ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

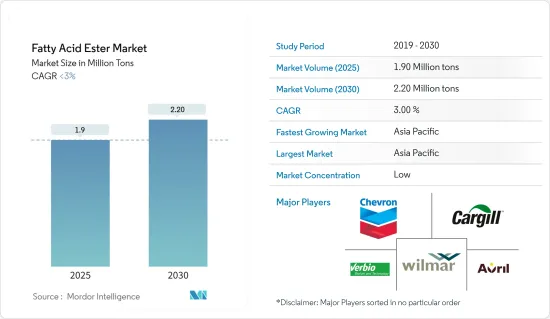

지방산 에스테르 시장 규모는 2025년에 190만 톤으로 추정되고, 예측 기간 중 2025년부터 2030년까지 CAGR 3% 미만으로 성장할 전망이며, 2030년에는 220만 톤에 달할 것으로 예측됩니다.

주요 하이라이트

지방산 에스테르 시장을 견인하는 주요 요인은 바이오 디젤에 대한 선호 증가와 개인 관리 제품 수요 증가입니다.

한편, 지방산 에스테르와 관련된 성능 제약은 예측 기간 동안 시장 성장을 방해할 가능성이 높습니다.

지방산 에스테르의 새로운 용도와 재활용은 앞으로 수년간 시장 조사에 기회가 될 전망입니다.

아시아태평양은 예측 기간 동안 가장 높은 CAGR을 기록하며 최대 급성장 시장이 될 것으로 예상됩니다.

지방산 에스테르 시장 동향

바이오연료 용도에서 지방산 에스테르 수요 증가

바이오디젤은 석유디젤보다 유해오염 물질과 온실가스 발생량이 많습니다. 바이오디젤은 지방산 에스테르와 같은 광범위한 신재생 자원으로 만들어집니다. 일반적으로 사용되는 신재생 자원에는 지방산 메틸 에스테르와 에틸 에스테르가 있습니다.

이 지방산 에스테르는 순수한 형태로 사용하거나 석유디젤과 혼합할 수 있습니다. 혼합연료에는 B2(바이오디젤 2%, 석유디젤 98%), B5(바이오디젤 5%, 석유디젤 95%), B20, B100 등 고농도의 연료가 있습니다. 특히 대규모 트럭 운송 회사에서는 바이오 디젤을 가장 순도가 높은 B100에서 사용하는 경우가 많습니다.

미국 에너지 정보국에 따르면 미국의 바이오디젤 생산량은 2023년에 약 17억 갤런에 달할 전망입니다.

같은 시기에 브라질이 남미 유수의 바이오연료 생산국으로 부상했습니다. 에너지연구소의 'Statistical Review of World Energy'에 따르면 2023년 1일 석유 생산량은 45만 5,000배럴에 이르렀으며 18.5% 증가했습니다.

바이오디젤 수요가 증가함에 따라 기업은 생산 능력을 강화하고 있습니다. 예를 들어, 브라질의 유명한 바이오디젤 제조업체인 Binatural은 2023년 12월 연간 생산량을 20% 늘리고 2026년 말까지 연간 6억 5,000만 리터를 생산할 계획을 발표했습니다.

이러한 개발은 바이오연료 생산에 있어서 각종 지방산 에스테르 수요가 견조하다는 것을 보여줍니다.

아시아태평양이 시장을 독점할 것으로 예측

아시아태평양은 바이오연료, 합성 윤활유 및 기타 용도의 엄청난 수요로 인해 지방산 에스테르(FAE)의 최대 시장입니다.

2024 World Energy Statistical Review에 따르면 아시아태평양은 바이오디젤의 주요 생산국으로 부상했습니다. 2023년 이 지역은 세계 바이오디젤 생산량의 33% 이상을 차지했고, 하루에 약 32만 배럴을 생산했으며 2022년 29만 배럴에서 증가했습니다.

지방산 에스테르는 그리스, 유압 작동유와 같은 합성 윤활유의 생산에도 사용됩니다.

최근에는 인도의 다양한 윤활유 수요 증가에 대응하기 위해 다양한 기업들이 생산 공장 설립에 투자하고 있습니다. 예를 들어, 엑손모빌은 2023년 3월 인도 뭄바이에 윤활유 생산 공장을 설립하기 위해 1억 1,000만 달러를 투자할 것이라고 발표했습니다. 공장은 2025년 말까지 가동될 예정이며 연간 15만 9,000킬로톤의 완성 윤활유 생산 능력을 보유하고 있습니다.

