ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

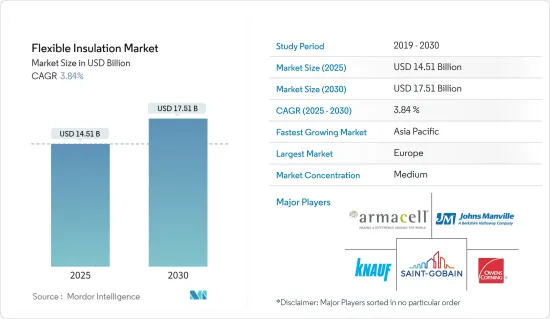

플렉서블 단열재 시장 규모는 2025년에 145억 1,000만 달러로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 3.84%로 성장할 전망이며, 2030년에는 175억 1,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

건설 업계의 에너지 효율에 대한 요구 증가 및 플렉서블 배관 단열재의 용도 확대가 향후 몇 년간의 플렉서블 단열재 시장을 견인할 것으로 예상됩니다.

그러나 더 나은 대체품을 사용할 수 있다는 것은 시장 성장을 방해할 것으로 예상됩니다.

전기자동차에서 에어로겔 단열재의 새로운 기회가 예측 기간 동안 시장에 기회를 가져올 것으로 기대됩니다.

유럽이 시장을 독점할 것으로 예상되지만, 아시아태평양은 중국, 인도, 일본 등 국가에서의 소비 증가로 인해 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

플렉서블 단열재 시장 동향

유리 섬유 단열재 수요 증가

유리 섬유는 얇은 유리 섬유와 고온 바인더의 매우 강력한 결합으로 구성됩니다. 이러한 섬유(1개의 직경은 거의 6-7미크론)는 수백만의 작은 공기 포켓을 가두도록 분포되어 있어 뛰어난 단열성과 차음성을 만들어내고 있습니다. 섬유 유리는 화학적으로 불활성이며, 철 샷, 황, 염화물 등의 불순물은 포함되어 있지 않습니다.

부식성이 없고 곰팡이의 발생도 없습니다. 그것은 신재생 원료로 제조되며 제조의 모든 단계에서 환경 친화적입니다. 담요(배트 및 롤) 및 루즈필과 같은 다양한 형태의 단열재에 사용되며 경질 보드 및 덕트 단열재로도 사용할 수 있습니다. 유리 섬유 단열재는 모래, 석회석, 소다 재, 재생 유리 칼렛을 혼합하여 제조됩니다.

두 유형의 유리 섬유가 주택, 상업시설, 인프라 건설에 널리 사용됩니다. 하나는 섬유상이며, 유연한 담요, 경질 보드, 파이프 단열재, 기타 미리 성형된 형상이 있습니다. 불연성으로 흡음성이 우수합니다. 또 하나는 셀룰러 유형으로, 보드 형상이나 블록 형상의 것이 있어, 파이프 단열재나 다양한 형상으로 가공할 수 있습니다. 구조 강도는 높지만 내충격성은 낮습니다. 이 소재는 불연성, 비 흡수성이며 많은 화학 약품에 내성이 있습니다. 주로 산업용 오븐, 열교환기, 건조기, 보일러, 배관 등의 단열에 사용됩니다.

미국과 같은 국가에서는 건설 활동이 증가하고 있으며, 이는 유리 섬유로 만들어진 플렉서블 단열재에 대한 수요를 증가시키고 있습니다. 예를 들어 미국 인구조사국에 따르면 2023년 미국의 연간 건설액은 1조 9,787억 달러로 2022년에 비해 약 7.03% 증가하고 있습니다.

섬유상 유리 단열재는 판금 덕트, 하우징, 플레넘의 외장에 사용됩니다. 반 경질에서 단단한 보드를 형성하고 냉동기 및 기타 냉열 장비의 단열에도 적합합니다. 0°F(-18°C)-450°F(232°C)의 온도 범위에서 사용할 수 있습니다.

최근에는 유리 섬유 제조에 재활용 창유리, 자동차 유리, 병 유리를 사용하는 경우가 늘고 있습니다. 시장에서 이용할 수 있는 재활용 원료의 양은 재활용 함량에 제한을 두고 있습니다. 재활용 재료의 사용은 단열 제품 제조에 필요한 에너지를 꾸준히 줄이는 데 도움이 됩니다.

위의 요인들로부터, 유리 섬유 단열재 수요는 예측 기간 동안 더 늘어날 것으로 예상됩니다.

시장을 독점하는 유럽

유럽은 플렉서블 단열재의 최대 시장이 될 것으로 예상됩니다. 건축물의 효율을 높이기 위한 EU 지침에 따른 엄격한 건축물 에너지 규제는 이 지역에서 플렉서블 단열재 수요를 촉진할 것으로 예상됩니다.

