ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

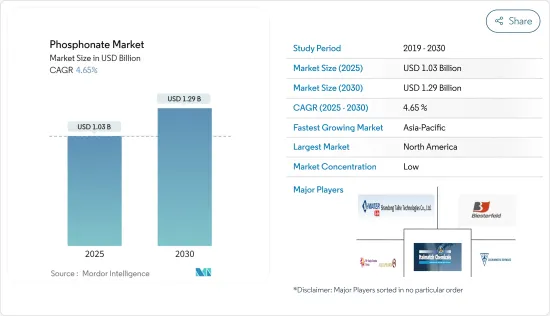

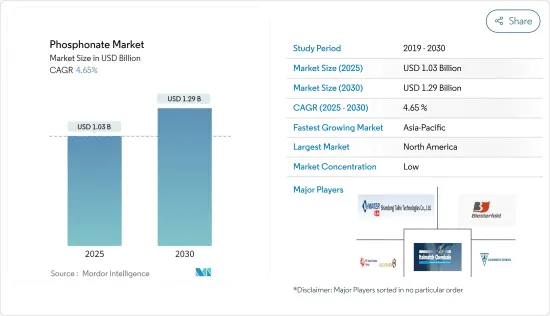

포스폰산염 시장 규모는 2025년에 10억 3,000만 달러로 추정되고, 2030년에는 12억 9,000만 달러에 이를 것으로 예측되며, 예측 기간인 2025-2030년 CAGR 4.65%로 성장할 전망입니다.

수처리 산업의 긍정적인 전망과 최근의 세제 및 세정제 산업의 꾸준한 진전이 향후 수년간 포스폰산염 수요를 견인할 것으로 보입니다.

주요 하이라이트

수처리 산업에 있어서의 포스폰산염의 용도는 넓습니다. 세정제 및 세제 산업의 급성장도, 포스폰산염 수요를 견인할 것으로 예상됩니다.

그러나, 포스폰산염의 비분해성에 의한 환경 문제에 대한 우려나, 대체품의 이용가능성이 시장의 성장을 방해할 것으로 예상됩니다.

포스폰산염의 프로드러그나 나노 다공성 포스폰산염에 대한 새로운 용도는 조사 대상 시장에 새로운 기회를 가져올 것으로 기대되고 있습니다.

아시아태평양이 시장을 독점하고 중국과 인도 수요가 대부분을 차지할 것으로 예상됩니다.

포스폰산염 시장 동향

수처리 산업 수요 증가

포스폰산염의 일종인 포인산염과 폴리인산염은 수처리에 있어서 매우 중요한 역할을 하고 있습니다. 그 주요 기능은 특히 납이나 구리 등의 파이프로부터의 부식이나 금속 용출을 억제하는 것입니다. 인산염은 이러한 금속과 반응하여 용해성이 낮은 화합물을 형성하고 오염의 위험을 최소화합니다. 또한 인산염은 철과 망간을 격리하여 물의 변색을 방지합니다.

수처리란, 화학제품을 사용해 스케일링을 제거 및 방지해, 부식을 억제하며, 박테리아나 조류를 사멸시켜, 물을 정화하는 선진적 기술입니다. 수처리 약품에는 주로, 응집제, 살생물제, 스케일 방지제의 3유형이 있습니다.

HEDP 포스폰산염은 다양한 산업용 수처리 공정에서 화학첨가제로 일반적으로 사용되고 있습니다.

기타 스케일 방지제와 비교해, HEDP에는 많은 이점이 있습니다. 뛰어난 내오염성, 저오염성, 뛰어난 용해성, 뛰어난 시너지 효과를 발휘합니다.

온실가스의 확산에 의한 기후의 변화에 의해 미국이나 멕시코 등의 나라에서는 가뭄의 빈도가 대폭 증가하고 있습니다.

미국의 가뭄 모니터가 보고하고 있듯이, 2023년에는 미국의 약 28%가 가뭄 상태에 직면했으며, 심각한 카테고리는 최근 몇개월 만에 급증하고 있습니다. 이러한 가뭄은 지하수, 댐, 운하의 물을 포함한 국가의 담수 자원을 현저하게 고갈시켜 깨끗한 식수의 위기적인 부족으로 이어집니다.

