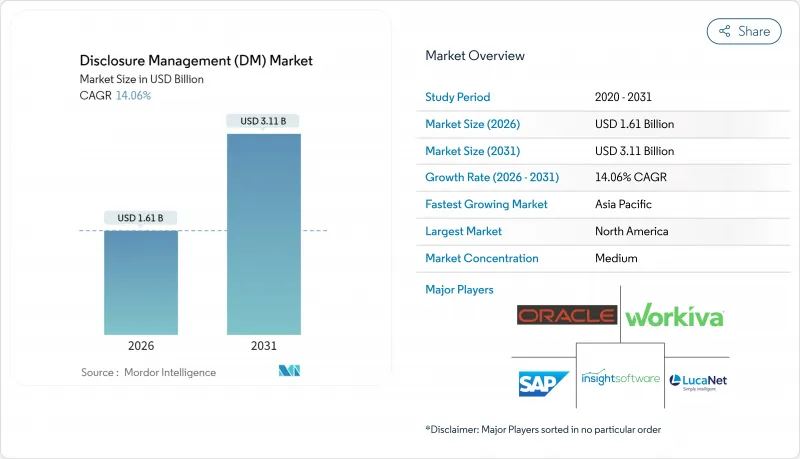

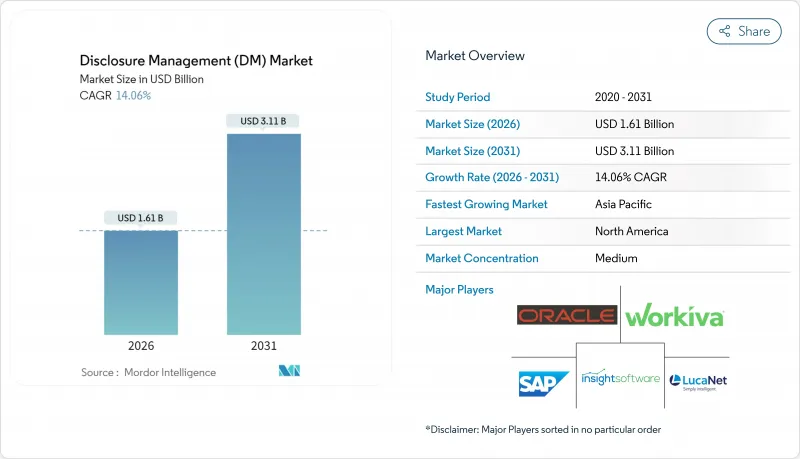

공시 관리(DM) 시장은 2025년 14억 1,000만 달러로 평가되었으며, 2026년 16억 1,000만 달러에서 2031년까지 31억 1,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 14.06%로 예상됩니다.

기업은 인라인 XBRL 의무에서 ESG 보고 제도에 이르기까지 증가하는 여러 관할 구역에 걸친 규제에 대응하기 위해 자동화된 컴플라이언스 플랫폼의 도입을 가속화하고 있습니다. 재무 팀이 엔드 투 엔드 관리, 주기 시간 단축 및 보다 강력한 감사 추적을 요구하는 가운데 구조화된 데이터 태그 지정과 내러티브 생성을 결합한 통합 솔루션이 단일 기능 툴을 대체하고 있습니다. 클라우드의 성숙도, AI 기반 이상 감지, 데이터 주권 요건을 존중하는 하이브리드 아키텍처가 수요를 더욱 촉진하는 한편 지속가능성 지표에 대한 투자자의 모니터링 강화로 ESG 모듈은 필수 기능 세트로서의 지위를 확고히 하고 있습니다.

