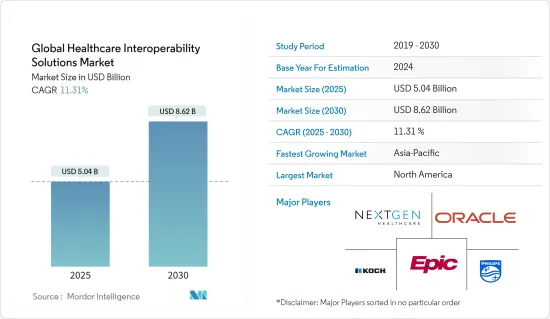

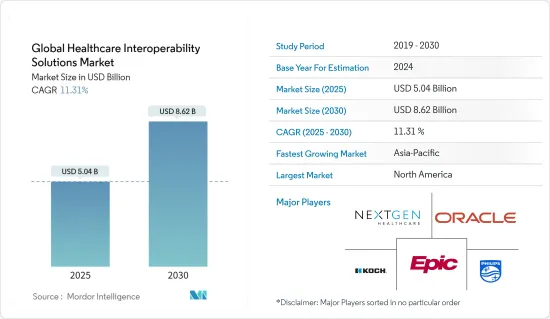

세계의 헬스케어 상호운용성 솔루션 시장 규모는 2025년 50억 4,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 11.31%로 성장할 전망이며, 2030년에는 86억 2,000만 달러에 이를 것으로 예측됩니다.

COVID-19 팬데믹은 COVID-19 환자의 급증으로 세계 경제와 헬스케어 인프라에 큰 영향을 미쳤습니다. 다양한 건강 상태에 있는 코로나19 환자들이 예기치 못한 형태로 유입되면서 헬스케어 제공 시설의 일반적인 기능을 혼란스럽게 했기 때문입니다. 예를 들어 2021년 2월 발표된 '코로나19 Highlights Need for Laboratory Data Sharing and Interoperability'라는 제목의 기사에 따르면 SARS-CoV-2 팬데믹 결과 상호 운용 가능한 헬스케어 시스템의 필요성이 밝혀졌습니다. 게다가 같은 정보원에 따르면, 상호운용 가능한 헬스케어 시스템에 의해 코로나19에 대한 국가의 대응은 대폭 개선됩니다. 예를 들어, 환자는 증상을 헬스케어 제공자에게 연락할 수 있고, 헬스케어 제공자는 환자의 완전한 헬스케어 정보에 신속하게 접근하여 근본적인 문제를 치료할 수 있습니다. 따라서 코로나19 팬데믹은 헬스케어 상호운용성 솔루션 시장에 큰 영향을 줄 것으로 예상됩니다.

헬스케어 상호운용성 솔루션 시장 성장을 가속할 것으로 예상되는 주요 요인으로는 세계 의료 제공자의 디지털 헬스케어 솔루션 채택 및 투자 증가, 헬스케어 비용 증가에 대한 우려가 증가하고 있습니다. 헬스케어 상호운용성 솔루션은 증가하는 헬스케어 비용을 줄이는 데 도움이 되기 때문에 예측 기간 동안 더 널리 채택되고 시장 성장이 예상됩니다. 예를 들어, 헬스케어 상호운용성 솔루션을 채택하는 주요 이점은 헬스케어 효율성 향상, 헬스케어 품질 및 환자 경험 개선, 헬스케어 비용 절감, 의사의 소진 증후군 완화 등입니다. 따라서 의료 IT 및 상호운용성 솔루션에 대한 투자는 예측 기간 동안 증가할 것으로 전망되며, 이는 헬스케어 상호운용성 솔루션 시장의 성장을 가속할 것으로 기대됩니다. 예를 들어, 2020년 9월, 미국의 의료정보기술 국가조정관실은 헬스케어 생태계 전반에서 헬스케어 IT 표준을 채택하고 사용하기 위한 새로운 기회를 탐구하기 위해 의료 정보 기술의 선도적 가속 프로젝트 프로그램 하에서 총 270만 달러의 자금을 4개 조직에 기부했습니다.

