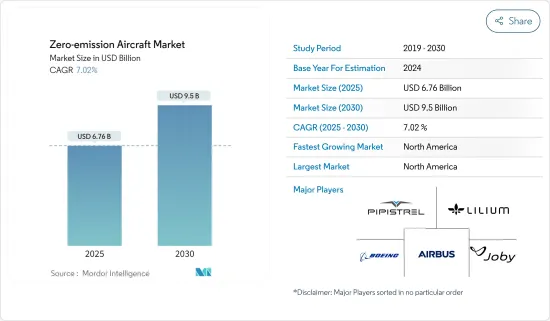

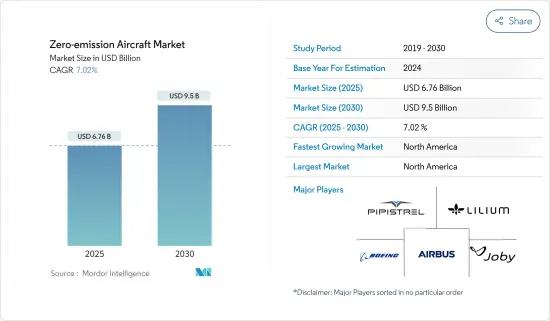

제로 에미션 항공기 시장 규모는 2025년에 67억 6,000만 달러로 추정되고, 예측 기간(2025-2030년) 중 CAGR 7.02%로 성장할 전망이며, 2030년에는 95억 달러에 달할 것으로 예측됩니다.

COVID-19 팬데믹의 발생은 여행 제한으로 인해 민간과 일반 항공 시장을 혼란시켰습니다. 또한 경제에도 영향을 주어 몇몇 항공 우주 기업은 혁신적인 프로젝트를 위한 자금을 일시 정지하는 결과가 되었습니다. 이러한 결정은 제로 에미션 항공기 시장의 성장에 일시적인 영향을 주었습니다. 그러나 항공기 운항사들이 운항 비용과 이산화탄소 배출량 감축을 모색하고 있어 예측 기간 동안 전 전기 항공기에 대한 투자, 검사, 채용이 크게 증가할 것으로 보입니다.

배기가스 규제의 엄격화로 인해 제조업체는 제로 에미션 개념으로 이동하고 있습니다. 엔진 제조사는 항공 산업이 새로운 컨셉으로 이행하는 데 중요한 역할을 할 것으로 생각됩니다. 지속가능한 항공 연료(SAF)는 Airbus나 Boeing과 같은 기업이 100% SAF에서의 비행을 목표로 하고 있듯이 산업의 CO2 배출량을 삭감하기 위한 항공 로드맵의 중요한 부분이기도 합니다.

기술적 과제뿐만 아니라 항공 산업의 전환은 규제와 인프라의 생태계를 바꾸어야 합니다. 인프라 및 제조 비용을 낮추기 위해서는 산업을 초월한 협력이 필요하며, 이는 상호 이익을 가져오고 제로 에미션 항공기 개발을 가속화하는 데 도움이 될 것으로 생각됩니다.

전기 항공기는 일반 항공 시장에 침투하고 있습니다. 그러나 장거리 상업 항공에 대한 채용은 예측 기간의 후반에 큰 개발이 기대되기 때문에 곧 현실이 되기에는 아직 갈 길이 멉니다.

2015년 미국 환경보호청(EPA)은 항공기에 사용되는 특정 클래스의 엔진에서 배출되는 온실가스가 대기오염의 원인이 되어 공중위생과 복지를 위험에 빠뜨린다고 인정했습니다. 2016년 ICAO는 유엔 회원국의 여객편과 화물편에 적용되는 세계 배출 감축 계획을 최종 결정했습니다. 2020년의 세계의 항공 배출량을 벤치마크로 해, 2020년의 배출량의 약 80%를 2035년까지 항공사가 오프 세트 하는 것이 결정되었습니다.

이와 같은 획기적인 결정에 의해 제조업체는 이산화탄소 배출량을 삭감하는 지속가능한 방법에 의지하고자, 전기항공기의 개발에 대한 길이 열렸습니다. 시장 관계자는 전기 항공기 기술에 대한 투자를 시작해, 이미 시제기의 성공이나 경비행기의 상업화라고 하는 형태로 성공을 거두고 있습니다.

새로운 기술이 등장함에 따라 상업적 실현 가능성을 향상시키기 위한 규제가 개발되고 있습니다. CS-23과 같은 규제는 항공기의 목적과 설계에 의존하지 않는 요건을 재정립하는 것입니다. 이로써 전 전기 추진과 하이브리드 추진 개발에 있어 다양한 기회의 길이 열렸습니다. 초점은 설계 요건을 충족하는 것에서 소비자의 안전성과 항공기 자동화를 향상시키는 것으로 옮겨졌습니다. 이를 통해 설계자는 항공기 전체를 처음부터 재설계하고 설계상의 제약으로 불가능했던 필요한 개조를 하는 데 집중할 수 있게 되었습니다.

