가스 분리막 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Gas Separation Membrane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1689955

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

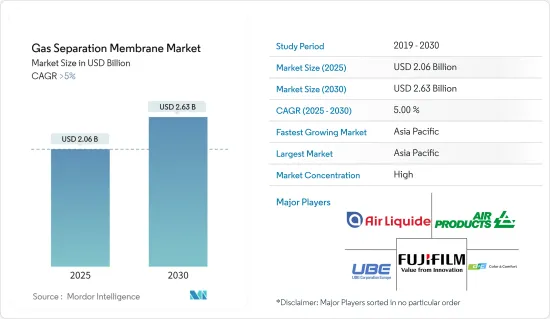

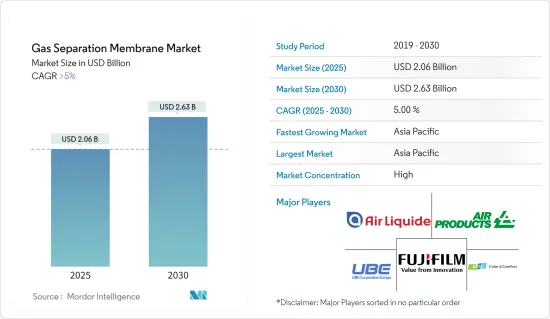

가스 분리막 시장 규모는 2025년에 20억 6,000만 달러로 추정되고, 2030년에는 26억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 중 2025년부터 2030년까지 CAGR은 5%를 초과할 것으로 예측되고 있습니다.

COVID-19 팬데믹은 가스 분리막 시장에 부정적인 영향을 미쳤습니다. 팬데믹은 세계 공급망을 혼란스럽게 하여 가스 분리막의 제조에 필요한 원재료, 부품, 장치의 입수에 영향을 주었습니다. 생산과 출하 지연은 막 시스템과 구성 요소의 일시적인 부족으로 이어졌습니다. 그러나 각국이 점차 봉쇄 규제를 해제함에 따라 가스 분리막 시스템 수요가 회복되기 시작했습니다.

주요 하이라이트

이산화탄소 분리 공정에서의 막 수요 증가 및 온실가스 배출에 대한 엄격한 정부 규제가 가스 분리막 시장을 견인할 것으로 예상됩니다.

그러나 고온 용도에서 고분자막의 가소화, 새로운 막의 스케일 업과 채용이 가스 분리막 시장의 성장을 방해할 것으로 예상됩니다.

또한, 혼합 매트릭스 막(MMM)과 용도를 확대하는 고분자막의 개발은 시장 개척에 새로운 기회를 제공할 것으로 예상됩니다.

아시아태평양은 조사한 시장에서 지역별로 가장 큰 점유율을 차지하고 있습니다. 중국, 인도, 일본의 가스 분리막 수요 증가로 예측 기간 동안 가장 빠르게 성장하는 시장이 될 것으로 예상됩니다.

가스 분리막 시장 동향

질소 생성 및 산소 부화 부문이 시장을 독점

질소 생성 및 산소 부화는 다양한 산업 분야에서 필수적인 공정입니다. 석유 및 가스, 화학, 일렉트로닉스, 식음료, 의약품 등의 산업에서는 담요, 퍼지, 불활성화, 패키징 등을 위해 질소가 필요합니다. 동시에, 산소 농축은 연소, 발효, 폐수 처리 등의 공정에 필요합니다.

가스 분리막을 이용한 질소 생성과 산소 농축은 현장에서의 가스 제조를 가능하게 하고, 압축 가스나 액화 가스의 수송, 저장, 취급을 불필요하게 합니다. 이를 통해 물류 비용을 줄이고 공급망의 신뢰성을 높이고 산업 운영의 안전성을 높일 수 있습니다.

질소는 식품 및 식품 산업에서 식품 포장의 산소를 대체하여 보존 기간을 연장하고 신선도를 유지하는 데 사용됩니다. 배럴을 가압하고 맥주와 소다와 같은 탄산 음료를 공급하는 데에도 사용됩니다. 식품 가공 작업에서 질소는 불활성화, 담요화, 저온화 및 냉동에 사용됩니다.

중국의 맥주 산업도 세계적으로 가장 빠르게 확대되고 있으며, 그 총 매출은 2023년 말까지 약 1,315억 달러에 달할 전망입니다.

질소와 산소는 전자 산업에도 응용되고 있습니다. 질소는 오염을 방지하고 정확한 대기 조건을 유지하기 위해 반도체 제조 공정에서 캐리어 가스로 사용됩니다. 또한 웨이브 납땜, 리플로우 납땜, 등각 코팅 공정에도 사용되어 납땜 품질을 향상시키고 산화를 방지합니다.

