ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

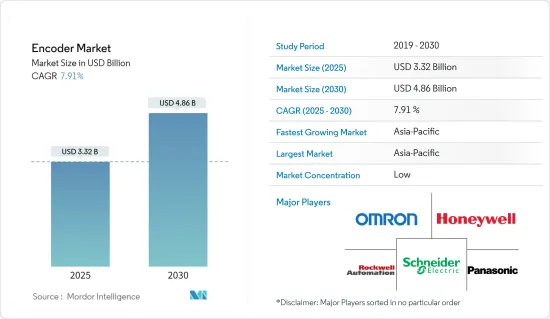

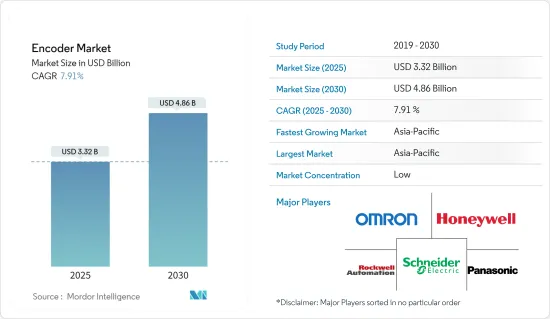

엔코더 시장 규모는 2025년에 33억 2,000만 달러로 추정되고, 2030년에는 48억 6,000만 달러에 달할 것으로 예측되며, 예측 기간(2025-2030년)의 CAGR은 7.91%를 나타낼 전망입니다.

이 시장은 데이터센터에서 통신에 이르기까지 다양한 용도로 엔코더 수요가 증가하고 있기 때문에 급성장하고 있습니다.

주요 하이라이트

하이엔드 자동화의 요구와 인더스트리 4.0이 시장 성장의 주요 요인입니다.

전 세계 많은 국가에서 인더스트리 4.0의 구현을 강화하기 위한 전략을 개발하여 인더스트리 4.0에 적극적으로 대응하고 있습니다. 예를 들어, 사마르 우디옥 바랏 4.0은 인도 자본재 부문의 경쟁력 강화 계획에 따른 인도 중공업 및 공기업부의 인더스트리 4.0 전략입니다. UNCTAD에 따르면 중국과 미국은 인더스트리 4.0 기술에 대한 투자와 역량에서 선두를 달리고 있습니다. 이들은 시가총액의 90%를 차지하는 가장 큰 디지털 플랫폼의 본거지입니다.

게다가 엔코더는 모션 컨트롤 용도의 중심적 존재입니다. 위치, 속도, 방향에 대한 피드백을 컨트롤러나 드라이브에 제공하여 드라이브 시스템의 정확성과 신뢰성을 높일 수 있습니다.

엔코더의 가장 큰 한계 중 하나는 상당히 복잡하고 일부 섬세한 부품으로 구성되어 있다는 점입니다. 따라서 기계적 남용에 대한 내성이 떨어지고 허용 온도가 제한됩니다. 1200℃ 이상에서 견딜 수 있는 광학 엔코더를 찾기가 어렵습니다. 이 외에도 모션 제어 설계에서 매우 중요한 기능 안전 문제에 대한 관심이 높아지면서 기능 안전 인증을 획득하는 것이 까다롭고 모션 제어 엔코더의 기능과 관련된 오류가 발생할 수 있다는 점도 시장 성장에 큰 제약이 되고 있습니다.

게다가 팬데믹은 자동화의 중요성을 돋보이게 하고, 제조업에 있어서의 원격 용도는 자동화에 대한 투자를 증가시켜 다양한 유형의 엔코더 수요를 끌어올릴 가능성이 있습니다.

엔코더 시장 동향

업 부문이 시장에서 큰 비중을 차지할 전망

선형 측정, 등록 마크 타이밍, 웹 장력 측정, 백스톱 측정, 이송 및 충전 등 다양한 산업 분야에서 엔코더의 사용이 빠르게 증가하고 있습니다.

특히 용접, 자재 취급, 조립, 연삭과 같은 작업에서 로봇의 적용 분야가 점점 더 많아지고 있습니다.

