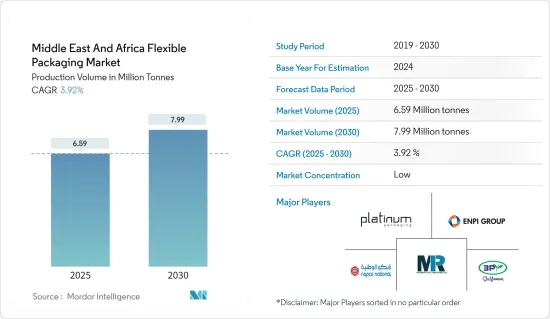

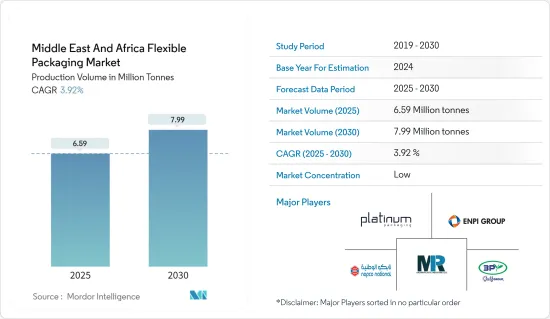

중동 및 아프리카의 연포장 시장 규모는 생산량 기준으로 2025년 659만톤, 2030년 799만톤으로 확대될 전망입니다. 예측기간(2025-2030년)의 CAGR은 3.92%를 나타낼 전망입니다.

부드러운 포장은 보다 경제적이고 맞춤화 가능한 제품 포장 옵션을 가능하게합니다. 식품, 퍼스널케어, 제약 산업 등 다재 다능한 포장이 필요한 업계에서 특히 유용합니다. 연포장은 높은 효율성과 비용 효율성으로 인기가 높아지고 있습니다.

주요 하이라이트

이 지역의 포장 사업은 소비자의 기대 변화와 인구 증가로 지난 10년간 일관된 성장을 이루었습니다. 이 지역에서는 포장재료에서 다양한 혁신을 볼 수 있기 때문에 지속가능성과 환경적 측면이 계속 중시될 수 있습니다. 종이 및 골판지, 재생 PET(rPET), 바이오플라스틱 등 재활용 가능하고 지속 가능한 포장재에 대한 수요 증가가 시장 성장을 뒷받침하고 있습니다.

게다가 아랍에미리트(UAE)에서 소비자 음식의 선호도의 변화는 특히 식품 및 식품 산업에 있어서 포장 산업에 큰 성장 기회를 가져왔습니다. 아랍에미리트(UAE) 금융기관 Alpen Capital의 보고서에 따르면 중동 및 아프리카의 식품 산업은 전략적 입지와 인구 증가로 성장할 것으로 추정됩니다. 유행 후 온라인 식품 택배의 급증은 랩, 슬리브, 라벨 등의 연포장 수요를 높여 업계의 성장을 이끌고 있습니다.

게다가 국내 소비자들 사이에서 서양 식습관의 영향이 강해지고 있는 것도 포장식품 수요를 끌어올리고 있습니다. 이 동향은 또한 이민자, 여행자, 젊은 소비자가 조리된 식품, 가공 식품, 냉동 식품에 대한 수요를 견인하고 있습니다.

스탠드 업 파우치는 경질 포장보다 가볍고 재료 사용량이 적고 운송 비용이 낮기 때문에 포장 식품 제조업체에 이익을줍니다. 이 지역에서는 음료 산업에 의한 파우치 소비가 증가하고 있으며, 이 시장 수요는 증가할 것으로 예상됩니다.

중동은 리사이클 인프라가 제한되어 있기 때문에 연포장 업계에서는 큰 과제에 직면하고 있습니다. 이 문제는 지속가능성에 대한 우려가 세계적으로 그리고 이 지역 내에서도 증가함에 따라 점점 더 두드러지고 있습니다. 환경문제에 대한 인식이 높아지고, 재활용과 폐기물 감축을 촉진하기 위한 다양한 정부 이니셔티브가 시행되고 있음에도 불구하고, 적절한 재활용 시설과 시스템의 필요성은 여전히 큰 장애물이 되고 있습니다. 이러한 상황은 이 지역의 유연한 패키징 제조업체와 사용자에게 복잡한 역학을 창출하고 시장 수요와 새로운 지속가능성 요구사항의 균형을 맞추려고 노력하고 있습니다.

