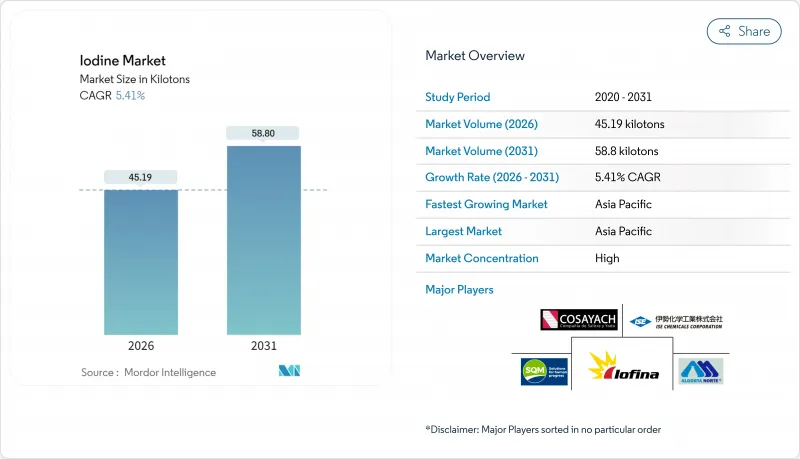

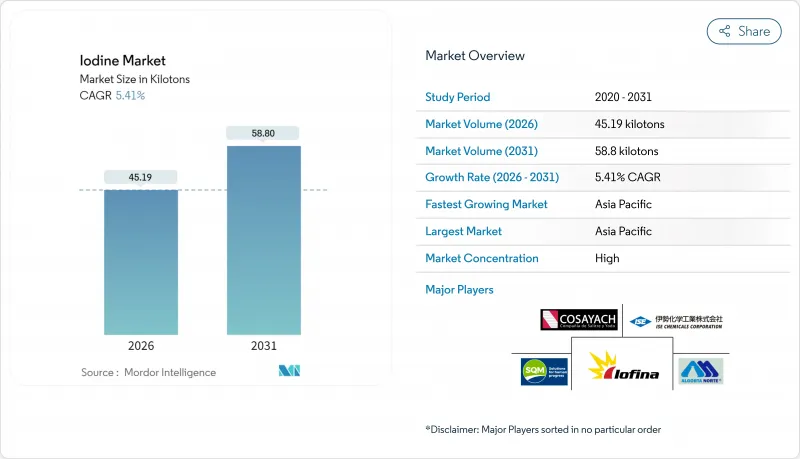

2026년 요오드 시장 규모는 45.19킬로톤으로 추정되며, 2025년 42.87킬로톤에서 성장할 것으로 예상됩니다. 2031년 예측치는 58.8킬로톤으로 2026년부터 2031년에 걸쳐 CAGR 5.41%를 나타낼 전망입니다.

이 수량 증가는 X선/CT 화상 진단, 액정·OLED용 편광판, 축산 위생 제품, 특수 화학제품 등 모두 비용 효율적인 대체품이 존재하지 않는 분야에서 요오드의 대체 불가능한 역할을 반영하고 있습니다. 의료 영상 진단이 여전히 수요의 기간을 지원하는 반면, WET IOsorb 등의 지하 염수 추출 기술은 생산 비용을 계속 낮추고 칠레산 칼리체 광자원의 우위성을 낮추고 있습니다. 아시아태평양은 중국의 전자기기 제조와 인도의 진단 능력 확대를 배경으로 소비를 견인하고 있지만, 이 지역의 수입 의존도가 높아 공급 혼란에 대한 취약성을 증폭시키고 있습니다. 2022-2023년 공급 부족 이후 글로벌 재고가 타이트해지면서 하류 사용자들은 장기 계약 체결, 현물 가격 안정화, 재활용 이니셔티브 촉진에 나서고 있어, 예측 가능성은 높아졌으나 여전히 취약한 수급 균형을 형성하고 있습니다.