반도체산업협회가 발표한 보고서에 따르면 2023년 11월 세계 반도체 매출은 전년 대비 5.3% 증가했습니다.

산소 부화는 제철, 제련, 비철금속 정련과 같은 야금 공정으로 연소 효율 향상, 연료 소비 감소, 공정 생산성 향상을 위해 사용됩니다.

따라서 가스 분리막 수요가 증가하고 시장 조사에 긍정적인 영향을 미칠 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양에는 인도, 중국, 일본, 한국 및 기타 동남아시아 국가 등 빠르게 성장하는 국가가 있습니다. 이들 국가들은 현저한 산업 성장을 이루고 있으며, 석유 및 가스, 화학, 일렉트로닉스, 헬스케어, 식음료 등 다양한 분야에서 가스 분리막 기술 수요를 견인하고 있습니다.

아시아태평양은 화학, 일렉트로닉스, 반도체, 자동차, 소비재를 생산하는 다양한 산업을 보유한 제조업 중심지입니다. 가스 분리막은 많은 제조 공정에서 필수적인 부품이며, 이 지역에서 높은 수요로 이어지고 있습니다.

세계 철강 기관에 따르면 2023년 12월 중국의 철강 생산량은 67.4톤이었습니다. 한편 인도는 세계 2위인 조강생산국에 올랐습니다. 이 나라는 2022-2023 회계연도에 602만 톤을 수입하는 반면 672만 톤의 완성강을 수출했습니다.

게다가 반도체 협회에 따르면 2024년 1월 중국의 반도체 매출은 147억 6,000만 달러로 급증하여 전년부터 현저한 성장세를 보였습니다. 2023년 1월 매출액이 116억 6,000만 달러였던 것에 비하면 이것은 상당한 급상승입니다.

또한, 이 지역 산성 가스 분리 시장에서의 가스 분리막 수요는 이 지역 에너지 생산의 상승에 의해 자극될 것으로 예상됩니다.

가스 분리막 산업 개요

가스 분리막 시장은 부분적으로 통합되어 소수의 대기업이 시장을 독점하고 있습니다. 시장에 진입하는 주요 기업으로는 Air Products and Chemicals Inc., UBE Corporation, Air Liquide Advanced Separations, DIC Corporation, FUJIFILM Corporation 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건 및 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

이산화탄소 분리 공정에서 막 수요 증가

온실가스 배출에 대한 정부의 엄격한 규범

성장 억제요인

고온 용도에 있어서 폴리머막의 가소화

새로운 막의 대규모화 및 채용

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

재료 유형별

폴리이미드 및 폴리아미드

폴리설폰

셀룰로오스 아세테이트

기타 재료 유형(나노 구조막)

용도별

질소 생성 및 산소 부화

수소 회수

이산화탄소 제거

황화수소 제거

기타 용도(탄산화)

지역별

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

터키

러시아

노르딕

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

나이지리아

카타르

이집트

아랍에미리트(UAE)

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율(%)** 및 랭킹 분석

주요 기업의 전략

기업 프로파일

Air Liquide Advanced Separations

Air Products and Chemicals Inc.

DIC CORPORATION

Evonik Industries AG

FUJIFILM Corporation

GENERON

Honeywell International Inc.

Linde PLC

Membrane Technology and Research Inc.

Parker Hannifin Corp.

SLB(schlumberger)

Toray Industries Inc.

UBE Corporation

제7장 시장 기회 및 향후 동향

혼합 매트릭스막(MMM) 개발

고분자막의 개발 및 용도 확대

AJY

영문 목차

영문목차

The Gas Separation Membrane Market size is estimated at USD 2.06 billion in 2025, and is expected to reach USD 2.63 billion by 2030, at a CAGR of greater than 5% during the forecast period (2025-2030).

The COVID-19 pandemic negatively affected the gas separation membrane market. The pandemic disrupted the global supply chain, which affected the availability of raw materials, components, and equipment for manufacturing gas separation membranes. Delays in production and shipping led to temporary shortages of membrane systems and components. However, as countries gradually lifted lockdown restrictions, demand for gas separation membrane systems started to rebound.

Key Highlights

The rising demand for membranes in carbon dioxide separation processes and strict government regulations for GHG emissions are expected to drive the gas separation membrane market.

However, the plasticization of polymeric membranes in high-temperature applications and the upscaling and adoption of new membranes are expected to hamper the market growth of gas separation membranes.

Furthermore, developing mixed matrix membranes (MMMs) and polymeric membranes with expanding applications is projected to provide new opportunities for the market studied.

Asia-Pacific holds the largest share by geography in the market studied. It is expected to be the fastest-growing market over the forecast period due to the rising demand for gas separation membranes in China, India, and Japan.

