열가소성 폴리우레탄(TPU) 필름 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)

Thermoplastic Polyurethane (TPU) Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

상품코드:1689907

리서치사:Mordor Intelligence

발행일:2025년 03월

페이지 정보:영문

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

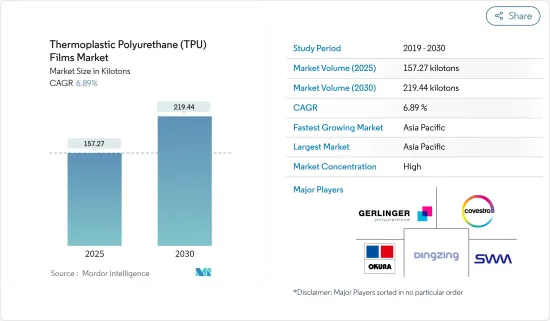

열가소성 폴리우레탄(TPU) 필름 시장 규모는 2025년 157.27킬로톤에 이를 것으로 추정되고, 예측기간(2025-2030년)의 CAGR은 6.89%를 나타내 2030년에는 219.44킬로톤에 달할 것으로 예측됩니다.

열가소성 폴리우레탄(TPU) 필름 시장은 COVID-19의 유행에 의해 신발, 의류, 스포츠 용품 등 주요 최종 사용자 산업에 악영향을 미쳤습니다. 그러나 현재 시장은 유행 이전 수준에 있을 것으로 추정되며 안정적인 속도로 성장할 것으로 기대됩니다.

주요 하이라이트

시장 성장의 주요 요인은 신발 및 의류 산업에서 TPU 필름의 사용량이 증가하는 것입니다.

한편, 원재료 가격 상승은 향후 수년간 시장 성장에 영향을 미칠 것으로 예상됩니다.

바이오 TPU 필름의 잠재력은 예측 기간 동안 시장에 좋은 기회가 될 것입니다.

아시아태평양은 가장 큰 시장이며 예측 기간 동안 가장 높은 CAGR을 나타낼 것으로 예상됩니다.

열가소성 폴리우레탄(TPU) 필름 시장 동향

신발 의류가 시장을 독점

TPU(열가소성 폴리우레탄)는 매우 내구성이 높고 연질 플라스틱입니다. 이 고품질 소재는 내마모성, 충격 흡수성, 미끄러운 노면에서의 그립력, 경량성에 다른 추종을 허용하지 않습니다.

발포 TPU 필름은 안전화, 알파인 부츠, 하이킹 부츠 등, 신발의 외측의 미끄럼 방지, 내마모성 보호 커버로서의 사용에 최적입니다.

World Footwear Yearbook 2023에 따르면 2021년의 222억에 비해 2022년에는 239억의 신발이 세계에서 생산되었습니다.

신발 산업은 세계에서 완만한 성장을 이어가고 있습니다.

신발 사업은 아시아에 매우 집중하고 있으며, 10개의 신발 중 약 9개는 아시아에서 생산되고 있습니다.

브랜드 의식의 고조와 혁신적인 디자인에 대한 관심이 신발 업계를 견인하는 주요 요인입니다

유럽에서도 신발의 생산과 소비가 서서히 증가하고 있어 이것이 열가소성 폴리우레탄(TPU) 필름 시장의 성장을 가속할 것으로 기대되고 있습니다.

아시아의 신흥 국가에 있어서의 도시화 레벨의 상승과, 스포츠나 음악 이벤트의 인기의 높아지는 예측 기간 중에 풋 웨어의 생산과 TPU 필름의 용도를 확대할 것으로 예상됩니다.

Invest India에 따르면 인도는 세계 2위의 신발 생산국이며 소비국이기도 합니다.

Industrievereinigung Chemiefaser에 따르면 세계의 섬유 생산량은 2022년에는 1억 1,380만 톤이 되었습니다.

중국, 인도, 미국, 베트남과 같은 국가에서는 섬유 및 의류의 국내 생산을 향한 노력이 증가하고 있으며 예측 기간 동안 열가소성 폴리우레탄(TPU) 필름 시장의 성장을 증가시킬 것으로 예상됩니다.

아시아태평양이 시장을 독점

아시아태평양은 열가소성 폴리우레탄(TPU) 필름 시장에서 세계적으로 큰 점유율을 차지하고 있으며 예측 기간 동안에도 시장을 독점할 것으로 예상됩니다.

중국은 세계 신발 산업을 지배하고 있으며 세계 신발 총 생산량의 60% 이상을 차지하고 있습니다. World Footwear Yearbook 2023에 따르면, 중국은 2022년에 130억 이상의 신발을 생산했습니다.

중국의 섬유 시장은 세계 최대의 섬유 시장이며, 세계의 섬유 및 의류 생산의 절반 이상을 차지하고 있습니다. World Trade Statistical Review 2023에 따르면 2022년 세계 의류 수출의 31% 이상이 중국에 의한 것이었습니다.