지방자치단체의 폐수를 처리하기 위해서, 몇개의 하수도 인프라가 정비되고 있습니다. 미국에서는 매일 약 340억 갤런의 폐수가 처리되고 있습니다. 이 도시 폐수에는 식품, 배설물, 비누, 세제에서 발생하는 질소와 인이 대부분 포함되어 있습니다.

각국 정부는 북미 전역에서 폐수처리 시책의 추진에 투자하고 있습니다. 예를 들면, 미국 환경 보호청은 2024년 2월, 청결한 식수와 폐수 인프라를 위해서 약 60억 달러를 투자한다고 발표했습니다.

또한 인도에서는 물 부족과 싸우기 위해 첨단 하수도 계획이 시행되고 있습니다. AMRUT(Atal Mission for Rejuvenation & Urban Transformation), Swachh Bharat Mission(Urban) 2.0, Smart Cities Mission 등의 대처가 주택 도시성에서 추진되고 있습니다.

2022년 12월, 국가 하천 보전 계획(NRCP)은 36개 하천 오염 방지 대책에 약 754억 7,800만 달러(6조 2,481억 6,000만 루피)를 기록했습니다. 이러한 치료는 16개 주 80개 도시에 걸쳐 있으며, 오염 대책으로서 하루에 27억 4,570만 리터(MLD)의 오수 처리 능력을 확립하는 것을 목표로 하고 있습니다.

최근 산업 부문 수요 증가 및 수질 오염 억제를 목적으로 한 정부 규제의 진전이 결합되어 수처리 솔루션에 대한 수요 증가에 박차를 가하고 있습니다.

산업단지의 새로운 수처리 시설에 대한 투자가 조사 대상 시장 수요를 높일 것으로 예상됩니다. 예를 들면

2024년 1월-로트겐 출신의 멤비온은 획기적인 멤비온 MBR 모듈에 대해 500만 유로(약 550만 달러)의 투자를 획득했습니다. 이 특허받은 모듈은 공간 효율이 높고 점유 면적이 75% 줄어들어 폐수 중 박테리아 부하를 기존 플랜트를 능가하는 1,000분의 1로 줄일 수 있습니다. 이 모듈은 도시 폐수와 산업 폐수 모두를 치료하기 위해 설계되었습니다.

2023년 10월-워터 코퍼레이션은 호주 모완줌 폐수 처리 공장의 830만 달러 상당 업그레이드를 완료했습니다. 이 노력은 새로운 원주민 커뮤니티 워터 서비스(ACWS) 프로그램의 일환으로 원주민 커뮤니티에서 최초의 인증 플랜트입니다.

2023년 6월-미국 환경보호청(EPA)은 아메리칸 인디언과 알래스카 원주민 부족을 위한 상하수도 인프라를 강화하기 위해 2억 7,800만 달러를 넘는 획기적인 투자를 발표했습니다.

물 부족과 자원의 감소에 따라, 수처리에 대한 수요는 세계적으로 높아지고 있으며, 예측 기간 중 포스폰산염의 거대 시장이 형성될 것으로 예상됩니다.

아시아태평양이 포스폰산염 시장을 독점할 전망

아시아태평양은 중국, 인도, 일본 등의 국가에서의 물 사용량 증가에 의해 포스폰산염의 소비량이 증가하여 포스폰산염 시장을 리드하고 있습니다.

중국과 인도는 세제, 수처리, 유전용 화학제품, 화장품, 기타 최종 이용 산업에서 수요가 높기 때문에 포스폰산염 시장을 견인하게 될 것으로 예상됩니다.

중국에서는 특히 COVID-19의 대유행 후, 위생 의식이 높아지고, 특히 타일이나 바닥재의 사용이 일반적이기 때문에 고급 바닥 클리너 수요에 박차가 걸리고 있습니다.

인도는 세계 최대의 세제 생산 및 공급국의 하나입니다. 인도에서 섬유용 세제 수요는 주로 세탁기의 보급률 상승에 견인되고 있습니다.

주요 세제 제조업체는 시장의 성장을 뒷받침하기 위해 제품의 혁신과 새로운 시설의 설립을 진행하고 있습니다. 예를 들면

2023년 12월-고드레이 컨슈머 프로덕츠(GCPL)는 세탁 체험의 변화를 목표로 한 액체 세제 'Godrej Fab'을 발매했습니다.