북미와 유럽은 항공 시장이 성숙하고 있습니다. 주요 항공기 OEM에 가깝기 때문에 여러 항공우주 기업이 이러한 지역에 진출하고 있습니다. NASA, Airbus, Boeing, Rolls-Royce 등 항공우주 대기업의 존재는 제로 에미션 항공기 시장의 성장을 뒷받침할 것으로 보입니다. 현재, 제로 에미션 컨셉에 임하고 있는 기업의 90% 이상이 미국과 유럽에 거점을 두고 있습니다. 2020년 9월, 에어버스는 2035년까지 취항 가능한 제로 에미션 민간 항공기의 세 가지 컨셉을 밝혔습니다. 이러한 컨셉은 모두 1차 동력원으로서 수소에 의존하고 있습니다. Rolls-Royce는 최근 향후 10년간 에너지 저장 시스템에 8,000만 파운드를 투자할 계획을 발표했습니다. 이 회사는, 1회 충전으로 100마일 이상의 제로 이미션 비행을 가능하게 하는 에너지 저장 시스템(ESS)을 개발하고 있습니다. Rolls-Royce의 항공우주 인증 ESS 솔루션은 어반 에어 모빌리티 시장에서는 eVTOL(전동 수직 이착륙기), 커뮤터 시장에서는 최대 19석의 고정익기용 전기와 하이브리드 전기 추진 시스템에 전력을 공급합니다. 2020년 12월 초 수소전기항공기 개발사인 제로아비아는 아마존과 셸을 포함한 다수의 대형 투자자들로부터 미화 2,140만 달러를 지원받아 2023년부터 첫 업무용 제로 에미션 비행기를 운항하는 계획을 지원하기 위한 첫 번째 자금 조달 라운드를 완료했습니다. 이 회사는 또한 British Airways와 제휴하여 이 항공 기체에서 사용하는 제로 에미션 항공기의 개발을 모색하고 있습니다. 이 회사는 또, 항공 우주 기술 랩(ARI)을 통해서, 영국 정부로부터 1,630만 달러의 자금 원조를 받았습니다. 이러한 시장 개척은 예측 기간 동안 북미와 유럽의 시장 성장을 촉진할 것으로 예상됩니다.

다수의 신흥 기업이 이 시장에 진입함에 따라 시장은 급속하게 세분화되고 있습니다. 신흥 기업은 프로토타입을 설계하고 있으며, 항공기 개발의 다양한 단계에 있습니다. 이들 기업은 대형 항공 우주 기업이나 투자 회사로부터의 일련의 자금 조달에 의존하고 있습니다. 최근의 동향에서는 능력, 효율의 확대, 개발 사이클의 추진을 목적으로 한 새로운 제휴를 몇 가지 볼 수 있습니다. 예를 들어, Rolls-Royce는 최근 항공 우주 제조업체인 Tecnam과 스칸디나비아 최대 지역 항공사 Wideroe와 제휴하여 새로운 배터리 구동 항공기를 제조했습니다. 이 제휴는 Rolls-Royce와 Tecnam이 과거에 했던 'P-Volt'라고 불리는 전전기식 항공기를 바탕으로 2026년까지 노르웨이에서 통근자를 위한 전전기식 여객기를 취항시키는 것을 목적으로 하고 있습니다. 이 파트너십은 Rolls-Royce가 여러 항공 시장에서 전 전기와 하이브리드 전기 추진 및 동력 시스템의 선도적 공급업체가 되겠다는 야심을 보여줍니다. 이외에도 에어버스의 시티에어버스와 보잉의 eVTOL 등 몇몇 항공우주업체들이 배터리 구동 항공기를 계획하고 있습니다. 그 대부분은 도시 간이나 공항에서 시가지로 가는 페리를 목적으로 한 단거리 항공기입니다. 이 시장에서의 다른 유력 기업으로는 PIPISTREL do.o., Bye Aerospace, Aurora Flight Sciences, Eviation, Joby Aviation, NASA, Lilium GmbH, ZeroAvia, Inc. 등이 있습니다.

The Zero-emission Aircraft Market size is estimated at USD 6.76 billion in 2025, and is expected to reach USD 9.50 billion by 2030, at a CAGR of 7.02% during the forecast period (2025-2030).

The outbreak of the COVID-19 pandemic disrupted the commercial and general aviation market due to travel restrictions. It also had an impact on the economy and resulted in several aerospace companies to pause funds towards innovative projects. Such decisions have temporarily impacted the growth of the zero-emission aircraft market. However, as aircraft operators looking to reduce their operational costs and carbon emission, there will be significant growth in investment, testing, and adoption of all-electric aircraft during the forecast period.

Increasing stringency on the emission regulations has made manufacturers shift towards zero-emission concept. Engine manufacturers will play a vital role for the aviation industry to move towards the new concept. Sustainable aviation fuel (SAF) is also an important part of the aviation roadmap to reduce the industry's CO2 emissions as companies like Airbus and Boeing are targeting flights on 100% SAF.

Beyond technology challenges, the aviation industry's transition will require the regulatory and infrastructure ecosystems to change. Cross-industry collaboration will be required to drive down infrastructure and production costs, which will be mutually beneficial and help speed up development of the zero-emission aircraft.

Electric aircraft has penetrated the general aviation market. However, its adoption in long-haul commercial aviation is still far away from becoming reality soon with major developments expected in the later half of the forecast period.

In 2015, the US Environmental Protection Agency (EPA) found that the greenhouse gas emissions from certain classes of engines used in aircraft contribute to air pollution and endanger public health and welfare. In 2016, the ICAO finalized a global emissions-reduction scheme applicable to passenger and cargo flights in the member countries of the UN. It was decided that the global aviation emission in 2020 will be used as a benchmark, and around 80% of the emission levels in 2020 will be offset by the airlines until 2035.

Such a landmark decision paved the way for the development of electric aircraft as manufacturers sought to resort to sustainable ways of reducing carbon footprint. The market players started investing in electric aircraft technologies and have already been successful in the form of successful prototypes and commercialization of light aircraft.

With new technology coming into the foray, regulations are being framed to improve their commercial feasibility. Regulations, such as CS-23, reestablish the objectives and design independent requirements of an aircraft. This has opened various avenues of opportunities in the development of all-electric and hybrid propulsion. The focus has shifted from fulfilling design requirements to improving consumer safety and automation in aircraft. This has enabled the designers to focus on redesigning the total aircraft from scratch and make necessary modifications that were otherwise impossible due to design restrictions.

North America and Europe have a matured aviation market. Several aerospace companies are in these regions due to their proximity to major aircraft OEMs. The presence of aerospace giants like NASA, Airbus, Boeing, and Rolls Royce among others will support the growth of the zero-emission aircraft market. Over 90% of the companies currently working on the zero-emission concept are based in the US and Europe. In September 2020, Airbus revealed three concepts for zero-emission commercial aircraft which could enter service by 2035. All of these concepts rely on hydrogen as a primary power source. Rolls-Royce recently announced its plan to invest £80 million in energy storage systems over the next decade. The company is developing energy storage systems (ESS) that will enable aircraft to undertake zero-emission flights of over 100 miles on a single charge. Aerospace-certified ESS solutions from Rolls-Royce will power electric and hybrid-electric propulsion systems for eVTOLs (electric vertical takeoff and landing) in the urban air mobility market and fixed-wing aircraft, with up to 19 seats, in the commuter market. Earlier in December 2020, Hydrogen-electric aircraft developer ZeroAvia secured USD 21.4 million of backing from a raft of major investors, including Amazon and Shell, as the company completed its first fundraising round in support of plans to run its first commercial zero emission planes from 2023. The company has also partnered with British Airways to explore the development of zero emission aircraft for use in the airline's fleet. It also received approval of USD 16.3 million of U.K. government funding via the Aerospace Technology Institute (ARI). Such developments are anticipated to drive the market growth in the North America and Europe region during the forecast period.

The market is rapidly becoming fragmented as several new companies are venturing into this market. Start-ups are designing prototypes and are at various stages of aircraft development. These companies are dependent on series funding from major aerospace companies and investment firms. Several new collaborations have been observed in the recent past as companies look to expand capabilities, efficiency, and propel the development cycle. For instance, Rolls Royce has recently partnered with aerospace manufacturer Tecnam and Scandinavia's largest regional airline, Wideroe, to produce a new battery-powered aircraft. The partners aim to launch an all-electric passenger aircraft for commuters in Norway by 2026, building on previous work by Rolls Royce and Tecnam on an all-electric aircraft called the P-Volt. This partnership demonstrates Rolls-Royce's ambitions to be the leading supplier of all-electric and hybrid-electric propulsion and power systems across multiple aviation markets. Several other aerospace manufacturers have plans for battery-powered aircraft, including Airbus with the CityAirbus and Boeing's eVTOL. Most are short-range aircraft designed to ferry people between cities or from airports to city centers. Some of the other prominent players in the market are PIPISTREL d.o.o., Bye Aerospace, Aurora Flight Sciences, Eviation, Joby Aviation, NASA, Lilium GmbH, and ZeroAvia, Inc. among others.