ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

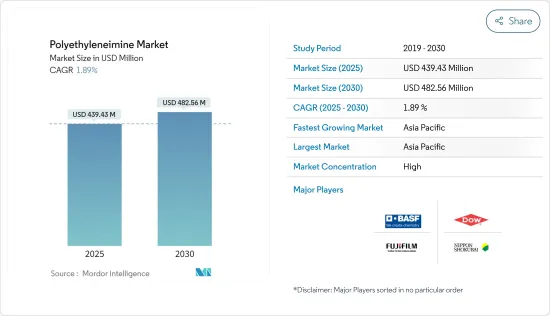

폴리에틸렌이민 시장 규모는 2025년에 4억 3,943만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 1.89%로 성장할 전망이며, 2030년에는 4억 8,256만 달러에 달할 것으로 예측됩니다.

COVID-19가 시장에 미친 영향은 마이너스였습니다. 그러나 시장은 팬데믹 전 수준에 도달했고 예측 기간 동안 안정적인 성장이 예상됩니다.

주요 하이라이트

시장을 견인하는 주요 요인은 세제나 수처리 약품 용도에서 수요 증가와 접착제 및 실란트에서의 사용량 증가입니다.

반면, 엄격한 환경 규제가 시장의 성장을 방해하고 있습니다.

폴리에틸렌이민-나노실리카 복합재료의 개발, 퍼스널케어 및 화장품 업계의 급확대 등의 요인은 시장에 다양한 성장 기회를 가져올 것으로 예측됩니다.

아시아태평양이 세계 시장을 독점하고 있으며, 중국과 인도에 의한 소비가 가장 큽니다.

폴리에틸렌이민 시장 동향

접착제 및 실란트 부문이 시장을 독점

폴리에틸렌이민(PEI)은 폭넓은 접착제 및 실란트 용도에 사용되고 있습니다. 접착제 업계에서는 접착 촉진제로서 라미네이트에 사용됩니다. 또한 포장 필름용 수성 프라이머에도 사용되고 있습니다.

폴리에틸렌이민은 포장 업계에서는 압출 코팅용 프라이머로 이전부터 사용되고 있습니다. 특히 폴리에틸렌을 종이 등의 셀룰로오스계 기재에 접착할 때 사용됩니다. 실제로는 희석한 물 또는 물과 알코올 용액을 도포합니다.

포장 업계는 세계적으로 접착제의 최대의 소비자입니다. 이 동향은 예측 기간 중에도 계속될 것으로 예측되는데, 그 주된 이유는 식음료 분야에서 포장 용도의 왕성한 수요입니다.

접착제는 포장 업계에서 사용되는 가장 일반적인 접착 메커니즘 중 하나입니다. 폴리에틸렌이민 기반 접착제는 주로 냉동 식품 포장에 사용됩니다. 이것이 포장업계의 접착제 수요를 끌어올려 시장을 뒷받침하고 있습니다.

S&P Global에 의하면, 2021년도의 인도 국내의 접착제 및 실란트 시장은 1,340억-1,360억 루피(18억 1,000만-18억 3,000만 달러)였습니다. 인도의 접착제 및 실란트 시장은 2개의 부문으로 나뉩니다. 공업용 부문은 포장, 신발, 도료, 자동차 등의 B2B 산업에 대응하고 있습니다. 소매 부문은 가구 및 목공, 빌딩 건설, 미술 공예, 전기 조인트 등의 산업에 대응하고 있습니다.

전자 산업은 등각 코팅, 단자 전극 보호, 표면 실장 장치 접착 등 다양한 용도로 접착제를 사용합니다. 전자 산업은 인도에서 가장 급성장하고 있는 산업 중 하나로, 전자 및 IT부에 의하면, 2021년도 시장 규모는 4조 9,500억-5조 루피(669억 5,000만-676억 2,000만 달러)였습니다.

상기의 요인으로부터, 예측 기간 중 접착제 및 실란트 부문이 시장을 독점할 가능성이 높습니다.