세계의 진단 업무량은 계속 증가하고 있으며, 2023년에만 1,000만 건이 넘는 메디케어 조영 CT 검사가 실시된 것은 공급 쇼크가 가져오는 비용을 여실히 보여주었습니다. 계약 조영제 제조업체는 아일랜드 거점의 생산 능력 확대와 프리미엄 가격이라도 요오드 공급을 확보하는 다년 원료 계약 체결에 의해 대응하고 있습니다. 개별 투여량과 다회 투여 바이알을 중시하는 지속가능성에 대한 대처로 성장은 '검사 건수당'의 강도 모델에서 '검사 건수' 기반 모델로 이행하고 있으며, 이는 장기적인 수요를 안정화시키고 있습니다. 병원 측은 2011년 1kg당 100달러 이상까지 가격을 밀어 올린 스팟 시장의 급등으로부터 몸을 지키기 위해 공급처 다변화를 동시에 진행하고 있습니다. 인도와 동남아시아 전역에서 방사선과가 근대화됨에 따라 요오드 시장은 성숙 경제권의 포화 상태를 상쇄하는 추가적인 구조적 추풍을 얻고 있습니다.

최근 설문조사는 인도 전 가구에서 식염요오드 첨가율(유니버설 솔트 요오드화)이 92.4%에 달했지만, 임산부와 수유부에서의 경미한 결핍은 여전히 존재하고 있으며, 강화 조치만으로는 충분한 섭취량을 보장할 수 없습니다는 것이 밝혀졌습니다. 중국의 2025년판 식사 섭취 기준 개정은 잔존하는 영양 격차를 메우기 위해 방출 조절 비료나 바이오 강화 작물에 대한 의존도를 높이는 지역 특화형 영양 전략의 유효성을 더욱 뒷받침하는 것입니다. 미국 식품의약국(FDA)에서 홍콩식품안전센터에 이르는 규제당국은 단회 섭취량으로 400마이크로그램이 넘는 요오드를 포함한 해조 간식에 의한 우발적인 과잉섭취를 막기 위해 동시에 표시 규칙을 강화하고 있습니다. 이러한 병렬 동향은 식품 가공용 의약품 등급 요오드산염의 꾸준한 수량 성장을 지원하는 동시에 비의료 수요를 낳는 방출 조절 비료 코팅 기술의 개발을 촉진하고 있습니다.

미국 노동안전보건국(OSHA)은 직장 요오드 증기 농도를 0.1ppm으로 제한하고 미국 산업위생전문가 회의(ACGIH)는 더욱 엄격한 0.01ppm을 권장하기 때문에 가공업자는 스크러버, 격리 부스, 지속적인 모니터링에 대한 투자가 요구됩니다. 동시에 미국 환경보호청(EPA)에 의한 요오드계 항균제의 재등록 판단은 지속적으로 진행되고 있으며, 배합업자는 보다 환경친화적인 용제로의 이행과 추가 독성학 자료 제출이 요구되고 있습니다. 의료용 동위원소는 소량임에도 불구하고 추가 방사선 안전 프로토콜이 필요하며 통합 생산자의 간접비가 증가합니다. 이러한 규제 대응 요건이 결합되어 신규 참가자의 비용 하한을 끌어올려, 규제 인프라가 한정된 지역에서는 프로젝트 인가의 지연 요인이 될 수 있습니다.

2025년 시점에서 카리체 광석은 세계 공급량의 50.72%를 차지하고 요오드 시장의 과반수를 차지했지만, 브라인 프로젝트의 보급에 따라 상대적인 점유율은 저하 경향을 보였습니다. 이 부문의 광석 2,500kg당 1kg의 생산 비율에 더해, 칠레에 있어서 물 사용량의 감시 강화가, 보다 간편한 산화·추출 공정을 제공하는 지하 염수에 대한 경쟁력을 손상시키는 요인이 되고 있습니다. 지하염수 추출은 CAGR 5.55%로 확대되고 있어 기존의 석유 및 가스 인프라를 활용함으로써 설비 비용을 최소한으로 억제하면서 단위 에너지 소비량을 삭감. 이를 통해 가장 빠른 성장 공급 경로로서의 지위를 강화하고 있습니다. 전자 부품용 편광 필름의 리사이클은 생산량이야말로 미성숙이면서 기술적으로는 실현 가능하고, 회수 비용의 저하에 수반하여 재생 요오드가 틈새 고순도 수요를 가짐으로써, 최초 사용시의 소비 급증을 완화할 가능성이 있습니다. 해초 기반의 추출은 현재 특수한 틈새 시장이며, "생물 유래"의 인증을 중시하는 건강 식품·영양 보조 식품 제조업체용으로 공급되고 있지만, 주요한 공업용 공급원과 비교하면 생산량은 여전히 소규모입니다.

