ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

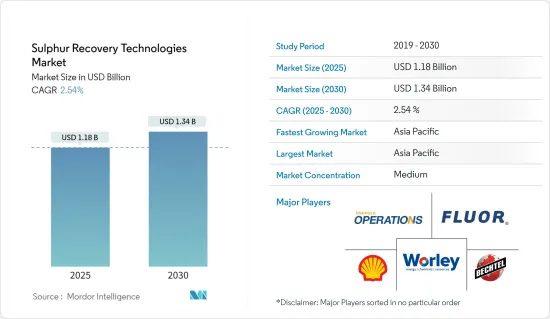

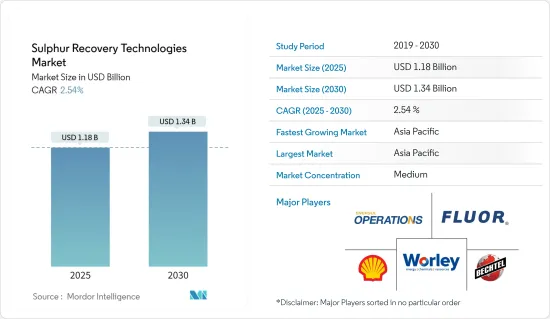

황 회수 기술 시장 규모는 2025년에 11억 8,000만 달러, 2030년에는 13억 4,000만 달러에 달할 것으로 예측됩니다. 예측 기간(2025년-2030년) CAGR은 2.54%를 나타낼 전망입니다.

주요 하이라이트

장기적으로는 환경 문제에 대한 관심이 높아지고, 엄격한 오염 기준, 향후 새로운 정유소와 확장 프로젝트가 황 회수 기술 시장을 견인할 것으로 예상됩니다.

한편, 황 회수 프로세스의 한계와 황 함유량 삭감을 위한 고비용이 시장을 억제할 것으로 예상됩니다.

그렇다고는 해도, 신흥 시장에 있어서의 미개발의 석유 및 가스의 잠재력은 예측 기간 이후도 급속히 증가할 것으로 예상됩니다.이러한 개발은 시장 성장에 큰 기회를 가져올 것으로 예상됩니다.

아시아태평양은 예측 기간 중 최대 시장이 될 것으로 예상되며, 석유 및 가스 생산의 고수준화, 환경 규제의 강화, 정제 능력의 향상에 의해 수요의 대부분은 중국과 인도에서 가져옵니다.

황 회수 기술 시장 동향

정유소 부문이 현저한 성장을 이룰 전망

황 회수 기술은 정유소에서 매우 중요한 역할을 하고 있어, 황 회수 장치(SRU)는 황 회수의 핵심 역할을 합니다. 특히, 휘발유나 디젤의 황 레벨을 낮추는 것은 배기가스 규제를 강화해, 제품 사용시의 대기 오염을 억제합니다.

석유 및 가스 정제 플랜트의 확장을 향한 투자가 증가해, 환경 규제가 세계적으로 강화되는 가운데, 정유 공장은 앞으로도 지배력을 유지할 준비가 되어 있습니다.

석유 정제소의 황 회수 장치(SRU)는 다양한 정제 공정의 제품별인 사워 가스에서 H2S를 추출하여 공업 등급의 용융 황으로 변환하는 것을 임무로 하고 있습니다. 이 장치들에서 주로 사용되는 방법인 클라우스 공정은 가스류로부터 95-99.9%의 황화수소를 제거할 수 있습니다.

예를 들어 석유수출국기구에 따르면 정유소의 원유처리 능력은 2023년에는 하루 8,076만 배럴, 2022년에는 7,908만 배럴이었습니다.

많은 국가들이 향후 수요에 대응하기 위해 황 회수 등의 기술을 중심으로 석유 정제 능력을 증강하고 있습니다. Bharat Petroleum Corporation Limited (BPCL)는 약 59억 8천만 달러 (50,000 crore 인도 루피)를 투자하여 인도에 연간 1,200만 톤(MMTPA)의 정유소를 신설할 계획을 발표했습니다.

2024년 6월, BPCL은 2029년도까지 정제능력을 4,500만 톤/년에 증강하는 의욕을 표명했습니다.

BPCL은 향후 5년간 약 200억 달러(1조 7,000억 카롤 루피)의 투자를 예정하고 있습니다. 파이프라인 구상에 9억 5,700만 달러(8,000캐롤 루피), 마케팅 활동에 24억 달러(20,000카롤 루피) 이상이 할당되고 있습니다.

