ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

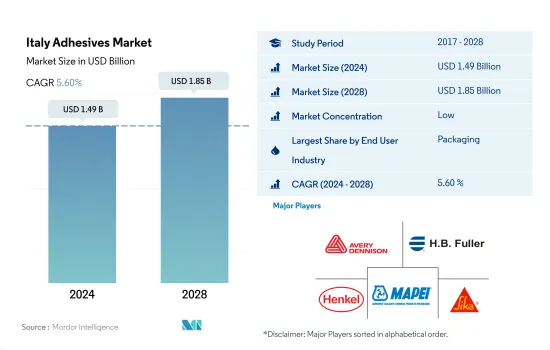

이탈리아의 접착제 시장 규모는 2024년에 14억 9,000만 달러로 추정되고, 2028년에는 18억 5,000만 달러에 이를것으로 예측되며, 예측 기간중(2024-2028년)에 CAGR 5.60%로 성장할 전망입니다.

이탈리아의 신흥 가구 시장과 연포장 트렌드 변화로 접착제 소비 증가 예상

접착제는 산업 전반에 걸쳐 사용되는 다양한 피착재를 접착하고 결합하는 데 중요한 역할을 합니다.

이 국가에서는 포장 부문이 현저한 성장을 이루고 있습니다. 포장 산업에는 전자, 소비재, 의료 및 식품 산업을 위한 콜드 체인 솔루션 및 운송 포장과 같은 특정 응용 분야가 있습니다. 이탈리아의 포장 산업은 유럽에서 가장 큰 산업 중 하나입니다. 이탈리아에는 약 7,000개의 크고 작은 포장 회사가 활동하고 있습니다.

이탈리아는 전 세계적으로 인기 있는 이탈리아 가구로 유명합니다. 따라서 이탈리아의 목공 산업에서 접착제가 주로 소비됩니다.

이탈리아에서 연포장 및 주택 개조가 증가하는 추세로 인해 향후 몇 년 동안 이탈리아에서 접착제 수요가 증가할 것으로 예상됩니다.

이탈리아의 접착제 시장 동향

이탈리아의 저렴하고 가벼운 포장 트렌드 증가로 유연하고 경질 플라스틱 포장에 대한 수요 증가

이탈리아의 1인당 GDP는 3만 4,780달러로, 2022년의 성장률은 전년 대비 2.3%입니다. 포장 산업 부문은 이 나라의 GDP의 약 0.36%에 기여하고 있습니다.

이탈리아는 코로나19 팬데믹의 영향으로 경기 침체를 겪었습니다.

유럽 연합의 포장재 생산량은 연간 4,000억 달러에 달하며, 이 중 15%가 이탈리아에서 생산됩니다.

이탈리아는 유럽에서 두 번째로 큰 골판지 상자 포장 국가입니다. 프랑스에서 저렴하고 가벼운 포장재의 수요가 증가함에 따라 향후 몇 년 동안 연포장 및 경질 플라스틱 포장재에 대한 수요가 증가할 것으로 예상됩니다. 따라서 프랑스 포장 산업의 성장으로 이어질 것으로 예상됩니다. 이탈리아는 세계 최대의 와인 생산국입니다. 그러나 이탈리아의 와인 생산량 감소는 향후 제품 포장에 걸림돌이 될 수 있습니다. 2021년 와인 생산량은 전년 대비 9% 감소했습니다.

전기자동차 수요 증가로 자동차 생산량 증가 전망

이탈리아는 유럽의 주요 자동차 제조업체 중 하나입니다.

2020년 자동차 생산량은 2019년 같은 기간에 비해 20% 감소했습니다.

2020년에는 전기자동차의 성장이 더욱 증가했습니다. 2020년 상반기 순수 전기차 등록 대수는 2019년에 비해 86% 증가했습니다. 전체 플러그인 차량의 총 판매량은 5만 500대로 증가했습니다.

마찬가지로 2021년에도 이탈리아 전기차 시장은 지속적으로 성장했습니다.