독일과 같은 국가의 건설 부문에서 플렉서블 단열재에 대한 왕성한 수요는 플렉서블 단열재 시장의 성장의 또 다른 이유입니다. 독일에서의 호텔 건설도 예측 기간 동안 급증할 전망입니다. 2022년에는 89개의 새로운 호텔과 15,780개의 객실이 출시되었으며, 2023년에는 78개의 프로젝트와 13,073개의 키가 추가로 계획되었습니다. 호텔 파이프라인은 2024년 이후에도 견조하게 추이할 것으로 예상되며 이미 153개 프로젝트, 22,769개실이 진행 중입니다.

또한 영국에서는 다양한 건설 프로젝트가 활발하게 진행되고 있으며 플렉서블 단열재에 대한 미래 수요가 높아질 것으로 예상됩니다. 예를 들어 뉴런던 아키텍처에 따르면 런던에서는 고층 빌딩이 540동 가까이 계획 및 건설 중이며 기존의 고층 빌딩 수는 360동입니다. 고층 빌딩의 건설이 증가하고 있다는 것은 조사된 시장을 견인할 것으로 추정됩니다.

프랑스에서는 건설 업계의 매출 지수가 지난 몇 년간 완만한 성장을 이어가고 있습니다. 이 나라의 건설 업계는 8년간 침체된 뒤 최근에 기세를 되찾았습니다. 생태연대이행성은 프랑스의 총 건축허가가 2023년 12월 33,765호에서 2024년 1월 26,585호로 증가한 것으로 나타났습니다.

유럽은 급속한 산업화와 주요 단열재 제조업체의 존재로 신흥 소재를 신속하게 채용하여 높은 제품 매출을 기록했습니다.

따라서 유럽에서 플렉서블 단열재 수요 증가가 예측 기간 동안 시장 조사를 촉진할 것으로 예상됩니다.

플렉서블 단열재 산업 개요

플렉서블 단열재 시장은 세분화되어 있습니다. 이 시장의 주요 기업으로는 Armacell, Knauf Group, Johns Manville, Owens Corning, Saint-Gobain 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 성장 촉진요인

건설 업계로부터의 에너지 효율화 요구 증가

플렉서블 배관용 단열재의 용도 확대

기타 촉진요인

시장 성장 억제요인

대체품의 이용가능성

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

소재별

에어로겔

가교 폴리에틸렌

엘라스토머

유리 섬유

기타 소재

단열 유형별

방음재

전기 절연

단열재

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

Altana AG

Armacell

Cabot Corporation

Etex Group

Fletcher Insulation

Johns Manville

Kingspan Group

Knauf Insulation

Owens Corning

Saint-Gobain

Superlon Holdings Berhad

Thermaxx Jackets

제7장 시장 기회 및 향후 동향

전기자동차에 있어서 에어로겔 단열재의 새로운 기회

기타 기회

AJY

영문 목차

영문목차

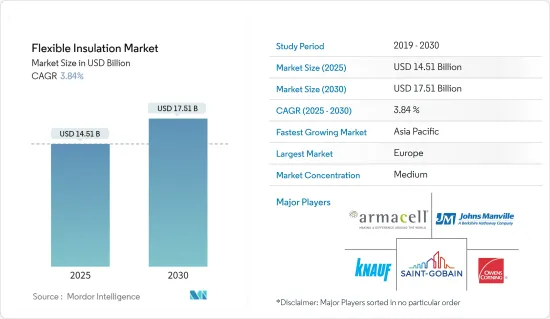

The Flexible Insulation Market size is estimated at USD 14.51 billion in 2025, and is expected to reach USD 17.51 billion by 2030, at a CAGR of 3.84% during the forecast period (2025-2030).

Key Highlights

The increasing demand for energy efficiency from the construction industry and the increasing application of flexible piping insulation are expected to drive the flexible insulation market in the coming years.

However, the availability of better alternatives is expected to hinder the growth of the market.

Emerging opportunities for aerogel insulation in electric vehicles are expected to create opportunities for the market during the forecast period.

Europe is expected to dominate the market, while Asia-Pacific is expected to register the highest CAGR owing to the increasing consumption from countries such as China, India, and Japan.

Flexible Insulation Market Trends

Rising Demand for Fiberglass Insulation

Fiberglass consists of extremely strong bonds between thin glass fibers and a high-temperature binder. These fibers (each of nearly 6-7 microns in diameter) are distributed to trap millions of tiny pockets of air in them, thereby creating excellent thermal and acoustic insulation. Fiberglass is chemically inert and has no impurities, such as iron shots, sulfur, or chloride.