우간다는 2024년 1월에 두바이의 왕족이 이끄는 투자 회사와 협상하고 있었습니다 그 협의의 중심은 우간다의 원유 매장량의 일부에 대한 40억 달러의 정유소의 개발 계획이었습니다.

2023년 11월까지 스리랑카의 내각은 중국의 거대 에너지 기업인 시노펙으로부터의 45억 달러의 투자를 승인했습니다.

따라서 클린 연료 수요 증가에 따라 황 회수 기술 시장은 예측 기간 중에 크게 확대될 것으로 예상됩니다.

아시아태평양이 시장을 독점할 전망

아시아태평양은 넓은 지역 정세별로 다양한 경관, 기후, 사회, 문화, 경제를 가지고 있습니다.세계 인구의 50% 이상이 이 지역에 살고 있습니다.

이 지역에는 석유 및 가스 부문에 상당액의 투자를 하고 있는 인도나 중국 등의 신흥 경제국이 다수 있습니다.

아시아태평양은 인도와 중국과 같은 신흥 국가와 일본, 한국, 호주와 같은 선진국이 존재하기 때문에 세계에서 가장 급성장하는 지역 중 하나입니다. 수입 의존도를 낮추고 에너지 안보를 향상시키기 위해 탄화수소 수요의 50% 가까이를 수입하고 있습니다.

중국은 사천 분지와 같은 다양한 내륙 셰일 분지에 걸친 국내 매장량을 개발함으로써 셰일의 잠재력을 최대한 끌어내려고 합니다. 중국의 셰일가스 개발은 최근 몇 년간 꾸준히 증가하고 있으며, 2017년 이후 매년 21%의 성장을 기록하고 있습니다.

인도의 석유 정화 및 석유화학 산업의 경우 유해한 황 배출을 줄이고 보다 깨끗한 연료를 생산하기 위한 황 회수 기술은 매우 중요합니다. 2030의 일환으로 인도의 공적 부문 정유소에서 유황 회수 블록을 설치하는 1억 4,902만 달러의 수주를 체결했습니다.

2024년 2월 말레이시아 국영 페트로나스는 말레이시아 석유 관리를 통해 반도 말레이시아 해안에 잠재적인 가스 매장량을 가진 두 곳의 발견 자원 기회 클러스터의 생산 분여 계약(PSC)에 조인했습니다. DRO 클러스터는 추정 회수량 4조 입방 피트로, 페트로나스 칼리가리와 업스트림 기업의 JX 일광일석 개발이 각각 50%의 참가 권익을 획득했습니다.

따라서 대규모 석유 및 가스 정제산업과 보다 깨끗한 화석연료에 대한 수요 증가로 아시아태평양이 시장을 독점할 것으로 예상됩니다.

황 회수 기술 산업 개요

황 회수 기술 시장은 세분화되어 있습니다. 이 시장의 주요 기업(특별한 순서 없음)에는 Enersul Limited Partnership, WorleyParsons Limited, Shell PLC, Bechtel Corporation, Fluor Corporation 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 지원

목차

제1장 서론

조사 범위

시장의 정의

조사의 전제

제2장 조사 방법

제3장 주요 요약

제4장 시장 개요

소개

2029년까지 시장 규모 및 수요 예측

2029년까지 정유소 설치 용량과 예측

2029년까지 정제 제품 중의 황분 허용량(백만톤/년)

최근 동향과 개발

정부의 규제와 정책

시장 역학

성장 촉진요인

환경 문제에 대한 관심 증가와 공해에 관한 엄격한 규범

억제요인

황 회수 공정의 한계

공급망 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

제5장 시장 세분화

용도

정유소

가스 처리 플랜트

발전소

기타

지역

북미

미국

캐나다

기타 북미

아시아태평양

인도

중국

한국

일본

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

유럽

독일

프랑스

영국

스페인

노르딕

튀르키예

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

나이지리아

오만

남아프리카

이집트

알제리

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

주요 기업의 전략

시장 점유율 분석

기업 프로파일

Enersul Limited Partnership

Worley Limited

Shell Plc

Bechtel Corporation

Fluor Corporation

Sulfur Recovery Engineering Inc.

Honeywell UOP

Air Liquide SA

List of Other Prominent Companies(Company Name, Headquarters, Revenue, Relevant Products and Services, Operating Sector, Recent Trends, Technology or Projects, Contact Details, etc.)

시장 랭킹 분석

제7장 시장 기회와 앞으로의 동향

신흥 시장에서의 석유 및 가스의 미개발 잠재력

SHW

영문 목차

영문목차

The Sulphur Recovery Technologies Market size is estimated at USD 1.18 billion in 2025, and is expected to reach USD 1.34 billion by 2030, at a CAGR of 2.54% during the forecast period (2025-2030).

