영국의 데이터센터 - 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)

United Kingdom Data Center - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1690142

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

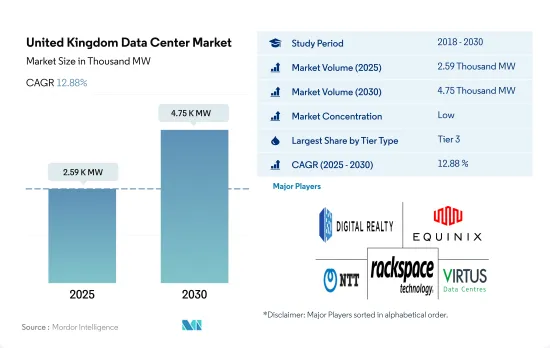

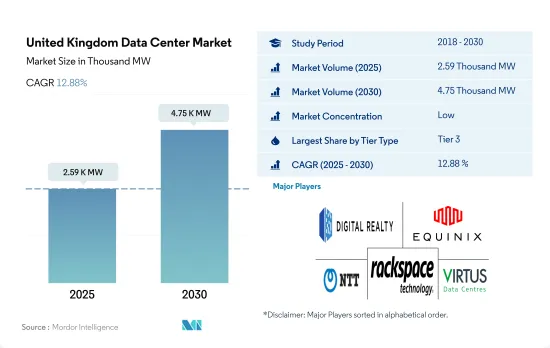

영국의 데이터센터 시장 규모는 2025년에 2,590MW, 2030년에는 4,750MW에 이를 것으로 예상되며, CAGR 12.88%로 성장할 것으로 예측됩니다.

또한 2025년 코로케이션 수익은 26억 6,100만 달러, 2030년에는 67억 9,950만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR은 20.64%를 나타낼 전망입니다.

Tier 3 데이터센터는 2023년에 수량 기준으로 대부분의 점유율을 차지하며, 예측 기간 동안에도 이점이 계속됩니다.

Tier 3 데이터센터는 현장 지원, 전력 및 냉각 중복성 등으로 인해 가장 선호되고 있습니다. 10.88%로 2023년 1,813.19MW에서 2029년에는 3,369.24MW로 성장할 전망입니다.

중소기업은 일반적으로 제공되는 중복 보호가 훨씬 우수하기 때문에 최소 3단계 등급의 시스템을 선호하고 사용합니다. 영국에서는 중소기업이 기업 인구의 99.9%를 차지합니다. 2022년 초에 영국의 민간 부문에는 550만 개 기업이 있는 것으로 추정됩니다. Tier 3 시설의 주요 채용은 BFSI, 통신, 미디어 엔터테인먼트 사용자가 홀세일과 하이퍼스케일 코로케이션을 주로 채용하고 있음에 반영됩니다. 2022년 현재 국내에는 약 148개의 3단계 데이터센터가 있으며, 약 28개의 3단계 데이터센터가 건설 중입니다.

Tier 4는 내결함성, 낮은 다운타임 및 99.99%의 가동 시간으로 대기업이 선호하는 데이터센터입니다. 클라우드 및 커뮤니케이션 부문의 주요 최종 사용자가 하이퍼스케일 코로케이션을 채택함으로써, 예측 기간 동안 시장은 잠재적인 성장을 보일 것으로 예상됩니다. 영국 정부의 G-Cloud 프로그램은 공공 부문에서 정보 통신 기술을 구입하는 방법을 바꾸고 있습니다. 2022년, 이 나라에는 Exascale Ltd와 ServerMania가 소유한 두 개의 Tier 4 데이터센터가 있었습니다.

Tier1&2 데이터센터는 전력 및 냉각을 위한 단일 경로이며 Tier3 및 Tier4 시설에 비해 99.671%(연간 28.8시간의 다운타임)의 예상 가동 시간을 제공하므로 가장 선호되지 않습니다.

영국 데이터센터 시장 동향

스마트폰 보급률 상승, 4G와 5G 서비스 등장이 시장 성장을 뒷받침

이 나라의 스마트폰 사용자 수는 2022년에는 6,346만명으로, 예측기간 중 CAGR은 1.01%로, 2029년에는 6,800만명에 달할 것으로 예측됩니다.