게다가 세계적으로 증가하는 헬스케어 지출은 정부의 주요 우려 사항 중 하나이며, 이를 줄이기 위해 의료 IT 솔루션이 채택되고 도입되었습니다. 예를 들어 독일 연방 통계국(Destatis)의 2022년 6월 보고서에 따르면 독일의 헬스케어 지출은 해마다 증가하고 있으며, 2020년에는 4,410억 유로에 달했습니다.

게다가, 시장 진출 기업에 의한 이 부문에서의 신제품 출시는 헬스케어 상호운용성 솔루션 시장의 성장을 더욱 끌어올릴 것으로 예상됩니다. 예를 들어 2021년 12월에 CareCloud Inc.는 헬스케어 기관을 위한 차세대 인터페이스와 데이터 관리 엔진인 CareCloud Connector를 발표했습니다. 이 솔루션은, 바로 사용할 수 있는 통합을 제공하는 것으로, 데이터 관리와 전개 속도를 향상시키는 것과 동시에, 인터페이스의 제어 및 가시성의 향상을 실현하고 있습니다. 따라서 위의 요인들로 인해 조사 대상 시장은 예측 기간 동안 성장할 것으로 예상됩니다. 그러나 이 부문의 숙련된 전문가 부족이 예측 기간 동안 헬스케어 상호운용성 솔루션 시장의 성장을 억제할 것으로 예상됩니다.

상호 운용성 솔루션을 제공하는 서비스 제공업체가 많기 때문에 서비스 부문이 큰 점유율을 차지할 것으로 예상됩니다. 게다가 헬스케어 애플리케이션의 성능을 향상시키고 고속화하기 위한 전체적인 운영 비용을 최소화하는 클라우드 기반 플랫폼과 클라우드 컴퓨팅에 대한 헬스케어 및 과학 커뮤니티의 관심이 고조되면서 이 부문의 성장을 촉진하고 있습니다.

또한 이 시장의 서비스 제공업체는 지속적으로 제품을 혁신하고 있으며 시장에 큰 영향을 미칠 것으로 예상되는 신제품을 발표하고 있습니다. 예를 들어 2021년 7월 구글 클라우드는 생명과학과 헬스케어 조직을 위해 청구, 헬스케어 기록, 연구 데이터, 임상 검사 등 여러 소스의 데이터를 조화시키는 엔드 투 엔드 솔루션인 헬스케어 데이터 엔진을 발표했습니다. 마찬가지로 2020년 5월, New Wave Telecom은 Technologies, Inc.와 협업하여 헬스케어 데이터의 상호운용을 지원하는 데 필요한 서비스 및 제품을 헬스플랜에 제공하는 데 특화된 자회사 Onyx Technology를 출범시켰습니다. 따라서 이 부문은 예측 기간 동안 성장할 것으로 예상됩니다.

또한 소프트웨어 업그레이드, 교육 및 유지보수를 포함한 서비스의 빈번한 구매 및 기타 상호운용성 솔루션 채택이 조사 대상 부문의 성장을 더욱 높일 것으로 예상됩니다. 예를 들면, 2021년 4월, Reliq Health Technologies Inc.는, 대규모 기업의 요건을 충족시키기 위해서 iUGO Care 플랫폼에 FHIR(Fast Healthcare Interoperability Resources) 표준을 채용했습니다. 따라서 상기 요인들로 인해 서비스 부문은 예측 기간 동안 헬스케어 상호운용성 솔루션 시장에서 큰 점유율을 차지할 것으로 예상됩니다.

북미는 헬스케어 인프라의 디지털화에 대한 투자 증가, 헬스케어 비용 증가, 신제품 출시 등으로 조사 대상 시장에서 큰 점유율을 차지할 것으로 예상됩니다. 예를 들어, Canadian Institute for Health Information의 2021년 11월 보고서에 따르면 캐나다의 헬스케어 인프라는 2019년 2,670억 달러에서 2021년 3,080억 달러로 증가했습니다. 마찬가지로 미국의 의료 지출은 2019년 3조 8,000억 달러에서 2021년에는 4조 3,000억 달러로 증가했습니다. 따라서 증가하는 헬스케어 비용을 억제하기 위해 헬스케어 상호운용성 솔루션 수요가 증가해 시장 성장을 뒷받침할 것으로 예상됩니다.