Key Highlights

Over the long term, growing environmental concerns, strict pollution norms, and upcoming new refinery and expansion projects are expected to drive the sulfur recovery technologies market.

On the other hand, the limitations of the sulfur recovery process and the high cost of reducing the sulfur content are expected to restrain the market.

Nevertheless, untapped oil and gas potential in emerging markets is expected to increase rapidly beyond the forecast period. Such developments are expected to provide considerable opportunities for market growth.

Asia-Pacific is expected to be the largest market during the forecast period, with most demand coming from China and India due to high oil and gas production, increased environmental regulations, and increased refining capacity.

Sulphur Recovery Technologies Market Trends

The Refineries Segment is Likely to Witness Considerable Growth

Sulfur recovery technologies play a pivotal role in refineries, with the sulfur recovery unit (SRU) being a linchpin for sulfur recovery. Notably, lowering sulfur levels in gasoline and diesel enhances emission controls, subsequently curbing air pollution upon product usage.

With the rising investments in expanding oil and gas refining plants and the global push for stricter environmental regulations, refineries are poised to maintain their dominance in the future.

The sulfur recovery unit (SRU) in a petroleum refinery is tasked with extracting H2S from sour gases, a byproduct of various refinery processes, and transforming it into industrial-grade molten sulfur. The predominant method employed in these units, known as the "Claus Process," eliminates a substantial 95-99.9% of hydrogen sulfide from gas streams. In a modified version of the Claus Process, the H2S-rich sour gas is combusted with oxygen, followed by the resulting gas being cooled; molten sulfur is then recovered.

For instance, according to the Organization of the Petroleum Exporting Countries, refinery crude throughput was 80.76 million barrels per day in 2023 and 79.08 million in 2022. Key contributors to this capacity were the United States, China, India, Japan, Saudi Arabia, and other ASEAN nations. These countries predominantly rely on hydrocarbons and their derivatives.

Many nations are ramping up their oil refining capabilities, with a focus on technologies like sulfur recovery, to meet future demands. For example, in July 2024, Bharat Petroleum Corporation Limited (BPCL) unveiled plans for a new 12 million metric tons per annum (MMTPA) refinery in India, with an investment of approximately USD 5.98 billion (INR 50,000 crore). The company is scouting locations in Andhra Pradesh, Uttar Pradesh, and Gujarat.

In June 2024, BPCL announced its ambition to boost its refining capacity to 45 mmtpa by FY 2029. BPCL, which operates refineries in Mumbai, Kochi, and Bina (Madhya Pradesh), boasts a collective refining capacity of about 36 mmtpa.

BPCL has earmarked around USD 20 billion (INR 1.7 trillion) for investments over the next five years. Of this, INR 75,000 crore is allocated to refinery and petrochemical projects, USD 957 million (INR 8,000 crore) to pipeline initiatives, and over USD 2.4 billion (INR 20,000 crore) to its marketing endeavors.

Uganda was in talks with an investment firm spearheaded by a member of Dubai's royal family in January 2024. The discussions centered around the development of a planned USD 4 billion refinery for a portion of its crude oil reserves.

By November 2023, the Sri Lankan cabinet had greenlit a USD 4.5 billion investment from China's energy behemoth, Sinopec. The approval paved the way for Sinopec to set up a new petroleum refinery at the strategically vital Hambantota port.

Therefore, with the increase in demand for clean fuel, the sulfur recovery technologies market is expected to expand considerably during the forecast period.

Asia-Pacific is Expected to Dominate the Market

Asia-Pacific covers a wide geographical area and has diverse landscapes, climates, societies, cultures, religions, and economies. More than 50% of the world's population lives in this region. The region is also home to a large number of oil and gas refineries, which are the primary source of sulfur. This resulted in a high demand for sulfur recovery technologies, such as Claus and Tail Gas Treating Units.

The region is home to a number of emerging economies, such as India and China, which are investing heavily in the oil and gas sector. This has resulted in increased demand for sulfur recovery technologies due to the need to reduce environmental impact. The region is also home to several large-scale petrochemical projects, which require sulfur recovery technologies in order to meet their environmental standards.