영국의 스마트폰 보급률은 해마다 상승하고 있으며, 2022년에는 전체의 93%에 달할 전망입니다. 넷 유저수는 6,230만명에 이르고, 이 숫자는 4G와 5G의 출현에 의해 약 286만명 증가해, 2026년에는 6,500만명을 넘을 것으로 예측되고 있습니다. 이후 사람들은 스마트폰 사용을 늘리고 온라인 게임과 미디어 스트리밍 플랫폼에 더 많은 시간을 보내고 있습니다. 그 결과 2020년 4월 산업은 온라인 결제를 지원하기 위해 개인의 비접촉 카드 결제 이용 한도액을 30 파운드에서 45 파운드로 늘렸습니다.

사용자 수 증가는 데이터센터 시장 수요를 증가시켰습니다. 스마트폰은 대용량 데이터 청크를 실시간으로 처리해야 하기 때문에 대부분 저장을 위한 데이터 센터가 필요합니다. 스마트폰의 보급률이 2017년의 72%에서 2022년에는 90% 이상으로 증가한 과거의 기간중, 데이터센터의 랙수는 2017년의 약 21만 5,000개에서 2022년에는 38만 8,000개로 증가했습니다.

2G, 3G의 단계적 폐지와 4G, 5G 네트워크 채용, 모바일 기기 이용 증가가 시장 성장을 견인

영국 최초의 5G 네트워크는 2019년 5월에 가동했으며, 4G는 2012년 10월에 시작되었습니다. 4G 속도는 2012년 12Mbps에서 2022년 36.40Mbps로 증가했습니다. 마찬가지로 5G 속도는 2019년 139.5Mbps에서 2022년에는 160.15Mbps로 증가하였습니다.

영국은 2033년까지 2G와 3G 모바일 서비스를 단계적으로 폐지합니다. 영국 정부는 1억 1,000만 파운드(1억 3,500만 달러) 상당의 투자를 지원하고 5G와 6G의 개발 촉진에 투자할 의향을 보여주고 있습니다. 또한, 2G와 3G의 전환일은 이동통신사 Vodafone, EE, Virgin Media, O2, Three와 합의되었습니다.

가속화와 전반적인 연결성 향상은 다른 최종 사용자 산업에도 길을 열었습니다. 수는 전체 인구의 84.3%에 상당하며 2021-2022년 사이에 460만명 증가했습니다.

영국 데이터센터 산업 개요

영국의 데이터센터 시장은 세분화되어 있으며 상위 5개사에서 34.50%를 차지하고 있습니다. 이 시장의 주요 기업은 Digital Realty Trust Inc., Equinix Inc., NTT Ltd.,랙스페이스 테크놀로지(Rackspace Technology Inc.), 버투스 데이터 센터 프로퍼티(STT GDC)(가나다순으로 정렬됨)입니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

조사의 전제조건과 시장 정의

조사 범위

조사 방법

제4장 시장 전망

내하중

바닥면적

코로케이션 수입

설치 랙 수

랙 공간 이용률

해저 케이블

제5장 주요 산업 동향

스마트폰 사용자수

스마트폰 1대당 데이터 트래픽

모바일 데이터 속도

광대역 데이터 속도

광섬유 접속 네트워크

규제 프레임워크

영국

밸류체인과 유통채널 분석

제6장 시장 세분화

핫스팟

런던

기타 중동 및 아프리카

데이터센터의 규모

대규모

초대규모

중규모

극초대규모

소규모

티어 유형

Tier 1과 2

Tier 3

Tier 4

흡수량

비이용

이용

코로케이션 유형별

하이퍼스케일

소매

홀세일

최종 사용자별

BFSI

클라우드

전자상거래

정부기관

제조업

미디어&엔터테인먼트

텔레콤

기타

제7장 경쟁 구도

시장 점유율 분석

기업 상황

기업 프로파일.

Colt Technology Services

CyrusOne Inc.

Digital Realty Trust Inc.

Equinix Inc.

Global Switch Holdings Limited

Global Technical Realty SARL

Kao Data Ltd

NTT Ltd

Rackspace Technology Inc.