규제 당국은 기계 판독 가능 공시의 범위를 확대하고 있습니다. 미국 증권거래위원회(SEC)가 2024년 7월부터 인라인 XBRL에 사이버 보안 관련 자료의 제출을 의무화하면서, 태그 지정의 세분화가 진행되어 발행체에는 제출 워크플로의 근대화가 요구되고 있습니다. 동시에 유럽 ESEF 프레임워크에서는 XHTML 기반 연례 보고서가 요구되며, 아시아태평양 규제 당국도 독자적인 택소노미 도입 스케줄을 책정 중입니다. 다국적 기업은 현재 서로 다른 방식을 동시에 처리할 필요가 있어 데이터 모델의 조화, 택소노미 업데이트 관리, 단일 출처 공개를 가능하게 하는 플랫폼에 대한 수요가 증가하고 있습니다. 2025년 12월에 시행된 MiCAR(암호자산시장법)에 따른 암호화 자산 백서 규정은 구조화 보고를 새로운 자산 클래스로 확대하여 규제 당국의 디지털 제출에 대한 장기적인 노력을 나타냅니다.

인라인 XBRL은 기존에 인간이 읽을 수 있는 HTML과 기계가 읽을 수 있는 XBRL 사이에 존재하는 격차를 없애고 데이터가 제출된 순간에 알고리즘이 분석할 수 있도록 합니다. 유럽 증권시장국(ESMA)이 2024년 8월에 발표한 ESRS Set 1 택소노미는 투자자가 대규모로 벤치마킹할 수 있는 기계 판독 가능 ESG 문장을 실현합니다. SEC의 EDGAR Next 프로그램은 2025년 9월까지 제출자를 개별 다단계 인증 계정으로 이전하며 이는 규제 당국의 데이터 무결성과 사이버 보안에 대한 노력을 강조합니다. 금융기관은 표준화된 태그와 준실시간 액세스를 통해 감사 비용을 줄이고 분석을 가속화하는 가장 큰 혜택을 누릴 수 있습니다.

IFRS가 공통 기반을 제공하는 한편, 지역별 택소노미 사양이 비호환성을 초래하고 있습니다. EU의 ESRS 태그는 SEC의 미국 회계 기준 확대와 상이하며 일본은 ISSB 기반 택소노미를 구축 중이지만 라벨 구조에서는 여전히 차이가 있습니다. SEC는 2022-2024년에 걸쳐 맞춤 태그 사용률이 상승한 것을 지적하고 있으며, 이는 발행자가 자신의 공개사항을 표준 요소에 매핑하는 데 어려움을 겪고 있음을 보여주고 있습니다. 공급업체는 병렬 스키마 라이브러리를 유지해야 하며 따라서 엔지니어링 오버헤드가 증가하고 릴리스 사이클이 지연됩니다. 다국적 기업은 분기별 재태깅 비용에 직면하며 이는 플랫폼 전환의 가속화를 막고 있습니다.

2025년 소프트웨어는 통합 제품군으로 태그 지정, 워크플로 및 분석 기능을 제공하여 공시 관리(DM) 시장에서 점유율 70.68%를 유지했습니다. 그러나 서비스 부문은 15.74%의 연평균 복합 성장률(CAGR)로 빠르게 성장하고 있습니다. 이는 제도 변경에 대응하기 위해 기업이 권고, 도입 지원, 매니지드 서비스 등 전문 지식을 요구하는 움직임 때문입니다. 전문 서비스 파트너는 택소노미 업데이트를 플랫폼 설정에 반영하여 재무, 법무, IT 팀을 통한 변경 관리를 조정합니다. 매니지드 서비스 모델은 인력이 부족한 중견 규모의 제출 기업에게는 제출 사이클에 연동한 예측 가능한 구독 요금으로 인해 매력적입니다. 그 결과, 서비스 수익은 2031년까지 소프트웨어와의 차이를 부분적으로 줄이고 성과 기반 계약 형태를 중심으로 벤더의 경제 구조를 재구축할 것으로 예측됩니다.