게다가 북미에서 미국은 전자 의료기기(EHR)와 같은 디지털 헬스케어 솔루션이 거의 모든 병원에서 널리 사용되는 주요 국가 중 하나이기 때문에 헬스케어 상호운용성 솔루션의 지역 주요 시장이 될 것으로 예상됩니다. 예를 들어 2020년 12월에 발표된 '미국과 미국 이외의 헬스케어 시스템 간 전자 진료기록카드 이용의 평가'라는 제목의 조사연구에 따르면 다른 나라의 동업자와 비교했을 때 미국 임상의는 매우 많은 임상업무에 EHR을 적극적으로 이용하고 있으며, 이에 따라 헬스케어 상호운용성 솔루션의 채택이 진행되고 있습니다.

이에 더해 이 나라에서 주요 시장 진출기업의 존재와 제품 발매, M&A, 제휴 등의 사업 확대 이니셔티브가 시장 성장을 더욱 밀어올릴 것으로 예상됩니다. 예를 들면, 엠브라텔은 2022년 4월, 임상 접속, 정보 통합, 헬스케어 기록 공유와 같은 과제를 해결하고, 헬스케어를 통합적으로 파악하고자 하는 공공 기관이나 민간 기관에 적합한 Embratel Saude Interoperabilidade 솔루션을 발표했습니다. 따라서 상기 요인들로 인해 북미 지역이 큰 점유율을 차지할 것으로 예상되며, 예측 기간 동안 미국이 헬스케어 상호운용성 솔루션 시장의 주요 시장이 될 것으로 보입니다.

헬스케어 상호운용성 솔루션 시장은 현재 대기업에서 중소기업에 이르기까지 여러 기업이 존재하는 단편적인 시장이기 때문에 시장 경쟁이 완만합니다. 현재 시장을 독점하고 있는 기업으로는 Koninklijke Philips NV, Allscripts Healthcare LLC, Cerner Corporation, EPIC Systems Corporation, NextGen Healthcare Inc., Infor Inc., Jitterbit、Virtusa Corp., Orion Health Group Limited, IBM 등이 있습니다.

The Global Healthcare Interoperability Solutions Market size is estimated at USD 5.04 billion in 2025, and is expected to reach USD 8.62 billion by 2030, at a CAGR of 11.31% during the forecast period (2025-2030).

The COVID-19 pandemic had a significant impact on the world economy and healthcare infrastructure due to the sudden surge in COVID-19 patients. It significantly increased the demand for healthcare interoperability solutions because of the unforeseen influx of COVID-19 patients with different health conditions which disrupted the general functioning of any healthcare providing facility. For instance, according to an article published in February 2021, titled 'COVID-19 Highlights Need for Laboratory Data Sharing and Interoperability', the necessity for an interoperable healthcare system has become abundantly clear as a result of the SARS-CoV-2 pandemic, and in the United States, each state has its requirements for responding to the COVID-19, figures are inconsistent and depend on the location and information source. Further, as per the same source, the country's response to COVID-19 would be significantly improved by an interoperable healthcare system. For instance, a patient could contact their provider with symptoms, and the provider would have rapid access to the patient's complete medical information to treat any underlying issues. Hence it is anticipated that the COVID-19 pandemic is expected to have a significant impact on the healthcare interoperability solutions market.

The major factors that are expected to fuel growth in the healthcare interoperability solutions market include increasing adoption and investment in digital healthcare solutions by healthcare providers across the world and rising concerns over increasing healthcare costs. The healthcare interoperability solutions can help in reducing the increasing healthcare costs due to which they are expected to be adopted more widely over the forecast period and the market is expected to grow. For example, some of the major benefits of adopting healthcare interoperability solutions are an increase in healthcare efficiency, improvement in quality of care and patient experience, reduction the healthcare cost, and lightening physician burnout among other benefits. Hence, the investment in healthcare IT and interoperability solutions is expected to increase over the forecast period which is expected to fuel growth in the healthcare interoperability solutions market. For instance, in September 2020, the Office of the National Coordinator for Health Information Technology of the United States rewarded four organizations with funding of a total of USD 2.7 million under the Leading Edge Acceleration Projects in Health Information Technology program for the exploration of new opportunities for the adoption and use of health IT standards across the healthcare ecosystem.

