ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

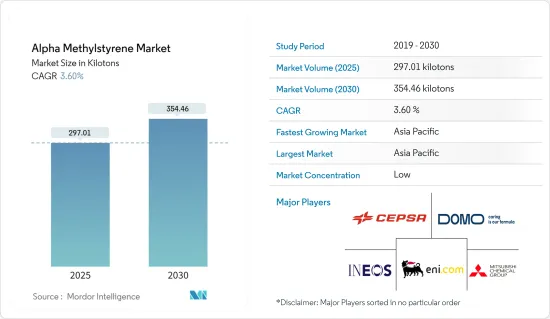

알파 메틸스티렌 시장 규모는 2025년에 297.01킬로톤으로 추정되고, 예측 기간 2025년부터 2030년까지 CAGR 3.6%로 성장할 전망이며, 2030년에는 354.46킬로톤에 이를 것으로 예측됩니다.

COVID-19는 모든 산업이 제조 공정을 중단했기 때문에 시장에 부정적인 영향을 미쳤습니다. 봉쇄, 사회적 거리두기, 무역 제재가 세계 공급망 네트워크에 대규모 혼란을 일으켰습니다. 그러나 이 상황은 2021년에는 회복되었으며, 예측 기간 동안 시장에 이익을 가져올 것으로 예상됩니다.

주요 하이라이트

중기적으로는 ABS 수지의 제조 수요 증가 및 전자 분야에서 알파 메틸스티렌 수요 증가가 시장을 견인하는 주요 요인입니다.

반면에 알파 메틸스티렌 제조 시 배출되는 유해폐기물이 시장 성장을 억제할 가능성이 높습니다.

내구성 있는 왁스와 내열성 접착제에 대한 수요 증가는 앞으로 수년간 시장에 호기가 될 전망입니다.

아시아태평양이 가장 높은 시장 점유율을 차지하고 있으며 예측 기간 동안 이 지역이 시장을 독점할 가능성이 높습니다.

알파 메틸스티렌 시장 동향

자동차 산업이 시장을 독점

알파 메틸스티렌은 ABS 수지 제조의 중간체입니다. 또한, ABS 수지는 자동차 산업에서 금속의 대안으로 사용됩니다. 경량화를 추구하는 다양한 자동차 부품에 ABS 수지가 사용되고 있습니다. ABS는 일반적으로 대시보드 부품, 시트백, 안전벨트 부품, 핸들, 도어 로너, 필러 트림, 계기판 등의 부품에 사용됩니다.

OICA(Organization Internationale des Constructeurs d'Automobiles)에 따르면 세계 자동차 생산 대수는 2022년 8,501만 대에 이르렀으며, 2021년 8,020만 대에 비해 6%의 성장률을 보였습니다.

게다가 전기차 생산량 증가는 시장 조사 시장 수요를 높일 가능성이 높습니다. 예를 들어 EV Volumes에 따르면 2022년에는 총 1,050만 대의 BEV와 PHEV가 새롭게 납품되어 2021년에 비해 55% 증가했습니다.

아시아태평양은 세계에서 가장 가치있는 자동차 제조 업체의 본거지입니다. 중국, 인도, 일본, 한국 등 신흥 국가들은 제조거점을 강화하고 효율적인 공급망을 구축하고 수익성을 높이기 위해 노력해 왔습니다.

중국 자동차공업협회(CAAM)에 따르면 중국은 세계 최대의 자동차 생산 거점이며, 2022년의 자동차 총 생산 대수는 2,720만 대로, 작년의 2,610만 대에서 3.4% 증가했습니다.

유럽에서는 독일이 중요한 자동차 제조업체 중 하나입니다. 독일 자동차공업회(VDA)에 따르면 독일의 2022년 7월 자동차 생산 대수는 26만 3,400대로 2021년 동기 대비 7%의 성장을 기록했습니다. 또한 독일에서는 전기차 수요가 증가하고 있습니다. 따라서 다양한 기업들이 이 나라에서 전기차 생산량을 늘리고 있습니다. 예를 들어, 2023년 6월, 포드는 독일의 하이테크 생산 시설인 쾰른 전기자동차 센터의 낙성을 발표했습니다.