서비스 부문의 급성장은 "서비스형 컴플라이언스"로의 구조적 전환을 보여줍니다. 프로바이더는 공유형 센터 오브 엑셀런스를 활용해 규제 모니터링 비용을 고객 간에 분산시키는 한편, 고객은 XBRL 택소노미 매핑이나 ESG 중요성 평가 범위 설정 등 전문 스킬을 외부에 위탁합니다. AI 탑재 고객센터는 현재 설명 문서 작성 및 검증 오류의 자동 해결을 통해 생산성과 이익률을 향상시키고 있습니다. 이 운영 모델은 공급업체와 고객 간의 연결을 강화합니다. 공시 업무 흐름을 외부로 위탁하면 전환 비용이 증가하고, 결과적으로 지속적인 수익원이 확보되어 공시 관리(DM) 시장 전체의 회복력이 향상됩니다.

클라우드 도입은 2025년에 매출의 63.64%를 차지하였으며 연간 16.78%의 성장이 예상되고, 이는 기업이 탄력적인 컴퓨팅, 자동 업데이트, 공동 리뷰를 선호하는 경향을 뒷받침하고 있습니다. SaaS 공급업체는 택소노미 업데이트를 당일 제공하고 로컬 패치 적용 없이 제출 서류 규정 준수를 유지합니다. 자동 스케일링은 제출 피크 시의 부하를 회피하고 통합 전자 서명 및 감사 로그를 통해 인증 절차를 단순화합니다. 온프레미스 잔존 워크로드는 은행 및 방위 등 엄격한 규제 산업에 집중하고 있지만, 기밀 데이터를 로컬 노드에 유지하면서 처리 결과를 퍼블릭 클라우드 포털에 전송하는 하이브리드 전개가 기세를 늘리고 있습니다.

클라우드 주권에 대한 우려로 인해 전용 암호화 키와 고객 관리형 HSM을 갖춘 멀티 리전 아키텍처가 권장됩니다. 주요 공급자는 2024년 EU 전용 주권 클라우드 존을 시작하여 기관이 Schlems II 이전 제도를 충족할 수 있도록 했습니다. 워키바의 멀티 테넌트 SaaS 설계는 팀 횡단적인 공동 편집을 허용하지만, 회사는 기밀 공개를 다루는 정부 기관을 위한 싱글 테넌트 정부 전용 클라우드 옵션도 도입했습니다. 이러한 강화 전략이 결합되어 클라우드는 미래 구현의 기본 옵션으로 확고한 입지를 구축하고 공시 관리(DM) 시장에서 성장 엔진으로서의 역할을 강화하고 있습니다.

북미는 2025년 매출의 33.68%를 유지했으며 SEC의 인라인 XBRL과 사이버 보안 관련 서류에 대한 적극적인 자세가 이를 지원했습니다. 미국 발행체는 자동화 플랫폼을 활용하여 다중요소 인증을 통한 EDGAR Next 로그인 관리와 진화하는 GAAP 업데이트에 따른 서류 태그 지정 동기화를 실현하고 있습니다. 캐나다의 규제 당국은 미국 택소노미 스케줄을 따르고 있으며, 멕시코 증권위원회는 대기업용 XBRL 템플릿의 시험적 운용을 진행하고 있습니다. 높은 클라우드 성숙도와 풍부한 XBRL 인재를 배경으로 이 지역은 AI 구동형 내러티브 생성과 이상 감지 엔진의 혁신에 대한 시험장이 되고 있습니다.

유럽에서는 CSRD(기업 지속가능성 보고 지침)의 의무화와 ESEF(유럽 지속가능성 보고 프레임워크) 파일 패키징 요건을 바탕으로 꾸준한 확대가 나타났습니다. 50,000개가 넘는 회사가 CSRD의 대상이 되면서 이중 중요성 평가와 스코프 3 데이터 집계를 통해 급증하는 처리 능력에 대한 수요를 이끌고 있습니다. ESMA에 의한 ESRS Set 1 택소노미의 공시는 지속가능성 보고서의 공통 디지털 언어를 구축하여 경계 비교 가능성을 실현했습니다. 데이터 주권의 의무화는 하이브리드 아키텍처를 촉진하고, 주권 클라우드 구상에 의해 발행체는 개인 데이터를 EU 영역 내에 유지하면서 SaaS 공개 엔진을 활용한 가시화를 실현하고 있습니다.