2022년 5월-Procter & Gamble(P& G)이 인도의 하이데라바드 교외에 20억 루피(2,683만 달러)를 투자하여 액체 세제의 제조 장치를 가동시켰습니다.

India Brand Equity Foundation(IBEF)은 인도 식기 세척기 시장이 델리, 뭄바이, 방갈로르 등 대도시 수요에 힘입어 2025-2026년 9,000만 달러 이상에 달할 것으로 예측했습니다.

이러한 동향으로부터, 아시아태평양의 포스폰산염 시장은 앞으로도 안정된 성장이 전망됩니다.

포스폰산염 산업 개요

세계의 포스 폰산 시장은 세분화되어 있습니다. 주요 진출 기업으로는 Italmatch Chemicals, Shandong Taihe Water Treatment Technologies, Biesterfeld AG, Aquapharm Chemical Pvt. Ltd, Zschimmer & Schwarz Chemie GmbH 등이 있습니다.(순부동)

ShanDong XinTai Water Treatment Technology Co. Ltd

Uniphos Chemicals

Zschimmer & Schwarz Chemie GmbH

제7장 시장 기회 및 향후 동향

프로드러그 및 나노다공성 포스폰산염에서 포스폰산염의 새로운 용도

기타 기회

AJY

영문 목차

영문목차

The Phosphonate Market size is estimated at USD 1.03 billion in 2025, and is expected to reach USD 1.29 billion by 2030, at a CAGR of 4.65% during the forecast period (2025-2030).

The positive outlook of the water treatment industry and steady progress in the detergent and cleaning agent industry in recent times are likely to drive the demand for phosphonates in the coming years.

Key Highlights

There are wide applications of phosphonates in the water treatment industry. The rapid growth of the cleaners and detergents industry is also expected to drive the demand for phosphonates.

However, environmental concerns due to its non-degradable nature and availability of substitutes are expected to hinder the market's growth.

Nevertheless, emerging applications of phosphonates in pro-drugs and nano-porous phosphonates are expected to create new opportunities for the market studied.

Asia-Pacific is expected to dominate the market, with the majority of demand coming from China and India.

Phosphonate Market Trends

Increasing Demand in the Water Treatment Industry

Orthophosphate and polyphosphates, types of phosphonates, play a pivotal role in water treatment. Their primary function is to curb corrosion and metal leaching from pipes, notably lead and copper. By reacting with these metals, phosphates form less soluble compounds, thereby minimizing contamination risks. Furthermore, phosphates sequester iron and manganese, averting water discoloration.

Water treatment is an advanced technique that uses chemicals to eliminate and prevent scaling, reduce corrosion, kill bacteria and algae, and purify water. There are three main types of water treatment chemicals: flocculants, biocides, and scale inhibitors.

HEDP phosphonate is commonly used as a chemical additive in various industrial water treatment processes. HEDP is a type of scale inhibitor that can prevent scale and dirt.

Compared to other scale inhibitors, HEDP has many advantages. It provides excellent dirt resistance, low pollution, good dissolution, and good synergy.

The changing climate due to the proliferation of greenhouse gases has greatly increased the frequency of droughts in countries like the United States and Mexico.

As reported by the US Drought Monitor, in 2023, around 28% of the United States faced drought conditions, with severe categories spiking in recent months. These droughts severely deplete the country's freshwater resources, including groundwater, dams, and canal water, leading to a critical shortage of clean drinking water.

Several sewerage infrastructures have been created to process municipal wastewater. In the United States, approximately 34 billion gallons of wastewater is being processed every day. This municipal wastewater mostly contains nitrogen and phosphorus from food, human waste, soaps, and detergents.

Governments are investing in promoting wastewater treatment policies across North America. For instance, in February 2024, the US EPA announced an investment of nearly USD 6 billion for clean drinking water and wastewater infrastructure.

Furthermore, in India, advanced sewerage programs are being implemented to combat water scarcity. Initiatives like the Atal Mission for Rejuvenation & Urban Transformation (AMRUT), Swachh Bharat Mission (Urban) 2.0, and the Smart Cities Mission are driving these efforts under the Ministry of Housing & Urban Affairs.