Asia-Pacific is one of the fastest-growing regions in the world, owing to the presence of emerging countries, like India and China, and developed countries, such as Japan, South Korea, and Australia. In 2023, China was the world's second-largest oil consumer and the sixth-largest oil producer. The country imported nearly 50% of its hydrocarbon demand to reduce dependence on imports and improve energy security. Asia-Pacific is one of the significant regions in the sulfur recovery technologies market and is likely to continue its dominance owing to the rapid growth in energy-intensive industries like refineries.

China has been trying to maximize its shale potential by exploiting its domestic reserves across various inland shale basins, such as the Sichuan Basin. Shale gas development in China has increased steadily over the past few years, recording a growth of 21% annually since 2017. In 2023, China produced 232.43 billion cubic meters of natural gas.

Sulfur recovery technologies are crucial for India's oil refining and petrochemical industries to reduce harmful sulfur emissions and produce cleaner fuels. In March 2022, Thermax Ltd, an Indian multinational engineering company, concluded a USD 149.02 million order from an Indian public sector refinery to set up a sulfur recovery block as a part of the Government's North East Hydrocarbon Vision 2030.

In February 2024, Malaysia's state-owned Petronas, through Malaysia Petroleum Management, signed production sharing contracts (PSCs) for two discovered resource opportunity clusters with potential gas reserves offshore peninsular Malaysia. The BIGST DRO cluster has an estimated recovery of 4 trillion cubic feet and was awarded to Petronas Carigali and upstream firm JX Nippon Oil and Gas Exploration, each with a 50% participating interest. The cluster is made up of five undeveloped high-CO2 gas fields, namely the Bujang, Inas, Guling, Sepat, and Tujoh fields.

Hence, Asia-Pacific is expected to dominate the market due to its large oil and gas refining industry and increasing demand for cleaner fossil fuels.

Sulphur Recovery Technologies Industry Overview

The sulfur recovery technologies market is semi-fragmented. Some of the key players in this market (not in particular order) include Enersul Limited Partnership, WorleyParsons Limited, Shell PLC, Bechtel Corporation, and Fluor Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

4.1 Introduction

4.2 Market Size and Demand Forecast in USD billion, till 2029

4.3 Refinery Installed Capacity and Forecast, Till 2029

4.4 Allowed Sulphur Content in Refined Products in Million Tons Per Year, Till 2029

4.5 Recent Trends and Developments

4.6 Government Policies and Regulations

4.7 Market Dynamics

4.7.1 Drivers

4.7.1.1 Growing Environmental Concerns and Strict Norms on Pollution

4.7.2 Restraints

4.7.2.1 Limitations of Sulphur Recovery Process

4.8 Supply Chain Analysis

4.9 Porter's Five Forces Analysis

4.9.1 Bargaining Power of Suppliers

4.9.2 Bargaining Power of Consumers

4.9.3 Threat of New Entrants

4.9.4 Threat of Substitutes Products and Services

4.9.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

5.1 Application

5.1.1 Refineries

5.1.2 Gas Processing Plants

5.1.3 Power Plants

5.1.4 Others

5.2 Geography

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Rest of North America

5.2.2 Asia-Pacific

5.2.2.1 India

5.2.2.2 China

5.2.2.3 South Korea

5.2.2.4 Japan

5.2.2.5 Malaysia

5.2.2.6 Thailand

5.2.2.7 Indonesia

5.2.2.8 Vietnam

5.2.2.9 Rest of Asia-Pacific

5.2.3 Europe

5.2.3.1 Germany

5.2.3.2 France

5.2.3.3 United Kingdom

5.2.3.4 Spain

5.2.3.5 NORDIC

5.2.3.6 Turkey

5.2.3.7 Russia

5.2.3.8 Rest of Europe

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Colombia

5.2.4.4 Rest of South America

5.2.5 Middle-East and Africa

5.2.5.1 United Arab Emirates

5.2.5.2 Saudi Arabia

5.2.5.3 Nigeria

5.2.5.4 Oman

5.2.5.5 South Africa

5.2.5.6 Egypt

5.2.5.7 Algeria

5.2.5.8 Rest of Middle East & Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Market Share Analysis

6.4 Company Profiles

6.4.1 Enersul Limited Partnership

6.4.2 Worley Limited

6.4.3 Shell Plc

6.4.4 Bechtel Corporation

6.4.5 Fluor Corporation

6.4.6 Sulfur Recovery Engineering Inc.

6.4.7 Honeywell UOP

6.4.8 Air Liquide S.A.

6.5 List of Other Prominent Companies (Company Name, Headquarters, Revenue, Relevant Products and Services, Operating Sector, Recent Trends, Technology or Projects, Contact Details, etc.)

6.6 Market Ranking Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Untapped Oil And Gas Potential In Emerging Markets