인도의 섬유 산업은 일본 경제에서 가장 오래된 산업 중 하나입니다. 수작업, 손으로 짠 섬유 산업에서 자본 집약적인 선진 공장에 이르기까지 매우 다양성이 풍부합니다.

Invest India에 따르면 인도는 세계 섬유 및 의류 무역의 4% 점유율을 차지하고 있습니다. 인도는 세계 5위의 테크니컬 텍스타일 제조업체이며, 그 시장 규모는 약 220억 달러로, 2047년까지 3,000억 달러까지 확대하는 것을 목표로 하고 있습니다.

중국은 세계 최대의 건설 산업이며, 향후 10년간의 세계 신규 건설 활동의 절반 가까이를 차지합니다. 국가 통계국(NBS)에 따르면 중국에서는 건설 업계의 사업활동지수(BASI)가 2023년 11월 55.9에서 12월에는 56.9로 상승했습니다. BASI 점수가 50을 초과하면 건설 업계의 성장을 보였으며 2023년 10월 BASI 점수는 53.5였습니다.

인도의 건설산업은 2025년까지 1조 4,000억 달러로 성장할 것으로 예측되고 있습니다. 국가투자계획(NIP) 아래 인도에서는 1조 4,000억 달러의 인프라 투자예산이 짜여져 있으며, 그 24%가 재생가능에너지, 도로·고속도로, 도시인프라, 12%가 철도에 할당되고 있습니다.

이와 같이, 다양한 산업에서의 수요의 고조가, 예측 기간 중에 있어서, 이 지역에서 시장을 견인할 것으로 예상됩니다.

열가소성 폴리우레탄(TPU) 필름 산업 개요

열가소성 폴리우레탄(TPU) 필름 시장은 통합된 성질을 가지고 있습니다. 시장 진출기업에는 Covestro AG, SWM, Gerlinger Industries GmbH, DingZing Advanced Materials Inc. 등이 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월의 애널리스트 서포트

목차

제1장 서론

조사의 전제조건

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

신발 및 의류 업계에서의 용도의 확대

기타

성장 억제요인

원재료 가격 상승

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

소비자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

화학 분류별

폴리에스테르

폴리에테르

폴리카프로락톤

최종 사용자 산업별

신발 및 의류

의료 용품

스포츠 장비

건축 및 건설

기타

지역별

아시아태평양

중국

인도

일본

한국

태국

베트남

말레이시아

인도네시아

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

노르딕

러시아

튀르키예

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

카타르

나이지리아

이집트

기타 중동 및 아프리카

제6장 경쟁 구도

합병, 인수, 합작사업, 제휴, 협정

시장 랭킹 분석

주요 기업의 전략

기업 프로파일

3M

American Polyfilm Inc.

Avery Dennison Corporation

Covestro AG

Ding Zing Advanced Materials Inc.

Gerlinger Industries GmbH

Huntsman International LLC

Okura Industries Co. Ltd

Permali Gloucester Ltd

Schweitzer-Mauduit International Inc.

Wiman Corporation

The Lubrizol Corporation

제7장 시장 기회와 앞으로의 동향

바이오 기반 TPU의 가능성

KTH

영문 목차

영문목차

The Thermoplastic Polyurethane Films Market size is estimated at 157.27 kilotons in 2025, and is expected to reach 219.44 kilotons by 2030, at a CAGR of 6.89% during the forecast period (2025-2030).

The TPU films market was adversely affected by the COVID-19 pandemic owing to its negative impact on major end-user industries such as footwear, apparel, and sports equipment. However, the market is currently estimated to be at pre-pandemic levels, and it is expected to grow at a steady pace.

Key Highlights

The primary factor driving the growth of the market is the increasing usage of TPU film in the footwear and apparel industry.

On the other hand, the rising prices of raw materials are expected to impact the growth of the market during the coming years.

The potential of bio-based TPU film is likely to act as an opportunity for the market studied during the forecast period.

Asia-Pacific is the largest market and is expected to register the highest CAGR during the forecast period.

Thermoplastic Polyurethane (TPU) Films Market Trends

Footwear and Apparel to Dominate the Market

TPUs (thermoplastic polyurethanes) are extremely durable and flexible plastics. This high-quality material is unrivaled in abrasion resistance, shock absorption, grip on slick surfaces, and low weight.

Foamed TPU film is ideal for use as a non-slip, wear-resistant protective covering for the outside of shoes, including safety shoes, alpine boots, and hiking boots. TPU keeps its unique qualities even when wet, making it a popular material for orthopedic insoles.

According to the World Footwear Yearbook 2023, 23.9 billion pairs of footwear were produced around the world in 2022, compared to 22.2 billion pairs in 2021. China was the world's leading producer of footwear in 2022, followed by India, Vietnam, Indonesia, and Brazil.

The footwear industry is growing at a moderate level across the world. Many major footwear companies are shifting their manufacturing facilities to Asia due to the availability of cheap labor and the increasing demand in developing countries of the Asia-Pacific.

