ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

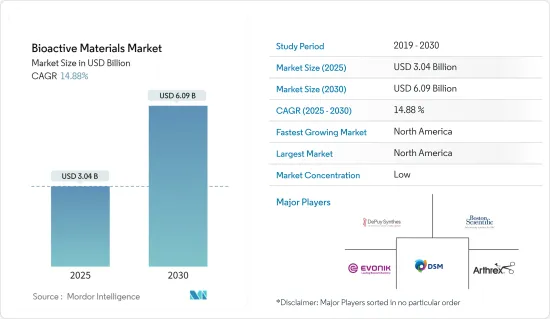

생체활성 재료 시장 규모는 2025년에 30억 4,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 14.88%로 성장할 전망이며, 2030년에는 60억 9,000만 달러에 달할 것으로 예측됩니다.

이 소재는 의료 산업에서 널리 사용되고 있기 때문에 COVID-19는 의료기기에 대한 수요가 크게 증가하여 시장에 긍정적인 영향을 미쳤습니다.

장기적으로는 치과 및 근관 치료에 대한 수요 증가가 시장을 견인할 것으로 보입니다.

주요 하이라이트

높은 비용, 규제, 독성의 가능성이 시장 성장을 크게 저해합니다.

정형외과 수요 증가 및 새로운 개발은 시장의 기회를 창출할 것으로 기대됩니다.

예측 기간 중 북미가 시장을 독점할 것으로 예측됩니다.

생체활성 재료 시장 동향

정형외과에서 수요 증가

생체활성 재료는 조직과의 결합 등 신체의 생물학적 반응을 자극합니다. 생체활성 재료는 나노 의료나 바이오 센서, 기계적 인터록, 뼈 조직의 치유, 치과 등에 응용되고 있습니다.

정형외과에서는 하이드록시아파타이트가 가장 일반적으로 이용되고 있는 생체활성 세라믹 재료입니다. 생체활성 재료는 임플란트 표면에 생리적으로 활성한 층을 만들고 그 결과 본래의 조직과 물질을 연결합니다. 생체활성 재료의 조성을 바꿈으로써 결합율이나 계면결합층의 두께를 다양하게 바꿀 수 있습니다.

생체활성 유리는 체내에서의 생체활성이 높음에도 불구하고 정형외과 수술에 있어서는 금속 임플란트와 비교하여 한정적인 역할밖에 하지 않습니다. 생체활성 유리는 외과적 성형 분야에서 용도가 기대되는 신소재입니다.

Eurostat에 따르면 2021년에는 EU 인구의 5분의 1(20.8%)이 65세 이상이 됩니다. 2021-2100년 EU 인구 중 80세 이상의 비율은 6.0%에서 14.6%로 2배 이상이 될 것으로 예상됩니다.

국가 통계국(NSO)의 Old in India 2021 study에 따르면, 인도의 고령자 인구(60세 이상)는 2031년에는 1억 9,400만 명에 달할 전망이며, 2021년의 1억 3,800만 명으로부터 41% 증가할 것으로 예상되고 있습니다.

이러한 요인이 모두, 예측 기간중의 정형외과 분야에서 생체활성 재료 수요를 촉진할 것으로 예측됩니다.

시장을 독점하는 북미

북미는 미국의 고도로 발전한 헬스케어 부문과 의료기술 부문을 진전시키기 위한 지속적인 투자로 세계 시장을 독점할 것으로 예측됩니다.

미국의 헬스케어 부문은 이 지역에서 가장 선진적인 것 중 하나입니다. 메디케어 메디케이드 서비스센터에 따르면 2021-2028년 국민 의료비는 평균 5.5% 이상으로 성장해 2028년 약 6조 1,920억 달러에 이를 것으로 전망됩니다.

생체활성 재료는 근관치료나 골결손치료, 치아재생, 경조직수복, 줄기세포 이식 등에 사용되고 있습니다. 생체활성 유리와 유리 세라믹은 뼈 조직 공학에 사용되는 주요 생체활성 재료입니다.