북미에서는 OICA에 따르면 2022년 자동차 생산 대수는 1,770만 대로 2021년 약 1,610만 대에 비해 10% 증가했습니다.

이 때문에 예측기간 동안 자동차 생산 확대와 함께 알파 메틸스티렌 수요도 증가할 것으로 예상됩니다.

아시아태평양이 알파 메틸스티렌 시장을 독점

아시아태평양은 알파 메틸스티렌 시장에서 세계적으로 눈에 띄는 점유율을 차지하고 있으며 예측 기간 동안에도 시장을 독점할 것으로 예상됩니다.

국가 통계국이 발표한 데이터에 따르면 중국의 타이어 산업은 상당한 성장을 이루고 있으며, 이는 국내 및 국제 시장에서의 타이어 수요 증가를 반영합니다.

중국 국가 통계국에 따르면 2023년 5월 현재 중국 플라스틱 제품의 월간 생산량은 약 600만 톤이었습니다. 2020년 1월 이후 플라스틱 제품의 월간 생산량이 가장 많았던 것은 2021년 12월 795만 톤이었습니다.

또한, 중국은 화학 가공의 허브이며 세계 화학제품의 대부분을 차지하고 있습니다. 세계 최대의 화학제품 시장인 중국에서는 2023년에는 화학제품 생산의 성장이 약간 둔화된 것으로 평가되었습니다. 러시아와 우크라이나 전쟁에 이어 화학산업은 2022년 에너지와 원재료 비용 상승, 유통, 경제 불확실성, 정치적 혼란에 의해 이미 긴장된 세계 공급망이 더욱 병목 현상이 되는 것을 경험했습니다. BASF의 화학산업 아웃룩에 따르면 2023년 중국의 화학생산은 5.9%의 감소가 된 것으로 평가되었습니다. 그러나 새로운 화학 플랜트 건설에 대한 투자가 증가하고 있으며 중기적으로 AMS 수요를 지원합니다.

인도는 아시아태평양에서 중국에 이은 고무의 최대 생산국 및 소비국 중 하나입니다. 인도에서는 생산되는 고무의 65% 이상이 자동차용 타이어(50%)와 자전거용 타이어 튜브(15%)의 제조에 사용되고 있습니다. 게다가 이 나라에는 66개 가까운 타이어 생산 공장과 약 41개의 타이어 생산 기업이 있습니다.

IBEF에 따르면 2022년 4-9월 플라스틱 수출 총액은 63억 8,000만 달러였습니다. 이 기간 동안 플라스틱 원료, 의료품, 파이프 및 피팅 수출은 전년 동기 대비 32.3%, 24.8%, 17.9% 증가했습니다.

이런 식으로 다양한 산업 수요 증가는 예측 기간 동안 이 지역에서 조사된 시장을 홍보할 것으로 예상됩니다.

알파 메틸스티렌 산업 개요

알파 메틸스티렌 시장은 세분화되어 있습니다. 시장의 주요 기업으로는 ENI SpA, INEOS, Cepsa, Mitsubishi Chemical, Domo Chemicals 등이 있습니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

ABS 수지 제조 수요 증가

전자 분야에서 알파 메틸스티렌 수요 증가

성장 억제요인

알파 메틸스티렌 제조시 유해폐기물 배출

기타 억제요인

산업 밸류체인 분석

Porter's Five Forces 분석

신규 참가업체의 위협

구매자의 협상력

공급기업의 협상력

대체품의 위협

경쟁도

제5장 시장 세분화

용도별

ABS 제조

플라스틱 첨가제 및 중간체

접착제

코팅제

기타 용도

최종 사용자 산업별

타이어

자동차

일렉트로닉스

플라스틱

기타 최종 사용자 산업

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

세계 기타 지역

남미

중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 점유율(%) 및 랭킹 분석

주요 기업의 전략

기업 프로파일

AdvanSix

Altivia

Cepsa

Chang Chun Group

Deepak

Domo Chemicals

Eni SPA

INEOS

Kraton Corporation

Kumho P&B Chemicals.,inc.