중동 및 아프리카 연포장 시장 동향

식품 산업이 가장 큰 최종 사용자에게

중동 패키지 식품 시장은 식품 가공 기술의 선진화와 소비자의 라이프 스타일 변화로 인해 성장하고 있습니다. 이러한 요인은 제품 수요를 증가시키고 예측 기간 동안 연포장의 성장을 가속할 것으로 예상됩니다.

게다가 중동 인구 증가와 고기, 해산물, 닭고기에 대한 식욕 증가가 연질 플라스틱 포장 수요를 부추기고 있습니다. 제조업체가 편의성과 보존 기간 연장을 요구하는 소비자의 선호도에 부응하려고 노력하고 있기 때문에 포장재료와 디자인 혁신도 이러한 동향에 기여하고 있습니다.

또한 아랍에미리트(UAE)와 사우디아라비아와 같은 중동 국가에서 전자상거래 성장이 편의점 수요를 촉진하고 있습니다. 이 동향은 식품의 신선도와 보온성을 장기간 유지하는데 도움이 되는 필름, 랩, 파우치, 가방 등의 연포장을 둘러싼 환경을 재구성하고 있습니다.

중동 및 아프리카의 주요 덩어리인 GCC 지역의 식품 산업은 유행 후에 회복되었습니다. 인구 증가와 더불어 사회인 증가와 많은 해외 주재원 증가가 이 지역의 식품업계를 견인하고 있습니다. 높은 영양가를 요구하는 이 지역 소비자의 건강한 식습관에 대한 의식이 높아지면 신선한 식품과 유기농 식품에 대한 수요가 증가하고 있습니다. 파우치는 무게와 강도가 낮기 때문에 식품 포장에 플라스틱 가방이나 파우치를 사용하면 연질 플라스틱 포장 수요를 견인하고 있습니다.

알펜 캐피탈의 보고서에 따르면 GCC 국가의 식품 소비량은 1인당 소득 증가와 인구 증가로 견인되었으며, 2027년에는 5620만 톤으로 성장할 것으로 추정됩니다. 식량 소비량에서는 사우디아라비아가 이 지역 최대의 나라로, 아랍 에미리트 연합과 바레인이 이에 따른다고 추정됩니다.

사우디아라비아가 주요 시장 점유율을 차지

사우디아라비아는 3개의 대륙이 교차하는 전략적 위치에 있기 때문에 중동, 아프리카, 아시아 시장에 중요한 액세스 포인트가 되고 있습니다. 사우디아라비아의 정비된 인프라, 효율적인 교통망, 고급 물류 시설은 세계 무역 및 투자 기회에 큰 이점을 제공합니다.

사우디아라비아는 새로운 기회와 성장을 요구하는 기업들에게 매력적인 진출지로 자리매김하고 있습니다. 사우디아라비아의 야심찬 경제 개혁, 전략적 이니셔티브, 진화하는 비즈니스 환경은 사우디아라비아를 잠재적인 세계 비즈니스의 중심지로 바꾸고 있습니다. 이 변모는 국제 시장에서 사우디아라비아의 중요성 증가를 반영하여 세계 포장 사업에서 점점 더 주목을 받고 있습니다.

식품, 소매, 소비재, 의약품 등의 분야에서 연포장 솔루션 수요가 높아지는 가운데 사우디아라비아에 주목하는 기업이 늘고 있습니다. 사우디아라비아는 그 전략적 위치에 따라 지역 및 국제 무역, 투자, 혁신의 형성에 중요한 역할을 할 것입니다.

조리된 식품(Ready-to-Eat Meals) 및 냉동식품(Frozen Food) 분야는 소비 전에 최소한의 준비만 필요하거나 준비할 필요가 없는 조리된 식품을 제공합니다. 이 부문은 속도가 빠른 도시의 라이프 스타일과 다양한 문화의 영향으로 중동 국가, 특히 사우디아라비아에서 인기를 얻고 있습니다.

사우디아라비아의 가공 고기, 해산물, 대체 고기 시장은 성장하고 있습니다. 2023년 시장 규모는 약 1,499.10톤이었습니다. 2027년에는 약 1,839.50톤으로 증가할 것으로 예상되지만, 이는 가공육에 대한 소비자의 기호의 변화와 증가를 반영합니다.