아시아태평양이 시장을 독점

아시아태평양에서는 폴리에틸렌이민이 세제, 접착제, 수처리 약품, 화장품, 제지 등의 용도로 강하게 사용되고 있기 때문에 예측 기간 중 폴리에틸렌이민 시장이 지배적이 될 것으로 예측됩니다.

폴리에틸렌이민은 펄프 및 종이 제조의 습윤 강화제로 사용됩니다. 중국, 인도, 동남아시아에서 종이 및 펄프 산업의 성장은 앞으로도 시장의 촉진요인으로 작용할 수 있습니다.

중국은 잉크 생산에서 가장 급속하게 성장하고 있는 국가 중 하나입니다. 이 나라의 잉크 업계는, 국제적인 잉크 제조업체와, T&K Toka와의 합작 회사인 Hangzhou TOKA Ink나 Toyo Ink와의 합작 회사인 Tianjin Toyo Ink 등의 국내 기업이 혼재하고 있어, 이것들은 중국에서 주요한 다국적 잉크 공급업체입니다. 또, DIC, Sakata INX, Siegwerk, Flint Group, Hubergroup 등의 대기업 잉크 제조업체도 중국에 제조 공장을 가지고 있습니다. Yip's Chemical의 자회사인 Bauhinia VariegataInk & 케미컬스는 국내 최대의 잉크 제조업체입니다.

세제와 산업용 세정제는 소비자 습관의 변화와 가정에서의 위생에 대한 관심 증가로 중국에서 수요가 높아지고 있습니다. 코로나19 대유행으로 중국 시장에서는 세제와 산업용 세정제 수요가 크게 증가했습니다. 세제 및 세정제의 매출액은 2020년에 10배의 성장을 보였습니다. 2021년에는 매출액이 400-500% 성장했습니다.

비누 제조는 인도의 FMCG 부문에서 가장 오래된 산업 중 하나이며, 소비재 부문의 50% 이상을 차지하고 있습니다. 최근 데이터로는 국내에는 비누를 판매하는 소매점이 약 500만 개 있고, 그 중 375만 개는 농촌 지역에서 영업하고 있습니다.

인도와 덴마크는 코펜하겐에서 개최된 2022년 세계수회의 및 전시회에서 '인도의 도시폐수 시나리오'에 관한 백서를 발표했습니다. 2021년 인도 도시 지역의 하수 발생량은 72,368MLD였지만 하수 처리 능력은 31,841MLD에 불과했습니다. 정부는 지난해 발표한 스와치 바라트 미션 2.0(SBM 2.0) 아래 하수 처리 능력 향상을 꾀하고 있습니다. 이를 통해 수처리에 있어 폴리에틸렌이민의 막대한 수요가 예상됩니다.

인도의 접착제 업계는 그 성장성으로부터 제조업체 각사가 투자를 하고 있습니다. 따라서 파이프라인에 있는 신공장이나 능력 확장은 해당 국가의 폴리에틸렌이민 수요를 증가시킬 것으로 예측됩니다. 예를 들어, 2021년 12월, 시카는 인도 푸네에 새로운 기술 센터와 고품질 접착제 및 실란트 제조 공장을 개설할 계획을 발표했습니다.

이와 같이, 이러한 요인에 의해 아시아태평양이 시장 전체를 지배할 것으로 기대되고 있습니다.

폴리에틸렌이민 산업 개요

폴리에틸렌 이민 시장은 국제 및 국내 기업의 존재에 의해 고도로 통합되어 있습니다. 주요 기업으로는, BASF SE, Nippon Shokubai, Dow, FUJIFILM Wako Pure Chemical Corporation 등이 있습니다.(순부동)

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

세제 및 수처리 약품 용도에서 수요 증가

접착제 및 실란트로 용도 확대

성장 억제요인

엄격한 환경 규제

기타

밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

유형별

선형

분기형

용도별

세제

접착제 및 실란트

수처리 약품

화장품

종이

도료, 잉크 및 염료

기타

지역별

아시아태평양

중국

인도

일본

한국

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

기타 유럽

남미

브라질

아르헨티나

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

BASF SE

Dow

FUJIFILM Wako Pure Chemical Corporation

Gongbike New Material Technology(Shanghai) Co. Ltd

NIPPON SHOKUBAI Co. Ltd

Polysciences, Inc.

