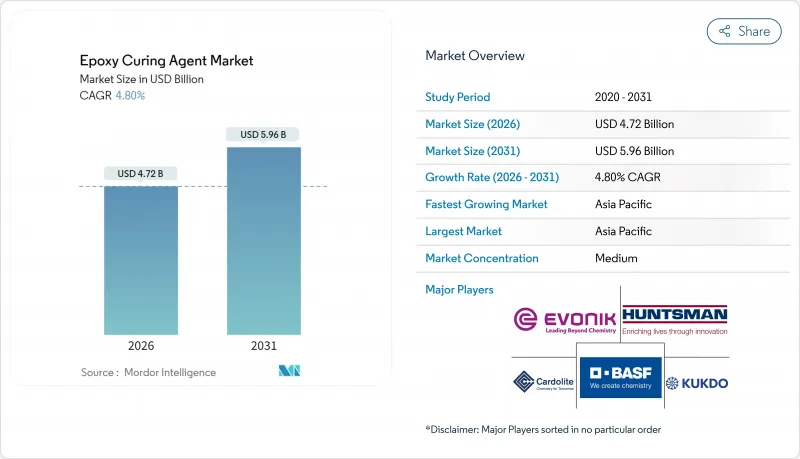

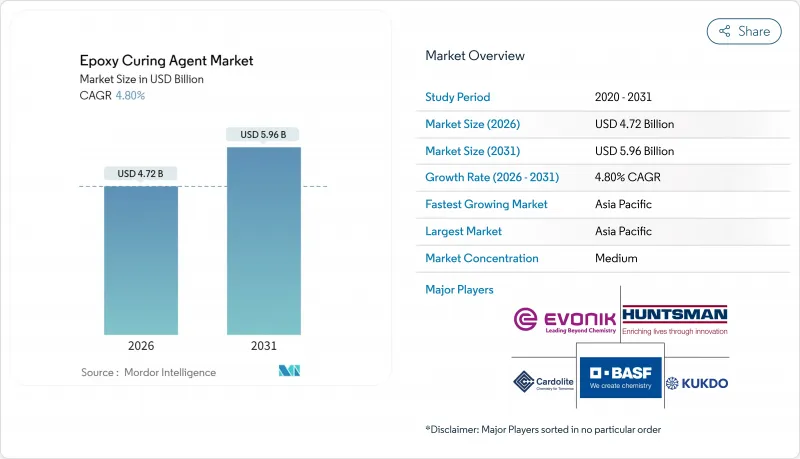

세계의 에폭시 경화제 시장 규모는 2026년 47억 2,000만 달러로 추정되고 있으며, 2025년 45억 달러에서 성장이 예상됩니다. 2031년에는 59억 6,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 4.8%로 성장할 것으로 전망됩니다.

이러한 성장은 아시아태평양의 인프라 정비, 신재생에너지 자산의 꾸준한 도입, 이동성 및 항공우주 분야에서 경량 복합재료 수요 급증에 힘입어 있습니다. 안티 덤핑 관세가 세계 무역의 흐름을 바꾸는 가운데 경쟁 환경은 변화하고 있으며, 유럽과 미국의 생산자는 고이익률 특수 화학제품 분야로 중심을 옮기고 있습니다. 제품혁신은 저휘발성 유기화합물(VOC), 바이오베이스, 고속 경화 시스템 등 생산 사이클의 단축을 가능하게 하는 방향으로 치우칩니다. 한편, 북미 및 유럽에서 공급망의 안보 이니셔티브는 조달 전략의 재구축을 촉구하고 있습니다. 그 결과, 에폭시 경화제 시장은 통합이 진행되고 있지만, 지속가능성에 초점을 맞춘 틈새 신규 참가자가 계속 등장하고 있으며, 경쟁 구도는 복잡해지고 있습니다.