Mitsubishi Chemical Corporation

Prasol Chemicals Limited

Rosneft

Seqens

SI Group, Inc.

Solvay

Yangzhou Lida Chemical Co., Ltd.

제7장 시장 기회 및 향후 동향

내구성 왁스 및 내열성 접착제 수요 증가

기타 기회

AJY

영문 목차

영문목차

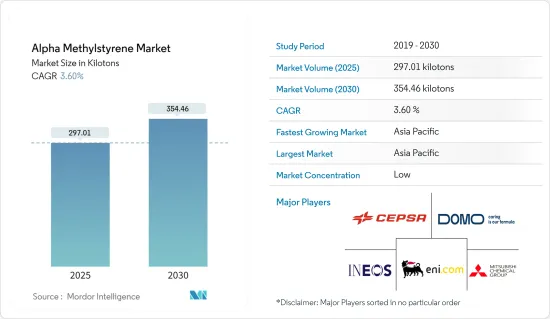

The Alpha Methylstyrene Market size is estimated at 297.01 kilotons in 2025, and is expected to reach 354.46 kilotons by 2030, at a CAGR of 3.6% during the forecast period (2025-2030).

COVID-19 negatively impacted the market as all the industries halted their manufacturing processes. Lockdowns, social distances, and trade sanctions triggered massive disruptions to global supply chain networks. However, the condition is recovered in 2021, which is expected to benefit the market during the forecast period.

Key Highlights

In the medium term, the major factors driving the market studied are the increasing demand for the manufacturing of ABS resins and increasing demand for alpha-methyl styrene in the electronics segment.

On the flip side, hazardous waste release during the production of alpha methyl styrene is likely to restrain the market growth.

Increase in demand for durable waxes and heat-resistant adhesives is likely to act as an opportunity for the market in coming years.

Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Alpha Methylstyrene Market Trends

Automotive Industry to Dominate the Market

Alpha methyl styrene is an intermediate for the production of ABS resin. Further, ABS resin is used as a replacement for metal in the automotive industry. Various automotive parts that look for weight reduction factors use ABS thermoplastic. ABS is commonly used for parts that include dashboard components, seat backs, seat belt components, handles, door loners, pillar trim, and instrument panels.

According to the Organization Internationale des Constructeurs d'Automobiles (OICA), global automotive vehicle production reached 85.01 million in 2022, with a growth rate of 6% as compared to 80.20 million vehicles manufactured in 2021, thereby indicating an increased demand for alpha methyl styrene from the automotive industry.

Furthermore, the rising production of electric vehicles is likely to enhance the market demand for the market-studied. For instance, according to the EV Volumes, a total of 10.5 million new BEVs and PHEVs were delivered during 2022, an increase of 55 % compared to 2021.

Asia-Pacific region is home to some of the world's most valuable vehicle manufacturers. Developing countries such as China, India, Japan, and South Korea have been working hard to strengthen the manufacturing base and develop efficient supply chains for greater profitability.

According to the China Association of Automobile Manufacturers (CAAM), China has the largest automotive production base in the world, with a total vehicle production of 27.2 million units in 2022, registering an increase of 3.4 % compared to 26.1 million units produced last year.

In Europe, Germany is among the vital manufacturer of vehicles. According to the German Association of the Automotive Industry (VDA), Germany produced 263,400 units of cars in July 2022, registering a growth rate of 7% compared to the same period in 2021. Additionally, the demand for electric cars is increasing in Germany. Thus, various companies are increasing the production volume of electric cars in the country. For instance, in June 2023, Ford announced the inauguration of the Cologne Electric Vehicle Center, a hi-tech production facility in Germany.