중동 및 아프리카의 연포장 산업 개요

중동 및 아프리카의 연포장 시장은 단편화되어 있어 여러 기업이 지역별로 사업을 전개하고 있습니다. 경쟁도는 브랜드 아이덴티티, 강력한 경쟁 전략, 투명성의 정도, 기업 집중률 등 시장에 영향을 미치는 다양한 요인에 의해 결정됩니다. 시장의 주요 기업으로는 Napco National, 3P Gulf Group, Platinum Packaging Ltd, Aalmir Plastic Industries LLC, ENPI Group 등이 있습니다.

2024년6월 - 지속 가능한 패키징 솔루션의 주요 기업 인 Fultamaki는 아랍 에미리트 연합(UAE)의 유연한 패키징 제조 사업을 통합 할 계획을 발표했습니다. 이 전략은 제벨 알리의 시설을 유지하면서 라스 알하이마의 시설을 크게 확장합니다. 회사에 따르면 이 움직임은 업무를 간소화하고 경쟁력을 높이고 향후 지역 확대에 대한 발판을 강화하는 것을 목표로 하고 있습니다.

2024년 5월 - Napco National은 아랍에미리트(UAE)에 본사를 둔 브랜드 Alsharq Plas LLC를 전략적으로 인수하고 포장 부문을 확대했습니다. 인수 후 Alsharq Plas LLC 브랜드는 Napco Sharq Plas LLC로 변경됩니다. 이 움직임은 GCC 지역의 고객의 첨단 수요에 대응하는 양사의 능력을 강화하는 것입니다. 게다가 이 인수는 Napco National 시장에서의 존재감을 높일 것으로 기대됩니다.

The Middle East And Africa Flexible Packaging Market size in terms of production volume is expected to grow from 6.59 million tonnes in 2025 to 7.99 million tonnes by 2030, at a CAGR of 3.92% during the forecast period (2025-2030).

Flexible packaging allows more economical and customizable options for packaging products. It is particularly useful in industries requiring versatile packaging, including food and beverage, personal care, and pharmaceutical industries. Flexible packaging has grown popular due to its high efficiency and cost-effectiveness.

Key Highlights

The packaging business in the region has experienced consistent growth over the last decade due to changing consumer expectations and a rising population. Sustainability and environmental aspects might continue to be emphasized in the region as the market is witnessing various innovations in packaging materials. Increased demand for recyclable and sustainable packaging materials, such as paper and cardboard, recycled PET (rPET), and bioplastics, are driving market growth.

Moreover, the changing consumer food preferences in the United Arab Emirates have created significant growth opportunities in the packaging industry, especially for the food and beverage industry. According to a report by Alpen Capital, a financial institute in the United Arab Emirates, the food industry in the Middle East and African region is estimated to grow due to its strategic location and growing population. Post-pandemic, the surge in online food delivery has enhanced the demand for flexible packaging such as wraps, sleeves, labels, and others, driving industry growth.

Additionally, the increasing influence of Western eating habits among domestic consumers has boosted the demand for packaged foods. This trend is further supported by immigrants, tourists, and young consumers driving the demand for ready-to-eat, processed, and frozen foods.

The lighter weight, reduced material use, and lower shipping cost of stand-up pouches than the rigid packaging benefit the packaged food producers. With the beverage industry increasingly consuming pouches in the region, the demand from the market is expected to increase.

The Middle East faces significant challenges in the flexible packaging industry due to its limited recycling infrastructure. This issue has become increasingly prominent as sustainability concerns gain traction globally and within the region. Despite growing awareness of the environmental problems and implementing various government initiatives to promote recycling and waste reduction, the need for adequate recycling facilities and systems continues to pose a substantial obstacle. This situation creates a complex dynamic for flexible packaging manufacturers and users in the region as they strive to balance market demands with emerging sustainability requirements.

Middle East and Africa Flexible Packaging Market Trends

Food Industry to be the Largest End User

The Middle East packaged food market is experiencing growth due to advancements in food processing techniques and changing consumer lifestyles. These factors are expected to increase product demand, driving the growth of flexible packaging during the forecast period.

Further, the rising Middle Eastern population and a growing appetite for meat, seafood, and poultry fuel the demand for flexible plastic packaging. Innovations in packaging materials and designs also contribute to this trend, as manufacturers seek to meet consumer preferences for convenience and extended shelf life.