IFR의 세계 로봇공학 2023 보고서에 따르면 전 세계 공장에 설치된 산업용 로봇은 약 55만 3,052대에 달합니다. 중국, 일본, 미국, 한국, 독일은 전기/전자, 자동차, 금속 및 기계 등 주요 산업에서 연간 산업용 로봇 설치 대수가 많은 상위 국가에 속합니다.

산업 자동화가 빠르게 추진됨에 따라 다양한 산업 분야에서 엔코더에 대한 수요가 증가하고 있습니다. 따라서 이러한 수요를 충족하기 위해 시장에서 활동하는 공급업체들은 산업용 애플리케이션을 위한 새로운 엔코더를 출시하고 있습니다. 예를 들어, 2023년 6월, SICK는 유압 실린더의 피스톤 위치를 고정밀로 감지하고 기계의 선형 움직임을 모니터링하는 새로운 리니어 엔코더 제품군을 출시했습니다.

아시아태평양이 가장 빠른 성장을 기록할 전망

가장 빠른 성장을 기록할 것으로 예상되는 아시아태평양 지역

중국, 인도 및 기타 동남아시아 국가들은 급속한 산업화와 제조 기반 확대로 인해 로봇, CNC 기계, 조립 라인, 컨베이어 및 포장 기계와 같은 다양한 산업 장비의 생산성 향상을 위한 공장 기계에서 정밀한 위치 지정 및 제어를 위해 산업 자동화에 사용되는 엔코더에 대한 수요가 급증하고 있습니다.

아시아태평양 지역 각국 정부는 해외 기술 수입 의존도를 낮추고 혁신에 투자하기 위한 중국의 '중국 제조 2025', 생산 패러다임의 기술 전환을 통한 자립을 주창하는 인도의 '제조업 국가 전략' 등 자동화 및 인더스트리 4.0 전략을 적극적으로 추진하고 있습니다.

또한 자동차 산업의 급속한 확장은 예측 기간 동안 엔코더에 대한 수요를 촉진 할 것으로 보입니다. 이 지역에는 주요 글로벌 자동차 제조업체가 있습니다. 엔코더는 자동차 부품 및 조립 라인의 제조 공정에서 점점 더 많이 사용되고 있습니다. 이 지역에서 전기자동차 생산이 증가함에 따라 고급 모터 제어 및 배터리 관리 시스템에 필수적인 엔코더에 대한 수요가 증가할 것으로 예상됩니다.

2024년 1월, 스즈키 모터 Corp.는 인도의 구자라트 주에서 사업을 확대하고 자동차 생산 능력을 거의 두 배로 늘릴 계획을 발표했습니다.

엔코더 산업 개요

엔코더 시장에는 Omron Corporation, Honeywell, Heidenhain GmbH, Baumer Group, Posital Fraba Inc. 등 다양한 기업이 참가하고 있습니다. 기업들은 대규모 고객 기반을 확보하고 있어 센서 시장에서 더 나은 수익과 규모의 경제를 보장하는 핵심 요소인 대량의 엔코더를 생산할 수 있다는 이점이 있습니다. 강력한 브랜드는 좋은 성능과 동의어이기 때문에 오랜 역사를 가진 업체들이 우위를 점할 것으로 예상됩니다. 이들의 시장 침투력과 고급 제품 제공 능력으로 인해 경쟁이 계속 치열할 것으로 예상됩니다.

2023년 11월, 세계 센서 및 엔코더 솔루션 제조업체인 Baumer는 이동기기 및 실외 환경과 같은 가혹한 용도에서 안전성과 성능을 발휘하도록 설계된 앱솔루트 엔코더 EAM580RS를 출시했습니다. 이 마그네틱 안전 엔코더는 열악한 실외 환경으로부터 보호하기 위해 스테인리스 스틸 케이스로 제작되었으며 진동 및 충격과 같은 산업적 요인을 견딜 수 있습니다.