SERVA Electrophoresis GmbH

Shanghai Holdenchem Co.

WUHAN BRIGHT CHEMICAL Co. Ltd

제7장 시장 기회 및 향후 동향

폴리에틸렌이민 나노실리카 복합재료의 개발

퍼스널케어 및 화장품 산업의 급 확대

AJY

영문 목차

영문목차

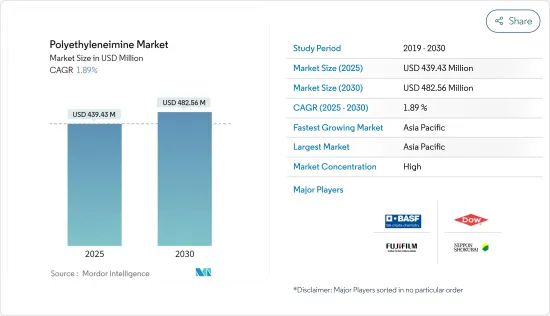

The Polyethyleneimine Market size is estimated at USD 439.43 million in 2025, and is expected to reach USD 482.56 million by 2030, at a CAGR of 1.89% during the forecast period (2025-2030).

The impact of COVID-19 on the market was negative. However, the market has reached pre-pandemic levels and is expected to grow steadily during the forecast period.

Key Highlights

The major factors driving the market are the increasing demand from applications in detergents and water treatment chemicals and the growing usage in adhesives and sealants.

On the flip side, stringent environmental regulations are hindering the growth of the market.

Factors such as the development of polyethyleneimine-nano silica composites and the rapidly expanding personal care and cosmetics industry are expected to offer various growth opportunities for the market.

Asia-Pacific dominates the market worldwide, with the largest consumption coming from China and India.

Polyethyleneimine Market Trends

Adhesives and Sealants Segment to Dominate the Market

Polyethyleneimine (PEI) is used for a wide range of adhesive and sealant applications. It is used for laminations in the adhesives industry as an adhesion promoter. It is also used in water-based primers for packaging films.

Polyethyleneimine has been used for some time as an extrusion coating primer in the packaging industry. It has particularly found use in bonding polyethylene to paper and other cellulosic substrates. In practice, it is applied with diluted water or water-alcohol solutions.

The packaging industry is the largest consumer of adhesives globally. This trend is estimated to continue during the forecast period, primarily due to the robust demand for packaging applications in the food and beverage sector.

Adhesives are one of the most common bonding mechanisms used in the packaging industry. Polyethyleneimine-based adhesives are used majorly in the packaging of frozen food products. This factor boosts the demand for adhesives in the packaging industry, thus driving the market studied.

According to S&P Global, India's domestic adhesives and sealants market is INR 134-136 billion (~USD 1.81-1.83 billion) in fiscal year 2021. Indian adhesives and sealant market is divided into two segment. The industrial segment caters to B2B industries such as packaging, footwear, paints, automotive, etc. The retail segment caters to industries such as furniture/woodwork, building construction, arts and craft, electrical fittings, etc.

The electronics industry uses adhesives for various applications, including conformal coatings, protecting terminal electrodes, bonding of surface mount devices, among many others. The electronics industry is one of the fastest-growing industries in India and, as per the Ministry of Electronics and IT, the market size of the industry is INR 4,950-5,000 billion (~ USD 66.95-67.62 billion) as of fiscal 2021.

Based on the above-mentioned factors, the adhesive and sealants segment is likely to dominate the market during the forecast period.

Asia-Pacific to Dominate the Market

Asia-Pacific is expected to dominate the market for polyethyleneimine during the forecast period, as polyethyleneimine is strongly used in applications, such as detergents, adhesives, water treatment chemicals, cosmetics, and paper, in the region.