아시아의 인프라 대형 프로젝트는 계속 증가하고 있으며 화학제품, 기계적 충격, 고교통량을 견디는 산업용 바닥재에 대한 엄격한 성능 사양이 탄생하고 있습니다. 중국, 인도, 동남아시아의 공공 부문 지출은 데이터센터 캠퍼스, 지하철 네트워크, 재생에너지 시설에 자금을 투입하고 있으며, 이들 모두에 내구성, 정전기 방지성, 속경화성을 갖춘 코팅이 요구되고 있습니다. 그 결과, 제조 업체는 보다 엄격한 환경 규제를 준수하면서 계약자의 다운타임을 줄이는 저배출 에폭시 시스템을 맞춤화하고 있습니다. 이러한 변화는 전도성 바닥재가 통합된 자산 추적 및 에너지 관리 기술을 가능하게 하는 스마트 빌딩의 개념으로 확산되고 있습니다. 균형 잡힌 비용 성능 패키지를 제공할 수 있는 공급업체는 다년간공급 계약을 획득했으며 에폭시 경화제 시장의 성장 궤도를 강화하고 있습니다.

2024년 세계 풍력발전 설비 용량은 115GW를 돌파했고, 블레이드 제조업체는 수주 잔여에 대응하기 위해 택 타임 단축을 서두르고 있습니다. 대형 로터 설계에는 발열량이 낮고 보이드를 최소화하고 층간 인성을 높이는 경화제가 요구됩니다. BASF의 Baxxodur 시리즈는 최적화된 아민 블렌드가 기계적 강도를 손상시키지 않고 사이클 시간을 단축하는 좋은 예입니다. 유럽의 OEM 제조업체는 온도 감소와 재활용 목표를 설정하고 블레이드 부품 분해를 단순화하는 가역성 화학 기술의 연구 개발을 촉진하고 있습니다. 한편, 중국의 블레이드 공장은 현지 원료와 물류의 우위성을 활용해, 유럽 및 미국 제조업체에 생산 라인 현지화를 촉구하는 것으로, 아시아에 제조 거점을 가지는 에폭시 경화제 시장 참가 기업에 대한 지역 수요를 확대하고 있습니다.

미국 국가 에어로졸 페인트 규칙의 개정과 남해안 대기질 관리지구(AQMD)의 개정안에 의해 허용 VOC 임계치가 크게 인하되고, 제조업자는 수성, 고고형분, 무용제계 화학 기술로의 이행을 강요받고 있습니다. 규제 대응으로 환경 친화적인 대체품 시장 기회는 확대되는 반면, 특히 성능을 저해할 수 없는 분야에서는 연구 개발비 및 인증 비용이 증가하고 있습니다. 급속 경화형 바이오 대체품이 개발 중이지만, 스케일업 장벽에 직면하고 있으며, 이는 단기적인 공급 가능성을 제한하고 에폭시 경화제 시장 전체의 성장 가속을 방해할 수 있습니다.

아민계는 2025년 매출액의 41.12%를 차지해, 대부분의 복합재, 도료, 접착제 시스템의 기간 화학제품으로서 지위를 확고한 것으로 하고 있습니다. 이 카테고리 내에서는 지방족 및 지환식 아민이 내자외선성을 제공하고 폴리에테르아민은 선박용 보호도료 등 유연성이 요구되는 환경에서 뛰어난 성능을 발휘합니다. 무수물은 180℃에서의 사용이 일상적인 고온 전기 절연재 및 자동차 엔진 룸 부품에서 여전히 중요한 역할을 합니다. 페놀알카민은 틈새 분야이지만, 습윤 환경이나 저온 작업 현장에서의 급속 경화를 실현해, 전천후형의 생산성을 추구하는 시공업자로부터 평가되는 가치 제안이 되고 있습니다. 이 부문의 적응성이 높은 성능 프로파일은 지속가능성의 동향이 경쟁 화학물질을 초래하는 가운데 에폭시 경화제 시장의 핵심임을 보장합니다.

아민계가 주류인 한편, 경쟁 압력은 계속 존재하고 있습니다. 폴리아미드 공급자는 바이오 유래 이량체산 공정을 강조하고 탄소 삭감 우위성을 주장. 한편, 무수물 제조업체는 뛰어난 내열 사이클 성능을 소구하고 있습니다. 특수 제조업체는 경화 지연, 경화 속도, 기계적 성능의 밸런스를 도모하기 위해, 하이브리드형 아민 무수물 패키지의 실험을 진행하고 있습니다. 예측기간 중 아민화학 분야에서의 중점적인 연구개발은 경화 사이클을 연장하지 않고 인성을 향상시키는 잠재성 촉매나 나노필러의 통합을 목표로 하고 있습니다. 이러한 꾸준한 개선의 지속으로, 본 부문은 에폭시 경화제 시장 전체를 계속 견인하는 입장을 확립하고 있습니다.