이탈리아의 접착제 산업 개요

이탈리아의 접착제 시장은 세분화되어 있으며 상위 5개사에서 34.73%를 차지하고 있습니다. 이 시장의 주요 업체는 AVERY DENNISON CORPORATION, H.B. Fuller Company, Henkel AG & Co. KGaA, MAPEI SpA Sika AG(알파벳 순 정렬) 입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 주요 산업 동향

최종 사용자 동향

항공우주

자동차

건축 및 건설

신발 및 가죽

포장

목공 및 목공예

규제 프레임워크

이탈리아

밸류체인과 유통채널 분석

제5장 시장 세분화

최종 사용자 산업

항공우주

자동차

건축 및 건설

신발 및 가죽

헬스케어

포장

목공 및 목공예

기타 최종 사용자 산업

기술

핫멜트

반응성

용매 기반

UV 경화 접착제

수계

수지

아크릴계

시아노아크릴레이트

에폭시

폴리우레탄

실리콘

VAE/EVA

기타 수지

제6장 경쟁 구도

주요 전략 동향

시장 점유율 분석

기업 상황

기업 프로파일

3M

Arkema Group

AVERY DENNISON CORPORATION

DURANTE ADESIVI SpA

FRATELLI ZUCCHINI SpA

HB Fuller Company

Henkel AG & Co. KGaA

Huntsman International LLC

MAPEI SpA

Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

세계의 접착제 및 실란트 산업의 개요

개요

Five Forces 분석 프레임워크(산업 매력도 분석)

세계의 밸류체인 분석

성장 촉진요인, 저해요인, 기회

출처 및 참고문헌

도표 일람

주요 인사이트

데이터 팩

용어집

HBR

영문 목차

영문목차

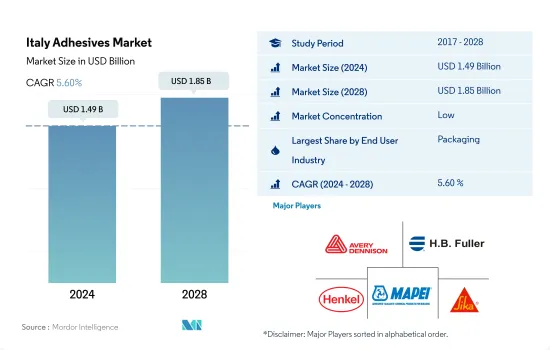

The Italy Adhesives Market size is estimated at 1.49 billion USD in 2024, and is expected to reach 1.85 billion USD by 2028, growing at a CAGR of 5.60% during the forecast period (2024-2028).

Emerging furniture market and evolving trend of flexible packaging expected to boost the consumption of adhesives in Italy

Adhesives play an important role in bonding and joining various substrates that are used across industries. These adhesives help manufacturers lower the weight of their components and assemblies and form joints quickly, easily, and accurately. The COVID-19 pandemic impacted the country in 2020, which reduced consumption by 10.38% compared to 2019.

The packaging sector has been experiencing significant growth in the country. The packaging industry has specific applications, such as cold chain solutions and transport packaging for electronics, consumer goods, medical, and food industries. The Italian packaging industry is one of the largest industries in Europe. There are nearly 7,000 active major and minor packaging companies in the country. The increasing importance of supermarket retailing and the changing consumer buying habits are increasing the demand for adhesives in packaging applications in the country.

Italy is known for its Italian furniture, which is popular around the world. Therefore, adhesives are largely consumed in the woodworking industry in Italy. In 2021, around 63,030 tons of adhesives were consumed by this industry, which is the second-largest end user of adhesives in the country during that year. Water-borne adhesives are largely consumed in this industry, as they are eco-friendly and cheaply available compared to other types of adhesives. The cost of these adhesives is nearly half compared to other adhesives.

The rising trend of flexible packaging and home renovation in the country is expected to drive the demand for adhesives in the coming years in Italy.

Italy Adhesives Market Trends

Rising trend of cheap and lightweight packaging in Italy drives the demand for flexible and rigid plastic packaging

Italy has a GDP of USD 34,780 per capita with a growth rate of 2.3% Y-o-Y in 2022. The packaging industry sector contributes to around 0.36% of the country's GDP. Italy is the second-largest packaging industry in Europe after Germany. Factors that are affecting the Italian packaging industry are trade exchange, employment, wine production, government policy support, etc.

The country witnessed an economic slowdown because of the impact of the COVID-19 pandemic. The production volume was reduced by 3.75% in the same year compared to 2019. This happened due to a supply chain disruption, labor shortages, and a lockdown in the country for nearly three months. International borders were opened in 2021 because of the economic recovery, which resulted in a regular supply of raw materials for production that increased by 3500 tons in 2021.