엔코더 제조업체인 Dynapar는 2023년 8월, 새로운 프로그래머블 중공축 엔코더인 PulseIQ 기술을 탑재한 HS35iQ 엔코더를 발표했습니다. 이 제품은 색상으로 구분된 LED와 디지털 출력을 갖춘 자가 진단 피드백 장치로, 중장비 애플리케이션의 OEM 및 최종 사용자가 실시간으로 엔코더 상태를 파악하여 결함이 있는 엔코더의 문제를 해결할 수 있는 새로운 방법을 제공합니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 지원

목차

제1장 서론

조사의 전제조건과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

시장 개요

업계의 매력도 - Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁 기업간 경쟁 관계

산업 밸류체인 분석

제5장 시장 역학

시장 성장 촉진요인

첨단 자동차 시스템에서의 높은 채택률

산업 자동화 수요 증가

시장의 과제

열악한 조건에서의 기계적 고장

제6장 시장 세분화

유형별

로터리 엔코더

선형 엔코더

기술별

광학

자기

광전

기타

최종 사용자 산업별

자동차

전자

섬유

인쇄 기계

산업

의료

기타

지역별

북미

유럽

아시아

라틴아메리카

중동 및 아프리카

제7장 경쟁 구도

기업 프로파일

Omron Corporation

Honeywell International

Schneider Electric

Rockwell Automation Inc.

Panasonic Corporation

Baumer Group

Renishaw PLC

Dynapar Corporation(Fortive Corporation)

FAULHABER Drive Systems

Pepperl Fuchs International

Hengstler GMBH(Fortive Corporation)

Maxon Motor AG

Dr. Johannes Heidenhain GmbH

POSITAL FRABA Inc.(FRABA BV)

Sensata Technologies

제8장 투자 분석

제9장 시장 전망

HBR

영문 목차

영문목차

The Encoder Market size is estimated at USD 3.32 billion in 2025, and is expected to reach USD 4.86 billion by 2030, at a CAGR of 7.91% during the forecast period (2025-2030).

The market is witnessing rapid growth due to the increasing demand for encoders in multiple applications, from data centers to telecommunication.

Key Highlights

The need for high-end automation and Industry 4.0 are the major factors driving the growth of the market. Industry 4.0 describes the fourth industrial revolution, a new world where factory automation moves beyond manufacturing plants controlled by conventional information technology systems to a cloud-based infrastructure that permits big data analytics and the virtualization of production processes.

Many countries worldwide have positively responded to Industry 4.0 by developing strategic initiatives to strengthen its implementation. For instance, SAMARTH Udyog Bharat 4.0 is an Industry 4.0 initiative of the Ministry of Heavy Industry & Public Enterprises, Government of India, under its scheme on Enhancement of Competitiveness in the Indian Capital Goods Sector. According to the UNCTAD, China and the United States are leaders in investment and capacity in Industry 4.0 technologies. They are home to the largest digital platforms, accounting for 90% of the market capitalization.

Furthermore, encoders are central to motion control applications. They can offer feedback on position, speed, and direction to a controller or drive to increase the accuracy and reliability of a drive system. As technology advances, so do encoders, incorporating the latest developments in communications and networking and offering engineers tools to solve challenges they face across a diverse array of motion control applications.

One of the most significant limitations of encoders is that they can be reasonably complex and comprise some delicate parts. This makes them less tolerant of mechanical abuse and restricts their allowable temperature. One would be hard-pressed to find an optical encoder that will survive beyond 1200C. In addition to this, rising concern about functional safety issues, which is of significant importance in any motion control design, is also a notable limitation for the growth of the market as the acquisition of functional safety certification can be arduous, and there can be some errors associated with the functionality of the motion control encoders. Such limitations pose a challenge to the market's growth.

Furthermore, the pandemic highlighted the importance of automation, and remote applications in manufacturing resulted in increased investments in automation, potentially boosting demand for various types of encoders. The rise of e-commerce and automation in sectors like warehousing and logistics is anticipated to drive demand for encoders in these applications.

Encoder Market Trends

The Industrial Sector is Expected to Hold a Major Share in the Market

The use of encoders is rapidly growing in multiple industrial applications, such as linear measurement, registration mark timing, web tensioning, backstop gauging, conveying, and filling. The most standard application is providing feedback on the motion control of electric motors. In the industrial sector, a significant amount of electricity goes to electric power motors, most of which incorporate encoders.