2024년 5월, 마찬가지로 윤활유의 세계 제조업체인 Kluber Lubrication은 인도 마이소르의 윤활유 제조 공장 확장에 1,560만 유로(1,720만 달러)를 투자할 것이라고 발표했습니다.

2024년 3월, 쉘 인도네시아는 인도에 최초의 그리스 제조 공장을 설립할 것이라고 발표했습니다. 이 공장은 연간 12킬로톤의 그리스 생산 능력을 가질 예정이며 베어링 및 기어와 같은 용도에 사용되는 Shell Gadus의 상표 그리스 제품을 생산합니다.

이러한 투자는 아시아태평양의 지방산 에스테르 소비에 긍정적인 영향을 미칠 것으로 예상됩니다.

지방산 에스테르 산업 개요

지방산 에스테르 시장은 단편적인 성격을 가지고 있으며 소수의 대기업만이 시장을 독점하고 있습니다. 주요 기업의 일부(순부동)는 Wilmar International Ltd, Avril, Chevron Corporation, Verbio Vereinigte Bioenergie AG, Cargill Corporation입니다.

기타 혜택 :

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

시장 성장 촉진요인

바이오디젤에 대한 기호의 고조

퍼스널케어 제품에 대한 수요 증가

시장 성장 억제요인

지방산 에스테르에 관한 성능의 한계

산업 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

유형별

지방산 메틸 에스테르(FAME)

폴리올 에스테르

소르비탄 에스테르

자당 에스테르

기타 유형(에틸 에스테르, 프로파일 에스테르, 수크로스 에스테르 등)

용도별

합성 윤활유

의약품

퍼스널케어 제품

식품

바이오연료

기타 용도

지역별

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

이탈리아

프랑스

스페인

북유럽 국가

터키

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

카타르

아랍에미리트(UAE)

나이지리아

이집트

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

합병, 인수, 합작사업, 제휴 및 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

Avril

Cargill Incorporated

Chevron Corporation

Cremer Oleo Gmbh & Co. KG

Croda International PLC

DuPont

Granol

Inolex Incorporated

IOI Corporation Berhad

KLK Oleo

P&G Chemicals

Sasol

Stepan Company

Verbio Vereinigte Bioenergie AG

Wilmar International Ltd

제7장 시장 기회 및 향후 동향

지방산 에스테르의 새로운 용도 및 재활용

AJY

영문 목차

영문목차

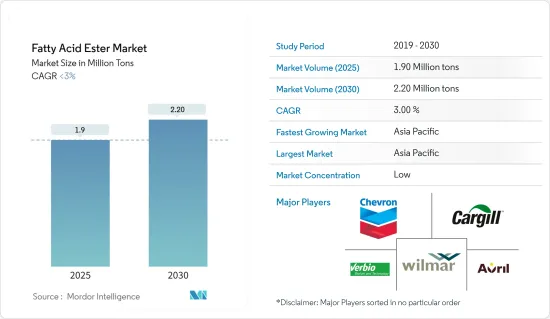

The Fatty Acid Ester Market size is estimated at 1.90 million tons in 2025, and is expected to reach 2.20 million tons by 2030, at a CAGR of less than 3% during the forecast period (2025-2030).

Key Highlights

The major factors driving the fatty acid ester market are a growing preference for biodiesels and a rising demand for personal care products.

On the other hand, performance limitations associated with fatty acid esters are likely to hamper the market's growth during the forecast period.

Emerging applications and recycling of fatty acid esters are likely to act as opportunities for the market studied in the coming years.

Asia-Pacific is expected to be the largest and fastest-growing market, registering the highest CAGR during the forecast period.

Fatty Acid Ester Market Trends

Increasing Demand for Fatty Acid Ester from Biofuel Applications

Biodiesel produces a higher level of toxic pollutants and greenhouse gases than petroleum diesel. It is made from a wide range of renewable sources, such as fatty acid esters. Some of the commonly used renewable sources are fatty acid methyl and ethyl esters.

These fatty acid esters can be utilized in their pure form or blended with petroleum diesel. Blends include B2 (2% biodiesel, 98% petroleum diesel), B5 (5% biodiesel, 95% petroleum diesel), and larger concentrations like B20 and B100. Notably, large trucking companies often use biodiesel in its purest form, B100.