요오드 보고서는 공급원별(지하염수, 카리체 광석, 해조, 재활용), 형태별(원소 및 동위원소, 무기염 및 착체, 유기화합물), 최종사용자 산업(사료, 의료, 살균제, 광학편광필름 등), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분석되고 시장 예측은 킬로톤 단위로 제공됩니다.

아시아태평양은 2025년 요오드 시장의 34.27%를 차지하며 6.82%의 연평균 복합 성장률(CAGR)로 성장했습니다. 이것은 중국의 전자 장비 생태계, 견조한 조영제 수요, 공중 보건 강화 프로그램에 의해 지원됩니다. 중국의 최근 5개년 계획에서는 진단 능력의 확충이 목표로 되어 있어 국내의 광석·염수 프로젝트가 두드러지는 가운데도 원료 수요는 지속할 것으로 전망됩니다. 인도에서는 CT검사 건수의 높은 성장과 규제된 요오드 첨가염 프로그램에 의해 수요가 유지되어 의약품 등급 요오드산염의 주요 신규 소비국으로서의 지위를 확립하고 있습니다.

북미 시장은 성숙하면서도 견조한 추이를 나타내고 있으며, 오클라호마주와 유타주에서의 미국 염수 사업이 기반이 되고 있습니다. 이 지역에서는 안정적인 수직 통합 전략으로 수입 위험이 줄어 듭니다. 모듈식 추출장치에 대한 최근 투자는 중요한 광물 공급망의 현지화를 추진하는 정책을 반영하고 있으며, 이 동향은 2024년 IO#10 시설 가동 개시에 의해 더욱 강화되었습니다.

유럽에서는 엄격한 식품 안전 기준과 직업 노출 규제가 유지되어 유아 영양 식품 및 의약품용 고순도 요오드산염 수요를 견인하고 있습니다. 독일, 프랑스, 영국이 지역 소비를 지원하는 한편, 유제품 분야의 잔류 기준치가 성장에 자연적인 억제요인이 되고 있습니다. 항균제 내성 대책을 향한 규제 강화의 움직임에 의해 클로르헥시딘 대체품의 심사가 진행되는 동안, 병원용 소독제에 있어서 요오드 사용이 더욱 증가할 가능성이 있습니다.

남미는 칠레의 수출에 의존하고 있으며 소비량보다 공급량을 지배하고 있습니다. 브라질과 아르헨티나에서는 의료 지출과 농약 수요가 증가함에 따라 국내 소비가 늘어나고 있지만, 지역의 순수출은 여전히 견조하게 플러스를 유지하고 있습니다. 중동 및 아프리카은 절대 톤수로는 최소 규모이면서 걸프 국가의 병원에서는 두 자리 수술 건수 증가를 기록하고 지역 영양 부족을 보완하기 위한 요오드 비료의 초기 시험이 실시되고 있습니다.

Iodine market size in 2026 is estimated at 45.19 kilotons, growing from 2025 value of 42.87 kilotons with 2031 projections showing 58.8 kilotons, growing at 5.41% CAGR over 2026-2031.

Volume growth reflects the element's irreplaceable role in X-ray/CT imaging, LCD and OLED polarizers, livestock hygiene products, and specialty chemicals, all of which lack cost-effective substitutes. Medical imaging remains the pivotal demand anchor, while underground brine extraction technologies such as WET IOsorb continue lowering production costs and diluting the dominance of Chilean caliche ore resources. Asia-Pacific leads consumption on the back of Chinese electronics manufacturing and India's expanding diagnostic capacity, even as the region's import dependency magnifies exposure to supply disruptions. Tight global inventories following 2022-2023 shortages have prompted downstream users to sign longer contracts, stabilize spot prices, and encourage recycling initiatives, creating a more predictable yet still fragile supply-demand balance.

Global diagnostic workloads keep climbing, and more than 10 million Medicare contrast CT scans in 2023 alone illustrated the cost of any supply shocks. Contract-media producers have responded by expanding Irish-based capacity and by committing to multi-year feedstock contracts that lock in iodine supply even at premium prices. Sustainability initiatives that emphasize individualized dosing and multi-dose vials are shifting growth toward a procedure-volume model rather than per-procedure intensity, which steadies long-run demand. Hospitals are concurrently diversifying suppliers to shield themselves from the spot-market spikes that pushed prices above USD 100 per kg in 2011. As radiology departments modernize across India and Southeast Asia, the iodine market gains an additional structural tailwind that offsets mature-economy saturation.