Robots are experiencing a growing number of application areas, especially for operations like welding, material handling, assembly, and grinding. Since there is typically limited human oversite or monitoring, these robots must have reliable encoders to help guide their movement. In robotics, encoders are essential for controlling robotic arms' and mobile robots' position and movement.

According to IFR's World Robotics 2023 report, about 553,052 industrial robots were installed in factories across the world. Among the total installed industrial robots, 73% of all newly deployed robots were installed in Asia, 15% in Europe, and 10% in the Americas. China, Japan, the United States, the Republic of Korea, and Germany are among the top countries with a greater number of annual installations of industrial robots in key industries, including electrical/electronics, automotive, and metal and machinery. Such a rise in the adoption of automation in industries is expected to further fuel the demand for encoders in the market.

As industrial automation rapidly gains momentum, the demand for encoders in various industrial applications is growing. Thus, to cater to this demand, vendors operating in the market are introducing new encoders for industrial applications. For instance, in June 2023, SICK launched a new linear encoder product family for high-precision detection of piston positions in hydraulic cylinders and monitoring linear movements in machines. This new linear encoder product line offers flexibility for countless industrial applications.

Asia-Pacific is Expected to Register the Fastest Growth

Countries like China, India, and other Southeast Asian countries are experiencing rapid industrialization and expansion of their manufacturing bases, translating to a surge in demand for encoders used in industrial automation for precise positioning and control in robots, CNC machines, and assembly lines and factory machinery that used to improve productivity in various industrial equipment like conveyors and packaging machines.

Governments across Asia-Pacific are actively promoting automation and Industry 4.0 initiatives, including China's "Made in China 2025" to reduce dependence on foreign technology imports and invest in innovations and India's "National Strategy for Manufacturing" to advocate self-reliance through the technological transformation of the production paradigm. Such initiatives are expected to fuel industrial activities with increased use of automation, creating the need for encoders in various applications.

Moreover, the rapid expansion of the automotive industry is likely to propel the demand for encoders during the forecast period. The region has the presence of major global automotive manufacturers. Encoders are increasingly used in the manufacturing processes of automotive components and assembly lines. The rise in the production of electric vehicles in the region is expected to drive demand for encoders, as they are essential in advanced motor control and battery management systems.

In January 2024, Suzuki Motor Corp. announced its plan to expand its operations in Gujarat, India, to nearly double its automotive manufacturing capacity, seeking to roll 4 million units off the assembly lines annually. The plant is planned to start operations in fiscal 2028 and is expected to increase its production capacity to 1 million units annually. Such growth in the automotive manufacturing plant expansion drives demand for encoders by necessitating increased automation, precision control in production lines, enhanced quality control systems, and optimized supply chain management.

Encoder Industry Overview

The encoder market comprises various players, such as Omron Corporation, Honeywell, Heidenhain GmbH, Baumer Group, and Posital Fraba Inc. Companies have the advantage of a large client base, enabling them to produce large volumes of encoders, a key factor in ensuring better profits and economies of scale in the sensor market. As strong brands are synonymous with good performance, long-standing players are expected to have the upper hand. Owing to their market penetration and the ability to offer advanced products, the competitive rivalry is expected to continue to be high.

In November 2023, Baumer, a global sensor and encoder solutions manufacturer, launched the absolute encoder EAM580RS, designed to deliver safety and performance in harsh applications, including mobile machinery and outdoor environments. Additionally, this safety-certified encoder would provide safe automation, which is cost-effective and easy to implement. The magnetic safety encoder has a stainless-steel casing for its protection from harsh outdoor environments, and it is able to withstand industrial factors, like vibrations and shock.

In August 2023, Dynapar, a manufacturer of encoders, launched HS35iQ Encoder with PulseIQ Technology, which is a new programmable hollow shaft encoder. This is a self-diagnosing feedback device with color-coded LEDs and digital output and offers a new way for OEM and end-users in heavy-duty machine applications to troubleshoot faulty encoders with access to encoder health status in real time.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Threat of Substitutes

4.2.5 Intensity of Competitive Rivalry

4.3 Industry Value Chain Analysis

5 MARKET DYNAMICS

5.1 Market Drivers

5.1.1 High Adoption in Advanced Automotive Systems