In addition, the growth of e-commerce in Middle Eastern countries, such as the United Arab Emirates and Saudi Arabia, is driving demand for convenience food. This trend is reshaping the flexible packaging landscape, including films, wraps, pouches, and bags, which help maintain food freshness and warmth for extended periods.

The food industry in the GCC region, a major chunk of Middle East and Africa, recovered after the pandemic. The growing population, coupled with the increasing number of working professionals and many expatriates, is a major driver for the region's food industry. Growing awareness of healthy eating habits of consumers in the region seeking high nutritional value has led to rising demand for fresh and organic food items. The use of plastic bags and pouches for food packaging, as pouches are low in weight and strength, drives the demand for flexible plastic packaging.

According to a report by Alpen Capital, food consumption in GCC countries is estimated to grow to 56.2 million metric tons in 2027, driven by the increase in per capita income and growing population. Saudi Arabia is estimated to be the largest country in the region in terms of food consumption, followed by the United Arab Emirates and Bahrain.

Saudi Arabia Holds Major Market Share

Saudi Arabia's strategic location at the intersection of three continents positions it as a critical access point to markets in the Middle East, Africa, and Asia. The country's well-developed infrastructure, efficient transportation networks, and advanced logistics facilities provide significant advantages for global trade and investment opportunities.

Saudi Arabia has positioned itself as an attractive destination for businesses seeking new opportunities and growth. The Kingdom's ambitious economic reforms, strategic initiatives, and evolving business landscape transform it into a potential global business center. This transformation has garnered increasing attention from packaging businesses worldwide, reflecting Saudi Arabia's growing importance in the international market.

With the demand for flexible packaging solutions rising in sectors like food, retail, consumer goods, and pharmaceuticals, businesses are increasingly eyeing Saudi Arabia. The country's strategic positioning will make it a key player in shaping regional and international trade, investment, and innovation.

The Ready-to-Eat Meals and Frozen Food segment offers prepared food that requires minimal or no preparation before consumption. This segment is gaining popularity in Middle Eastern countries, particularly in Saudi Arabia, due to the fast-paced urban lifestyle and diverse cultural influences.

The Saudi Arabian market for processed meat, seafood, and meat alternatives is experiencing growth. In 2023, the market volume was approximately 1,499.10 metric tons. Projections indicate an increase to about 1,839.50 metric tons by 2027, reflecting the country's changing and growing consumer preferences for processed meat.

Middle East and Africa Flexible Packaging Industry Overview

The Middle East and Africa Flexible Packaging Market are fragmented, with multiple players in the market operating regionally. The degree of competition depends on various factors affecting the market, such as brand identity, powerful competitive strategy, degree of transparency, and firm concentration ratio. Some of the major players in the market are Napco National, 3P Gulf Group, Platinum Packaging Ltd, Aalmir Plastic Industries LLC, and ENPI Group, among others.

June 2024 - Huhtamaki, a key player in sustainable packaging solutions, has revealed plans to consolidate its Flexible Packaging manufacturing operations in the United Arab Emirates (UAE). The strategy involves retaining its Jebel Ali facility while significantly enlarging its Ras Al Khaimah site. According to the company, this move aims to streamline operations, elevate competitiveness, and fortify its foothold for future regional expansion.

May 2024 - Napco National expanded its packaging division by strategically acquiring Alsharq Plas LLC, a brand based in the United Arab Emirates. Post-acquisition, Alsharq Plas LLC will be rebranded as Napco Sharq Plas LLC. This move is poised to bolster both companies' capabilities in meeting the increasingly sophisticated demands of customers in the GCC region. Furthermore, the acquisition is expected to bolster Napco National's market presence.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Ecosystem Analysis Suppliers, Material Manufacturers, etc.

4.3 Industry Attractiveness - Porter's Five Forces Analysis

4.3.1 Bargaining Power of Suppliers

4.3.2 Bargaining Power of Buyers

4.3.3 Threat of New Entrants

4.3.4 Intensity of Competitive Rivalry

4.3.5 Threat of Substitute Products

4.4 Import-Export Analysis

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Steady Rise in Demand for Processing Food

5.2 Market Restraints

5.2.1 High Raw Material Costs and Limited Recycling Infrastructure

5.3 Market Opportunities

5.3.1 Growing Demand for Sustainable Packaging Solution