Gas Separation Membrane Market Trends

The Nitrogen Generation and Oxygen Enrichment Segment to Dominate the Market

Nitrogen generation and oxygen enrichment are essential processes in various industrial applications. Industries such as oil and gas, chemicals, electronics, food and beverage, and pharmaceuticals require nitrogen for blanketing, purging, inerting, and packaging. At the same time, oxygen enrichment is necessary for processes such as combustion, fermentation, and wastewater treatment.

Nitrogen generation and oxygen enrichment using gas separation membranes enable onsite gas production, eliminating the need for transportation, storage, and handling of compressed or liquified gases. This reduces logistic costs, enhances supply chain reliability, and improves safety in industrial operations.

Nitrogen is used in the food and beverage industry to displace oxygen in food packaging to extend the shelf life and preserve freshness. It is used to pressurize kegs and dispense carbonated beverages like beer and soda. In food processing operations, nitrogen is used for inerting, blanketing, cryogenic, and freezing.

China's beer industry is also experiencing the quickest expansion globally, with its total revenue reaching about USD 131.5 billion by the close of 2023.

Nitrogen and oxygen find applications in the electronics industry. Nitrogen is used as a carrier gas in semiconductor fabrication processes to prevent contamination and maintain precise atmospheric conditions. It is also used for wave soldering, reflow soldering, and conformal coating processes to improve soldering quality and prevent oxidation.

According to the report released by the Semiconductor Industry Association, global semiconductor sales increased by 5.3 % year-to-year in November 2023.

Oxygen enrichment is used in metallurgical processes such as steelmaking, iron smelting, and non-ferrous metal refining to increase combustion efficiency, reduce fuel consumption, and improve process productivity.

Therefore, the demand for gas separation membranes is expected to increase and thus have a positive impact on the market studied.

Asia-Pacific to Dominate the Market

Asia-Pacific is home to rapidly growing countries such as India, China, Japan, South Korea, and other Southeast Asian countries. These countries are experiencing significant industrial growth, driving demand for gas separation membrane technologies across various sectors, including oil and gas, chemicals, electronics, healthcare, and food and beverage.

Asia-Pacific is a central manufacturing hub with a diverse range of industries producing chemicals, electronics, semiconductors, automobiles, and consumer goods. Gas separation membranes are essential components in many manufacturing processes, leading to high demand in the region.

According to the World Steel Organization, in December 2023, China produced 67.4 metric tons of steel. Meanwhile, India has risen to become the second-largest producer of crude steel globally. The country exported 6.72 million metric tons of finished steel while only importing 6.02 million metric tons in the fiscal year 2022-23.

Furthermore, according to the Semiconductor Association, in January 2024, China's semiconductor sales soared to USD 14.76 billion, marking a notable rise from the previous year. This is a considerable jump compared to the sales in January 2023, which stood at USD 11.66 billion.

In addition, the demand for gas separation membranes in the region's acid gas separation market is expected to be stimulated by the rising energy production in this area.

Gas Separation Membrane Industry Overview

The gas separation membrane market is partially consolidated in nature, with a few major players dominating the market. The major companies operating in the market include Air Products and Chemicals Inc., UBE Corporation, Air Liquide Advanced Separations, DIC Corporation, and FUJIFILM Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand for Membranes in Carbon Dioxide Separation Processes

4.1.2 Strict Government Norms Toward GHG Emissions

4.2 Restraints

4.2.1 Plasticization of Polymeric Membranes in High-temperature Applications

4.2.2 Upscaling and Adoption of New Membranes

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

5.1 Material Type

5.1.1 Polyimide and Polyamide

5.1.2 Polysulfone

5.1.3 Cellulose Acetate

5.1.4 Other Material Types (Nanostructured Membrane)

5.2 Application

5.2.1 Nitrogen Generation and Oxygen Enrichment

5.2.2 Hydrogen Recovery

5.2.3 Carbon Dioxide Removal

5.2.4 Removal of Hydrogen Sulphide

5.2.5 Other Applications (Carbonation)

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Spain

5.3.3.6 Turkey

5.3.3.7 Russia

5.3.3.8 NORDIC

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Nigeria

5.3.5.4 Qatar

5.3.5.5 Egypt

5.3.5.6 UAE

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Air Liquide Advanced Separations

6.4.2 Air Products and Chemicals Inc.

6.4.3 DIC CORPORATION

6.4.4 Evonik Industries AG

6.4.5 FUJIFILM Corporation

6.4.6 GENERON

6.4.7 Honeywell International Inc.

6.4.8 Linde PLC

6.4.9 Membrane Technology and Research Inc.

6.4.10 Parker Hannifin Corp.

6.4.11 SLB (schlumberger)

6.4.12 Toray Industries Inc.

6.4.13 UBE Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Development of Mixed Matrix Membranes (MMM)

7.2 Development in Polymeric Membranes and Expanding Applications