아시아태평양은 2025년에 35.12%의 점유율을 차지했고, 공공 인프라 투자, 재생에너지에 대한 노력, 전자기기 제조의 지역 집중을 배경으로 CAGR 5.66%로 확대하고 있습니다. 중국의 풍력 터빈 블레이드 공장과 인도의 반도체 조립 클러스터는 엄청난 양의 아민 시스템을 흡수합니다. 지역 제조업체는 에피클로로히드린과 벤질아민 원료에 대한 지리적 근접성을 활용하여 물류 비용과 리드타임을 절감하고 있습니다. 지속가능성에 대한 규제는 강화되고 있지만, 비용 경쟁력은 여전히 가장 중요한 과제이며, 에폭시 경화제 시장에서 지역 통합 공급망의 필요성을 뒷받침하고 있습니다.

북미는 점유율에서 뒤쳐지지만, 리쇼어링 움직임과 항공우주 복합재 분야의 주도적 입장으로부터 혜택을 받고 있습니다. 2025년 미국 국제무역위원회가 정식으로 결정한 아시아산 에폭시 수입품에 대한 반덤핑 관세는 국내 설비 가동률을 높여 특수 등급에 대한 투자를 촉진합니다. 미국과 멕시코의 전기자동차(EV) 배터리 공장의 확장은 고고형분 접착제 수요를 자극하고, 대서양 연안 지역에서 해상 풍력 발전 설비의 증설은 블레이드 등급 경화제의 새로운 소비층을 만들어 냅니다.

유럽은 급등하는 에너지 비용과 아시아의 치열한 경쟁에 직면하여 기업은 범용품의 생산 합리화와 고부가가치 틈새 분야에 주력을 강요하고 있습니다. West Lake의 네덜란드 자산 손상 처리는 이러한 재조정을 상징합니다. 그러나 자동차 복합재료와 재생가능 풍력 블레이드의 연구개발에 있어서 유럽의 리더십은 차세대 화학물질에 대한 선택적 수요를 지원하고 있습니다. 순환형 경제에 대한 규제 중시가 바이오 베이스 및 저 VOC 경화 시스템의 채용을 가속화해, 지역의 에폭시 경화제 시장에 혁신 주도의 길을 개척하고 있습니다.

Epoxy Curing Agent Market size in 2026 is estimated at USD 4.72 Billion, growing from 2025 value of USD 4.5 Billion with 2031 projections showing USD 5.96 Billion, growing at 4.8% CAGR over 2026-2031.

This growth rests on Asia-Pacific infrastructure upgrades, the steady rollout of renewable-energy assets, and surging demand for lightweight composites in mobility and aerospace. Competitive dynamics are shifting as antidumping duties alter global trade flows, prompting Western producers to pivot toward high-margin specialty chemistries. Product innovation is skewing toward low-Volatile Organic Compound (VOC), bio-based, and fast-cure systems that enable shorter production cycles, while supply-chain security initiatives in North America and Europe are re-ordering sourcing strategies. As a result, the epoxy curing agents market is consolidating, yet niche entrants focusing on sustainability continue to emerge, adding complexity to the competitive landscape.

Asian infrastructure megaprojects continue multiplying, spawning stringent performance specifications for industrial floors that withstand chemicals, mechanical shock, and heavy traffic. Public-sector spending across China, India, and Southeast Asia is channeling funds into data-center campuses, metro rail networks, and renewable-power facilities, all requiring durable, anti-static, and rapid-cure coatings. Consequently, formulators are tailoring low-emission epoxy systems that lower downtime for contractors while complying with tougher environmental mandates . The shift extends to smart-building concepts, where conductive floors enable integrated asset-tracking and energy-management technologies. Suppliers able to deliver balanced cost-performance packages are winning multi-year supply contracts, reinforcing the growth trajectory of the epoxy curing agents market.