The footwear business is highly concentrated in Asia, where nearly nine out of ten pairs of shoes are produced.

Increased brand awareness and interest in innovative designs are the major factors driving the footwear industry.

Europe is also seeing a gradual uplift in footwear production and consumption, which is expected to drive the growth of the TPU films market.

Rising urbanization levels in emerging Asian countries and the increasing popularity of sporting and music events are expected to augment footwear production and the application of TPU films during the forecast period.

According to Invest India, India is the second-largest producer and consumer of footwear in the world, with 9% of global footwear production. The country is projected to produce nearly 3 billion units of footwear by 2024, growing at an 8% compound annual growth rate (CAGR).

According to the Industrievereinigung Chemiefaser, the global production volume of textile fibers accounted for 113.8 million tons in 2022, compared to 113.8 million tons in 2021.

Such increasing efforts toward the domestic production of textiles and apparel in countries like China, India, the United States, and Vietnam are anticipated to augment the growth of the TPU films market during the forecast period.

Asia-Pacific to Dominate the Market Studied

Asia-Pacific holds a prominent share of the TPU films market globally and is expected to dominate the market during the forecast period.

China dominates the global footwear industry, accounting for over 60% of total footwear production worldwide. According to World Footwear Yearbook 2023, more than 13 billion pairs of shoes were produced in China in 2022.

The textile market in China is the world's largest textile market, accounting for more than half of the global textile and clothing production. According to the World Trade Statistical Review 2023, more than 31% of worldwide apparel exports in 2022 were done by China.

India's textile industry is one of the oldest in the country's economy. It is extremely varied and consists of hand-spun and hand-woven textile industries as well as capital-intensive sophisticated mills.

According to Invest India, India holds a 4% share of the global trade in textiles and apparel. India is the world's 5th largest manufacturer of technical textiles with a market value of nearly USD 22 billion, which the country aims to increase to USD 300 billion by 2047.

China has the largest construction industry in the world, reflecting nearly half of new construction activities in the global scenario in the upcoming decade. According to the National Bureau of Statistics (NBS), in China, the construction industry's business activity index (BASI) rose to 56.9 as of December 2023 from 55.9 in November 2023. A BASI score above 50 indicates growth in the industry, and the country's October 2023 BASI score was 53.5.

India's construction industry is projected to grow to USD 1.4 trillion by 2025. By 2030, an estimated 600 million people will live in urban centers, resulting in a need for 25 million additional mid- and ultra-luxury units. Under the National Investment Plan (NIP), India has an infrastructure investment budget of USD 1.4 trillion, with 24% of the budget earmarked for renewable energy, roads and highways, and urban infrastructure and 12% for railways.

Thus, the rising demand from various industries is expected to drive the market studied in the region during the forecast period.

Thermoplastic Polyurethane (TPU) Films Industry Overview

The thermoplastic polyurethane (TPU) films market is consolidated in nature. Some of the players in the market include (not in any particular order) Covestro AG, SWM, Gerlinger Industries GmbH, DingZing Advanced Materials Inc., and Okura Industrial Co. Ltd.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumptions

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Usage in the Footwear and Apparel Industry

4.1.2 Other Drivers

4.2 Restraints

4.2.1 Rising Prices of Raw Materials

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 Chemical Class

5.1.1 Polyester

5.1.2 Polyether

5.1.3 Polycaprolactone

5.2 End-user Industry

5.2.1 Footwear and Apparel

5.2.2 Medical Supplies

5.2.3 Sports Equipment

5.2.4 Building and Construction

5.2.5 Other End-user Industries

5.3 Geography

5.3.1 Asia-Pacific

5.3.1.1 China

5.3.1.2 India

5.3.1.3 Japan

5.3.1.4 South Korea

5.3.1.5 Thailand

5.3.1.6 Vietnam

5.3.1.7 Malaysia

5.3.1.8 Indonesia

5.3.1.9 Rest of Asia-Pacific

5.3.2 North America

5.3.2.1 United States

5.3.2.2 Canada

5.3.2.3 Mexico

5.3.3 Europe

5.3.3.1 Germany

5.3.3.2 United Kingdom

5.3.3.3 France

5.3.3.4 Italy

5.3.3.5 Spain

5.3.3.6 NORDIC

5.3.3.7 Russia

5.3.3.8 Turkey

5.3.3.9 Rest of Europe

5.3.4 South America

5.3.4.1 Brazil

5.3.4.2 Argentina

5.3.4.3 Colombia

5.3.4.4 Rest of South America

5.3.5 Middle East and Africa

5.3.5.1 Saudi Arabia

5.3.5.2 South Africa

5.3.5.3 United Arab Emirates

5.3.5.4 Qatar

5.3.5.5 Nigeria

5.3.5.6 Egypt

5.3.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers, Acquisitions, Joint Ventures, Collaborations, and Agreements