In the European Union, packaging production reaches USD 400 billion annually, out of which 15% of the share is produced in Italy. The packaging industry in the country is dominated by the paper and paperboard packaging segment, which is the second largest in Europe. Packaging is majorly used in food and beverages (29%) and healthcare and beauty products packaging (26%).

Italy is the second largest in corrugated box packaging in Europe. The rising trend of cheap and lightweight packaging in France is expected to drive the demand for flexible packaging and rigid plastic packaging in the coming years. Hence, it is expected to lead to the growth of the packaging industry in the country. Italy is the world's largest producer of wine. However, declining wine production in the country may hinder packaging products in the future. Wine production was reduced by 9% Y-o-Y in 2021.

Rising electric vehicles demand is likely to boost automotive production

Italy is one of the major automotive manufacturers in Europe. Compared to 2017, automotive vehicle production in the country contracted by 9.26% in 2018 and 22.2% in 2019, as in 2018 and 2019, factors like the fallout from Brexit, the implementation of more complex environmental regulations, and the tensions between the United States and China negatively affected the market for automotive vehicles in Italy.

The automotive vehicle production volume contracted by 20% in 2020 compared to the same period in 2019. The COVID-19 pandemic resulted in disruptions in car manufacturing and had a negative impact on the whole supply chain. Many suppliers additionally suffer from increased raw material costs (e.g., for steel, plastics, and resin) and higher energy prices, affecting the automotive market in the country.

In 2020, the country's electric vehicle growth further increased. Registrations for pure EVs in the first six months of 2020 were up by 86% compared to 2019. Almost 31,000 pure EVs were sold in 2020 till the end of June. Total sales of all plug-in vehicles rose to 50,500 units. The average pure-electric market share also increased significantly, driving the market for adhesives and sealants in the country.

Similarly, the year 2021 witnessed continued growth in the Italian EV market. In recent years, electric vehicle sales increased by six-fold in just three years. Similarly, the market share of electric vehicles increased to 4.6% in 2021. Thus, it is expected to improve the market for adhesives and sealants in the country.

Italy Adhesive Industry Overview

The Italy Adhesives Market is fragmented, with the top five companies occupying 34.73%. The major players in this market are AVERY DENNISON CORPORATION, H.B. Fuller Company, Henkel AG & Co. KGaA, MAPEI S.p.A. and Sika AG (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 KEY INDUSTRY TRENDS

4.1 End User Trends

4.1.1 Aerospace

4.1.2 Automotive

4.1.3 Building and Construction

4.1.4 Footwear and Leather

4.1.5 Packaging

4.1.6 Woodworking and Joinery

4.2 Regulatory Framework

4.2.1 Italy

4.3 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2028 and analysis of growth prospects)

5.1 End User Industry

5.1.1 Aerospace

5.1.2 Automotive

5.1.3 Building and Construction

5.1.4 Footwear and Leather

5.1.5 Healthcare

5.1.6 Packaging

5.1.7 Woodworking and Joinery

5.1.8 Other End-user Industries

5.2 Technology

5.2.1 Hot Melt

5.2.2 Reactive

5.2.3 Solvent-borne

5.2.4 UV Cured Adhesives

5.2.5 Water-borne

5.3 Resin

5.3.1 Acrylic

5.3.2 Cyanoacrylate

5.3.3 Epoxy

5.3.4 Polyurethane

5.3.5 Silicone

5.3.6 VAE/EVA

5.3.7 Other Resins

6 COMPETITIVE LANDSCAPE

6.1 Key Strategic Moves

6.2 Market Share Analysis

6.3 Company Landscape

6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

6.4.1 3M

6.4.2 Arkema Group

6.4.3 AVERY DENNISON CORPORATION

6.4.4 DURANTE ADESIVI S.p.A.

6.4.5 FRATELLI ZUCCHINI S.p.A.

6.4.6 H.B. Fuller Company

6.4.7 Henkel AG & Co. KGaA

6.4.8 Huntsman International LLC

6.4.9 MAPEI S.p.A.

6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR ADHESIVES AND SEALANTS CEOS

8 APPENDIX

8.1 Global Adhesives and Sealants Industry Overview

8.1.1 Overview

8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)