ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

ㅁ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송기일은 문의해 주시기 바랍니다.

한글목차

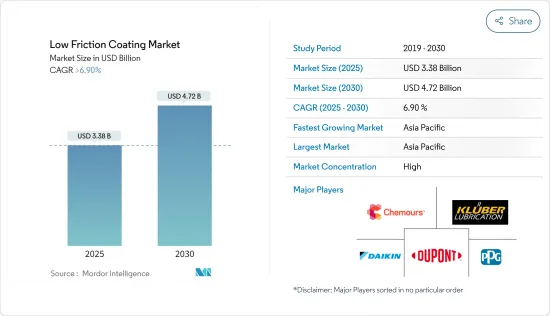

저마찰 코팅 시장 규모는 2025년 33억 8,000만 달러에 이르고 예측 기간 중(2025-2030년) CAGR은 6.9%를 나타내 2030년에는 47억 2,000만 달러에 달할 것으로 예측됩니다.

주요 하이라이트

시장을 견인하는 요인으로는 항공우주산업에 있어서의 저마찰 코팅 수요 증가와 주요국에서의 자동차산업에서의 용도 확대를 들 수 있습니다.

그러나 PTFE(폴리테트라플루오로에틸렌)의 독성에 관한 정부 규정이 시장 성장을 방해할 것으로 예상됩니다.

헬스케어 산업에서 유체 마찰 코팅 수요 증가는 앞으로 수년간 시장에 호기심이 될 것으로 예상됩니다.

예측 기간 동안 저마찰 코팅 시장은 가장 빠른 성장을 기록하고 아시아태평양에서 가장 지배적이라고 예측됩니다.

저마찰 코팅 시장 동향

자동차 및 운송 업계에서 저마찰 코팅 수요 증가

저마찰 코팅은 매우 저마찰 계수(COF), 카지리, 플레칭, 고착에 대한 우수한 이형성, 높은 내식성 및 기타 많은 이점을 가지고 있습니다.

따라서 자동차 및 운송업계에서는 연비개선, 배출가스 삭감, 성능향상 요구와 전동화, 자율주행차 등 신기술의 채용으로 저마찰 코팅 수요가 증가하고 있습니다.

게다가 세계의 자동차 생산 대수 증가가 수요를 한층 더 밀어 올리고 있습니다.

또한 유럽 자동차 공업회에 따르면 2023년 1-3분기(2023년 1월-9월)의 유럽 자동차 총 생산 대수는 2022년 동시기에 비해 거의 14% 증가했습니다.

자동차 산업은 향후 수년간 크게 성장할 것으로 예상됩니다.

예를 들어 Hyundai Motor Group, BMW Group, Toyota, Honda, Ford Motor Company, General Motors 등 다양한 자동차 제조 기업이 노스캐롤라이나주, 미시간주, 오하이오주, 미주리주, 캔자스주 등에서 전기차 제조에 대한 투자를 발표하고 있습니다.

따라서 자동차 및 운송산업은 예측기간 중 저마찰 코팅의 가장 높은 수요를 나타내며 시장에서의 우위성을 확고한 것으로 예측됩니다.

아시아태평양 급성장

예측기간 중 아시아태평양이 시장을 독점할 것으로 예측됩니다.

저마찰 코팅의 최대 생산국은 아시아태평양입니다.

중국은 생산·판매 모두 세계 최대의 자동차 시장입니다.

게다가 인도 자동차 제조 협회(SIAM)의 데이터에 따르면, 2023년도의 인도의 자동차 생산 대수는 458만대로, 2022년도의 365만대에서 현저하게 증가했습니다.

Boeing Commercial Outlook 2021-2040에 따르면 중국에서는 2040년까지 약 8,700대가 새로 납품되어 시장 서비스액은 1조 8,000억 달러에 달할 전망입니다.

또한 유틸리티부 장관 다툭세리 알렉산더 난타 Linggi에 따르면 말레이시아의 건설 부문은 2023년에 성장했으며, 2023년 9월까지 총 9,144개의 프로젝트가 성공적으로 시행되었습니다. 이 센터는 Google 클라우드의 허브 개발에 약 20억 달러를 투자했습니다.

상기와 같은 사실과 요인을 근거로 하면, 저마찰 코팅 수요는 예측 기간 중, 아시아태평양 시장에서 가장 빠른 페이스로 증가할 것으로 예상됩니다.

저마찰 코팅 산업 개요

세계의 저마찰 코팅 시장은 통합되어 있습니다.