According to the United States Energy Information Administration, biodiesel production in the United States reached approximately 1.7 billion gallons in 2023.

At the same time, Brazil emerged as South America's leading biofuel producer. In 2023, daily oil production hit 455 thousand barrels, marking an 18.5% rise, according to the Energy Institute's Statistical Review of World Energy.

In response to rising biodiesel demand, companies are ramping up production capacities. For example, Binatural, a prominent Brazilian biodiesel producer, announced plans in December 2023 to boost its annual output by 20%, targeting 650 million liters per annum by the end of 2026.

These developments indicate a robust demand for various kinds of fatty acid esters in biofuel production.

Asia-Pacific Projected to Dominate the Market

Asia-Pacific is the biggest market for fatty acid esters (FAEs) owing to the huge demand for biofuels, synthetic lubricants, and other applications.

As per the 2024 Statistical Review of World Energy, Asia-Pacific emerged as the dominant biodiesel producer. In 2023, the region accounted for over 33% of global biodiesel output, churning out approximately 320,000 barrels daily, up from 290,000 barrels in 2022.

Fatty acid esters are also used in the production of synthetic lubricants such as greases, hydraulic fluids, and others.

In recent times, various companies have invested in setting up production plants to meet the growing demand for various lubricants in India. For instance, in March 2023, Exxon Mobil announced the investment of USD 110 million in setting up a lubricant production plant in Mumbai, India. The plant is expected to be operational by the end of 2025 and will have a production capacity of 159,000 kilotons of finished lubricants every year.

In May 2024, Kluber Lubrication, another global manufacturer of lubricants, announced an investment of EUR 15.6 million (USD 17.20 million) in expanding its lubricant manufacturing plant in Mysore, India.

In March 2024, Shell Indonesia announced that it would set up its first grease manufacturing plant in India. The plant is expected to have a production capacity of 12 kilotons of grease every year and will produce grease products under the trademark of Shell Gadus, which are used in applications such as bearings and gears.

Such investments are expected to have a positive impact on the consumption of fatty acid esters in Asia-Pacific.

Fatty Acid Ester Industry Overview

The fatty acid ester market is fragmented in nature, with only a few major players dominating it. Some of the major companies (not in a particular order) are Wilmar International Ltd, Avril, Chevron Corporation, Verbio Vereinigte Bioenergie AG, and Cargill Corporation.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Market Drivers

4.1.1 Growing Preference toward Biodiesel

4.1.2 Rising Demand for Personal Care Products

4.2 Market Restraints

4.2.1 Performance Limitations Associated with Fatty Acid Ester

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 By Type

5.1.1 Fatty Acid Methyl Esters (FAME)

5.1.2 Polyol Esters

5.1.3 Sorbitan Esters

5.1.4 Sucrose Esters

5.1.5 Other Types (Ethyl Esters, Propyl Esters, Sucrose Esters, etc.)

5.2 By Application

5.2.1 Synthetic Lubricants

5.2.2 Pharmaceuticals

5.2.3 Personal Care Products

5.2.4 Food

5.2.5 Biofuel Applications

5.2.6 Other Applications

5.3 By Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Malaysia

5.3.1.6 Thailand

5.3.1.7 Indonesia

5.3.1.8 Vietnam

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 Italy

5.3.3.4 France

5.3.3.5 Spain

5.3.3.6 NORDIC countries

5.3.3.7 Turkey

5.3.3.8 Russia

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 Qatar

5.3.5.3 United Arab Emirates

5.3.5.4 Nigeria

5.3.5.5 Egypt

5.3.5.6 South Africa

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 Avril

6.4.2 Cargill Incorporated

6.4.3 Chevron Corporation

6.4.4 Cremer Oleo Gmbh & Co. KG

6.4.5 Croda International PLC

6.4.6 DuPont

6.4.7 Granol

6.4.8 Inolex Incorporated

6.4.9 IOI Corporation Berhad

6.4.10 KLK Oleo

6.4.11 P&G Chemicals

6.4.12 Sasol

6.4.13 Stepan Company

6.4.14 Verbio Vereinigte Bioenergie AG

6.4.15 Wilmar International Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Emerging Applications and Recycling of Fatty Acid Ester