세계은행의 데이터에 따르면 미국의 65세 이상의 인구는 전체 인구의 약 16.6%입니다. 65세 이상의 노인은 충치나 잇몸 문제로 더 많은 진찰을 필요로 하고 관절염 위험도 높습니다.

미국 정형외과학회(AAOS)에 의하면, 근골격 질환과 관절(무릎과 고관절)의 치환술은 미국인의 사이에서 가장 일반적인 수술입니다. 이 용도에서는 생체활성 재료의 사용이 증가하고 있습니다.

2022년 캐나다의 총 의료비는 2,457억 2,000만 달러로 평가되어 올해 말까지 2,645억 달러에 이를 것으로 예상되고 있습니다. 헬스케어 산업에서 의료기기 부문은 고도로 다각화된 수출 지향 산업으로 기기와 소모품을 제조하고 있습니다. 이 부문은 제품 혁신에 의해 견인되고 있습니다. 이 산업은 캐나다 대학, 연구기관, 병원에서 진행되는 세계적인 혁신적인 연구를 활용할 수 있으며, 그 중 일부는 캐나다 의료기기 기업에 스핀오프되어 있습니다.

수술의 실시에는 생체활성 재료를 포함한 고도의 의료기기나 부품이 필요합니다. 이는 이들 재료의 의약품 사용과 함께 북미 생체활성재료 시장을 향후 수년간 견인할 것으로 예상됩니다.

생체활성 재료 산업 개요

세계의 생체활성 재료 산업은 세분화되어 있으며, 주요 기업이 시장의 주요 점유율을 차지하고 있습니다. 주요 기업으로는 Boston Scientific, Depuy Synthes, Evonik Industries, DSM, Arthrex등을 들 수 있습니다(순부동).

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

치과 및 근관 치료에 대한 수요 증가

의료 산업에서 용도 증가

성장 억제요인

고비용, 규제, 독성의 가능성

업계 밸류체인 분석

Porter's Five Forces 분석

신규 참가업체의 위협

구매자의 협상력

공급기업의 협상력

대체품의 위협

경쟁도

제5장 시장 세분화

재료 유형별

생체 활성 유리

생체활성 세라믹

생체활성 복합재료

기타

용도별

정형외과

치과의료

나노의약품 및 바이오테크놀러지

기타

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴 및 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

Arthrex Inc.

Bioactive Bone Substitutes OyJ

Biomatlante

BTG(Boston Scientific)

Cam Bioceramics

Ceraver

Collagen Matrix Inc.

DePuy Synthes(Johnson and Johnson)

DSM

Evonik Industries

Medtronic Inc.

Noraker

OSARTIS GmbH

Pulpdent Corporation

Septodont Holding

Stryker Corporation

Zimmer Holdings Inc.

제7장 시장 기회 및 향후 동향

정형외과 수요 증가 및 신규 개발

AJY

영문 목차

영문목차

The Bioactive Materials Market size is estimated at USD 3.04 billion in 2025, and is expected to reach USD 6.09 billion by 2030, at a CAGR of 14.88% during the forecast period (2025-2030).

As the material is widely used in the healthcare industry, COVID-19 had a positive impact on the market, as the demand for healthcare equipment grew significantly.

Over the long term, the growing demand for dental care and root canal treatment will drive the market.

Key Highlights

On the flip side, high costs, regulations, and probable toxicity hinder market growth significantly.

The rising demand for orthopedics and new developments are expected to create opportunities for the market studied.

North America is expected to dominate the market during the forecast period.

Bioactive Materials Market Trends

Growing Demand from Orthopedics

Bioactive materials stimulate a biological response from the body, such as bonding to the tissue. Bioactive materials find their application in nanomedicine and biosensors, mechanical interlocks, bone tissue healings, and dental, amongst others.

In orthopedic surgery, hydroxyapatite is the most commonly utilized bioactive ceramic material. Bioactive materials create a physiologically active layer on the implant's surface, resulting in a link between the native tissues and the substance. Changing the composition of the bioactive material allows a wide variety of bonding rates and interfacial bonding layer thickness.