기타 혜택

엑셀 형식 시장 예측(ME) 시트

3개월간의 애널리스트 서포트

목차

제1장 서론

조사 상정과 시장 정의

조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

성장 촉진요인

자동차 산업에서의 용도 확대

항공우주산업에 있어서의 저마찰 코팅 수요 증가

성장 억제요인

과열된 PTFE의 독성에 관한 정부규제

업계 밸류체인 분석

Porter's Five Forces 분석

공급기업의 협상력

구매자의 협상력

신규 참가업체의 위협

대체품의 위협

경쟁도

제5장 시장 세분화

유형별

이황화 몰리브덴

이황화 텅스텐

폴리테트라플루오로에틸렌(PTFE)

기타

최종 사용자 산업별

자동차 및 운송

항공우주 및 방위

헬스케어

건설

석유 및 가스

기타

용도별

베어링

자동차 부품

동력 전달 항목

밸브 부품 및 액추에이터

기타

지역별

아시아태평양

중국

인도

일본

한국

말레이시아

태국

인도네시아

베트남

기타 아시아태평양

북미

미국

캐나다

멕시코

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

튀르키예

러시아

기타 유럽

남미

브라질

아르헨티나

콜롬비아

기타 남미

중동 및 아프리카

사우디아라비아

카타르

아랍에미리트(UAE)

나이지리아

이집트

남아프리카

기타 중동 및 아프리카

제6장 경쟁 구도

M&A, 합작사업, 제휴, 협정

시장 점유율(%)**/랭킹 분석

주요 기업의 전략

기업 프로파일

AFT Fluorotec Ltd

ASV Multichemie Private Limited

Carl Bechem GmBH

DAIKIN INDUSTRIES Ltd

DuPont

Endura Coatings

Curtiss-Wright Corporation

FUCHS

GGB

IHI HAUZER TECHNO COATING BV

IKV Tribology Ltd

Impreglon UK Limited

Indestructible Paint Limited

Kluber Lubrication(Freudenberg SE)

Micro Surface Corp.

Poeton

PPG Industries Inc.

The Chemours Company

VITRACOAT

제7장 시장 기회와 앞으로의 동향

헬스케어 산업에 있어서의 저마찰 코팅 수요 증가

KTH

영문 목차

영문목차

The Low Friction Coating Market size is estimated at USD 3.38 billion in 2025, and is expected to reach USD 4.72 billion by 2030, at a CAGR of greater than 6.9% during the forecast period (2025-2030).

Key Highlights

Factors driving the market include the increasing demand for low-friction coatings in the aerospace industry and increasing applications in the automotive industry across major economies.

However, government regulations on the toxicity of PTFE (polytetrafluoroethylene) are expected to hinder the market's growth.

The growing demand for flow-friction coating in the healthcare industry is expected to act as an opportunity for the market studied in the coming years.

During the forecast period, the low friction coating market is estimated to register the fastest growth and be the most dominant in Asia-Pacific.

Low Friction Coating Market Trends

Increasing Demand for Low Friction Coating in the Automotive and Transportation Industry

Low-friction coatings possess extremely low coefficients of friction (COF), excellent release properties for resistance to galling, fretting, and sticking, high corrosion resistance, and many other benefits.

Therefore, there is an increasing demand for low-friction coatings in the Automotive and Transportation Industry driven by the need for improved fuel efficiency, reduced emissions, and enhanced performance, as well as the adoption of new technologies like electrification and autonomous vehicles.

Moreover, the rising volume of vehicle production globally is propelling the demand even further. For instance, according to the Organisation Internationale des Constructeurs d'Automobiles (OICA), automotive production globally increased from 84.83 million units in 2022 to 93.54 million units in 2023, representing a growth of 17% year-on-year.

Furthermore, according to the European Automobile Manufacturers Association, in the first three quarters of 2023 (January 2023 to September 2023), the total production of cars in Europe increased by almost 14% compared to the same period in 2022. This substantially boosted the demand in the low-friction coating market.

The automotive industry is expected to grow significantly over the coming years. Evolving digital technology, changes in customer sentiment, and economic health have played a vital role in non-commercial business practices of manufacturing vehicles.

For instance, various automotive manufacturing companies such as Hyundai Motor Group, BMW Group, Toyota, Honda, Ford Motor Company, and General Motors have announced investments in electric vehicle manufacturing in North Carolina, Michigan, Ohio, Missouri, Kansas, and other states. This is likely to boost automotive manufacturing, thereby increasing the demand for low-friction coating.

Hence, the automotive and transportation industry is projected to exhibit the highest demand for low-friction coating during the forecast period, solidifying its dominance in the market.

Asia-Pacific to Witness the Fastest Growth

Asia-Pacific is expected to dominate the market during the forecast period. The rising demand for low-friction coatings, combined with the growing automotive and healthcare industry in countries like China and India, is expected to drive the demand for low-friction coatings in this region.

The largest producers of low-friction coating are based in Asia-Pacific. Some of the leading companies in the production of low-friction coating are VITRACOAT, Daikin Industries, The Chemours Company, Dow, and ASV Multichemie Private Limited.