Polyethyleneimine is used as a wet strengthening agent in pulp and paper manufacturing. The growing paper and pulp industry in China, India, and Southeast Asia may continue to act as a driver for the market studied.

China is one of the fastest-growing countries in terms of ink production. The country's ink industry is a mix of international ink manufacturers and domestic players, including Hangzhou TOKA Ink, a JV with T&K Toka, and Tianjin Toyo Ink Co. Ltd, a JV with Toyo Ink, which are the leading multi-national ink suppliers in China. DIC, Sakata INX, Siegwerk, Flint Group, Hubergroup, and other major ink companies also have manufacturing plants in China. The Bauhinia Variegata Ink & Chemicals, a subsidiary of Yip's Chemical, is the largest domestic ink producer in the country.

The detergents and industrial cleaning agents are gaining demand in China due to changing consumer habits and growing attention toward hygiene at home. Due to the COVID-19 pandemic, the Chinese market witnessed a huge rise in demand for detergent and industrial cleaning agents. The sales revenue for detergents and cleaning agents witnessed a ten-fold growth in 2020. In 2021, the sales grew by 400-500%.

Soap manufacturing is one of the oldest industries operating in the FMCG sector in India, accounting for more than 50% of the consumer goods sector. As per recent data, there are approximately five million retail outlets selling soaps in the country, of which 3.75 million operate in rural areas.

India and Denmark together launched a whitepaper recently on 'Urban Wastewater Scenario in India' at World Water Congress and Exhibition 2022 in Copenhagen. In 2021 India's sewage generation was 72,368 MLD in urban centres, whereas the installed sewage treatment capacity was only 31,841 MLD. The government is trying to increase the sewage treatment capacity under the government Swachh Bharat Mission 2.0 (SBM 2.0), which was announced last year. This is expected to create a huge demand for polyethyleneimine in water treatment.

The manufacturers have been investing in the Indian adhesives industry due to its growth potential. Thus, new plants and capacity expansions in the pipeline are projected to increase the demand for polyethyleneimine in the country. For instance, in December 2021, Sika announced its plans to open a new technology center and manufacturing plant for high-quality adhesives and sealants in Pune, India.

Thus, such factors are expected to help the Asia-Pacific region dominate the overall market.

Polyethyleneimine Industry Overview

The polyethyleneimine market is highly consolidated with the presence of international and domestic players. The major companies (in no particular order) include BASF SE, Nippon Shokubai Co. Ltd, Dow, and FUJIFILM Wako Pure Chemical Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 Introduction

1.1 Study Assumptions

1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

4.1 Drivers

4.1.1 Increasing Demand from Applications in Detergents and Water Treatment Chemicals

4.1.2 Growing Usage in Adhesive and Sealant Applications

4.2 Restraints

4.2.1 Stringent Environment Regulations

4.2.2 Other Restraints

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 Market Segmentation (Market Size in Revenue)

5.1 Type

5.1.1 Linear

5.1.2 Branched

5.2 Application

5.2.1 Detergents

5.2.2 Adhesives and Sealants

5.2.3 Water Treatment Chemicals

5.2.4 Cosmetics

5.2.5 Paper

5.2.6 Coatings, Inks, and Dyes

5.2.7 Other Applications

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Rest of South America

5.3.5 Middle-East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 Rest of Middle-East and Africa

6 Competitive Landscape

6.1 Market Ranking Analysis

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 BASF SE

6.3.2 Dow

6.3.3 FUJIFILM Wako Pure Chemical Corporation

6.3.4 Gongbike New Material Technology (Shanghai) Co. Ltd

6.3.5 NIPPON SHOKUBAI Co. Ltd

6.3.6 Polysciences, Inc.

6.3.7 SERVA Electrophoresis GmbH

6.3.8 Shanghai Holdenchem Co.

6.3.9 WUHAN BRIGHT CHEMICAL Co. Ltd

7 Market Opportunities and Future Trends

7.1 Development of Polyethyleneimine-nano Silica Composites

7.2 Rapidly Expanding Personal Care and Cosmetics Industry