Bioactive glasses, despite their higher bioactivity within the body, serve a minor role in orthopedic surgery compared to metallic implants. Bioactive glass is a new material that has the potential to be employed in surgical orthopedics.

According to Eurostat, in 2021, a fifth of the EU population (20.8%) was 65 or older. Between 2021 and 2100, the proportion of people aged 80 and up in the EU's population is expected to more than double, from 6.0% to 14.6%.

According to the National Statistical Office's (NSO) Old in India 2021 study, India's elderly population (aged 60 and more) is expected to reach 194 million in 2031, up by 41% from 138 million in 2021.

All such factors are expected to drive the demand for bioactive materials in the orthopedics sector during the forecast period.

North America Region to Dominate the Market

North America is expected to dominate the global market due to the highly developed healthcare sector in the United States and the continuous investments to advance the medical technology sector.

The healthcare sector in the United States is one of the most advanced in the region. According to the Centers for Medicare and Medicaid Services, during 2021-2028, national healthcare spending is projected to grow at an average of more than 5.5% and reach approximately USD 6.192 trillion by 2028.

Bioactive materials are used in root canal and bone defect treatment, tooth regeneration, hard tissue repairs, and stem cell transplantation. Bioactive glasses and glass ceramics are major bioactive materials used in bone tissue engineering.

According to World Bank data, the population above 65 years of age in the United States stood at around 16.6% of the total population. They require more medical attention for tooth decay and gum problems and pose a higher risk of arthritis.

According to the American Academy of Orthopedic Surgeons (AAOS), musculo skeletal diseases and replacement of joints (knee and hip) are the most common surgeries among the American population. These applications increasingly use bioactive materials.

In 2022, total health expenditure in Canada was valued at USD 245.72 billion and is expected to reach USD 264.5 billion by end of this year. In the healthcare industry, the medical device sector is a highly diversified and export-oriented industry that manufactures equipment and supplies. The sector is driven by product innovations. The industry can draw on world-class innovative research conducted in Canadian universities, research institutes, and hospitals, some of which are spun off into Canadian medical device companies.

Performing surgeries requires advanced medical devices and components, including bioactive materials.This, along with the use of these materials in pharmaceutical, is expected to drive the market for bioactive materials through the years to come in North America.

Bioactive Materials Industry Overview

The global bioactive materials industry is fragmented, with the top players accounting for a major share of the market. Some major companies are Boston Scientific, Depuy Synthes, Evonik Industries, DSM, and Arthrex, among others (not in any particular order).

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Growing Demand for Dental Care and Root Canal Treatment

4.1.2 Increasing Applications in Medical Industry

4.2 Restraints

4.2.1 High Cost, Regulations, and Probable Toxicity

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Threat of New Entrants

4.4.2 Bargaining Power of Buyers

4.4.3 Bargaining Power of Suppliers

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Revenue)

5.1 Material Type

5.1.1 Bioactive Glass

5.1.2 Bioactive Ceramics

5.1.3 Bioactive Composites

5.1.4 Other Material Types

5.2 Application

5.2.1 Orthopedics

5.2.2 Dental Care

5.2.3 Nanomedicines and Biotechnology

5.2.4 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Arthrex Inc.

6.4.2 Bioactive Bone Substitutes OyJ

6.4.3 Biomatlante

6.4.4 BTG (Boston Scientific)

6.4.5 Cam Bioceramics

6.4.6 Ceraver

6.4.7 Collagen Matrix Inc.

6.4.8 DePuy Synthes (Johnson and Johnson)

6.4.9 DSM

6.4.10 Evonik Industries

6.4.11 Medtronic Inc.

6.4.12 Noraker

6.4.13 OSARTIS GmbH

6.4.14 Pulpdent Corporation

6.4.15 Septodont Holding

6.4.16 Stryker Corporation

6.4.17 Zimmer Holdings Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Rising Demand from Orthopedics and New Developments