Telehouse(KDDI Corporation)

Vantage Data Centers LLC

Virtus Data Centres Properties Ltd(STT GDC)

제8장 CEO에 대한 주요 전략적 질문

제9장 부록

세계 개요

개요

Five Forces 분석 프레임워크

세계의 밸류체인 분석

세계 시장 규모와 DRO

정보원과 참고문헌

도표 목록

주요 인사이트

데이터 팩

용어집

SHW

영문 목차

영문목차

The United Kingdom Data Center Market size is estimated at 2.59 thousand MW in 2025, and is expected to reach 4.75 thousand MW by 2030, growing at a CAGR of 12.88%. Further, the market is expected to generate colocation revenue of USD 2,661 Million in 2025 and is projected to reach USD 6,799.5 Million by 2030, growing at a CAGR of 20.64% during the forecast period (2025-2030).

Tier 3 data center accounted for majority share in terms of volume in 2023, it will continue its dominance during forecast period

Tier 3 data centers are the most preferred due to features such as onsite assistance, power, and cooling redundancy. The Tier 3 DC market was operating at 1540.98 MW in 2022. The expected capacity during the forecast period is expected to grow from 1813.19 MW in 2023 to 3369.24 MW in 2029 at a CAGR of 10.88%. These data centers are 'concurrently maintainable' with redundant components as a key differentiator.

SMBs generally prefer to use at least a tier III-rated system for the far superior redundancy protections offered. In the United Kingdom, SMEs account for 99.9% of the business population. At the start of 2022, there were estimated to be 5.5 million businesses in the UK private sector. Major adoption of tier 3 facilities is reflected in BFSI, telecom, and media and entertainment users are majorly adopting wholesale and hyperscale colocation. As of 2022, there are around 148 Tier 3 data centers in the country, and around 28 upcoming data centers are under construction with Tier 3 standards.

Tier 4 is the next most preferred data centers by large enterprises due to their fault-tolerant functionality, lower downtime, and 99.99% uptime. It is expected that the market will showcase potential growth during the forecast period with the adoption of hyperscale colocation by major end users in the cloud and telecom sectors. The UK government's G-Cloud program is changing the way public sector organizations purchase information and communications technology. In 2022, the country had two Tier 4 data centers owned by Exascale Ltd and ServerMania.

The Tier 1&2 data centers are the least preferred due to their single path for power and cooling and providing expected uptime of 99.671% (28.8 hours of downtime annually) when compared to Tier 3 and Tier 4 facilities.

United Kingdom Data Center Market Trends

Increase smartphone penetration rate, emergence of 4G and 5G services to boost market growth

The number of smartphone users in the country was 63.46 million in 2022 and is expected to witness a CAGR of 1.01% during the forecast period to reach a value of 68 million by 2029.

The smartphone penetration rate in the United Kingdom has increased each year, reaching an overall figure of 93% in 2022. Among the age group of 16-24, the smartphone ownership rate was 99% in 2022. The number of mobile internet users in the United Kingdom reached 62.3 million, a figure which is projected to increase by approximately 2.86 million and amount to over 65 million by 2026 with the emergence of 4G and 5G. Further, since the COVID-19 pandemic hit, people have increased their smartphone usage and spent more time on online gaming or media streaming platforms. As a result, in April 2020, the industry increased the spending limit on individual contactless card payments from GBP 30 to GBP 45 to help with online payments. Such a scenario has increased smartphone penetration and is currently following the same trend.

The growth of the user base positively boosted the market demand for data centers. The increasing rate has positively upheld its growth in the e-commerce, media and entertainment, and BFSI sectors, where a large chunk of data has been generated. Since smartphones necessitate real-time processing on having a large data chunk, they mostly require a data center for storage. During the historical period, when smartphone usage penetration increased from 72% in 2017 to more than 90% in 2022, the number of racks in the data center increased from around 215k in 2017 to 388k in 2022. This trend is further expected to be witnessed during the forecast period.