Global wind-energy capacity additions crossed the 115 GW mark in 2024, and blade makers are chasing tighter takt times to meet order backlogs. Large-rotor designs demand curing agents that generate low exotherms, minimize voids, and elevate interlaminar toughness. BASF's Baxxodur range illustrates how optimized amine blends reduce cycle times without sacrificing mechanical integrity. European original equipment manufacturers (OEMs) have set temperature-reduction and recyclability targets, spurring research and development (R&D) into reversible chemistries that simplify blade component disassembly. Meanwhile, China's blade factories leverage local feedstock and logistics advantages, nudging Western players to localize production lines, thereby amplifying regional demand for epoxy curing agents market participants with Asian manufacturing footprints.

Revisions to the U.S. National Aerosol Coatings Rule and proposed South Coast AQMD (Air Quality Management District) updates are slashing allowable VOC thresholds, forcing formulators to migrate toward water-borne, high-solids, or solvent-free chemistries . While compliance widens the addressable market for greener alternatives, it raises R&D and qualification costs, especially where performance cannot be compromised. Rapid-cure, bio-based alternatives are in development but face scale-up hurdles that could constrain near-term supply availability and hamper overall epoxy curing agents market acceleration.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Amines controlled 41.12% of 2025 revenue, cementing their role as the backbone chemistry for most composite, coating, and adhesive systems. Within the category, aliphatic and cycloaliphatic versions deliver UV resistance, while polyetheramines excel in flexibility-demanding environments such as protective marine coatings. Anhydrides maintain relevance in high-temperature electrical insulation and under-hood automotive components where 180°C service is routine. Phenalkamines, though niche, unlock rapid cure in humid or low-temperature jobsites, a value proposition gaining recognition among contractors pursuing all-weather productivity. The segment's adaptable performance profile collectively ensures it stays at the core of the epoxy curing agents market even as sustainability trends invite competing chemistries.

Despite amines' dominance, competitive tension persists. Polyamide suppliers stress bio-sourced dimer-acid routes to claim a carbon-reduction edge, while anhydride producers tout superior heat-cycling endurance. Specialty players experiment with hybrid amine-anhydride packages to balance latency, cure speed, and mechanical performance. Over the forecast horizon, targeted R&D in amine chemistry aims to integrate latent catalysts and nano-fillers that elevate toughness without extending cure cycles. This steady pipeline of upgrades positions the segment to keep fueling the broader epoxy curing agents market.

The Epoxy Curing Agents Market Report is Segmented by Type (Amines, Polyamides, Anhydrides, and Other Types (Phenalkamines, Amidoamines, Etc. )), Application (Paints and Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 35.12% share in 2025 and is expanding at a 5.66% CAGR on the back of public infrastructure outlays, renewable-energy commitments, and electronics manufacturing gravitation toward the region. China's wind-turbine blade factories and India's semiconductor-assembly clusters absorb vast volumes of amine-based systems. Regional producers leverage proximity to epichlorohydrin and benzylamine feedstocks, reducing logistics costs and lead times. Sustainability regulations are tightening, but cost competitiveness remains paramount, reinforcing the need for locally integrated supply chains in the epoxy curing agents market.

North America trails in share but benefits from reshoring missions and aerospace composites leadership. Antidumping duties on Asian epoxy imports, formalized by the United States International Trade Commission in 2025, raise domestic capacity utilization and spur investment in specialty grades. Electric Vehicle (EV) battery-plant expansions in the United States and Mexico stimulate high-solids adhesive demand, while offshore-wind buildouts along the Atlantic corridor introduce a new consumption stream for blade-grade curing agents.

Europe confronts high energy costs and fierce Asian competition, forcing companies to rationalize commodity output and double down on high-value niches. Westlake's impairment of Dutch assets exemplifies this recalibration. Yet Europe's leadership in automotive composites and recyclable wind-blade R&D sustains selective demand for next-generation chemistries. Regulatory emphasis on circularity is accelerating adoption of bio-based and low-VOC curing systems, carving an innovation-led path for the regional epoxy curing agents market.