아시아태평양은 규제 당국에 의한 제출 제도의 근대화에 따라 16.92%라는 가장 높은 CAGR 전망을 보였습니다. 일본의 대형주용 ESG 의무화 제도과 싱가포르의 AI를 활용한 규제보고 샌드박스가 클라우드 플랫폼의 조기 도입을 촉진하고 있습니다. 중국은 STAR 시장 제출 서류 내에서 ESG 지표의 검사 운용을 시작했고, 인도에서는 공개 회사 수가 증가함에 따라 저비용 태그 지정 도구에 대한 수요가 높아지고 있습니다. 호주와 한국에서는 기후위험공개 템플릿의 정교화가 진행되고 있으며, 크로스보더 플랫폼의 기회가 확대되고 있습니다. 데이터 거주 요구 사항의 문제가 해결되면 모바일 퍼스트 사용자 경험과 구독 가격 설정에 대한 지역적 수요가 클라우드 배포를 가속화할 수 있습니다.

The Disclosure Management market was valued at USD 1.41 billion in 2025 and estimated to grow from USD 1.61 billion in 2026 to reach USD 3.11 billion by 2031, at a CAGR of 14.06% during the forecast period (2026-2031).

Enterprises are accelerating the adoption of automated compliance platforms to cope with mounting multi-jurisdictional regulations, from inline XBRL mandates to ESG reporting rules. Integrated solutions that combine structured data tagging with narrative generation are overtaking point tools as finance teams seek end-to-end control, lower cycle times, and stronger audit trails. Cloud maturity, AI-based anomaly detection, and hybrid architectures that respect data-sovereignty requirements further propel demand, while investor scrutiny of sustainability metrics cements ESG modules as a must-have feature set.

Regulators are widening the scope of machine-readable disclosures. The SEC's inclusion of cybersecurity exhibits in inline XBRL from July 2024 heightened tagging granularity and pushed issuers to modernize filing workflows. Simultaneously, Europe's ESEF framework demands XHTML-based annual reports, while Asia-Pacific regulators establish their own taxonomy timelines. Multinationals now juggle divergent schemes, prompting demand for platforms that harmonize data models, manage taxonomy updates and enable single-source publishing. Crypto-asset white-paper rules under MiCAR, effective December 2025, extend structured reporting to new asset classes and illustrate regulators' long-term commitment to digital filings.

Inline XBRL collapses the historical gap between human-readable HTML and machine-readable XBRL, letting algorithms parse data the instant it is filed. ESMA's ESRS Set 1 Taxonomy, published August 2024, enables machine-readable ESG statements that investors can benchmark at scale. The SEC's EDGAR Next program, which transitions filers to individual multifactor-authenticated accounts by September 2025, underscores regulators' drive for data integrity and cybersecurity. Financial institutions gain most, trimming audit fees and accelerating analytics thanks to standardized tags and near-real-time access.

While IFRS offers a common baseline, regional overlays spawn incompatibilities. EU ESRS tags differ from SEC U.S. GAAP extensions, and Japan is building an ISSB-based taxonomy that still diverges in label structure. The SEC highlighted rising custom tag rates between 2022-2024 as issuers struggled to map unique disclosures onto standard elements. Vendors must maintain parallel schema libraries, inflating engineering overhead and slowing release cycles. Multinationals face re-tagging costs each quarter, dampening rapid platform migrations.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Software retained 70.68% of the Disclosure Management market in 2025 by bundling tagging, workflow and analytics in unified suites. Yet the Services segment is racing ahead at a 15.74% CAGR as enterprises seek advisory, implementation and managed-service expertise to keep pace with rule changes. Professional-service partners translate taxonomy updates into platform configurations and orchestrate change-management across finance, legal and IT teams. The managed-service model appeals to mid-sized filers that lack headcount and want predictable subscription fees tied to filing cycles. As a result, Services revenue is forecast to close a portion of the gap with Software by 2031, reshaping vendor economics around outcome-based engagements.