Phase out of 2G and 3G and adoption of 4G and 5G network and increase in use of mobile devices to drive market growth

The United Kingdom's first 5G network was activated in May 2019, and 4G was launched in October 2012. Since being commissioned, both networks have shown an increment in their data speed. 4G speed increased from 12 Mbps in 2012 to 36.40 Mbps in 2022. Similarly, 5G speed increased from 139.5 Mbps in 2019 to 160.15 Mbps in 2022. In May 2022, according to an industry survey, around 67% of respondents in the United Kingdom (UK) had a 4G service on their smartphone, while about 25% had a 5G service.

The UK will phase out 2G and 3G mobile services by 2033. The major strategy for all the operators is to turn off their 2G and 3G networks, allowing them to focus investments and spectrum resources on further improving the 4G customer experience while rolling out 5G. The UK government has outlined its intentions to invest in driving 5G and 6G development with the support of GBP 110 million (USD 135 million) worth of investment. Moreover, the switch-off date for 2G and 3G has been agreed upon with mobile-network operators Vodafone, EE, Virgin Media, O2, and Three.

The growth in speed and better overall connectivity is paving the way for other end-user industries. In 2021, users in the United Kingdom spent an average of four hours per day using their mobile devices. This was an increase of 0.3 hours up from 2020. The number of social media users in the United Kingdom at the start of 2022 was equivalent to 84.3% of the total population, and it increased by 4.6 million between 2021 and 2022. Overall, this will increase the mobile data speed, increasing the data traffic, which thereby requires data centers for storing and processing data.

United Kingdom Data Center Industry Overview

The United Kingdom Data Center Market is fragmented, with the top five companies occupying 34.50%. The major players in this market are Digital Realty Trust Inc., Equinix Inc., NTT Ltd, Rackspace Technology Inc. and Virtus Data Centres Properties Ltd (STT GDC) (sorted alphabetically).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

3.1 Study Assumptions & Market Definition

3.2 Scope of the Study

3.3 Research Methodology

4 MARKET OUTLOOK

4.1 It Load Capacity

4.2 Raised Floor Space

4.3 Colocation Revenue

4.4 Installed Racks

4.5 Rack Space Utilization

4.6 Submarine Cable

5 Key Industry Trends

5.1 Smartphone Users

5.2 Data Traffic Per Smartphone

5.3 Mobile Data Speed

5.4 Broadband Data Speed

5.5 Fiber Connectivity Network

5.6 Regulatory Framework

5.6.1 United Kingdom

5.7 Value Chain & Distribution Channel Analysis

6 MARKET SEGMENTATION (INCLUDES MARKET SIZE IN VOLUME, FORECASTS UP TO 2030 AND ANALYSIS OF GROWTH PROSPECTS)

6.1 Hotspot

6.1.1 London

6.1.2 Rest of United Kingdom

6.2 Data Center Size

6.2.1 Large

6.2.2 Massive

6.2.3 Medium

6.2.4 Mega

6.2.5 Small

6.3 Tier Type

6.3.1 Tier 1 and 2

6.3.2 Tier 3

6.3.3 Tier 4

6.4 Absorption

6.4.1 Non-Utilized

6.4.2 Utilized

6.4.2.1 By Colocation Type

6.4.2.1.1 Hyperscale

6.4.2.1.2 Retail

6.4.2.1.3 Wholesale

6.4.2.2 By End User

6.4.2.2.1 BFSI

6.4.2.2.2 Cloud

6.4.2.2.3 E-Commerce

6.4.2.2.4 Government

6.4.2.2.5 Manufacturing

6.4.2.2.6 Media & Entertainment

6.4.2.2.7 Telecom

6.4.2.2.8 Other End User

7 COMPETITIVE LANDSCAPE

7.1 Market Share Analysis

7.2 Company Landscape

7.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

7.3.1 Colt Technology Services

7.3.2 CyrusOne Inc.

7.3.3 Digital Realty Trust Inc.

7.3.4 Equinix Inc.

7.3.5 Global Switch Holdings Limited

7.3.6 Global Technical Realty SARL

7.3.7 Kao Data Ltd

7.3.8 NTT Ltd

7.3.9 Rackspace Technology Inc.

7.3.10 Telehouse (KDDI Corporation)

7.3.11 Vantage Data Centers LLC

7.3.12 Virtus Data Centres Properties Ltd (STT GDC)