In North America, according to the OICA, automotive production in 2022 accounted for 17.7 million units, an increase of 10% compared to that in 2021, which was around 16.1 million units.

Therefore, the demand for alpha methyl styrene is expected to grow with the expanding automotive production during the forecast period.

Asia-Pacific to Dominate Alpha Methyl Styrene Market

Asia-Pacific holds a prominent share in the alpha-methylstyrene market globally and is expected to dominate the market during the period of forecast.

As per the data released by the National Bureau of Statistics, China's tire industry is experiencing substantial growth, reflecting the increasing demand for tires in the domestic as well as international markets.

According to the National Bureau of Statistics of China, as of May 2023, China produces roughly 6 million metric tons of plastic products monthly. Since January 2020, the highest monthly output of plastic products was recorded in December 2021, at 7.95 million metric tons.

Furthermore, China is a hub for chemical processing, accounting for a major chunk of global chemicals. In China, the world's largest chemicals market, a slight slowdown in chemical production growth is expected in 2023. Following Russia and Ukraine war, the chemical industry experienced a year marked by further bottlenecks in global supply chains already strained by rising energy and raw material costs, pandemic, economic uncertainty, and political turmoil in 2022. Continuing on the tumultuous grounds, China is expected to register a slightly weaker growth of 5.9% in chemical production in 2023, as per the BASF's chemical industry outlook. However, the increasing investments in the construction of new chemical plants support the demand for AMS in the mid-term.

India is one of the largest producers and consumers of rubber after China in the Asia-Pacific region. In India, over 65% of the rubber produced is used for manufacturing automotive (50%) and bicycle tires and tubes (15%). Moreover, the country has almost 66 tire-producing plants and about 41 tire-producing companies.

According to IBEF, total plastics exports between April-September 2022 stood at USD 6.38 billion. During this period, the exports of plastic raw materials, medical items, and pipes and fittings increased by 32.3%, 24.8%, and 17.9% over the same time last year.

Thus, rising demand from various industries is expected to drive the market studied in the region during the forecast period.

Alpha Methylstyrene Industry Overview

The alpha methyl styrene market is fragmented in nature. Some of the major companies in the market include ENI S.p.A., INEOS, Cepsa, Mitsubishi Chemical Corporation, and Domo Chemicals, among others.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Demand For the Manufacturing of ABS Resins

4.1.2 Increasing Demand For Alpha-methyl Styrene In the Electronics Segment

4.2 Restraints

4.2.1 Hazardous Waste Release During the Production of Alpha Methyl Styrene

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume and Value)

5.1 Application

5.1.1 ABS Manufacture

5.1.2 Plastic Additives and Intermediates

5.1.3 Adhesives

5.1.4 Coatings

5.1.5 Other Applications

5.2 End-user Industry

5.2.1 Tire

5.2.2 Automotive

5.2.3 Electronics

5.2.4 Plastics

5.2.5 Other End-user Industries

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 Rest of the World

5.3.4.1 South America

5.3.4.2 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share (%)/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 AdvanSix

6.4.2 Altivia

6.4.3 Cepsa

6.4.4 Chang Chun Group

6.4.5 Deepak

6.4.6 Domo Chemicals

6.4.7 Eni S.P.A.

6.4.8 INEOS

6.4.9 Kraton Corporation

6.4.10 Kumho P&B Chemicals.,inc.

6.4.11 Mitsubishi Chemical Corporation

6.4.12 Prasol Chemicals Limited

6.4.13 Rosneft

6.4.14 Seqens

6.4.15 SI Group, Inc.

6.4.16 Solvay

6.4.17 Yangzhou Lida Chemical Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Increase in Demand for Durable Waxes and Heat-resistant Adhesives