China is the world's largest automobile market in terms of production and sales. According to the China Association of Automobile Manufacturers (CAAM), vehicle production in China reached 30.16 million units in 2023, growing 11.6% compared to the previous year.

Furthermore, according to the Society of Indian Automotive Manufacturing (SIAM) data, in the financial year 2023, India manufactured 4.58 million vehicles, marking a notable increase from the 3.65 million produced in 2022-a growth rate of about 25%.

According to the Boeing Commercial Outlook 2021-2040, in China, around 8,700 new deliveries will be made by 2040, with a market service value of USD 1,800 billion.

Furthermore, the construction sector of Malaysia grew in 2023, with a total of 9,144 projects successfully implemented until September 2023, according to Public Works Minister Datuk Seri Alexander Nanta Linggi. In addition, there has been an increase in the country's investments in various commercial construction projects. For instance, Google invested around USD 2 billion in developing the country's first data center and a Google Cloud hub in May 2024. The new hubs will be developed at a business park in central Malaysia's Selangor state to meet the growing demand for IT services and artificial intelligence literacy programs for Malaysian students and educators.

Given the above-mentioned facts and factors, the demand for low-friction coatings is expected to increase at the fastest rate in the Asia-Pacific market during the forecast period.

Low Friction Coating Industry Overview

The global low-friction coating market is consolidated. Some of the major companies in the market include (not in any particular order) PPG Industries Inc., The Chemours Company, DuPont, Kluber Lubrication, and Daikin Industries Ltd.

Additional Benefits:

The market estimate (ME) sheet in Excel format

3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

1.1 Study Assumption and Market Definition

1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

4.1 Drivers

4.1.1 Increasing Application in the Automotive Industry

4.1.2 Growing Demand for Low-friction Coating in Aerospace Industry

4.2 Restraints

4.2.1 Government Regulation on Toxicity of Overheated PTFE

4.3 Industry Value Chain Analysis

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products and Services

4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

5.1 By Type

5.1.1 Molybdenum Disulphide

5.1.2 Tungsten Disulphide

5.1.3 Polytetrafluoroethylene (PTFE)

5.1.4 Other Types

5.2 By End-user Industry

5.2.1 Automotive and Transportation

5.2.2 Aerospace and Defense

5.2.3 Healthcare

5.2.4 Construction

5.2.5 Oil and Gas

5.2.6 Others End-user Industries

5.3 By Application

5.3.1 Bearings

5.3.2 Automotive Parts

5.3.3 Power Transmission Items

5.3.4 Valve Components and Actuators

5.3.5 Other Applications

5.4 By Geography

5.4.1 Asia-Pacific

5.4.1.1 China

5.4.1.2 India

5.4.1.3 Japan

5.4.1.4 South Korea

5.4.1.5 Malaysia

5.4.1.6 Thailand

5.4.1.7 Indonesia

5.4.1.8 Vietnam

5.4.1.9 Rest of Asia-Pacific

5.4.2 North America

5.4.2.1 United States

5.4.2.2 Canada

5.4.2.3 Mexico

5.4.3 Europe

5.4.3.1 Germany

5.4.3.2 United Kingdom

5.4.3.3 France

5.4.3.4 Italy

5.4.3.5 Spain

5.4.3.6 NORDIC Countries

5.4.3.7 Turkey

5.4.3.8 Russia

5.4.3.9 Rest of Europe

5.4.4 South America

5.4.4.1 Brazil

5.4.4.2 Argentina

5.4.4.3 Colombia

5.4.4.4 Rest of South America

5.4.5 Middle East and Africa

5.4.5.1 Saudi Arabia

5.4.5.2 Qatar

5.4.5.3 United Arab Emirates

5.4.5.4 Nigeria

5.4.5.5 Egypt

5.4.5.6 South Africa

5.4.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Market Share(%)**/Ranking Analysis

6.3 Strategies Adopted by Leading Players

6.4 Company Profiles

6.4.1 AFT Fluorotec Ltd

6.4.2 ASV Multichemie Private Limited

6.4.3 Carl Bechem GmBH

6.4.4 DAIKIN INDUSTRIES Ltd

6.4.5 DuPont

6.4.6 Endura Coatings

6.4.7 Curtiss-Wright Corporation

6.4.8 FUCHS

6.4.9 GGB

6.4.10 IHI HAUZER TECHNO COATING BV

6.4.11 IKV Tribology Ltd

6.4.12 Impreglon UK Limited

6.4.13 Indestructible Paint Limited

6.4.14 Kluber Lubrication (Freudenberg SE)

6.4.15 Micro Surface Corp.

6.4.16 Poeton

6.4.17 PPG Industries Inc.

6.4.18 The Chemours Company

6.4.19 VITRACOAT

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Growing Demand for Low Friction Coating in Healthcare Industry