In December 2022, the National River Conservation Plan (NRCP) earmarked approximately USD 75,478 million (INR 6,248,160 million) for pollution control efforts on 36 rivers. These efforts span 80 towns across 16 states and aim to establish a sewage treatment capacity of 2,745.7 million liters per day (MLD) to combat pollution.

In recent years, rising water demand from the industrial sector, coupled with evolving government regulations aimed at curbing water pollution, have spurred a heightened demand for water treatment solutions.

Investments in new water treatment facilities in industrial complexes are expected to boost the demand of the market studied. For instance,

In January 2024, Membion, hailing from Roetgen, garnered an investment of EUR 5 million (~USD 5.5 million) for its groundbreaking Membion MBR modules. These patented modules are space-efficient, occupying 75% less area, and can diminish bacterial load in wastewater by 1,000 times, surpassing traditional plants. They are designed for both municipal and industrial wastewater treatment.

In October 2023, Water Corporation completed an upgrade worth USD 8.3 million to the Mowanjum wastewater treatment plant in Australia. This initiative is part of a new Aboriginal Communities Water Services (ACWS) program, leading to the first licensed plant in an Aboriginal community.

In June 2023, The US Environmental Protection Agency (EPA) unveiled a landmark investment exceeding USD 278 million to enhance water and wastewater infrastructure for American Indian and Alaska Native tribes, marking the largest annual funding allocation for such initiatives.

With rising water scarcity and fewer resources, the demand for water treatment is increasing globally, which is expected to provide a huge market for phosphonates during the forecast period.

Asia-Pacific Expected to Dominate the Phosphonate Market

Asia-Pacific leads the phosphonate market, driven by rising water usage in nations like China, India, and Japan, subsequently boosting phosphonate consumption.

China and India are set to propel the phosphonate market due to high demand from detergents, water treatment, oil field chemicals, cosmetics, and other end-use industries.

Heightened hygiene awareness in China, especially after the COVID-19 pandemic, has spurred demand for premium floor cleaners, especially with the country's common use of tile and wood flooring.

India is one of the largest producers and suppliers of detergent globally. The demand for fabric detergents in India is mainly driven by the rising penetration of washing machines.

Key detergent manufacturers are innovating products and establishing new facilities to bolster the market's growth. For instance,

In December 2023, Godrej Consumer Products (GCPL) launched "Godrej Fab," a liquid detergent aimed at transforming the laundry experience.

In May 2022, Proctor & Gamble (P&G) inaugurated its inaugural liquid detergent manufacturing unit on the outskirts of Hyderabad, India, with an investment of INR 200 crore (USD 26.83 million).

The India Brand Equity Foundation (IBEF) projects India's dishwasher market to exceed USD 90 million by 2025-2026, spurred by demand in major cities like Delhi, Mumbai, and Bangalore.

Due to these trends, the Asia-Pacific phosphonate market is set for consistent growth in the years ahead.

Phosphonate Industry Overview

The global phosphonate market is fragmented in nature. The major players (not in any particular order) include Italmatch Chemicals, Shandong Taihe Water Treatment Technologies Co. Ltd, Biesterfeld AG, Aquapharm Chemical Pvt. Ltd, and Zschimmer & Schwarz Chemie GmbH.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Drivers

4.1.1 Wide Applications of Phosphonates in the Water Treatment Industry

4.1.2 Rapid Growth of the Cleaners and Detergents Industry

4.1.3 Other Drivers

4.2 Market Restraints

4.2.1 Environmental Impact Due to Non-Degradable Nature

4.2.2 Availability of Substitutes

4.2.3 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 By Types

5.1.1 ATMP

5.1.2 HEDP

5.1.3 DTPMP

5.1.4 Other Types

5.2 By End-user Industry

5.2.1 Detergent and Cleaning Agent

5.2.2 Water Treatment

5.2.3 Oil field chemicals

5.2.4 Cosmetics

5.2.5 Building Materials

5.2.6 Other End-user Industries

5.3 By Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 NORDIC Countries

5.3.3.7 Turkey

5.3.3.8 Russia

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 Qatar

5.3.5.3 United Arab Emirates

5.3.5.4 Nigeria

5.3.5.5 Egypt

5.3.5.6 South Africa

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements