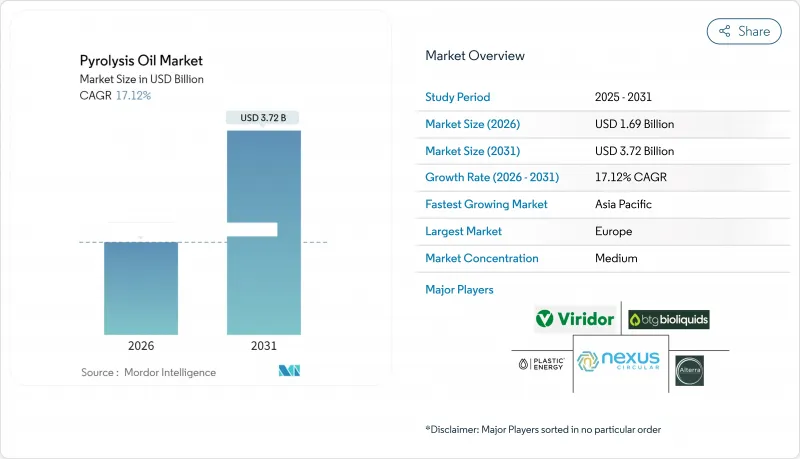

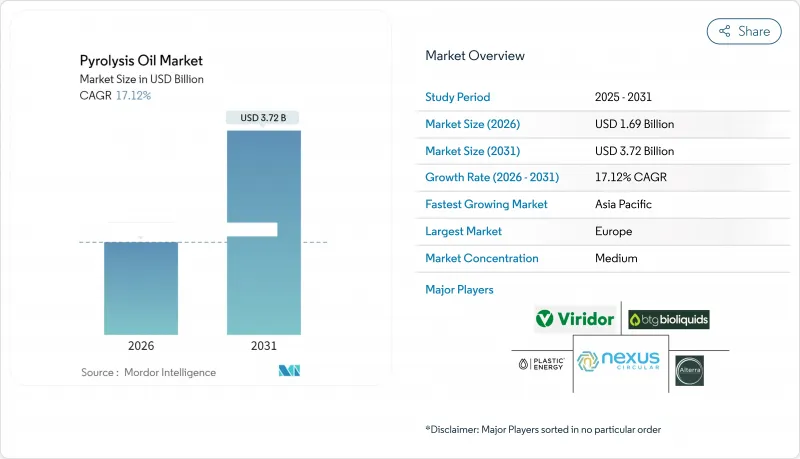

열분해유 시장은 2025년에 14억 4,000만 달러로 평가되었고, 2026년 16억 9,000만 달러에서 2031년까지 37억 2,000만 달러에 이를 것으로 예상되고 있습니다. 예측 기간(2026-2031년)에 있어서 CAGR은 17.12%를 나타낼 것으로 전망되고 있습니다.

플라스틱 폐기물 규제의 강화, 순환형 경제의 의무화 및 정유소에서의 공동처리 기술의 진전이 함께 수요를 가속화하고 있습니다. 한편, 두꺼운 탄소 신용 제도는 플랜트의 경제성을 향상시키고 있습니다. 유럽의 혁신 기금과 일본의 NEDO 프로그램으로부터의 전략적 자금 제공은 지원적인 정책 환경을 가진 지역으로 경쟁의 균형을 이행시키는 생산 능력의 증강을 지원하고 있습니다. 생산자는 자본 지출을 줄이고 판매 보증을 보장하기 위해 정유 업체와의 수직 통합을 추진하고 있습니다. 한편, 기술공여기업은 수율향상과 배출삭감을 실현하는 마이크로파 보조법이나 초임계법 등 상업화를 겨루고 있습니다. 동시에, 특히 다환 방향족 탄화수소(PAH)의 오염물질 관리는 사양에 중점을 둔 고객이 허용 한계를 엄격화하면서 주요 운영 과제로 남아 있습니다.

캘리포니아의 저탄소 연료 기준(LCFS)은 2030년까지 탄소 강도를 30% 줄이는 것을 목표로 하고 있으며, 폐기물 유래의 열분해유가 석유 원료와 경쟁하도록 고가치의 크레딧을 발행하고 있습니다. 캐나다의 청정연료 규제는 15% 절감 목표를 설정하고 국내 생산을 위해 15억 달러를 기부함으로써 북미 수요를 강화하고 있습니다. 병행하여, 일본의 플라스틱 자원 순환 전략과 미국의 지속 가능한 항공 연료 세액 공제는 열분해 오일을 직접적인 경제적 이점을 가진 적격 원료로 자리잡고 있습니다. 이러한 시책이 함께 폐유는 환경 부하에서 컴플라이언스 대응의 탈탄소화 상품으로 변모를 이루고 있습니다.

유럽의 2030년까지 포장재의 100% 리사이클화 의무화와 중국의 2025년까지 40억톤의 고형 폐기물을 리사이클하는 노력은 기계적 리사이클을 넘은 처리 루트 수요를 급격히 높여주고 있습니다. 2025년 9월에 시행된 캐나다 연방 플라스틱 등록 제도는 품질 인증이 가능한 고급 시설에 유리한 원료 투명한 추적 시스템을 추가했습니다. 인도네시아 폐기물 30% 감소 목표는 원료 공급원을 더욱 확대합니다. 이러한 규제 동향은 예측 가능한 장기 원료 공급원을 제공하여 고효율 열분해 기술에 대한 투자를 촉진합니다.

타이어 유래유에는 벤조(a)피렌 등의 다환 방향족 탄화수소가 10% 이상 함유되는 경우가 많아, 스테인리스제 또는 라이닝 처리된 탱크와 불활성 가스 봉입이 필요해, 물류 코스트를 밀어 올립니다. 혼합 플라스틱 오일은 황, 산소, 염화물 수준이 높고, 전처리를 하지 않으면 정제 촉매를 오염시킵니다. 생산 후 반응이 계속되기 때문에 장거리 수송 중에 점도와 산도가 변화하여 안정제와 온도 관리가 요구됩니다. 이러한 기술적 과제가 국경을 넘는 거래를 제한하고 표준화를 막기 때문에 세계의 보급이 늦어지고 있습니다.

폐플라스틱은 2025년 열분해유 시장 점유율의 55.02%를 차지했고 해당 부문은 2031년까지 연평균 복합 성장률(CAGR) 18.92%를 나타낼 전망입니다. 세계 플라스틱 폐기물이 연간 3억 8,000만 톤을 넘어 기계적 재활용 회수율이 10% 미만으로 정체되는 가운데 폐플라스틱 원료로 인한 열분해유 시장 규모도 마찬가지로 확대될 것으로 예측됩니다.

레조낙의 60% 이상의 수율 기술과 폴리프로필렌과 바이오매스의 시너지 효과에 의한 공동 열분해 등 혼합 플라스틱 처리 기술의 진보로 원료 준비가 간소화되어 선별 비용이 절감됩니다. 제2의 주요 원료인 폐타이어는 조직적인 회수 체제의 혜택을 받는 한편, 다환 방향족 탄화수소(PAH) 오염도가 높아 가격 할인 요인이 되고 있습니다. 바이오매스 원료는 탈산소 처리의 과제를 안고, 고비용의 수소화 처리를 필요로 하기 때문에 즉각적인 규모 확대가 제한되고 있습니다. 정제 원료에 대한 염화물·황 규제가 강화되는 가운데 고순도 플라스틱 오일 수요가 높아지고 있어 원료 시장 전체에서 프리미엄 부문을 형성하고 있습니다.

「열분해유 보고서」는 원료별(폐플라스틱, 폐타이어, 바이오매스, 기타), 용도별(연료·화학제품), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

유럽은 정책의 명확성과 전용 자금 조달원에 의해 지원되고 2025년 세계 판매량의 35.74%를 차지했습니다. 이 지역에는 리옹 델 바젤의 연간 5만 톤 규모의 웨슬링 공장과 OMV의 연간 1만 6천 톤 규모의 ReOil 플랜트가 존재하며, 모두 소각 처리에 비해 저탄소 실적로 확장 가능한 생산 능력을 가지고 있습니다.

아시아태평양은 일본의 NEDO 자금, 중국의 40억 톤 폐기물 이용 목표 및 ENEOS-미쓰비시화학 이바라키의 수열 플랜트와 같은 획기적인 프로젝트에 힘입어 22.98%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하는 시장입니다. 동남아시아도 이를 추종하고 있으며, 인도네시아의 파트너인 JGC와 마루베니는 증가하는 해양 플라스틱 유입에 대처하기 위해 모듈식 Pyro-Blue 시스템의 평가를 진행하고 있습니다.

북미에서는 장기 공급 계약과 견조한 저탄소 연료 기준(LCFS) 신용 구조로 잠재적인 성장이 가속화되고 있습니다. 다우사와 프리포인트사공급계약은 연간 18만톤의 애리조나 복합시설을 지원하고, 노바케미컬즈사는 온타리오주에서 플라스틱에너지사의 타코일 프로세스를 채용하여 연간 6만 6천톤의 생산능력을 추가합니다. 이는 2030년까지 재생재 함량 30%를 달성하겠다는 회사의 공약을 지지하는 것입니다.

The Pyrolysis Oil Market was valued at USD 1.44 billion in 2025 and estimated to grow from USD 1.69 billion in 2026 to reach USD 3.72 billion by 2031, at a CAGR of 17.12% during the forecast period (2026-2031).

Heightened plastic-waste regulations, circular-economy mandates and refinery co-processing breakthroughs together accelerate demand, while generous carbon-credit schemes improve plant economics. Strategic funding from Europe's Innovation Fund and Japan's NEDO program underpins capacity additions that shift the competitive balance toward regions with supportive policy ecosystems. Producers pursue vertical integration with refiners to reduce capital outlays and secure guaranteed offtake, and technology licensors are racing to commercialize microwave-assisted or supercritical routes that improve yield and cut emissions. At the same time, contaminant management, particularly for polycyclic aromatic hydrocarbons, remains the key operational hurdle as specification-driven customers tighten acceptance limits.

California's Low Carbon Fuel Standard now targets a 30% carbon-intensity cut by 2030, issuing high-value credits that make waste-derived pyrolysis oil competitive with petroleum inputs. Canada's Clean Fuel Regulations set a 15% reduction goal and earmark USD 1.5 billion for domestic production, reinforcing North American demand. In parallel, Japan's plastics resource-circulation strategy and U.S. sustainable aviation-fuel tax credits position pyrolysis oil as a qualifying feedstock with direct financial upside. Together these measures transform waste oil from an environmental liability into a compliance-grade decarbonization commodity.

Europe's mandate for 100% recyclable packaging by 2030 and China's push to recycle 4 billion tons of bulk solid waste by 2025 sharply raise demand for processing routes beyond mechanical recycling. Canada's Federal Plastics Registry, effective September 2025, adds transparent feedstock tracking that favors advanced facilities capable of quality certification. Indonesia's 30% waste-reduction target further broadens the raw-material pool. These regulatory forces provide predictable long-term feedstock streams and catalyze investments in high-efficiency thermal decomposition.

Tire-derived oils often contain more than 10% polycyclic aromatic hydrocarbons such as benzo[a]pyrene, requiring stainless or lined tanks and inert-gas blanketing, which inflate logistics costs. Mixed-plastic oils exhibit elevated sulfur, oxygen and chloride levels that foul refinery catalysts unless pre-treated. Ongoing post-production reactions alter viscosity and acidity during long-haul shipment, demanding stabilizers and temperature control. These technical complications restrict cross-border trade and limit standardization, slowing global adoption.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Waste plastics held 55.02% of the pyrolysis oil market share in 2025, and the segment is tracking a 18.92% CAGR through 2031. The pyrolysis oil market size attributable to waste-plastic feedstock is projected to rise in tandem as global plastic waste exceeds 380 million t y while mechanical recycling stalls below 10% recovery.

Advances in mixed-plastic processing, such as Resonac's more than or equal to 60% yield technology and synergistic co-pyrolysis of polypropylene with biomass, simplify feed preparation and cut sorting costs. Tire waste, the second-largest input group, benefits from well-organized collection but suffers from higher PAH contamination that commands price discounts. Biomass streams face oxygen-removal challenges that require costly hydrotreatment, limiting immediate scale-up. As regulators tighten chloride and sulfur limits for refinery feed, demand is rising for high-purity plastic oils, creating a premium segment within overall feedstock markets.

The Pyrolysis Oil Report is Segmented by Raw Material (Waste Plastics, Waste Tires, Biomass, and Others), Application (Fuels and Chemicals), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Europe accounted for 35.74% of global sales in 2025, underpinned by policy clarity and dedicated funding streams. The region hosts LyondellBasell's 50,000 tons per year Wesseling unit and OMV's 16,000 tons per year ReOil plant, both demonstrating scalable output with lower carbon footprints versus incineration.

Asia-Pacific is the fastest-growing market at a 22.98% CAGR, fueled by Japan's NEDO funding, China's 4 billion-t waste-utilization target and breakthrough projects such as ENEOS-Mitsubishi Chemical's hydrothermal plant in Ibaraki. Southeast Asia is following suit, with Indonesian partners JGC and Marubeni evaluating modular Pyro-Blue systems to tackle rising marine-plastic inflows.

North America shows accelerating potential through long-term offtake contracts and robust LCFS credit structures. Dow's supply deal with Freepoint anchors a 180,000 tons per year Arizona complex, and NOVA Chemicals will add 66,000 tons per year of capacity in Ontario using Plastic Energy's Tacoil process, supporting its 30% recycled content pledge by 2030.