The surge in Services illustrates a structural shift toward "compliance-as-a-service." Providers leverage shared centers of excellence to spread regulatory surveillance costs across clients, while customers offload niche skill-sets such as XBRL taxonomy mapping or ESG materiality scoping. AI-enabled service desks now draft narrative sections and auto-resolve validation errors, raising productivity and margins. This operating model reinforces vendor-customer stickiness: once disclosure workflows are outsourced, switching costs rise, which in turn anchors recurring revenue streams that improve overall Disclosure Management market resilience.

Cloud deployments accounted for 63.64% revenue in 2025 and are forecast to grow 16.78% annually, underscoring enterprises' preference for elastic compute, automated updates and collaborative review. SaaS vendors ship taxonomy refreshes overnight, ensuring filings remain compliant without local patching. Automated scaling accommodates peak filing-week loads, while integrated e-signatures and audit logs simplify attestation. Remaining on-premise workloads cluster in heavily regulated verticals such as banking and defense, yet hybrid deployments that keep sensitive data on local nodes while piping rendered outputs to public-cloud portals are gathering momentum.

Cloud sovereignty concerns encourage multi-region architectures with dedicated encryption keys and customer-controlled HSMs. Major providers launched EU-specific sovereign-cloud zones in 2024, allowing institutions to satisfy Schrems II transfer rules. Workiva's multi-tenant SaaS design enables cross-team co-authoring, but the firm also introduced single-tenant government-cloud options for agencies handling classified disclosures. Collectively, these enhancements reinforce cloud as the default path for future implementations and cement its role as the Disclosure Management market's growth engine.

The Disclosure Management Market Report is Segmented by Component (Software, Services), Deployment Model (On-Premises, Cloud, Hybrid), End-User Enterprise Size (Large Enterprises, Smes), Application (Regulatory and Tax Filing, Financial Consolidation and Close, and More), End-User Industry (BFSI, IT and Telecom, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America maintained 33.68% of 2025 revenue, underpinned by the SEC's proactive stance on inline XBRL and cybersecurity exhibits. U.S. issuers rely on automated platforms to manage multifactor EDGAR Next logins and to synch exhibit tagging with evolving GAAP updates. Canadian regulators are aligning with U.S. taxonomy schedules, while Mexico's securities commission pilots XBRL templates for large caps. High cloud maturity and a deep bench of XBRL talent make the region an innovation laboratory for AI-driven narrative generation and anomaly detection engines.

Europe demonstrated steady expansion on the back of CSRD obligations and ESEF file-package requirements. More than 50,000 companies fall under CSRD scope, driving surge-capacity needs for double materiality and Scope 3 data aggregation. ESMA's release of the ESRS Set 1 taxonomy built a common digital language for sustainability statements, enabling cross-country comparability. Data-sovereignty mandates boost hybrid architectures; sovereign-cloud initiatives let issuers keep personal data within EU borders while using SaaS disclosure engines for rendering.

Asia-Pacific delivered the fastest 16.92% CAGR outlook as regulators modernize filing regimes. Japan's mandatory ESG rules for large caps and Singapore's AI-powered regulatory reporting sandbox spur early uptake of cloud platforms. China is trialing ESG indicators within its STAR Market filings, while India's growing public-company base pushes demand for low-cost tagging tools. Australia and South Korea refine climate-risk templates, widening cross-border platform opportunities. Regional appetite for mobile-first user experiences and subscription pricing accelerates cloud adoption once data-residency hurdles are addressed.