Further, the increasing healthcare expenditure across the world is one of the major concerns for the governments, and to reduce that healthcare IT solutions are being adopted and deployed which is further expected to increase the adoption of healthcare interoperability solutions as they will play a crucial role in transferring of data from one place to another. For instance, according to the June 2022 report of the Federal Statistical Office (Destatis) of Germany, the country's healthcare expenditure is increasing year over year and in 2020 it stood at EUR 441 billion.

Moreover, the launch of new products in the area by the market players is further expected to boost the growth of the healthcare interoperability solutions market. For instance, in December 2021, CareCloud Inc. launched CareCloud Connector, a next-generation interface and data management engine for healthcare organizations. The solution offers ready-to-use integration that enhances data management and deployment speed while delivering improved interface control and visibility. Therefore, owing to the above-mentioned factors, the studied market is expected to grow over the forecast period. However, a shortage of skilled professionals in the area is expected to restrain the growth of the healthcare interoperability solutions market during the forecast period.

The service segment is anticipated to account for the major share owing to the presence of a substantial number of service providers for interoperability solutions. Furthermore, increasing interest of healthcare and scientific communities in the cloud-based platform and cloud computing to minimize the overall operational costs for better and faster performance of healthcare applications is driving the segment growth.

In addition, the service providers in the market are continuously innovating their products and launching new products which are expected to have a significant impact on the market. For instance, in July 2021, Google Cloud introduced a healthcare data engine, an end-to-end solution for life science and healthcare organizations that harmonizes data from multiple sources, including claims, medical records, research data, and clinical trials. Similarly, in May 2020, NewWave Telecom collaborated with Technologies, Inc. for the launch of Onyx Technology, a subsidiary focused on delivering health plans with services and products required to assist healthcare data interoperability. Hence, the segment is expected to grow over the forecast period.

Moreover, the frequent purchases of services, including software upgradation, training, and maintenance, and adoption of other interoperability solutions are further expected to boost growth in the studied segment. For instance, in April 2021, Reliq Health Technologies Inc. adopted the FHIR (Fast Healthcare Interoperability Resources) standard for its iUGO Care platform to fulfill the requirements of the large-scale enterprise. Therefore, due to the above-mentioned factors, the service segment is expected to hold a significant share in the healthcare interoperability solutions market during the forecast period.

The North American region is expected to hold a significant share in the studied market owing to the increasing investment in the digitalization of the healthcare infrastructure, increase healthcare expenditure, and launch of new products. For instance, according to the November 2021 report of the Canadian Institute for Health Information, the Canadian healthcare infrastructure increased from USD 267 billion in 2019 to USD 308 billion in 2021. Similarly, the healthcare expenditure of the United States increased from USD 3.8 trillion in 2019 to 4.3 trillion in 2021. Hence, to control the increasing healthcare cost, the demand for healthcare interoperability solutions is expected to increase which is expected to boost the market's growth.

Moreover, in the North American region, the United States is expected to be a major market in the region for healthcare interoperability solutions as it is one of the major countries where digital healthcare solutions like electronic health records (EHRs) are used widely in almost every hospital. For instance, according to the research study published in December 2020, titled 'Assessment of Electronic Health Record Use Between the US and Non-US Health Systems', when compared to their peers from other countries, clinicians from the United States used the EHR actively for a great deal more clinical tasks and hence, the adoption of healthcare interoperability solutions.

In addition to this, the presence of some key market players in the country and business expansion initiatives like product launches, mergers and acquisitions, and collaborations among others are expected to further boost the market growth. For instance, in April 2022, Embratel launched the Embratel Saude Interoperabilidade solution, suitable for public and private institutions that seek to solve the challenges of clinical connectivity, information integration, and sharing of medical records for an integral view of healthcare. Therefore, due to the above-mentioned factors, the North American region is expected to occupy a significant share, where the United States would be the major market for the healthcare interoperability solutions market over the forecast period.

The healthcare interoperability solutions market is currently fragmented in nature with the presence of several large to small and medium-sized players due to which, the market is moderately competitive. Some of the companies currently dominating the market are Koninklijke Philips NV, Allscripts Healthcare LLC, Cerner Corporation, EPIC Systems Corporation, NextGen Healthcare Inc., Infor Inc., Jitterbit, Virtusa Corp., Orion Health Group Limited, and IBM.