The product is non-corrosive and does not support mold growth. It is manufactured from renewable raw materials and is eco-friendly in every stage of manufacturing. It is used in different forms of insulation, such as blankets (batts and rolls) and loose-fill, and is also available as rigid boards and duct insulation. Fiberglass insulation is manufactured with a blend of sand, limestone, soda ash, and recycled glass cullet.

Two types of fiberglass are extensively used in residential, commercial, and infrastructural construction. One is the fibrous one, which is available in flexible blankets, rigid boards, pipe insulation, and other pre-molded shapes. It is non-combustible and has good sound absorption qualities. The second one is the cellular type, which is available in board and block forms and capable of being fabricated into pipe insulation and various shapes. It has good structural strength but poor impact resistance. The material is non-combustible, non-absorptive, and resistant to many chemicals. It is mainly used to insulate industrial ovens, heat exchangers, driers, boilers, and pipe work.

Construction activities are increasing in countries like the United States, which is increasing the demand for fiberglass flexible insulation. For instance, according to the US Census Bureau, the annual value for construction in the United States accounted for USD 1,978.7 billion in 2023, which is an increase of about 7.03% compared to that of 2022.

Fibrous glass insulation is applied to the exterior of sheet metal ducts, housings, and plenums. It forms semi-rigid to rigid boards that are also suitable for insulating chillers and other cold or hot equipment. It can be used in applications within the temperature range of 0°F (-18°C) to 450°F (232°C).

In recent times, recycled windows and automotive or bottle glass have been increasingly used in the manufacture of glass fiber. The amount of usable recycled material available in the market limits the recycled content. The use of recycled material has helped to reduce the energy required to produce insulation products steadily.

Owing to the above-mentioned factors, the demand for fiberglass insulation is expected to grow further over the forecast period.

Europe to Dominate the Market

Europe is projected to be the largest market for flexible insulation. Stringent building energy codes accompanied by EU Directives to enhance efficiency in buildings are expected to drive the demand for flexible insulation in the region.

Robust demand for flexible insulation from the construction sector in countries like Germany is another reason for the growth of the flexible insulation market. The construction of hotels in Germany is also expected to witness a sharp rise during the forecast period. The year 2022 witnessed the launch of 89 new hotels and 15,780 rooms, and 78 more projects with 13,073 keys were mooted for 2023. The pipeline of hotels is anticipated to stay strong for 2024 and beyond, with 153 projects and 22,769 rooms already in the works.

Moreover, various construction projects are active in the United Kingdom, which is expected to enhance the future demand for flexible insulation. For instance, according to New London Architecture, there are nearly 540 planned and under construction high-rise buildings in London, with an existing number of 360 tall buildings. The growing construction of high-rise buildings is estimated to drive the market studied.

In France, the construction index has been witnessing slow growth, with a gradual increase in the industry turnover index over the past few years. The construction industry in the country recently gained momentum after eight long years of decline. The Ministere de la Transition ecologique et solidaire revealed an increase in total building permits in France to 26,585 Units in January 2024 from 33,765 Units in December 2023.

Europe was an early adopter of emerging materials on account of rapid industrialization and the presence of major insulation product manufacturers, thus leading to high product sales.

Thus, the growing demand for flexible insulation in the Europe region is expected to drive the market studied during the forecast period.

Flexible Insulation Industry Overview

The flexible insulation market is fragmented in nature. Some of the major players in the market include (not in any particular order) Armacell, Knauf Group, Johns Manville, Owens Corning, and Saint-Gobain, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Drivers

4.1.1 Increasing Demand for Energy Efficiency from the Construction Industry

4.1.2 Increasing Application of Flexible Piping Insulation

4.1.3 Other Drivers

4.2 Market Restraints

4.2.1 Availability of Alternatives

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 By Material

5.1.1 Aerogel

5.1.2 Cross-Linked Polyethylene

5.1.3 Elastomer

5.1.4 Fiberglass

5.1.5 Other Materials

5.2 By Insulation Type

5.2.1 Acoustic Insulation

5.2.2 Electrical Insulation

5.2.3 Thermal Insulation

5.3 By Geography

5.3.1 Asia - Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Market Ranking Analysis

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 Altana AG

6.3.2 Armacell

6.3.3 Cabot Corporation

6.3.4 Etex Group

6.3.5 Fletcher Insulation

6.3.6 Johns Manville

6.3.7 Kingspan Group

6.3.8 Knauf Insulation

6.3.9 Owens Corning

6.3.10 Saint-Gobain

6.3.11 Superlon Holdings Berhad

6.3.12 Thermaxx Jackets

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Emerging Opportunity for Aerogel Insulation in Electric Vehicles