Universal Salt Iodization lifted India's household coverage to 92.4% in the latest survey, yet mild deficiency persists among pregnant and lactating women, proving that fortification alone cannot guarantee adequate intake. China's 2025 dietary-reference update further validated region-specific nutrition strategies that increasingly rely on controlled-release fertilizers and biofortified crops to close residual gaps. Regulatory agencies from the U.S. FDA to Hong Kong's Centre for Food Safety are concurrently tightening label rules to prevent accidental overconsumption from seaweed snacks whose single-serve iodine content can exceed 400 µg. These parallel trends support measured volume growth for pharmaceutical-grade iodates used in food processing while spurring innovation in slow-release fertilizer coatings that add non-medical demand.

OSHA caps workplace iodine vapor at 0.1 ppm, while ACGIH recommends an even tighter 0.01 ppm, obliging processors to invest in scrubbers, isolation booths, and continuous monitoring. At the same time, the EPA's reregistration decision for iodine-based antimicrobials continues to evolve, pushing formulators toward greener solvents and demanding extra toxicological dossiers. Medical isotopes raise additional radiation-safety protocols despite low volume, compounding overhead for integrated producers. Collectively these compliance layers raise the cost floor for new entrants and can slow project sanctioning in regions with limited regulatory infrastructure.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Caliche ore contributed 50.72% of global supply in 2025, equal to more than half of the iodine market, but its relative share continues slipping as brine projects gain acceptance. The segment's 2,500 kg ore-per-kilogram output ratio, coupled with water-use scrutiny in Chile, is eroding competitiveness versus subterranean brines that offer simpler oxidation-extraction sequences. Underground brine extraction, expanding at a 5.55% CAGR, leverages existing oil-and-gas infrastructure to minimize infrastructure cost while lowering unit energy consumption, reinforcing its position as the fastest-growing supply route. Recycling of electronics-grade polarizer film is still embryonic in tonnage but is technically viable; as recovery costs fall, reclaimed iodine may cover niche, high-purity demand, tempering first-use consumption spikes. Seaweed-based extraction, now a specialized niche, services health-food and nutraceutical producers who prize "biogenic" credentials, yet output volumes remain small relative to the main industrial streams.

The Iodine Report is Segmented by Source (Underground Brine, Caliche Ore, Seaweed, and Recycling), Form (Elementals and Isotopes, Inorganic Salts and Complexes, and Organic Compounds), End-User Industry (Animal Feed, Medical, Biocides, Optical Polarizing Films, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Kilotons).

Asia-Pacific held 34.27% of the iodine market in 2025 and is growing at 6.82% CAGR, fueled by China's electronics ecosystem, robust contrast-media demand, and public-health fortification programs. China's latest Five-Year Plan targets expanded diagnostic capacity, implying persistent feedstock pulls even as domestic ore and brine projects plateau. India sustains demand through high CT procedure growth and regulated iodized-salt programs, positioning the country as a major incremental consumer of pharmaceutical-grade iodates.

North America shows mature yet resilient performance underpinned by U.S. brine operations in Oklahoma and Utah, where stable vertical-integration strategies mitigate import risk. Recent investments in modular extraction units underscore a policy push to localize critical-mineral supply chains, a trend reinforced by the IO#10 facility ramp-up in 2024.

Europe maintains stringent food-safety and occupational-exposure rules, driving demand for highly purified iodates in infant nutrition and pharmaceuticals. Germany, France, and the United Kingdom anchor regional consumption, while dairy-sector residue ceilings impose a natural brake on growth. Regulatory momentum toward antimicrobial-resistance mitigation may further elevate iodine use in hospital disinfectants as chlorhexidine alternatives undergo scrutiny.

South America hinges on Chilean exports that dominate supply rather than consumption. Domestic uptake in Brazil and Argentina is climbing alongside healthcare spending and agrochemical demand, yet regional net exports remain firmly positive. The Middle East and Africa, though the smallest territory in absolute tonnage, registers double-digit procedure growth in Gulf hospitals and showcases early iodine-fertilizer trials aimed at correcting local dietary deficiencies.